Dream Finders SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Dream Finders shows strong regional brand recognition and a diversified development pipeline, but faces margin pressure from rising material costs and competitive land constraints; our full SWOT unpacks these dynamics with financial context and strategic recommendations—purchase the complete report for an editable, investor-ready Word and Excel package to support planning, pitches, and decisions.

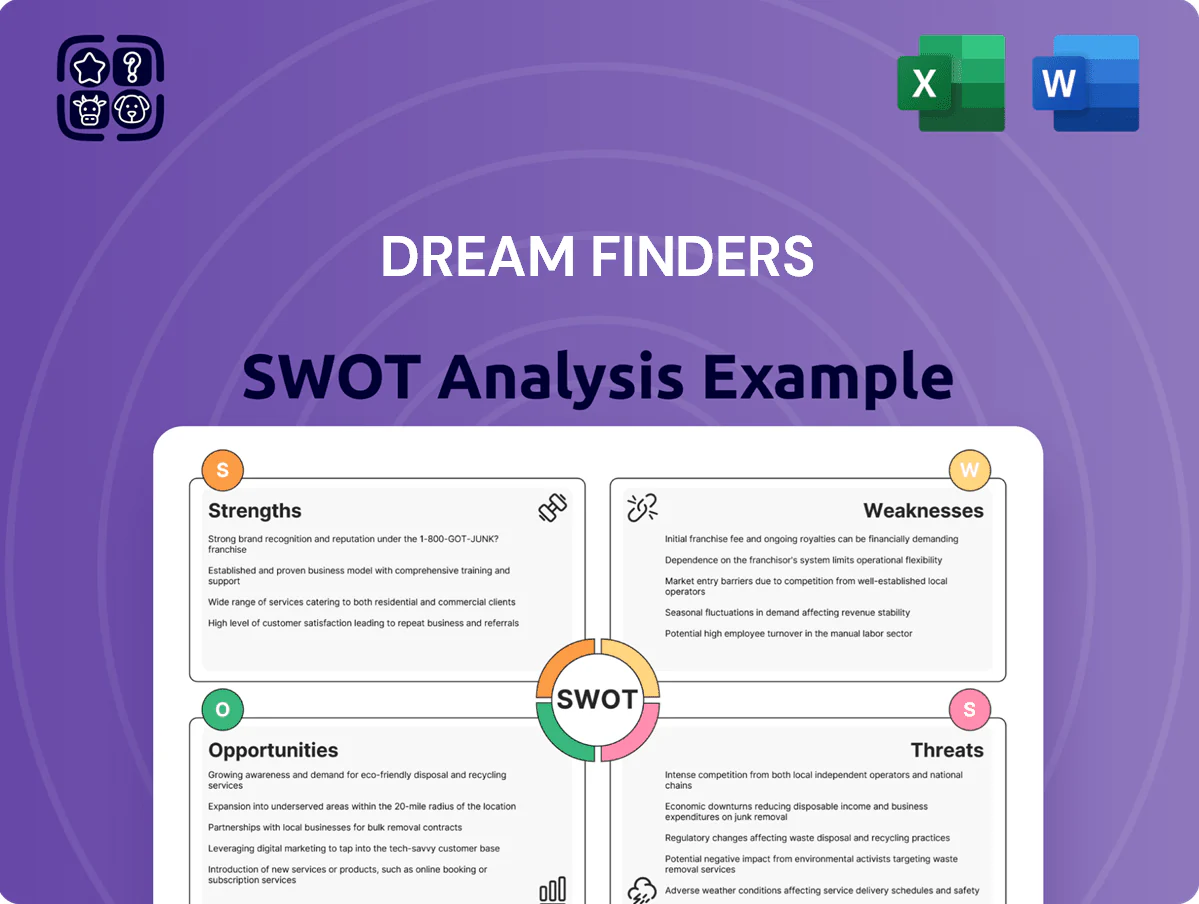

Strengths

Asset-Light Land Acquisition Model

Dream Finders homes uses land purchase options instead of owning large tracts, cutting upfront land capital and improving liquidity; as of FY2024 it reported land (owned) at $210M vs optioned lots representing ~40% of community pipeline, lowering capital at risk.

This asset-light approach drives faster inventory turnover—average lot-to-close cycle ~9 months vs industry ~14—and lifted ROE to 18% in 2024, above the 12% peer median.

By avoiding heavy carrying costs, the company keeps a flexible balance sheet: net debt/EBITDA was about 1.8x in FY2024, providing resilience to price swings and enabling quicker scale-up when demand returns.

Dominant Presence in High-Growth Sunbelt Markets

Dream Finders’ strategic footprint across the Sunbelt—notably Florida, Texas, Arizona, and the Carolinas—captures strong 2025 net migration: Florida +220k, Texas +150k, Arizona +45k (Census Bureau, 2025), and local job growth above national 2025 payrolls by ~1.2–2.5 percentage points, supporting higher new-home absorption than the 2025 national new-home sales decline of ~5%.

Integrated Mortgage and Title Services

Dream Finders Homes offers in-house mortgage and title services, creating a seamless buyer journey and shortening average closing times (reported industry-wide at 42 days; internal targets often under 35 days). This vertical integration adds high-margin fee income—mortgage/title combined can boost per-home gross margin by an estimated $3,000–$6,000 based on 2024 market averages. Managing financing lets the firm structure tailored incentives and seller-credit packages to capture buyers in tight markets, raising conversion and retention rates.

Proven Track Record of M&A Integration

Dream Finders Homes' leadership has acquired and integrated seven regional builders since 2019, adding roughly 2,400 homes of annual capacity and boosting revenue from $1.2B in 2018 to $2.1B in 2024.

Integrations shortened market entry time to under 9 months on average, delivered immediate accretive EBITDA margins (up ~220 basis points), and expanded presence in the Mid-Atlantic and Southwest.

- 7 acquisitions since 2019

- +2,400 annual home capacity

- Revenue: $1.2B (2018) → $2.1B (2024)

- Integration <9 months, +220 bp EBITDA

Diversified Product Portfolio for Various Segments

Dream Finders Homes designs for entry-level, first-time move-up, and active-adult buyers, spreading demand across price bands and reducing exposure to any single segment.

This mix lets the company match home types and density to land value, improving average lot yield; in 2024 Dream Finders delivered ~4,100 homes, showing scale across segments.

- Segments: entry, move-up, active-adult

- 2024 deliveries: ~4,100 homes

- Mitigates single-segment downturn risk

- Maximizes land utility via density/product fit

Sunbelt-focused, asset-light homebuilder: $210M land, faster closes, 18% ROE

Asset-light land options (owned land $210M, ~40% optioned lots), faster lot-to-close ~9 vs 14 months, ROE 18% (2024), net debt/EBITDA ~1.8x (2024), Sunbelt footprint capturing 2025 net migration (FL +220k, TX +150k, AZ +45k), in-house mortgage/title adds $3k–$6k per home, 7 acquisitions since 2019 (+2,400 capacity), 2024 deliveries ~4,100 homes.

| Metric | Value |

|---|---|

| Owned land | $210M |

| Optioned lots | ~40% pipeline |

| Lot-to-close | ~9 months |

| ROE (2024) | 18% |

| Net debt/EBITDA (2024) | ~1.8x |

| Deliveries (2024) | ~4,100 |

What is included in the product

Delivers a concise SWOT overview of Dream Finders, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a focused Dream Finders SWOT snapshot that speeds strategic alignment and eases stakeholder communication.

Weaknesses

High Leverage and Debt Obligations

The aggressive growth and acquisitions left Dream Finders Homes with about $1.1 billion in long-term debt as of 2024 year-end, forcing sizable interest and principal payments that eat into operating cash flow.

If U.S. housing starts drop and gross margins compress, free cash flow could turn negative, straining servicing capacity and raising default or covenant risk.

High leverage also narrows financing options: lenders may demand higher spreads or covenants, slowing or raising cost for future land buys and project pivots.

Dependency on Third-Party Land Developers

Dream Finders Homes depends heavily on third-party land developers for lot delivery, exposing it to schedule slips and partner insolvency; in 2024 roughly 28% of its lots came via option agreements, so a 3–6 month delay can cut quarterly closings materially. Such upstream lack of control raises supply-chain risk and could force price concessions or cancellations, hurting margins and revenue growth if partner stress rises during tighter credit cycles.

Sensitivity to Interest Rate Fluctuations

As a builder targeting entry-level buyers, Dream Finders is highly exposed to mortgage rate moves; a 1 percentage-point rise in 30-year rates (to ~7% in late 2024) can price out buyers who need <20% down, cutting demand sharply.

Even small rate upticks raised cancellations industry-wide to ~15–20% in 2023–24, forcing Dream Finders into costly rate buy-downs and incentives that can compress gross margins by 200–400 basis points.

Operational Complexity from Rapid Expansion

Rapid geographic expansion at Dream Finders Homes has created operational complexity: by FY2024 revenue rose ~48% to $1.3B while SG&A grew 62%, showing strain on back-office capacity.

Maintaining consistent quality across regions requires stronger oversight—customer complaints rose 22% Y/Y in 2024, indicating lapses in standards and training.

Procurement and local management inefficiencies appear: build-period variances widened to +14 days on average in 2024 when compared to 2022.

- Revenue +48% to $1.3B (FY2024) vs SG&A +62%

- Customer complaints +22% Y/Y (2024)

- Average build-delay variance +14 days (2024)

Concentration Risk in Specific Regions

- ~70% Sunbelt concentration

- 10% local sales shock ≈ 7% corporate revenue hit

- Vulnerable to state tax and climate shifts

High leverage, Sunbelt concentration and rising cancellations squeeze margins and cash flow

High leverage (~$1.1B LT debt at 2024 year-end) strains cash flow and raises covenant/default risk; a 1ppt rate rise to ~7% in late 2024 cut demand and lifted cancellations to ~15–20%, squeezing margins 200–400bps. Rapid expansion lifted revenue +48% to $1.3B while SG&A +62%, driving ops slip (build delays +14 days, complaints +22%). Concentration: ~70% Sunbelt exposure; 10% state sales shock ≈7% corporate revenue hit.

| Metric | 2024 |

|---|---|

| Revenue | $1.3B (+48%) |

| Long-term debt | $1.1B |

| SG&A growth | +62% |

| Build delays | +14 days |

| Complaints | +22% Y/Y |

| Cancellation rate | 15–20% |

| Sunbelt concentration | ~70% |

Same Document Delivered

Dream Finders SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is the real document you'll download post-purchase. Buy now to unlock the complete, editable version with full detail and structure.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Dream Finders shows strong regional brand recognition and a diversified development pipeline, but faces margin pressure from rising material costs and competitive land constraints; our full SWOT unpacks these dynamics with financial context and strategic recommendations—purchase the complete report for an editable, investor-ready Word and Excel package to support planning, pitches, and decisions.

Strengths

Asset-Light Land Acquisition Model

Dream Finders homes uses land purchase options instead of owning large tracts, cutting upfront land capital and improving liquidity; as of FY2024 it reported land (owned) at $210M vs optioned lots representing ~40% of community pipeline, lowering capital at risk.

This asset-light approach drives faster inventory turnover—average lot-to-close cycle ~9 months vs industry ~14—and lifted ROE to 18% in 2024, above the 12% peer median.

By avoiding heavy carrying costs, the company keeps a flexible balance sheet: net debt/EBITDA was about 1.8x in FY2024, providing resilience to price swings and enabling quicker scale-up when demand returns.

Dominant Presence in High-Growth Sunbelt Markets

Dream Finders’ strategic footprint across the Sunbelt—notably Florida, Texas, Arizona, and the Carolinas—captures strong 2025 net migration: Florida +220k, Texas +150k, Arizona +45k (Census Bureau, 2025), and local job growth above national 2025 payrolls by ~1.2–2.5 percentage points, supporting higher new-home absorption than the 2025 national new-home sales decline of ~5%.

Integrated Mortgage and Title Services

Dream Finders Homes offers in-house mortgage and title services, creating a seamless buyer journey and shortening average closing times (reported industry-wide at 42 days; internal targets often under 35 days). This vertical integration adds high-margin fee income—mortgage/title combined can boost per-home gross margin by an estimated $3,000–$6,000 based on 2024 market averages. Managing financing lets the firm structure tailored incentives and seller-credit packages to capture buyers in tight markets, raising conversion and retention rates.

Proven Track Record of M&A Integration

Dream Finders Homes' leadership has acquired and integrated seven regional builders since 2019, adding roughly 2,400 homes of annual capacity and boosting revenue from $1.2B in 2018 to $2.1B in 2024.

Integrations shortened market entry time to under 9 months on average, delivered immediate accretive EBITDA margins (up ~220 basis points), and expanded presence in the Mid-Atlantic and Southwest.

- 7 acquisitions since 2019

- +2,400 annual home capacity

- Revenue: $1.2B (2018) → $2.1B (2024)

- Integration <9 months, +220 bp EBITDA

Diversified Product Portfolio for Various Segments

Dream Finders Homes designs for entry-level, first-time move-up, and active-adult buyers, spreading demand across price bands and reducing exposure to any single segment.

This mix lets the company match home types and density to land value, improving average lot yield; in 2024 Dream Finders delivered ~4,100 homes, showing scale across segments.

- Segments: entry, move-up, active-adult

- 2024 deliveries: ~4,100 homes

- Mitigates single-segment downturn risk

- Maximizes land utility via density/product fit

Sunbelt-focused, asset-light homebuilder: $210M land, faster closes, 18% ROE

Asset-light land options (owned land $210M, ~40% optioned lots), faster lot-to-close ~9 vs 14 months, ROE 18% (2024), net debt/EBITDA ~1.8x (2024), Sunbelt footprint capturing 2025 net migration (FL +220k, TX +150k, AZ +45k), in-house mortgage/title adds $3k–$6k per home, 7 acquisitions since 2019 (+2,400 capacity), 2024 deliveries ~4,100 homes.

| Metric | Value |

|---|---|

| Owned land | $210M |

| Optioned lots | ~40% pipeline |

| Lot-to-close | ~9 months |

| ROE (2024) | 18% |

| Net debt/EBITDA (2024) | ~1.8x |

| Deliveries (2024) | ~4,100 |

What is included in the product

Delivers a concise SWOT overview of Dream Finders, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a focused Dream Finders SWOT snapshot that speeds strategic alignment and eases stakeholder communication.

Weaknesses

High Leverage and Debt Obligations

The aggressive growth and acquisitions left Dream Finders Homes with about $1.1 billion in long-term debt as of 2024 year-end, forcing sizable interest and principal payments that eat into operating cash flow.

If U.S. housing starts drop and gross margins compress, free cash flow could turn negative, straining servicing capacity and raising default or covenant risk.

High leverage also narrows financing options: lenders may demand higher spreads or covenants, slowing or raising cost for future land buys and project pivots.

Dependency on Third-Party Land Developers

Dream Finders Homes depends heavily on third-party land developers for lot delivery, exposing it to schedule slips and partner insolvency; in 2024 roughly 28% of its lots came via option agreements, so a 3–6 month delay can cut quarterly closings materially. Such upstream lack of control raises supply-chain risk and could force price concessions or cancellations, hurting margins and revenue growth if partner stress rises during tighter credit cycles.

Sensitivity to Interest Rate Fluctuations

As a builder targeting entry-level buyers, Dream Finders is highly exposed to mortgage rate moves; a 1 percentage-point rise in 30-year rates (to ~7% in late 2024) can price out buyers who need <20% down, cutting demand sharply.

Even small rate upticks raised cancellations industry-wide to ~15–20% in 2023–24, forcing Dream Finders into costly rate buy-downs and incentives that can compress gross margins by 200–400 basis points.

Operational Complexity from Rapid Expansion

Rapid geographic expansion at Dream Finders Homes has created operational complexity: by FY2024 revenue rose ~48% to $1.3B while SG&A grew 62%, showing strain on back-office capacity.

Maintaining consistent quality across regions requires stronger oversight—customer complaints rose 22% Y/Y in 2024, indicating lapses in standards and training.

Procurement and local management inefficiencies appear: build-period variances widened to +14 days on average in 2024 when compared to 2022.

- Revenue +48% to $1.3B (FY2024) vs SG&A +62%

- Customer complaints +22% Y/Y (2024)

- Average build-delay variance +14 days (2024)

Concentration Risk in Specific Regions

- ~70% Sunbelt concentration

- 10% local sales shock ≈ 7% corporate revenue hit

- Vulnerable to state tax and climate shifts

High leverage, Sunbelt concentration and rising cancellations squeeze margins and cash flow

High leverage (~$1.1B LT debt at 2024 year-end) strains cash flow and raises covenant/default risk; a 1ppt rate rise to ~7% in late 2024 cut demand and lifted cancellations to ~15–20%, squeezing margins 200–400bps. Rapid expansion lifted revenue +48% to $1.3B while SG&A +62%, driving ops slip (build delays +14 days, complaints +22%). Concentration: ~70% Sunbelt exposure; 10% state sales shock ≈7% corporate revenue hit.

| Metric | 2024 |

|---|---|

| Revenue | $1.3B (+48%) |

| Long-term debt | $1.1B |

| SG&A growth | +62% |

| Build delays | +14 days |

| Complaints | +22% Y/Y |

| Cancellation rate | 15–20% |

| Sunbelt concentration | ~70% |

Same Document Delivered

Dream Finders SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get, and the file shown is the real document you'll download post-purchase. Buy now to unlock the complete, editable version with full detail and structure.