DoubleVerify Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

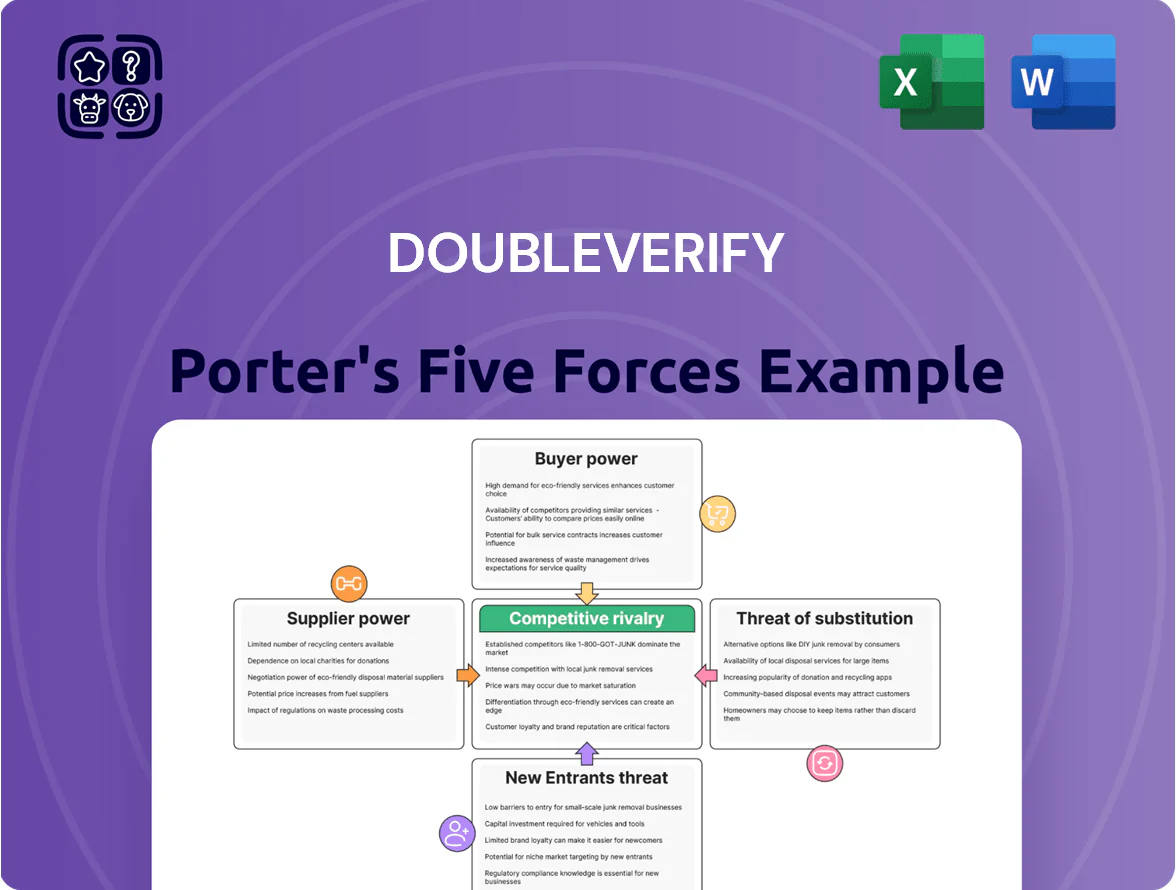

DoubleVerify faces intense buyer scrutiny, moderate supplier leverage, fierce rivalry among ad verification players, a rising threat of substitutes from in-house solutions, and regulatory/tech shifts that shape barriers to entry — but this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore DoubleVerify’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure and Data Hosting Providers

DoubleVerify depends on cloud giants such as Amazon Web Services and Google Cloud to process billions of ad impressions per day; their standardized pricing and data egress fees (often 0.09–0.12 USD/GB for cross-region egress in 2025) give suppliers moderate bargaining power.

To limit vendor leverage, DoubleVerify adopted a multi-cloud approach by late 2025, splitting workloads across providers and negotiating committed-use discounts (often 20–40% off list), reducing single-vendor lock-in risk.

Social Media Platforms and Walled Gardens

Access to data from Meta (Facebook/Instagram), TikTok, and Alphabet (Google/YouTube/Search) is essential for DoubleVerify’s ad measurement; in 2024 Meta reported 3.1 billion monthly users, TikTok 1.1 billion, and Alphabet $282.8B revenue, underscoring scale of needed signals.

These platforms supply raw signals and APIs that verification tools ingest; API rate limits, data sampling, or endpoint changes directly affect DoubleVerify’s coverage and latency.

Because these firms run closed ecosystems—walled gardens—they control transparency levels and can favor native measurement, giving them strong supplier power over third-party verification.

Specialized Data and Intelligence Feed Vendors

DoubleVerify integrates third-party intelligence feeds for fraud detection and contextual targeting; niche suppliers with patented data can demand premiums, especially where exclusivity exists—DoubleVerify reported $629m revenue in 2024, so supplier costs matter but are diluted by scale. Market breadth keeps power in check: over 50+ alternative feed providers and growing open-source threat data reduced vendor concentration. Still, unique cyber-intel raises switching costs for specific modules.

High-Level Engineering and AI Talent

High-level engineering and AI talent is a critical resource for DoubleVerify’s brand-safety algorithms, and in 2025 demand outstrips supply: US median data scientist pay rose to about $148,000 in 2024 and top AI hires command $250k+ total comp, boosting supplier (talent) bargaining power.

Cybersecurity experts and ML engineers insist on remote flexibility; 62% of tech hires in 2024 rejected offers lacking it, raising retention costs.

DoubleVerify must keep investing in employer brand, pay premiums, and training—its 2024 R&D spend of $121M (24% of revenue) shows scale of required investment.

- Top-tier hires: $250k+ comp

- Median data scientist pay: ~$148k (2024)

- 62% reject offers without remote work

- 2024 R&D: $121M (24% of revenue)

Regulatory and Compliance Consultants

Regulatory and compliance consultants have grown in leverage as GDPR and expanding US state privacy laws raise stakes; global fines reached €1.4bn in 2024 under GDPR enforcement, highlighting risk for measurement firms like DoubleVerify.

These specialists are crucial to keep DoubleVerify’s tracking methods compliant across 100+ jurisdictions, and their bargaining power is high because non-compliance can trigger multi-million‑dollar fines or regional service bans.

- High leverage: €1.4bn GDPR fines in 2024

- Scope risk: 100+ regulatory regimes

- Cost of failure: multi‑million fines or bans

- Specialist scarcity: rising demand for privacy legal experts

Suppliers Squeeze Adtech: Platforms, Cloud & Talent Keep Pricing Power Despite Scale

Suppliers exert moderate-to-strong power: cloud providers (AWS/GCP) and walled‑garden platforms (Meta, Google, TikTok) control crucial data and APIs, while niche intel feeds, top ML/security talent, and privacy consultants command premiums—DoubleVerify’s scale (2024 revenue $629M; R&D $121M) reduces but does not eliminate this squeeze.

| Supplier | Key metric (2024/25) | Bargaining power |

|---|---|---|

| Cloud (AWS/GCP) | egress $0.09–0.12/GB (2025); committed discounts 20–40% | Moderate |

| Walled gardens | Meta 3.1B users (2024); Alphabet revenue $282.8B (2024) | Strong |

| Talent | Median data scientist $148k; top hires $250k+ | High |

| Privacy consultants | GDPR fines €1.4B (2024); 100+ jurisdictions | High |

What is included in the product

Tailored exclusively for DoubleVerify, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier influence, entry barriers, substitutes, and emerging threats that shape its pricing power and market resilience.

A concise Porter's Five Forces snapshot for DoubleVerify—clarifies competitive pressures and risk levers for faster strategic decisions.

Customers Bargaining Power

Concentration of Global Advertising Holding Companies

A large share of DoubleVerify’s 2024 revenue is concentrated: WPP, Omnicom, and Publicis together account for an estimated 25–35% of platform spend, giving them strong leverage to demand volume discounts and strict SLAs.

These holding companies pool budgets from thousands of brands, so they can shift entire agency portfolios to competitors like Integral Ad Science, creating high buyer power and pricing pressure on DV’s margins.

Demand for Standardized Cross-Platform Metrics

Advertisers now demand unified measurement across Connected TV, social media, and programmatic web—66% of marketers in 2024 said cross-platform metrics are top priority, pushing DoubleVerify to expand integrations into 25+ CTV platforms and major social APIs.

This pressure forces constant innovation and R&D: DoubleVerify increased product development spend 18% in 2024 to build a single source of truth.

Without full channel coverage, customers would rapidly switch—TV and digital ad buyers cite 32% churn risk if vendors lack cross-platform parity.

Low Switching Costs for Basic Verification Services

Deep integration with publishers and DSPs gives DoubleVerify some stickiness, but core services like viewability and fraud detection are commoditized; industry surveys in 2024 show 62% of CMOs ran vendor bake-offs and 48% negotiated price cuts at renewal. Large advertisers frequently pit verification vendors against each other to cut fees, and performance marketers—often working on margins under 10%—drive high price sensitivity and churn risk.

Direct Enterprise Brand Relationships

- ~38% of advertisers increasing in-house ad-tech spend (2024)

- Buyers demand API access, granular metrics, custom safety rules

- Higher negotiation power → pressure on pricing and SLAs

Growth of Programmatic Bidding Power

Programmatic buy-side platforms let advertisers toggle verification on/off by ROI; DoubleVerify (DV) faces per-auction scrutiny and must justify fees in real time to avoid being bypassed.

Programmatic transparency lets buyers compare DV filters and switch to cheaper tools; industry data shows programmatic ad spend hit $150B in 2024, raising stakes for verification ROI.

Advertiser leverage rises: agencies, in‑house tech & $150B programmatic force ROI deals

Buyers hold high leverage: top agencies (WPP, Omnicom, Publicis) drive ~25–35% DV spend, 38% of advertisers increased in‑house ad‑tech (2024), 62% of CMOs ran vendor bake‑offs, and programmatic spend hit $150B (2024) — forcing discounts, bespoke SLAs, API access, and continuous ROI proof to avoid churn.

| Metric | Value (2024) |

|---|---|

| Top agencies share | 25–35% |

| In‑house ad‑tech | ~38% |

| Vendor bake‑offs | 62% CMOs |

| Programmatic spend | $150B |

Same Document Delivered

DoubleVerify Porter's Five Forces Analysis

This preview shows the exact DoubleVerify Porter’s Five Forces analysis you'll receive upon purchase—no placeholders or mockups. The document displayed is fully formatted, professionally written, and ready for immediate download and use after payment. What you see here is the complete deliverable, identical to the file you’ll get instantly once you buy. No surprises, no further setup required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

DoubleVerify faces intense buyer scrutiny, moderate supplier leverage, fierce rivalry among ad verification players, a rising threat of substitutes from in-house solutions, and regulatory/tech shifts that shape barriers to entry — but this snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore DoubleVerify’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure and Data Hosting Providers

DoubleVerify depends on cloud giants such as Amazon Web Services and Google Cloud to process billions of ad impressions per day; their standardized pricing and data egress fees (often 0.09–0.12 USD/GB for cross-region egress in 2025) give suppliers moderate bargaining power.

To limit vendor leverage, DoubleVerify adopted a multi-cloud approach by late 2025, splitting workloads across providers and negotiating committed-use discounts (often 20–40% off list), reducing single-vendor lock-in risk.

Social Media Platforms and Walled Gardens

Access to data from Meta (Facebook/Instagram), TikTok, and Alphabet (Google/YouTube/Search) is essential for DoubleVerify’s ad measurement; in 2024 Meta reported 3.1 billion monthly users, TikTok 1.1 billion, and Alphabet $282.8B revenue, underscoring scale of needed signals.

These platforms supply raw signals and APIs that verification tools ingest; API rate limits, data sampling, or endpoint changes directly affect DoubleVerify’s coverage and latency.

Because these firms run closed ecosystems—walled gardens—they control transparency levels and can favor native measurement, giving them strong supplier power over third-party verification.

Specialized Data and Intelligence Feed Vendors

DoubleVerify integrates third-party intelligence feeds for fraud detection and contextual targeting; niche suppliers with patented data can demand premiums, especially where exclusivity exists—DoubleVerify reported $629m revenue in 2024, so supplier costs matter but are diluted by scale. Market breadth keeps power in check: over 50+ alternative feed providers and growing open-source threat data reduced vendor concentration. Still, unique cyber-intel raises switching costs for specific modules.

High-Level Engineering and AI Talent

High-level engineering and AI talent is a critical resource for DoubleVerify’s brand-safety algorithms, and in 2025 demand outstrips supply: US median data scientist pay rose to about $148,000 in 2024 and top AI hires command $250k+ total comp, boosting supplier (talent) bargaining power.

Cybersecurity experts and ML engineers insist on remote flexibility; 62% of tech hires in 2024 rejected offers lacking it, raising retention costs.

DoubleVerify must keep investing in employer brand, pay premiums, and training—its 2024 R&D spend of $121M (24% of revenue) shows scale of required investment.

- Top-tier hires: $250k+ comp

- Median data scientist pay: ~$148k (2024)

- 62% reject offers without remote work

- 2024 R&D: $121M (24% of revenue)

Regulatory and Compliance Consultants

Regulatory and compliance consultants have grown in leverage as GDPR and expanding US state privacy laws raise stakes; global fines reached €1.4bn in 2024 under GDPR enforcement, highlighting risk for measurement firms like DoubleVerify.

These specialists are crucial to keep DoubleVerify’s tracking methods compliant across 100+ jurisdictions, and their bargaining power is high because non-compliance can trigger multi-million‑dollar fines or regional service bans.

- High leverage: €1.4bn GDPR fines in 2024

- Scope risk: 100+ regulatory regimes

- Cost of failure: multi‑million fines or bans

- Specialist scarcity: rising demand for privacy legal experts

Suppliers Squeeze Adtech: Platforms, Cloud & Talent Keep Pricing Power Despite Scale

Suppliers exert moderate-to-strong power: cloud providers (AWS/GCP) and walled‑garden platforms (Meta, Google, TikTok) control crucial data and APIs, while niche intel feeds, top ML/security talent, and privacy consultants command premiums—DoubleVerify’s scale (2024 revenue $629M; R&D $121M) reduces but does not eliminate this squeeze.

| Supplier | Key metric (2024/25) | Bargaining power |

|---|---|---|

| Cloud (AWS/GCP) | egress $0.09–0.12/GB (2025); committed discounts 20–40% | Moderate |

| Walled gardens | Meta 3.1B users (2024); Alphabet revenue $282.8B (2024) | Strong |

| Talent | Median data scientist $148k; top hires $250k+ | High |

| Privacy consultants | GDPR fines €1.4B (2024); 100+ jurisdictions | High |

What is included in the product

Tailored exclusively for DoubleVerify, this Porter's Five Forces overview uncovers competitive drivers, buyer/supplier influence, entry barriers, substitutes, and emerging threats that shape its pricing power and market resilience.

A concise Porter's Five Forces snapshot for DoubleVerify—clarifies competitive pressures and risk levers for faster strategic decisions.

Customers Bargaining Power

Concentration of Global Advertising Holding Companies

A large share of DoubleVerify’s 2024 revenue is concentrated: WPP, Omnicom, and Publicis together account for an estimated 25–35% of platform spend, giving them strong leverage to demand volume discounts and strict SLAs.

These holding companies pool budgets from thousands of brands, so they can shift entire agency portfolios to competitors like Integral Ad Science, creating high buyer power and pricing pressure on DV’s margins.

Demand for Standardized Cross-Platform Metrics

Advertisers now demand unified measurement across Connected TV, social media, and programmatic web—66% of marketers in 2024 said cross-platform metrics are top priority, pushing DoubleVerify to expand integrations into 25+ CTV platforms and major social APIs.

This pressure forces constant innovation and R&D: DoubleVerify increased product development spend 18% in 2024 to build a single source of truth.

Without full channel coverage, customers would rapidly switch—TV and digital ad buyers cite 32% churn risk if vendors lack cross-platform parity.

Low Switching Costs for Basic Verification Services

Deep integration with publishers and DSPs gives DoubleVerify some stickiness, but core services like viewability and fraud detection are commoditized; industry surveys in 2024 show 62% of CMOs ran vendor bake-offs and 48% negotiated price cuts at renewal. Large advertisers frequently pit verification vendors against each other to cut fees, and performance marketers—often working on margins under 10%—drive high price sensitivity and churn risk.

Direct Enterprise Brand Relationships

- ~38% of advertisers increasing in-house ad-tech spend (2024)

- Buyers demand API access, granular metrics, custom safety rules

- Higher negotiation power → pressure on pricing and SLAs

Growth of Programmatic Bidding Power

Programmatic buy-side platforms let advertisers toggle verification on/off by ROI; DoubleVerify (DV) faces per-auction scrutiny and must justify fees in real time to avoid being bypassed.

Programmatic transparency lets buyers compare DV filters and switch to cheaper tools; industry data shows programmatic ad spend hit $150B in 2024, raising stakes for verification ROI.

Advertiser leverage rises: agencies, in‑house tech & $150B programmatic force ROI deals

Buyers hold high leverage: top agencies (WPP, Omnicom, Publicis) drive ~25–35% DV spend, 38% of advertisers increased in‑house ad‑tech (2024), 62% of CMOs ran vendor bake‑offs, and programmatic spend hit $150B (2024) — forcing discounts, bespoke SLAs, API access, and continuous ROI proof to avoid churn.

| Metric | Value (2024) |

|---|---|

| Top agencies share | 25–35% |

| In‑house ad‑tech | ~38% |

| Vendor bake‑offs | 62% CMOs |

| Programmatic spend | $150B |

Same Document Delivered

DoubleVerify Porter's Five Forces Analysis

This preview shows the exact DoubleVerify Porter’s Five Forces analysis you'll receive upon purchase—no placeholders or mockups. The document displayed is fully formatted, professionally written, and ready for immediate download and use after payment. What you see here is the complete deliverable, identical to the file you’ll get instantly once you buy. No surprises, no further setup required.