dotDigital Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

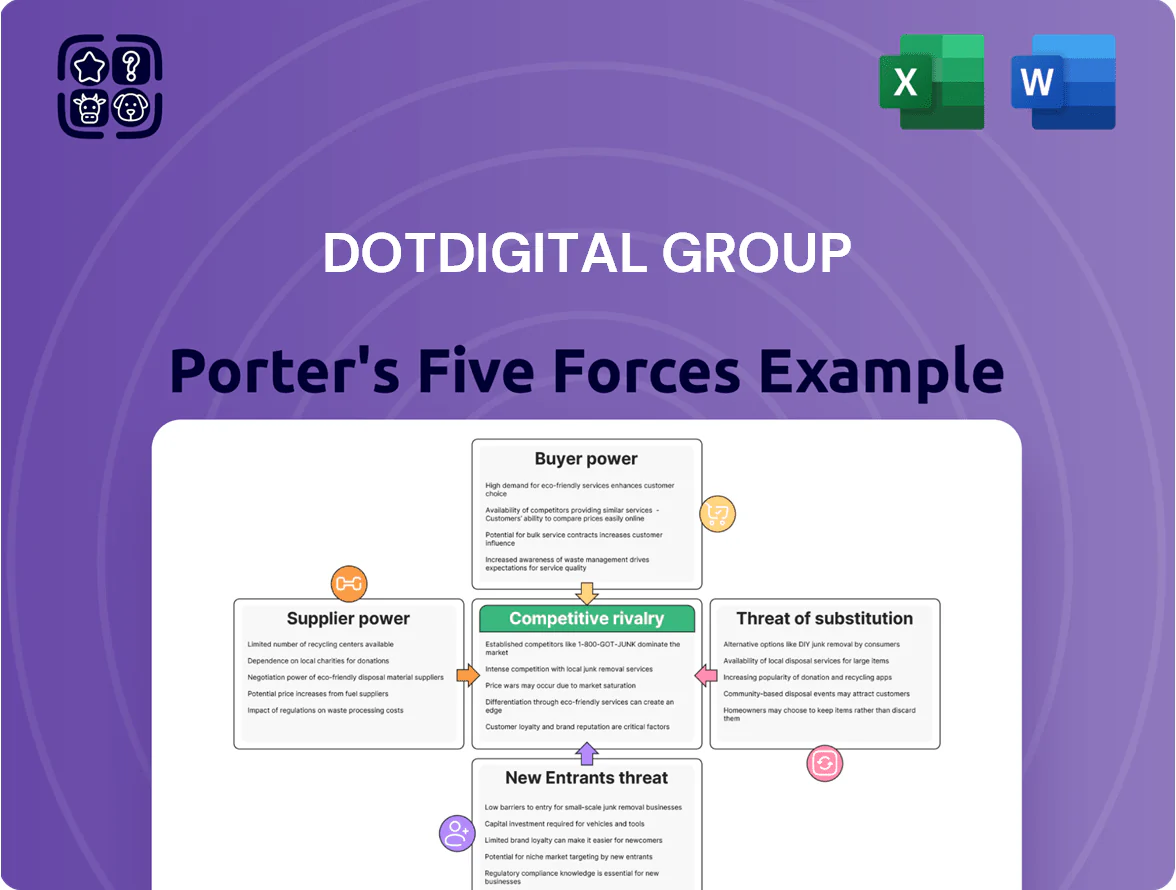

dotDigital operates in a competitive martech niche where customer switching costs and platform integration raise buyer power, while low hardware needs and modular SaaS offerings keep supplier power moderate and threat of substitutes manageable.

Barriers to entry are moderate—brand, data relationships, and compliance favor incumbents, but cloud-native rivals can scale quickly, intensifying rivalry among existing players.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore dotDigital Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Cloud Infrastructure Providers

Dotdigital depends on global cloud providers like Microsoft Azure and AWS for its SaaS stack; in 2025 AWS and Azure together held roughly 59% of global cloud IaaS/PaaS market, limiting alternatives.

These providers offer unique global scale, SOC/ISO security certifications, and >99.9% uptime, so switching costs and migration risk are high.

Any price hike or contract change—AWS raised key service fees in 2024 for bandwidth and compute—would lift Dotdigital’s COGS and compress margins unless offset by price increases or efficiency gains.

Dependency on Telecom and SMS Gateways

Dotdigital relies on telecom carriers and SMS/WhatsApp gateway providers for message delivery; in 2024 global A2P SMS revenue hit $50.5bn, showing carriers' pricing power over a key channel.

Multiple gateways exist, but regional carrier monopolies—e.g., parts of Africa and Southeast Asia where 2–3 firms control 70–90% of traffic—limit Dotdigital’s bargaining on rates and SLAs.

That dependency raises costs: average A2P SMS prices vary $0.005–$0.10 per message by region, squeezing margins on campaign-heavy clients.

Scarcity of Specialized AI and Engineering Talent

The development of advanced marketing automation features requires top software engineers and AI data scientists, a talent pool whose demand grew 35% globally from 2020–2024 and remained tight in late 2025 with vacancy rates near 4.1% in the UK tech sector (ONS). This scarcity gives suppliers of talent strong bargaining power, pushing median AI engineer pay in the UK to ~£90k–£130k and total hiring cost multipliers of 1.6x. Dotdigital must offer competitive pay, equity, and training to retain staff and protect its product roadmap.

Third-party Software and API Integrations

Dotdigital’s integrations with Salesforce, Adobe Commerce and Shopify (among others) are core to its value—Salesforce’s AppExchange and Shopify’s 2024 merchant base of 4.8M give Dotdigital reach but create supplier dependency.

If API limits, fee changes, or deprecation occur (Salesforce raised some partner fees in 2023), Dotdigital’s functionality and revenue could be hit; platform owners therefore hold meaningful bargaining power.

- Dependency on major CRMs/platforms

- Shopify ~4.8M merchants (2024)

- Salesforce partner fee shifts in 2023

- API policy changes can reduce feature set/revenue

Data Compliance and Cybersecurity Service Providers

Dotdigital relies heavily on specialized legal and cybersecurity firms to meet EU GDPR and US state privacy rules; recent fines show stakes—GDPR penalties reached €1.3 billion in 2023, so compliance spend is nontrivial.

These suppliers deliver audits, ISO/IEC 27001 certifications, and advanced tooling that enable Dotdigital to serve regulated markets; a single breach can cost tens of millions and spike churn.

Because switching costs, expertise scarcity, and high breach penalties raise supplier leverage, providers command premium fees and favorable contract terms.

- 2023 GDPR fines: €1.3 billion

- ISO/IEC 27001 often required

- Breaches can cost tens of millions

- High switching costs, scarce expertise

Supplier squeeze: cloud, carriers, talent & compliance threaten Dotdigital margins

Suppliers exert medium–high power: cloud giants (AWS/Azure ~59% IaaS/PaaS, 2025) and carriers (global A2P SMS revenue $50.5bn, 2024) raise costs and switching risk; talent scarcity (UK AI engineer pay ~£90k–£130k, vacancy ~4.1%, 2024) and compliance providers (GDPR fines €1.3bn, 2023) further strengthen suppliers, squeezing margins unless Dotdigital passes costs to clients.

| Supplier | Key stat | Impact |

|---|---|---|

| Cloud (AWS/Azure) | ~59% IaaS/PaaS (2025) | High switching cost |

| Carriers/SMS | $50.5bn A2P (2024) | Price variability $0.005–$0.10/msg |

| Talent | UK AI pay £90k–£130k (2024) | Higher OPEX |

| Compliance | GDPR fines €1.3bn (2023) | Mandatory spend |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to dotDigital Group, detailing competitive forces, supplier/buyer power, substitutes, and barriers to entry with strategic insights and industry context for use in investor materials and strategy decks.

A concise Porter's Five Forces snapshot for dotDigital—one-sheet clarity to speed strategic decisions and highlight competitive pain points.

Customers Bargaining Power

Low Switching Costs for Small Businesses

In the lower market, SMEs can typically export contact lists via CSV/JSON and migrate platforms in days, so switching costs are low; industry surveys show 42% of SMBs cite easy data export as a top reason to switch (2024, SaaS Insights).

Because rivals often undercut on price, dotDigital must keep pricing competitive and uptime/service quality high—SMB churn rises ~3–5% if support SLA slips beyond 24 hours (2023 CRM Benchmarks).

High Volume of Competitor Options

The marketing-automation market had over 400 vendors by 2024, from freemium tools under $50/month to enterprise suites >$100k/year, and dotDigital faces intense choice pressure; 72% of B2B buyers used peer reviews and comparison sites in 2024, so customers regularly cite competitor quotes to push prices down and demand richer SLAs, raising buyer bargaining power.

Demand for Measurable Return on Investment

Modern marketing teams demand measurable ROI, pushing vendors like dotDigital to add advanced attribution and reporting; 72% of CMOs in 2024 said ROI measurement drives martech spend decisions, so buyers press for performance pricing or steep discounts when outcomes are unclear. This bargaining power forces dotDigital to include more features at existing price points or risk churn—average contract lengths fell to 18 months in 2024 for vendors lacking clear ROI proof.

Sophistication of Enterprise Procurement Teams

Larger corporate clients use professional procurement teams that routinely secure multi-year contracts and volume discounts, pressuring dotDigital to match rates that can shave 10–25% off list pricing versus SMB deals.

These buyers demand custom SLAs, dedicated support, and bespoke features; delivering that can raise implementation margins by 5–15% but also lengthen delivery by months.

The ability to switch to HubSpot, Braze, or Salesforce Marketing Cloud gives customers leverage to push favorable termination and rebate terms; enterprise churn risk rises if renewal pricing exceeds 8–12% YoY.

- Procurement skill: lowers price 10–25%

- Custom SLAs raise delivery cost 5–15%

- Switching to HubSpot/Braze increases contract concessions

- Renewal sensitivity: >8–12% YoY price hikes risk churn

Influence of Agency Partners

Marketing agencies that manage stacks for many clients can flip platform choice at scale; a single agency switch could cost dotDigital Group millions — agencies often oversee portfolios generating 10–30% of vendor ARR per agency in enterprise channels (example: 2024 agency-led deals represented ~22% of mid-market SaaS procurement).

Because agencies control concentrated revenue blocks, they can demand discounts, white-labeling, or exclusive features, raising customer acquisition costs and compressing margins; losing one or two agency partners could reduce gross retention materially.

- Agency-led revenue concentration: ~22% of mid-market SaaS deals (2024)

- Risk: single-agency switch can drop clustered ARR by 10–30%

- Bargaining levers: preferential pricing, white-labeling, integration support

- Mitigation: diversify partner base, embed technical lock-in, partner SLAs

Buyers Rule: 400+ Vendors, Tough Discounts, ROI Demands — Contracts Shrink to 18 Months

Buyers hold high bargaining power: low switching costs (CSV/JSON exports), 400+ vendors (2024), and heavy use of reviews (72%); SMB churn rises 3–5% if support slips beyond 24h. Procurement and agencies extract 10–25% discounts; enterprise renewals fail if YoY price hikes exceed 8–12%. Vendors must add features/ROI proof or face shorter contracts (avg 18 months, 2024).

| Metric | Value (2024) |

|---|---|

| Vendors | 400+ |

| Review use | 72% |

| SMB churn ↑ if SLA>24h | 3–5% |

| Procurement discount | 10–25% |

| Avg contract (no ROI) | 18 months |

What You See Is What You Get

dotDigital Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of dotDigital Group that you’ll receive instantly after purchase—fully formatted, professionally written, and ready to download with no placeholders or mockups.

The document displayed here is the actual deliverable: a complete, ready-to-use strategic assessment covering competitive rivalry, supplier and buyer power, threats of substitutes and entrants, and implications for strategy and valuation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

dotDigital operates in a competitive martech niche where customer switching costs and platform integration raise buyer power, while low hardware needs and modular SaaS offerings keep supplier power moderate and threat of substitutes manageable.

Barriers to entry are moderate—brand, data relationships, and compliance favor incumbents, but cloud-native rivals can scale quickly, intensifying rivalry among existing players.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore dotDigital Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Cloud Infrastructure Providers

Dotdigital depends on global cloud providers like Microsoft Azure and AWS for its SaaS stack; in 2025 AWS and Azure together held roughly 59% of global cloud IaaS/PaaS market, limiting alternatives.

These providers offer unique global scale, SOC/ISO security certifications, and >99.9% uptime, so switching costs and migration risk are high.

Any price hike or contract change—AWS raised key service fees in 2024 for bandwidth and compute—would lift Dotdigital’s COGS and compress margins unless offset by price increases or efficiency gains.

Dependency on Telecom and SMS Gateways

Dotdigital relies on telecom carriers and SMS/WhatsApp gateway providers for message delivery; in 2024 global A2P SMS revenue hit $50.5bn, showing carriers' pricing power over a key channel.

Multiple gateways exist, but regional carrier monopolies—e.g., parts of Africa and Southeast Asia where 2–3 firms control 70–90% of traffic—limit Dotdigital’s bargaining on rates and SLAs.

That dependency raises costs: average A2P SMS prices vary $0.005–$0.10 per message by region, squeezing margins on campaign-heavy clients.

Scarcity of Specialized AI and Engineering Talent

The development of advanced marketing automation features requires top software engineers and AI data scientists, a talent pool whose demand grew 35% globally from 2020–2024 and remained tight in late 2025 with vacancy rates near 4.1% in the UK tech sector (ONS). This scarcity gives suppliers of talent strong bargaining power, pushing median AI engineer pay in the UK to ~£90k–£130k and total hiring cost multipliers of 1.6x. Dotdigital must offer competitive pay, equity, and training to retain staff and protect its product roadmap.

Third-party Software and API Integrations

Dotdigital’s integrations with Salesforce, Adobe Commerce and Shopify (among others) are core to its value—Salesforce’s AppExchange and Shopify’s 2024 merchant base of 4.8M give Dotdigital reach but create supplier dependency.

If API limits, fee changes, or deprecation occur (Salesforce raised some partner fees in 2023), Dotdigital’s functionality and revenue could be hit; platform owners therefore hold meaningful bargaining power.

- Dependency on major CRMs/platforms

- Shopify ~4.8M merchants (2024)

- Salesforce partner fee shifts in 2023

- API policy changes can reduce feature set/revenue

Data Compliance and Cybersecurity Service Providers

Dotdigital relies heavily on specialized legal and cybersecurity firms to meet EU GDPR and US state privacy rules; recent fines show stakes—GDPR penalties reached €1.3 billion in 2023, so compliance spend is nontrivial.

These suppliers deliver audits, ISO/IEC 27001 certifications, and advanced tooling that enable Dotdigital to serve regulated markets; a single breach can cost tens of millions and spike churn.

Because switching costs, expertise scarcity, and high breach penalties raise supplier leverage, providers command premium fees and favorable contract terms.

- 2023 GDPR fines: €1.3 billion

- ISO/IEC 27001 often required

- Breaches can cost tens of millions

- High switching costs, scarce expertise

Supplier squeeze: cloud, carriers, talent & compliance threaten Dotdigital margins

Suppliers exert medium–high power: cloud giants (AWS/Azure ~59% IaaS/PaaS, 2025) and carriers (global A2P SMS revenue $50.5bn, 2024) raise costs and switching risk; talent scarcity (UK AI engineer pay ~£90k–£130k, vacancy ~4.1%, 2024) and compliance providers (GDPR fines €1.3bn, 2023) further strengthen suppliers, squeezing margins unless Dotdigital passes costs to clients.

| Supplier | Key stat | Impact |

|---|---|---|

| Cloud (AWS/Azure) | ~59% IaaS/PaaS (2025) | High switching cost |

| Carriers/SMS | $50.5bn A2P (2024) | Price variability $0.005–$0.10/msg |

| Talent | UK AI pay £90k–£130k (2024) | Higher OPEX |

| Compliance | GDPR fines €1.3bn (2023) | Mandatory spend |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to dotDigital Group, detailing competitive forces, supplier/buyer power, substitutes, and barriers to entry with strategic insights and industry context for use in investor materials and strategy decks.

A concise Porter's Five Forces snapshot for dotDigital—one-sheet clarity to speed strategic decisions and highlight competitive pain points.

Customers Bargaining Power

Low Switching Costs for Small Businesses

In the lower market, SMEs can typically export contact lists via CSV/JSON and migrate platforms in days, so switching costs are low; industry surveys show 42% of SMBs cite easy data export as a top reason to switch (2024, SaaS Insights).

Because rivals often undercut on price, dotDigital must keep pricing competitive and uptime/service quality high—SMB churn rises ~3–5% if support SLA slips beyond 24 hours (2023 CRM Benchmarks).

High Volume of Competitor Options

The marketing-automation market had over 400 vendors by 2024, from freemium tools under $50/month to enterprise suites >$100k/year, and dotDigital faces intense choice pressure; 72% of B2B buyers used peer reviews and comparison sites in 2024, so customers regularly cite competitor quotes to push prices down and demand richer SLAs, raising buyer bargaining power.

Demand for Measurable Return on Investment

Modern marketing teams demand measurable ROI, pushing vendors like dotDigital to add advanced attribution and reporting; 72% of CMOs in 2024 said ROI measurement drives martech spend decisions, so buyers press for performance pricing or steep discounts when outcomes are unclear. This bargaining power forces dotDigital to include more features at existing price points or risk churn—average contract lengths fell to 18 months in 2024 for vendors lacking clear ROI proof.

Sophistication of Enterprise Procurement Teams

Larger corporate clients use professional procurement teams that routinely secure multi-year contracts and volume discounts, pressuring dotDigital to match rates that can shave 10–25% off list pricing versus SMB deals.

These buyers demand custom SLAs, dedicated support, and bespoke features; delivering that can raise implementation margins by 5–15% but also lengthen delivery by months.

The ability to switch to HubSpot, Braze, or Salesforce Marketing Cloud gives customers leverage to push favorable termination and rebate terms; enterprise churn risk rises if renewal pricing exceeds 8–12% YoY.

- Procurement skill: lowers price 10–25%

- Custom SLAs raise delivery cost 5–15%

- Switching to HubSpot/Braze increases contract concessions

- Renewal sensitivity: >8–12% YoY price hikes risk churn

Influence of Agency Partners

Marketing agencies that manage stacks for many clients can flip platform choice at scale; a single agency switch could cost dotDigital Group millions — agencies often oversee portfolios generating 10–30% of vendor ARR per agency in enterprise channels (example: 2024 agency-led deals represented ~22% of mid-market SaaS procurement).

Because agencies control concentrated revenue blocks, they can demand discounts, white-labeling, or exclusive features, raising customer acquisition costs and compressing margins; losing one or two agency partners could reduce gross retention materially.

- Agency-led revenue concentration: ~22% of mid-market SaaS deals (2024)

- Risk: single-agency switch can drop clustered ARR by 10–30%

- Bargaining levers: preferential pricing, white-labeling, integration support

- Mitigation: diversify partner base, embed technical lock-in, partner SLAs

Buyers Rule: 400+ Vendors, Tough Discounts, ROI Demands — Contracts Shrink to 18 Months

Buyers hold high bargaining power: low switching costs (CSV/JSON exports), 400+ vendors (2024), and heavy use of reviews (72%); SMB churn rises 3–5% if support slips beyond 24h. Procurement and agencies extract 10–25% discounts; enterprise renewals fail if YoY price hikes exceed 8–12%. Vendors must add features/ROI proof or face shorter contracts (avg 18 months, 2024).

| Metric | Value (2024) |

|---|---|

| Vendors | 400+ |

| Review use | 72% |

| SMB churn ↑ if SLA>24h | 3–5% |

| Procurement discount | 10–25% |

| Avg contract (no ROI) | 18 months |

What You See Is What You Get

dotDigital Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of dotDigital Group that you’ll receive instantly after purchase—fully formatted, professionally written, and ready to download with no placeholders or mockups.

The document displayed here is the actual deliverable: a complete, ready-to-use strategic assessment covering competitive rivalry, supplier and buyer power, threats of substitutes and entrants, and implications for strategy and valuation.