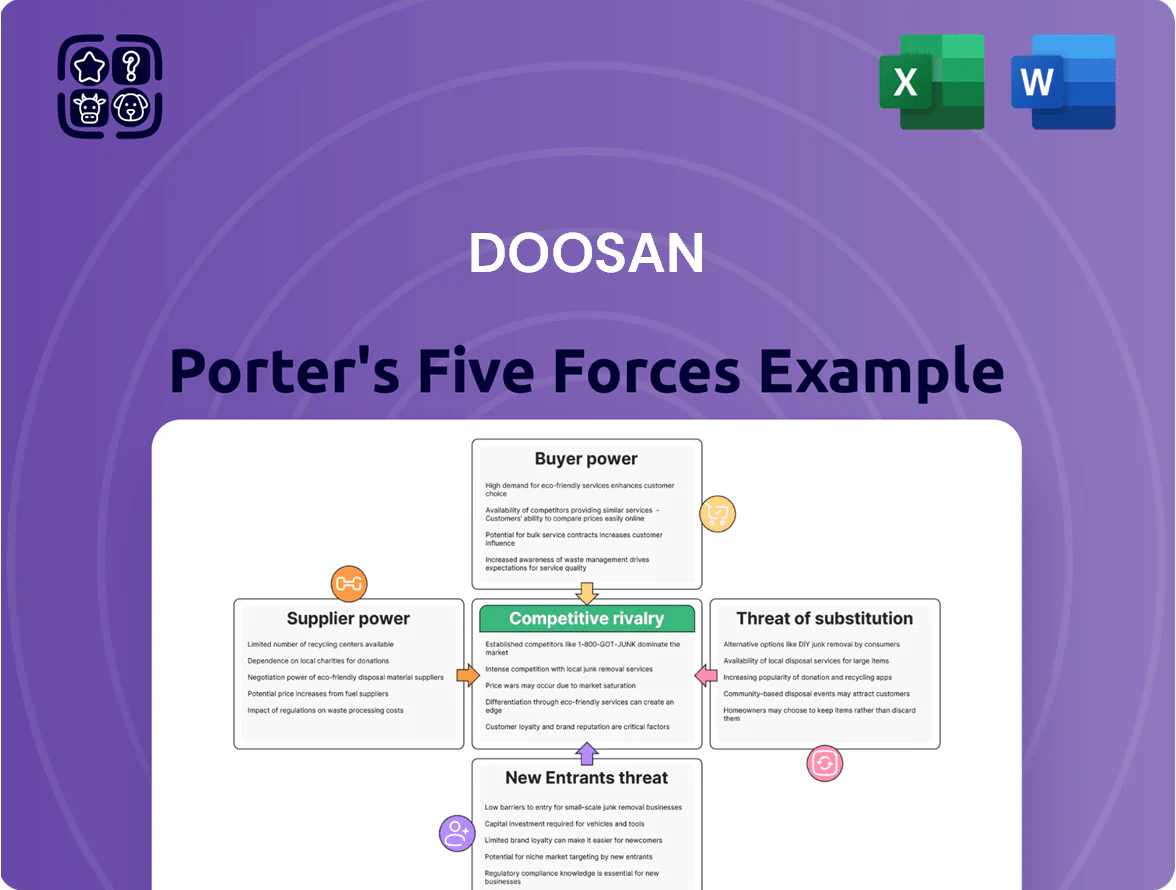

Doosan Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Doosan faces moderate buyer power and high supplier complexity from specialized component vendors, while rivalry intensifies in heavy industries and energy markets due to consolidation and price competition.

Barriers to entry are substantial but technology shifts and green energy trends raise the threat of innovative challengers and substitutes.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Doosan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Semiconductor and AI Component Sourcing

Doosan’s push into AI-driven robotics raises dependence on advanced semiconductors from a few suppliers; top chipmakers (TSMC, NVIDIA, Intel) controlled ~70% of high-performance AI accelerator capacity in 2024, giving them pricing and delivery leverage over Doosan’s new product lines.

Because 2023–25 global wafer fab utilization hit ~85–90%, any semiconductor disruption can delay Doosan production and raise unit costs by an estimated 6–12% per device, squeezing margins and project timelines.

Raw Material Volatility for Heavy Industry

Doosan’s heavy-equipment output needs large volumes of steel, copper and specialty alloys, making it a price-taker in global commodity markets; steel prices rose ~15% in 2024 and copper averaged $9,200/tonne, amplifying supplier leverage.

To cut exposure, Doosan uses multi‑year procurement deals and metal hedges; in 2024 ~40% of its steel needs were under long‑term contracts, which trimmed input-cost volatility by an estimated 6–8%.

Proprietary Technology Partnerships

Doosan’s partnerships with niche SMR and hydrogen tech firms and universities give suppliers strong leverage because their patents and prototyping know-how are scarce; for example, 2024 deal data show specialized IP partners can command 15–25% higher margins on licensing than general suppliers.

Energy Costs for Manufacturing Operations

Doosan’s factories are energy intensive, tying margins to utility contracts and world energy prices; a 30% rise in electricity or gas can cut heavy-equipment EBITDA by several percentage points—Doosan Enerbility reported energy costs at roughly 8–12% of COGS in 2024.

Volatile LNG and power markets — Korea’s wholesale power rose ~18% in 2023–24 — and higher carbon-compliant tariffs increase supplier pressure as grids green, raising passthrough risk and capex for on-site decarbonization.

- Energy = 8–12% of COGS (2024)

- Korean wholesale power +18% (2023–24)

- LNG price swings drive margin volatility

- Carbon-compliant energy raises supplier-side costs

Logistics and Global Shipping Constraints

Doosan’s heavy reliance on maritime shipping for oversized equipment exposes it to carrier pricing power after global liner consolidation; the top 10 container carriers controlled about 90% of capacity in 2024, pushing spot freight rates up 35% year-over-year on key Asia-Europe trades in 2024.

That concentration makes international delivery cost a volatile input for Doosan’s margins, so the firm must drive logistics savings via route optimization, longer-term contracts, and multimodal mixes to stabilize COGS.

- Top 10 carriers ~90% capacity (2024)

- Spot rates Asia-Europe +35% YoY (2024)

- Mitigants: long-term contracts, route/mode mix

Supplier squeeze: AI chips, fabs, steel and carriers dominate input costs and capacity

Suppliers wield high leverage: top AI-chipmakers held ~70% of high‑perf accelerator capacity (2024), wafer fab utilization ~85–90% (2023–25), steel up ~15% (2024), energy 8–12% of COGS (2024), top‑10 carriers ~90% capacity; Doosan uses 40% long‑term steel contracts and hedges to cut input volatility ~6–8%.

| Metric | 2024 |

|---|---|

| AI chip share | ~70% |

| Wafer utilization | 85–90% |

| Steel price change | +15% |

| Energy % of COGS | 8–12% |

| Top carriers share | ~90% |

What is included in the product

Tailored Porter's Five Forces analysis for Doosan that uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats to its market share, with strategic commentary and editable Word-ready format for investor or internal use.

Concise five-forces snapshot tailored to Doosan—instantly highlight competitive pressures and relief strategies for boardroom decisions.

Customers Bargaining Power

Concentration of Government and Utility Buyers

In power generation, Doosan’s main buyers are national governments and state-owned utilities, which together accounted for roughly 60% of global large-scale plant procurement in 2024, giving them outsized bargaining power.

These buyers control multi-billion-dollar contracts—typical combined equipment and service deals exceed $500m—so they can set strict technical specs and payment terms.

With a shortlist of global suppliers, utilities extract deep price concessions and insist on 15–25 year service agreements, squeezing margins and shifting product risk onto Doosan.

Price Sensitivity in Construction Equipment

Doosan Bobcat serves many construction and landscaping firms that are highly price-sensitive; in 2024 US small contractor equipment purchases fell ~8% year-over-year as interest rates rose, so buyers delay or downsize orders.

High rates push customers toward competitors with better financing—commercial loan spreads climbed ~150 bps in 2023–24—raising churn risk despite Doosan brand loyalty.

Loyalty holds if total cost of ownership and resale value beat rivals; Doosan’s 3-year resale premium of ~4% versus peers can defend sales but is often tested.

Switching Costs in Energy Infrastructure

Once a utility adopts Doosan’s nuclear or gas turbine tech, switching costs are huge—assets run 30–60 years for nuclear and 20–40 years for combined-cycle turbines—so Doosan gains aftermarket leverage for MRO (maintenance, repair, overhaul), often capturing 20–35% higher margin on service contracts versus equipment sales.

Still, during initial bids customers push hard: global tender win rates fell to 12% in 2024 for large EPCs, so utilities extract better payment terms, warranty limits, and price concessions before asset lock-in.

Demand for Sustainable and Green Solutions

Institutional investors and corporate clients now push for carbon-neutral solutions, increasing buyer leverage; 68% of global asset managers (2024 BCG) score suppliers on ESG, raising procurement barriers for non-compliant vendors.

Customers demand hydrogen-ready turbines and electric construction machinery as procurement prerequisites; Doosan risks lost contracts if product roadmap lags—IEA 2025 projects hydrogen power capacity growth of 20%+/yr in key markets.

Doosan must align R&D and capex to ESG specs to stay relevant; a 2024 survey found 54% of industrial buyers would pay a premium for low-carbon equipment.

- 68% asset managers use ESG scores (BCG 2024)

- Hydrogen power capacity +20%/yr (IEA 2025)

- 54% buyers pay premium for low-carbon gear (2024 survey)

Growth of the Rental Market Segment

- ~35% of compact-equipment revenue from rentals (2024)

- Typical fleet discounts: 10–20%

- Rental firms demand longer service intervals and rental-ready features

- Bulk buying shifts bargaining power from contractors to rental firms

Buyers Dominate: Utilities & Rentals Drive Specs, Discounts and Margin Shifts

Buyers hold high power: governments/utilities (~60% large-plant procurement in 2024) drive specs and multi-$100m terms; rental firms supply ~35% of Bobcat compact-equipment revenue and secure 10–20% fleet discounts, shifting leverage; service contracts yield 20–35% higher margins for Doosan post-switching, but tender win rates fell to 12% in 2024, increasing upfront concessions.

| Metric | 2024/25 |

|---|---|

| Utilities share | ~60% |

| Bobcat rental rev | ~35% |

| Fleet discounts | 10–20% |

| Win rate large EPC | 12% |

Same Document Delivered

Doosan Porter's Five Forces Analysis

This preview shows the exact Doosan Porter’s Five Forces analysis you'll receive immediately after purchase—no samples, no placeholders, fully formatted for instant use.

The document presented here is the complete, professional deliverable covering competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications—you’ll download this same file after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Doosan faces moderate buyer power and high supplier complexity from specialized component vendors, while rivalry intensifies in heavy industries and energy markets due to consolidation and price competition.

Barriers to entry are substantial but technology shifts and green energy trends raise the threat of innovative challengers and substitutes.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Doosan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Semiconductor and AI Component Sourcing

Doosan’s push into AI-driven robotics raises dependence on advanced semiconductors from a few suppliers; top chipmakers (TSMC, NVIDIA, Intel) controlled ~70% of high-performance AI accelerator capacity in 2024, giving them pricing and delivery leverage over Doosan’s new product lines.

Because 2023–25 global wafer fab utilization hit ~85–90%, any semiconductor disruption can delay Doosan production and raise unit costs by an estimated 6–12% per device, squeezing margins and project timelines.

Raw Material Volatility for Heavy Industry

Doosan’s heavy-equipment output needs large volumes of steel, copper and specialty alloys, making it a price-taker in global commodity markets; steel prices rose ~15% in 2024 and copper averaged $9,200/tonne, amplifying supplier leverage.

To cut exposure, Doosan uses multi‑year procurement deals and metal hedges; in 2024 ~40% of its steel needs were under long‑term contracts, which trimmed input-cost volatility by an estimated 6–8%.

Proprietary Technology Partnerships

Doosan’s partnerships with niche SMR and hydrogen tech firms and universities give suppliers strong leverage because their patents and prototyping know-how are scarce; for example, 2024 deal data show specialized IP partners can command 15–25% higher margins on licensing than general suppliers.

Energy Costs for Manufacturing Operations

Doosan’s factories are energy intensive, tying margins to utility contracts and world energy prices; a 30% rise in electricity or gas can cut heavy-equipment EBITDA by several percentage points—Doosan Enerbility reported energy costs at roughly 8–12% of COGS in 2024.

Volatile LNG and power markets — Korea’s wholesale power rose ~18% in 2023–24 — and higher carbon-compliant tariffs increase supplier pressure as grids green, raising passthrough risk and capex for on-site decarbonization.

- Energy = 8–12% of COGS (2024)

- Korean wholesale power +18% (2023–24)

- LNG price swings drive margin volatility

- Carbon-compliant energy raises supplier-side costs

Logistics and Global Shipping Constraints

Doosan’s heavy reliance on maritime shipping for oversized equipment exposes it to carrier pricing power after global liner consolidation; the top 10 container carriers controlled about 90% of capacity in 2024, pushing spot freight rates up 35% year-over-year on key Asia-Europe trades in 2024.

That concentration makes international delivery cost a volatile input for Doosan’s margins, so the firm must drive logistics savings via route optimization, longer-term contracts, and multimodal mixes to stabilize COGS.

- Top 10 carriers ~90% capacity (2024)

- Spot rates Asia-Europe +35% YoY (2024)

- Mitigants: long-term contracts, route/mode mix

Supplier squeeze: AI chips, fabs, steel and carriers dominate input costs and capacity

Suppliers wield high leverage: top AI-chipmakers held ~70% of high‑perf accelerator capacity (2024), wafer fab utilization ~85–90% (2023–25), steel up ~15% (2024), energy 8–12% of COGS (2024), top‑10 carriers ~90% capacity; Doosan uses 40% long‑term steel contracts and hedges to cut input volatility ~6–8%.

| Metric | 2024 |

|---|---|

| AI chip share | ~70% |

| Wafer utilization | 85–90% |

| Steel price change | +15% |

| Energy % of COGS | 8–12% |

| Top carriers share | ~90% |

What is included in the product

Tailored Porter's Five Forces analysis for Doosan that uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats to its market share, with strategic commentary and editable Word-ready format for investor or internal use.

Concise five-forces snapshot tailored to Doosan—instantly highlight competitive pressures and relief strategies for boardroom decisions.

Customers Bargaining Power

Concentration of Government and Utility Buyers

In power generation, Doosan’s main buyers are national governments and state-owned utilities, which together accounted for roughly 60% of global large-scale plant procurement in 2024, giving them outsized bargaining power.

These buyers control multi-billion-dollar contracts—typical combined equipment and service deals exceed $500m—so they can set strict technical specs and payment terms.

With a shortlist of global suppliers, utilities extract deep price concessions and insist on 15–25 year service agreements, squeezing margins and shifting product risk onto Doosan.

Price Sensitivity in Construction Equipment

Doosan Bobcat serves many construction and landscaping firms that are highly price-sensitive; in 2024 US small contractor equipment purchases fell ~8% year-over-year as interest rates rose, so buyers delay or downsize orders.

High rates push customers toward competitors with better financing—commercial loan spreads climbed ~150 bps in 2023–24—raising churn risk despite Doosan brand loyalty.

Loyalty holds if total cost of ownership and resale value beat rivals; Doosan’s 3-year resale premium of ~4% versus peers can defend sales but is often tested.

Switching Costs in Energy Infrastructure

Once a utility adopts Doosan’s nuclear or gas turbine tech, switching costs are huge—assets run 30–60 years for nuclear and 20–40 years for combined-cycle turbines—so Doosan gains aftermarket leverage for MRO (maintenance, repair, overhaul), often capturing 20–35% higher margin on service contracts versus equipment sales.

Still, during initial bids customers push hard: global tender win rates fell to 12% in 2024 for large EPCs, so utilities extract better payment terms, warranty limits, and price concessions before asset lock-in.

Demand for Sustainable and Green Solutions

Institutional investors and corporate clients now push for carbon-neutral solutions, increasing buyer leverage; 68% of global asset managers (2024 BCG) score suppliers on ESG, raising procurement barriers for non-compliant vendors.

Customers demand hydrogen-ready turbines and electric construction machinery as procurement prerequisites; Doosan risks lost contracts if product roadmap lags—IEA 2025 projects hydrogen power capacity growth of 20%+/yr in key markets.

Doosan must align R&D and capex to ESG specs to stay relevant; a 2024 survey found 54% of industrial buyers would pay a premium for low-carbon equipment.

- 68% asset managers use ESG scores (BCG 2024)

- Hydrogen power capacity +20%/yr (IEA 2025)

- 54% buyers pay premium for low-carbon gear (2024 survey)

Growth of the Rental Market Segment

- ~35% of compact-equipment revenue from rentals (2024)

- Typical fleet discounts: 10–20%

- Rental firms demand longer service intervals and rental-ready features

- Bulk buying shifts bargaining power from contractors to rental firms

Buyers Dominate: Utilities & Rentals Drive Specs, Discounts and Margin Shifts

Buyers hold high power: governments/utilities (~60% large-plant procurement in 2024) drive specs and multi-$100m terms; rental firms supply ~35% of Bobcat compact-equipment revenue and secure 10–20% fleet discounts, shifting leverage; service contracts yield 20–35% higher margins for Doosan post-switching, but tender win rates fell to 12% in 2024, increasing upfront concessions.

| Metric | 2024/25 |

|---|---|

| Utilities share | ~60% |

| Bobcat rental rev | ~35% |

| Fleet discounts | 10–20% |

| Win rate large EPC | 12% |

Same Document Delivered

Doosan Porter's Five Forces Analysis

This preview shows the exact Doosan Porter’s Five Forces analysis you'll receive immediately after purchase—no samples, no placeholders, fully formatted for instant use.

The document presented here is the complete, professional deliverable covering competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications—you’ll download this same file after payment.