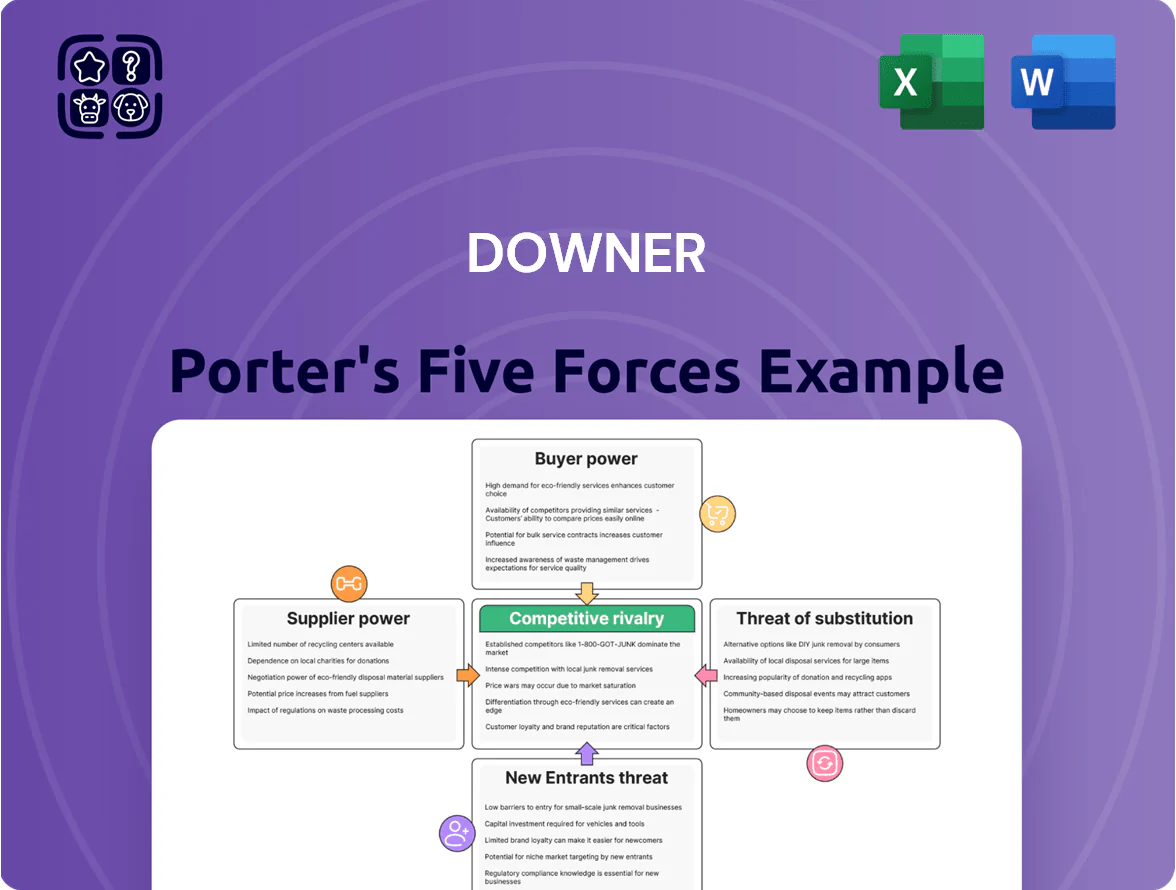

Downer Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Downer faces moderate supplier power and infrastructure-driven barriers to entry, while buyer concentration and substitute services create selective pricing pressure—this snapshot highlights competitive intensity and strategic levers you can act on.

Suppliers Bargaining Power

Specialized Labor and Trade Unions

The scarcity of skilled engineers and technicians in Australia and New Zealand boosts supplier power for labor unions and specialist contractors, with vacancy rates for trades roles at 3.8% nationally in Australia (Nov 2025) and 4.2% in NZ (Q3 2025), raising bargaining leverage. Wage inflation stayed high in late 2025—annual private-sector wages rose ~4.6% in Australia and 5.1% in NZ—forcing Downer to offer competitive pay and benefits to retain staff. For long-term projects this raises operating costs; payroll now represents ~22–25% of project budgets on large integrated contracts. Failure to match market rates risks delays, higher subcontractor premiums, and scope re-bids.

Raw Material and Commodity Volatility

Suppliers of bitumen, steel, and concrete exert moderate power: global commodity pricing drove steel up 25% in 2021–22 and bitumen volatility spiked 18% in 2022, while concrete shortages in Australia in 2023 caused 10–15% regional price jumps.

Downer uses bulk purchasing and rise-and-fall clauses; hedging reduced input-cost swings by ~6% in 2024, yet localized disruptions can still trigger short-term margin pressure.

Subcontractor Dependency

The reliance on specialized subcontractors for niche components gives them outsized bargaining power; for example, in 2024 Downer Group reported subcontractor costs at ~38% of revenue, and shortages pushed some civil subcontract rates up 12–18% in Australia in 2023–24. In high-demand periods those subcontractors can switch to rivals, raising procurement costs and squeezing margins, so tight supplier contracts and dual-sourcing are critical to protect timelines and margin integrity.

Technology and Fleet Providers

As Downer digitizes operations, specialized asset-management software and heavy-equipment OEMs gain leverage; global construction-tech VC funding hit US$29.8bn in 2024, boosting supplier innovation and pricing power.

Shifting to electric/hydrogen fleets concentrates power: only a few OEMs supply heavy EV/hydrogen trucks and electrolyzers, raising switching costs and forcing multi-year contracts.

Long-term strategic partnerships lock in software updates, support SLAs, and cap capex volatility—typical fleet supply contracts run 5–10 years with 10–20% upgrade clauses.

- Specialized software suppliers rising influence

- EV/hydrogen OEMs limited, high bargaining power

- Multi-year (5–10y) contracts common

- 2024 construction-tech VC: US$29.8bn

Energy and Fuel Inputs

The high energy intensity of Downer Group’s transport and construction ops makes it sensitive to fuel and utility pricing; diesel accounted for about 12–18% of operating costs in comparable contractors in 2024.

Australia’s renewable rollout is led by a few large firms—AGL, Origin Energy, and the big gentailers—so green energy at scale remains concentrated, raising supplier leverage.

Downer mitigates exposure via long-term power purchase agreements (PPAs); a 10–15 year PPA can cut electricity price volatility and cap energy OPEX.

- Diesel ≈12–18% of ops costs (peer FY2024)

- Major renewables market share: top 3 gentailers

- Preferred fix: 10–15 year PPAs to stabilize OPEX

Supplier pressure pinches Downer: wages, subcontractor costs & fuel risk squeeze margins

Supplier power for Downer is moderate-to-high: skilled labor shortages (Australia trades vacancy 3.8% Nov 2025; NZ 4.2% Q3 2025) and wage inflation (~4.6% Australia, 5.1% NZ in 2025) push payroll to ~22–25% of project budgets; subcontractor spend ~38% of revenue (2024) with rates up 12–18% in 2023–24; commodity and energy volatility (diesel ≈12–18% ops costs) add margin risk, so long-term contracts, hedges, and dual-sourcing are critical.

| Metric | Value |

|---|---|

| AU trades vacancy | 3.8% (Nov 2025) |

| NZ trades vacancy | 4.2% (Q3 2025) |

| Wage growth | AU 4.6%, NZ 5.1% (2025) |

| Payroll share | 22–25% of project budgets |

| Subcontractor share | ~38% of revenue (2024) |

| Subcontractor rate rise | 12–18% (2023–24) |

| Diesel/Ops | ≈12–18% (peers FY2024) |

What is included in the product

Concise Five Forces assessment focused on Downer’scompetitive dynamics, highlighting supplier/buyer power, rivalry intensity, entry barriers, substitutes, and emerging disruptors with strategic implications for pricing and profitability.

Downer Porter’s Five Forces condensed into a one-sheet, letting teams quickly gauge competitive pressure and make strategic choices without sifting through reports.

Customers Bargaining Power

Government Procurement Dominance

State and federal governments in Australia and New Zealand account for roughly 40–60% of Downer’s revenue mix, giving them outsized bargaining power through transparent, competitive tenders that heavily weight cost-efficiency and social value (e.g., Indigenous procurement targets, carbon reduction clauses).

Rigorous Contractual Terms

Large institutional and government clients often impose contractual terms that shift operational and financial risk to Downer, including liquidated damages—recent Australian infrastructure contracts show median LD clauses of A$250k–A$1m per month—and strict KPIs tied to payment; in FY2024 Downer reported A$52m in contract provisions linked to performance risk, so negotiating risk-sharing (capped LDs, shared delay clauses, gainshare) is a key competitive edge that can protect margins and cash flow.

Low Switching Costs at Contract Expiry

When a Downer maintenance or service contract expires, clients often run a new tender and can switch to rivals with minimal friction, driving a steady cycle of competitive bids; Australian federal procurement data shows 42% of infrastructure service contracts changed suppliers at renewal in 2023. Incumbents must repeatedly prove technical capability and cost-effectiveness, so loyalty ranks below proposal quality and price, pressuring margins and forcing continuous efficiency gains.

Demand for ESG Compliance

Modern clients require rigorous ESG (environmental, social, governance) reporting to qualify for contracts, with 72% of infrastructure tenders in Australia by 2024 citing ESG criteria and 40% applying minimum carbon targets.

That demand lets customers set standards on emissions and diversity, pushing Downer to meet decarbonisation timelines and 30%+ diverse workforce metrics or risk losing bids.

Failure to comply can cut access to major pipelines: public sector projects worth A$45bn (2024–25) increasingly prequalify only ESG-compliant firms.

- 72% of infra tenders include ESG (Australia, 2024)

- 40% apply carbon targets (2024)

- 30%+ diversity benchmarks common

- Public project pipeline A$45bn (2024–25)

Market Transparency and Benchmarking

Clients hiring independent consultants to benchmark service costs—industry average margins often 6–12% in 2024 for infrastructure services—caps Downer’s ability to charge premiums.

Customers access public data on labor rates (AUS avg. construction wage A$48/hr in 2024) and commodity prices, so high margins are visible and contested.

That transparency forces price sensitivity; operational efficiency (productivity, unit costs) becomes the main competitive lever.

- Consultant benchmarks limit premium pricing.

- Visible wages A$48/hr and 6–12% sector margins (2024).

- Transparency increases price pressure.

- Efficiency drives win rates and margins.

Public-sector clout squeezes Downer: tight margins, heavy ESG & penalty risks

Customers—especially Australian and NZ governments (40–60% of revenue)—hold strong bargaining power via competitive tenders, strict KPIs, liquidated damages (median A$250k–A$1m/month) and ESG prequalification (72% tenders, 40% carbon targets), forcing Downer to accept tight margins (industry 6–12%), meet A$48/hr wage transparency, and continually improve efficiency to win contracts.

| Metric | Value (2024) |

|---|---|

| Public revenue share | 40–60% |

| LD median | A$250k–A$1m/month |

| ESG tenders | 72% |

| Carbon targets in tenders | 40% |

| Sector margins | 6–12% |

| Avg construction wage (AUS) | A$48/hr |

| Public project pipeline | A$45bn (2024–25) |

Full Version Awaits

Downer Porter's Five Forces Analysis

This preview shows the exact Downer Porter’s Five Forces analysis you’ll receive—no placeholders or mockups—fully formatted and ready for immediate download after purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Downer faces moderate supplier power and infrastructure-driven barriers to entry, while buyer concentration and substitute services create selective pricing pressure—this snapshot highlights competitive intensity and strategic levers you can act on.

Suppliers Bargaining Power

Specialized Labor and Trade Unions

The scarcity of skilled engineers and technicians in Australia and New Zealand boosts supplier power for labor unions and specialist contractors, with vacancy rates for trades roles at 3.8% nationally in Australia (Nov 2025) and 4.2% in NZ (Q3 2025), raising bargaining leverage. Wage inflation stayed high in late 2025—annual private-sector wages rose ~4.6% in Australia and 5.1% in NZ—forcing Downer to offer competitive pay and benefits to retain staff. For long-term projects this raises operating costs; payroll now represents ~22–25% of project budgets on large integrated contracts. Failure to match market rates risks delays, higher subcontractor premiums, and scope re-bids.

Raw Material and Commodity Volatility

Suppliers of bitumen, steel, and concrete exert moderate power: global commodity pricing drove steel up 25% in 2021–22 and bitumen volatility spiked 18% in 2022, while concrete shortages in Australia in 2023 caused 10–15% regional price jumps.

Downer uses bulk purchasing and rise-and-fall clauses; hedging reduced input-cost swings by ~6% in 2024, yet localized disruptions can still trigger short-term margin pressure.

Subcontractor Dependency

The reliance on specialized subcontractors for niche components gives them outsized bargaining power; for example, in 2024 Downer Group reported subcontractor costs at ~38% of revenue, and shortages pushed some civil subcontract rates up 12–18% in Australia in 2023–24. In high-demand periods those subcontractors can switch to rivals, raising procurement costs and squeezing margins, so tight supplier contracts and dual-sourcing are critical to protect timelines and margin integrity.

Technology and Fleet Providers

As Downer digitizes operations, specialized asset-management software and heavy-equipment OEMs gain leverage; global construction-tech VC funding hit US$29.8bn in 2024, boosting supplier innovation and pricing power.

Shifting to electric/hydrogen fleets concentrates power: only a few OEMs supply heavy EV/hydrogen trucks and electrolyzers, raising switching costs and forcing multi-year contracts.

Long-term strategic partnerships lock in software updates, support SLAs, and cap capex volatility—typical fleet supply contracts run 5–10 years with 10–20% upgrade clauses.

- Specialized software suppliers rising influence

- EV/hydrogen OEMs limited, high bargaining power

- Multi-year (5–10y) contracts common

- 2024 construction-tech VC: US$29.8bn

Energy and Fuel Inputs

The high energy intensity of Downer Group’s transport and construction ops makes it sensitive to fuel and utility pricing; diesel accounted for about 12–18% of operating costs in comparable contractors in 2024.

Australia’s renewable rollout is led by a few large firms—AGL, Origin Energy, and the big gentailers—so green energy at scale remains concentrated, raising supplier leverage.

Downer mitigates exposure via long-term power purchase agreements (PPAs); a 10–15 year PPA can cut electricity price volatility and cap energy OPEX.

- Diesel ≈12–18% of ops costs (peer FY2024)

- Major renewables market share: top 3 gentailers

- Preferred fix: 10–15 year PPAs to stabilize OPEX

Supplier pressure pinches Downer: wages, subcontractor costs & fuel risk squeeze margins

Supplier power for Downer is moderate-to-high: skilled labor shortages (Australia trades vacancy 3.8% Nov 2025; NZ 4.2% Q3 2025) and wage inflation (~4.6% Australia, 5.1% NZ in 2025) push payroll to ~22–25% of project budgets; subcontractor spend ~38% of revenue (2024) with rates up 12–18% in 2023–24; commodity and energy volatility (diesel ≈12–18% ops costs) add margin risk, so long-term contracts, hedges, and dual-sourcing are critical.

| Metric | Value |

|---|---|

| AU trades vacancy | 3.8% (Nov 2025) |

| NZ trades vacancy | 4.2% (Q3 2025) |

| Wage growth | AU 4.6%, NZ 5.1% (2025) |

| Payroll share | 22–25% of project budgets |

| Subcontractor share | ~38% of revenue (2024) |

| Subcontractor rate rise | 12–18% (2023–24) |

| Diesel/Ops | ≈12–18% (peers FY2024) |

What is included in the product

Concise Five Forces assessment focused on Downer’scompetitive dynamics, highlighting supplier/buyer power, rivalry intensity, entry barriers, substitutes, and emerging disruptors with strategic implications for pricing and profitability.

Downer Porter’s Five Forces condensed into a one-sheet, letting teams quickly gauge competitive pressure and make strategic choices without sifting through reports.

Customers Bargaining Power

Government Procurement Dominance

State and federal governments in Australia and New Zealand account for roughly 40–60% of Downer’s revenue mix, giving them outsized bargaining power through transparent, competitive tenders that heavily weight cost-efficiency and social value (e.g., Indigenous procurement targets, carbon reduction clauses).

Rigorous Contractual Terms

Large institutional and government clients often impose contractual terms that shift operational and financial risk to Downer, including liquidated damages—recent Australian infrastructure contracts show median LD clauses of A$250k–A$1m per month—and strict KPIs tied to payment; in FY2024 Downer reported A$52m in contract provisions linked to performance risk, so negotiating risk-sharing (capped LDs, shared delay clauses, gainshare) is a key competitive edge that can protect margins and cash flow.

Low Switching Costs at Contract Expiry

When a Downer maintenance or service contract expires, clients often run a new tender and can switch to rivals with minimal friction, driving a steady cycle of competitive bids; Australian federal procurement data shows 42% of infrastructure service contracts changed suppliers at renewal in 2023. Incumbents must repeatedly prove technical capability and cost-effectiveness, so loyalty ranks below proposal quality and price, pressuring margins and forcing continuous efficiency gains.

Demand for ESG Compliance

Modern clients require rigorous ESG (environmental, social, governance) reporting to qualify for contracts, with 72% of infrastructure tenders in Australia by 2024 citing ESG criteria and 40% applying minimum carbon targets.

That demand lets customers set standards on emissions and diversity, pushing Downer to meet decarbonisation timelines and 30%+ diverse workforce metrics or risk losing bids.

Failure to comply can cut access to major pipelines: public sector projects worth A$45bn (2024–25) increasingly prequalify only ESG-compliant firms.

- 72% of infra tenders include ESG (Australia, 2024)

- 40% apply carbon targets (2024)

- 30%+ diversity benchmarks common

- Public project pipeline A$45bn (2024–25)

Market Transparency and Benchmarking

Clients hiring independent consultants to benchmark service costs—industry average margins often 6–12% in 2024 for infrastructure services—caps Downer’s ability to charge premiums.

Customers access public data on labor rates (AUS avg. construction wage A$48/hr in 2024) and commodity prices, so high margins are visible and contested.

That transparency forces price sensitivity; operational efficiency (productivity, unit costs) becomes the main competitive lever.

- Consultant benchmarks limit premium pricing.

- Visible wages A$48/hr and 6–12% sector margins (2024).

- Transparency increases price pressure.

- Efficiency drives win rates and margins.

Public-sector clout squeezes Downer: tight margins, heavy ESG & penalty risks

Customers—especially Australian and NZ governments (40–60% of revenue)—hold strong bargaining power via competitive tenders, strict KPIs, liquidated damages (median A$250k–A$1m/month) and ESG prequalification (72% tenders, 40% carbon targets), forcing Downer to accept tight margins (industry 6–12%), meet A$48/hr wage transparency, and continually improve efficiency to win contracts.

| Metric | Value (2024) |

|---|---|

| Public revenue share | 40–60% |

| LD median | A$250k–A$1m/month |

| ESG tenders | 72% |

| Carbon targets in tenders | 40% |

| Sector margins | 6–12% |

| Avg construction wage (AUS) | A$48/hr |

| Public project pipeline | A$45bn (2024–25) |

Full Version Awaits

Downer Porter's Five Forces Analysis

This preview shows the exact Downer Porter’s Five Forces analysis you’ll receive—no placeholders or mockups—fully formatted and ready for immediate download after purchase.