Dow PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, social trends, technological innovation, legal developments, and environmental pressures converge to shape Dow’s strategic outlook—our concise PESTLE highlights key external risks and opportunities. Ideal for investors and strategists, the full, ready-to-use report delivers deep-dive analysis, editable charts, and actionable recommendations. Purchase now to access the complete PESTLE and make better-informed decisions.

Political factors

Global Trade Policy Volatility

Dow operates in more than 160 countries, so U.S.-China tariff tensions—tariffs affecting chemical trades rose by about 15% in 2018–2019 and tariff volatility persisted through 2024—directly threaten margins and cross-border supply chains.

Trade barriers on chemical exports can raise feedstock and intermediate costs; Dow reported global raw-material inflation contributed to $1.1 billion of margin pressure in 2022–2023.

Protectionist policies and local content rules in key markets risk crowding out Dow’s global scale advantages, forcing higher local investment and potential price pass-through to customers.

Government Incentives for Green Energy

The Inflation Reduction Act allocates up to a $85/ton tax credit for carbon capture via 45Q and expanded hydrogen credits, enabling Dow to capture subsidies that lower capital intensity of low‑carbon projects; Dow reported $1.1 billion in sustainability‑linked investments in 2024, partly offset by these incentives.

Geopolitical Stability in Key Regions

Ongoing conflicts in Eastern Europe and the Middle East have pressured feedstock costs—European natural gas prices averaged about $35/MMBtu in 2024 vs $8–10/MMBtu pre-2022—pushing naphtha and ethylene margins down and prompting Dow to hedge and shift sourcing; political instability has led Dow to reduce exposure in volatile zones, increase insurance and write-offs (capital at risk unspecified) and maintain continuous diplomatic and risk-mitigation teams to protect assets and supply chains.

Plastic Waste Legislation

- 30% recycled PET by 2030 (EU)

- 60+ national plastic tax proposals in 2024

- Dow sustainability capex ~$1.2bn in 2024

- Active policymaker engagement to shape standards

Infrastructure Spending Programs

- Federal infrastructure pool ~1.2 trillion since 2021

- State/federal annual spending est. $100–150B through 2025

- PPPs fund ~20–40% of large projects

Policy shifts, tariffs and mandates reshape chemical margins and boost infrastructure demand

Geopolitical tensions, trade barriers and protectionism (tariff volatility since 2018; chemical tariffs ~15% 2018–19) raise feedstock costs and margin risk; policy incentives (45Q, hydrogen credits) and $85/ton tax credits lower low‑carbon CAPEX; plastic bans/recycled-content mandates (EU PET 30% by 2030) and 60+ tax proposals in 2024 force product shifts; infrastructure spending (~$1.2T federal since 2021) boosts demand.

| Metric | Value |

|---|---|

| Chemical tariff rise | ~15% (2018–19) |

| Plastic tax proposals (2024) | 60+ |

| EU PET mandate | 30% by 2030 |

| Fed infra pool | ~$1.2T since 2021 |

What is included in the product

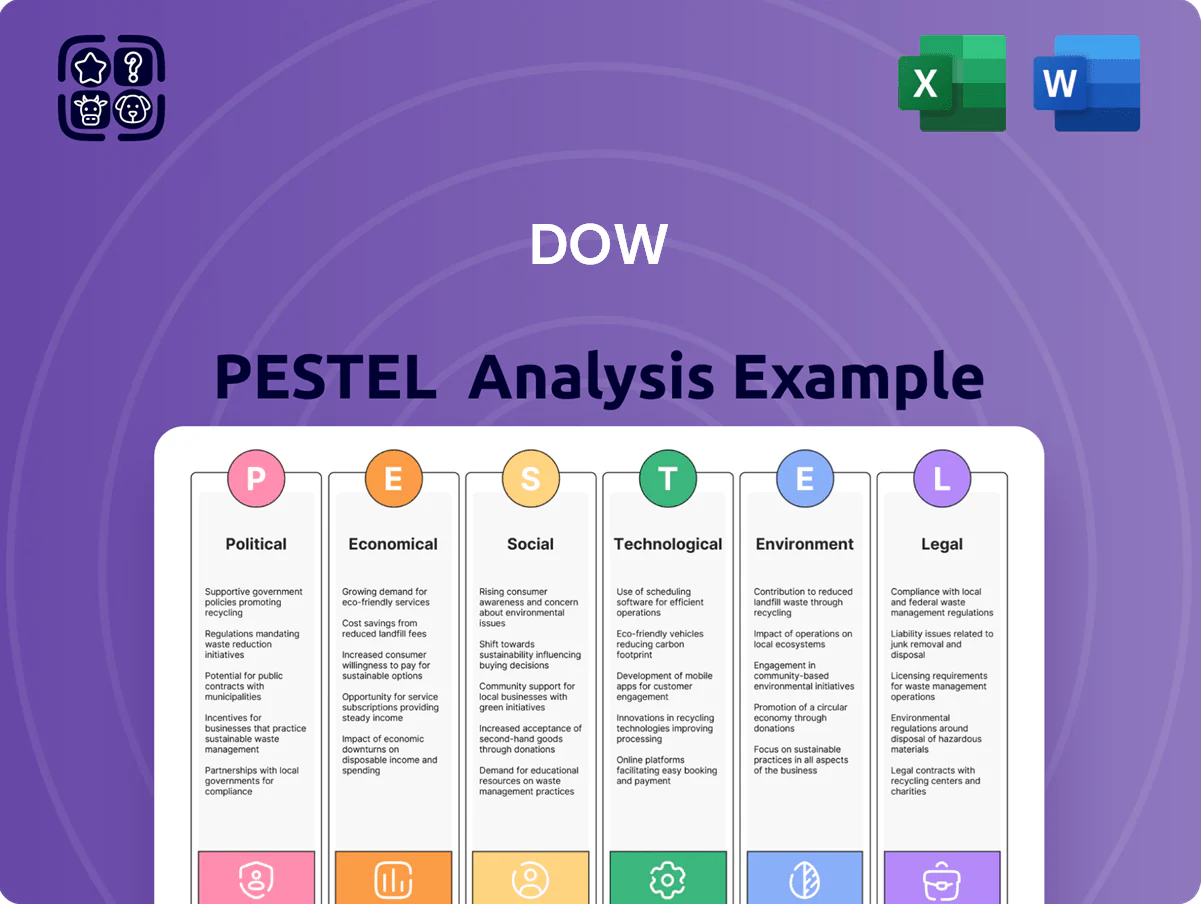

Explores how macro-environmental forces uniquely affect the Dow across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed trends and forward-looking insights to identify risks and opportunities.

A concise, visually segmented PESTLE summary tailored for the Dow that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Feedstock Price Volatility

Dow’s profitability is highly sensitive to feedstock costs—ethane, propane and crude oil—representing roughly 40–60% of variable cost in olefins production; a 10% rise in crude-linked feedstock in 2024 cut global chemical margins by an estimated $50–70/ton.

Global Economic Growth Cycles

Demand for chemicals and plastics tracks global GDP and industrial output; IMF projected 2025 global GDP growth at 3.2% in Oct 2024, and Dow’s revenues fell 8% in 2020 downturn when automotive and construction orders slumped. Cyclical weakness compresses margins as volumes drop; Dow reported a 6% YoY volume decline in industrial end-markets in 2023. Recovery in India and Southeast Asia, where IMF forecasts 2024–25 growth ~6–7%, offers high-growth expansion potential for Dow.

Interest Rate Environment

As a capital-intensive chemical leader, Dow depends on debt markets for projects and acquisitions; at end-2025 Dow reported net debt of about $10.8bn, making sensitivity to borrowing costs material. Rising global policy rates—Fed funds around 5.25–5.50% in 2024–25—heightened interest expense and pressured returns, slowing some planned plant modernization spending. Dow actively manages its debt maturity profile, with average debt maturity near 5 years and targeted refinancing to hedge central bank volatility.

Currency Exchange Rate Fluctuations

With sales in over 160 countries, Dow faces currency translation risk; in 2024 roughly 25% of revenue was sourced outside the U.S., so a 10% dollar appreciation could lower reported international earnings materially.

A stronger dollar reduces export competitiveness and cut 2023 adjusted EPS by an estimated mid-single-digit percentage; Dow uses forward contracts and options, disclosing $6–8 billion notional hedges in recent filings to mitigate FX volatility.

- Global exposure: >160 countries; ~25% revenue ex-US

- Impact: 10% USD rise → material earnings reduction; 2023 FX drag ~mid-single-digit EPS

- Mitigation: $6–8bn notional hedges via forwards/options

Inflationary Pressure on Operations

Persistent inflation raised global input costs for Dow in 2024–25, with US CPI averaging ~3.4% in 2024 and energy prices up ~8% year-over-year, increasing labor, logistics, and maintenance expenses across its ~100 manufacturing sites.

To protect margins Dow intensified efficiency programs and raised selling prices; Q4 2024 gross margin improved to 23.5% partly from price/mix actions.

Sustained inflation risks reducing end-market demand—global appliance shipments fell ~2% in 2024—pressuring volumes for Dow’s materials.

- Input cost inflation (CPI ~3.4% 2024) raised operating expenses

- Efficiency initiatives and price/mix drove gross margin to ~23.5% (Q4 2024)

- Weaker end-market demand (appliances down ~2% 2024) could depress volumes

Feedstock swings slash margins; debt, FX and rates pressure chemicals outlook

Feedstock volatility (ethane/propane/crude ~40–60% variable cost) can swing margins; 10% crude rise cut chemical margins ~$50–70/ton in 2024. Demand tracks GDP (IMF 2025 growth 3.2%); Dow volumes fell 6% YoY in 2023. Net debt ~ $10.8bn (end-2025); Fed funds ~5.25–5.50% in 2024–25 raises funding cost. FX: ~25% revenue ex-US; $6–8bn hedges; 2024 CPI ~3.4%.

| Metric | Value |

|---|---|

| Net debt | $10.8bn |

| Revenue ex-US | ~25% |

| Fed funds | 5.25–5.50% |

| 2024 CPI | ~3.4% |

What You See Is What You Get

Dow PESTLE Analysis

The preview shown here is the exact Dow PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible now are identical to the file you’ll download immediately after payment.

What you see is the final product—comprehensive, accurate, and delivered exactly as presented.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, social trends, technological innovation, legal developments, and environmental pressures converge to shape Dow’s strategic outlook—our concise PESTLE highlights key external risks and opportunities. Ideal for investors and strategists, the full, ready-to-use report delivers deep-dive analysis, editable charts, and actionable recommendations. Purchase now to access the complete PESTLE and make better-informed decisions.

Political factors

Global Trade Policy Volatility

Dow operates in more than 160 countries, so U.S.-China tariff tensions—tariffs affecting chemical trades rose by about 15% in 2018–2019 and tariff volatility persisted through 2024—directly threaten margins and cross-border supply chains.

Trade barriers on chemical exports can raise feedstock and intermediate costs; Dow reported global raw-material inflation contributed to $1.1 billion of margin pressure in 2022–2023.

Protectionist policies and local content rules in key markets risk crowding out Dow’s global scale advantages, forcing higher local investment and potential price pass-through to customers.

Government Incentives for Green Energy

The Inflation Reduction Act allocates up to a $85/ton tax credit for carbon capture via 45Q and expanded hydrogen credits, enabling Dow to capture subsidies that lower capital intensity of low‑carbon projects; Dow reported $1.1 billion in sustainability‑linked investments in 2024, partly offset by these incentives.

Geopolitical Stability in Key Regions

Ongoing conflicts in Eastern Europe and the Middle East have pressured feedstock costs—European natural gas prices averaged about $35/MMBtu in 2024 vs $8–10/MMBtu pre-2022—pushing naphtha and ethylene margins down and prompting Dow to hedge and shift sourcing; political instability has led Dow to reduce exposure in volatile zones, increase insurance and write-offs (capital at risk unspecified) and maintain continuous diplomatic and risk-mitigation teams to protect assets and supply chains.

Plastic Waste Legislation

- 30% recycled PET by 2030 (EU)

- 60+ national plastic tax proposals in 2024

- Dow sustainability capex ~$1.2bn in 2024

- Active policymaker engagement to shape standards

Infrastructure Spending Programs

- Federal infrastructure pool ~1.2 trillion since 2021

- State/federal annual spending est. $100–150B through 2025

- PPPs fund ~20–40% of large projects

Policy shifts, tariffs and mandates reshape chemical margins and boost infrastructure demand

Geopolitical tensions, trade barriers and protectionism (tariff volatility since 2018; chemical tariffs ~15% 2018–19) raise feedstock costs and margin risk; policy incentives (45Q, hydrogen credits) and $85/ton tax credits lower low‑carbon CAPEX; plastic bans/recycled-content mandates (EU PET 30% by 2030) and 60+ tax proposals in 2024 force product shifts; infrastructure spending (~$1.2T federal since 2021) boosts demand.

| Metric | Value |

|---|---|

| Chemical tariff rise | ~15% (2018–19) |

| Plastic tax proposals (2024) | 60+ |

| EU PET mandate | 30% by 2030 |

| Fed infra pool | ~$1.2T since 2021 |

What is included in the product

Explores how macro-environmental forces uniquely affect the Dow across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed trends and forward-looking insights to identify risks and opportunities.

A concise, visually segmented PESTLE summary tailored for the Dow that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Feedstock Price Volatility

Dow’s profitability is highly sensitive to feedstock costs—ethane, propane and crude oil—representing roughly 40–60% of variable cost in olefins production; a 10% rise in crude-linked feedstock in 2024 cut global chemical margins by an estimated $50–70/ton.

Global Economic Growth Cycles

Demand for chemicals and plastics tracks global GDP and industrial output; IMF projected 2025 global GDP growth at 3.2% in Oct 2024, and Dow’s revenues fell 8% in 2020 downturn when automotive and construction orders slumped. Cyclical weakness compresses margins as volumes drop; Dow reported a 6% YoY volume decline in industrial end-markets in 2023. Recovery in India and Southeast Asia, where IMF forecasts 2024–25 growth ~6–7%, offers high-growth expansion potential for Dow.

Interest Rate Environment

As a capital-intensive chemical leader, Dow depends on debt markets for projects and acquisitions; at end-2025 Dow reported net debt of about $10.8bn, making sensitivity to borrowing costs material. Rising global policy rates—Fed funds around 5.25–5.50% in 2024–25—heightened interest expense and pressured returns, slowing some planned plant modernization spending. Dow actively manages its debt maturity profile, with average debt maturity near 5 years and targeted refinancing to hedge central bank volatility.

Currency Exchange Rate Fluctuations

With sales in over 160 countries, Dow faces currency translation risk; in 2024 roughly 25% of revenue was sourced outside the U.S., so a 10% dollar appreciation could lower reported international earnings materially.

A stronger dollar reduces export competitiveness and cut 2023 adjusted EPS by an estimated mid-single-digit percentage; Dow uses forward contracts and options, disclosing $6–8 billion notional hedges in recent filings to mitigate FX volatility.

- Global exposure: >160 countries; ~25% revenue ex-US

- Impact: 10% USD rise → material earnings reduction; 2023 FX drag ~mid-single-digit EPS

- Mitigation: $6–8bn notional hedges via forwards/options

Inflationary Pressure on Operations

Persistent inflation raised global input costs for Dow in 2024–25, with US CPI averaging ~3.4% in 2024 and energy prices up ~8% year-over-year, increasing labor, logistics, and maintenance expenses across its ~100 manufacturing sites.

To protect margins Dow intensified efficiency programs and raised selling prices; Q4 2024 gross margin improved to 23.5% partly from price/mix actions.

Sustained inflation risks reducing end-market demand—global appliance shipments fell ~2% in 2024—pressuring volumes for Dow’s materials.

- Input cost inflation (CPI ~3.4% 2024) raised operating expenses

- Efficiency initiatives and price/mix drove gross margin to ~23.5% (Q4 2024)

- Weaker end-market demand (appliances down ~2% 2024) could depress volumes

Feedstock swings slash margins; debt, FX and rates pressure chemicals outlook

Feedstock volatility (ethane/propane/crude ~40–60% variable cost) can swing margins; 10% crude rise cut chemical margins ~$50–70/ton in 2024. Demand tracks GDP (IMF 2025 growth 3.2%); Dow volumes fell 6% YoY in 2023. Net debt ~ $10.8bn (end-2025); Fed funds ~5.25–5.50% in 2024–25 raises funding cost. FX: ~25% revenue ex-US; $6–8bn hedges; 2024 CPI ~3.4%.

| Metric | Value |

|---|---|

| Net debt | $10.8bn |

| Revenue ex-US | ~25% |

| Fed funds | 5.25–5.50% |

| 2024 CPI | ~3.4% |

What You See Is What You Get

Dow PESTLE Analysis

The preview shown here is the exact Dow PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible now are identical to the file you’ll download immediately after payment.

What you see is the final product—comprehensive, accurate, and delivered exactly as presented.