Diamondrock Hospitality PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and evolving consumer trends are reshaping Diamondrock Hospitality’s strategic landscape—our concise PESTLE highlights key risks and opportunities you need to know. Use these insights to refine investment theses, stress-test forecasts, or build competitive strategies. Buy the full PESTLE for the complete, actionable breakdown in editable formats and get instant clarity for smarter decisions.

Political factors

Federal Tax Policy and REIT Status

DiamondRock must strictly follow federal tax rules to retain REIT status and avoid entity-level taxation; in 2024 REITs distributed 90%+ of taxable income to shareholders to qualify, and any failure risks corporate tax at 21% federal rate.

By end-2025, proposed shifts to corporate tax rates or changes to the dividends paid deduction could alter free cash flow; a 1 percentage-point rise in effective tax could cut distributable cash by millions given DiamondRock’s 2024 FFO of roughly $1.10 per share.

Maintaining compliance preserves the pass-through tax advantage central to DiamondRock’s capital allocation and investor yield, where 2024 dividend yield averaged near 5.5% for lodging REIT peers.

Geopolitical Stability and International Travel

DiamondRock’s luxury urban portfolio is highly sensitive to geopolitical stability; Europe and Asia account for over 40% of inbound high-yield business and leisure travelers to major gateways, so political unrest can depress ADRs—London ADR fell 18% in Q3 2023 during strikes and instability, while Hong Kong ADR dropped 22% in 2019 protests.

Local Zoning and Land Use Regulations

Development and renovation projects in New York and Boston face layered zoning boards and community review; delays can add 12–24 months and 5–15% cost overruns, impacting DiamondRock Hospitality's planned capital expenditures (2024 capex guidance ~$90–110M). Changes in municipal leadership have recently tightened hotel conversion rules, risking reduced room counts and lower RevPAR in core markets. Proactive engagement with local councils is essential to protect NAV and execute $50–80M multi-year improvement plans.

Trade Policies and Supply Chain Costs

International trade agreements and tariffs affect the cost of FF&E for DiamondRock Hospitality; import duties added 8–12% to FF&E invoices in 2024–25, raising renovation costs across the portfolio.

Trade volatility in late 2025 forced a 6–9% increase in projected capital expenditures to preserve luxury standards, straining budgets for planned property upgrades.

Political tariff shifts risk causing single-project cost overruns of $0.5–2.0 million per hotel, depending on scope and sourcing.

- Tariff impact: +8–12% on FF&E (2024–25)

- CapEx uplift: +6–9% (late 2025)

- Potential overrun: $0.5–2.0M per property

Visa Processing and Immigration Reform

The hospitality sector depends on immigrant labor and guest-worker visas; U.S. H-2B caps (66,000 in 2024) and processing backlogs raised labor costs for operators like DiamondRock, where labor is ~30–40% of operating expenses in 2023–24 for the sector.

Delays in tourist visa processing reduced international arrivals; U.S. inbound travel was ~90% of 2019 levels by 2024, but group/convention recovery lags, cutting RevPAR recovery in major convention markets by ~5–10% vs. leisure-driven markets.

Policy shifts toward streamlined visa processing could lower recruitment costs and boost demand, while restrictive reforms would raise wages, increase F&B and housekeeping costs, and compress margins.

- H-2B cap 66,000 (2024)

- Labor ~30–40% of ops expenses

- U.S. inbound travel ~90% of 2019 by 2024

- Group/convention RevPAR -5–10% vs. leisure

DiamondRock Faces Tax, Tariff and Labor Risks Threatening 2024–25 FFO & Dividends

Political risks for DiamondRock include REIT tax compliance (2024: 90%+ distribution rule; federal corporate tax 21%), potential tax changes affecting FFO (~$1.10/sh 2024), tariff-driven FF&E cost uplifts (+8–12% 2024–25) and late-2025 capex increases (+6–9%), H-2B cap 66,000 (2024) raising labor costs (~30–40% of Opex) and visa/backlog-driven RevPAR headwinds (U.S. inbound ~90% of 2019 by 2024).

| Metric | Value |

|---|---|

| FFO per share (2024) | $1.10 |

| Dividend yield (lodging peers 2024) | ~5.5% |

| Tariff impact (FF&E) | +8–12% |

| CapEx uplift (late 2025) | +6–9% |

| H-2B cap (2024) | 66,000 |

What is included in the product

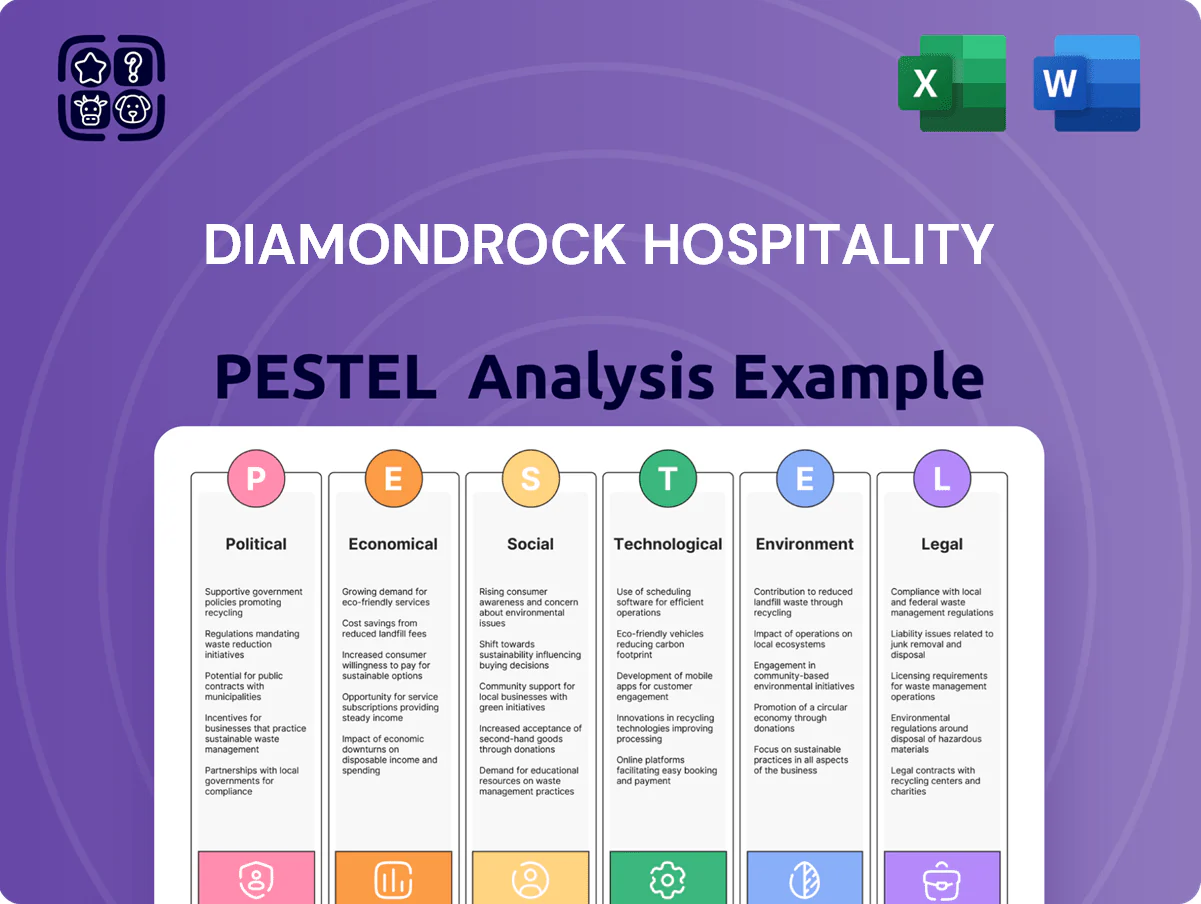

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically shape DiamondRock Hospitality’s operating landscape, backed by current market data and regional regulatory trends to identify risks and growth opportunities.

A concise, shareable PESTLE summary of DiamondRock Hospitality that highlights key political, economic, social, technological, legal, and environmental impacts for quick team alignment and presentation-ready insertion.

Economic factors

Interest Rate Environment and Financing

As a capital-intensive REIT, DiamondRock is highly sensitive to Fed-driven rates; the Fed funds target rose to 5.25–5.50% by Dec 2023 and remained elevated through 2025, pushing 2024 interest expense higher—DiamondRock reported $110m net interest expense in FY2024. High rates increase costs on floating-rate debt and can compress cap rates on acquisitions, so strategic refinancing (locked fixed-rate debt; 4.5% average fixed debt reported 2024) and a strong balance sheet are critical to mitigate pressure.

Inflation and Pricing Power

Sustained inflation—US CPI rose 3.4% in 2024 YTD—raises DiamondRock Hospitality operating costs such as utilities, insurance, and F&B, compressing margins if unrecovered.

Daily dynamic pricing and revenue management enable room-rate adjustments; the company reported a 2024 ADR of about $200, helping offset cost inflation.

Luxury positioning supports premium ADR and RevPAR resilience: DiamondRock’s 2024 RevPAR growth of ~8% shows pricing power amid fluctuating consumer purchasing power.

Labor Market Dynamics and Wage Growth

The hospitality sector faces a tight labor market, with US leisure and hospitality employment still about 300k below pre‑pandemic levels as of Dec 2025, driving average hourly earnings up ~6% YoY in 2024–25; DiamondRock must work with third‑party operators to absorb or pass through wage inflation to protect property EBITDA margins (2024 FFO/share grew 8% but margin pressure persists). Labor shortages in resort markets like Maui and Aspen reduce service capacity and can lower RevPAR by several percentage points during peak season.

Consumer Discretionary Spending Trends

Demand for DiamondRock's upscale properties tracks high-end consumer spending and corporate margins; in 2024 US top 10% household consumption rose ~4.2% while corporate profit margins hovered near 11%, supporting premium ADRs.

Economic downturns cut leisure travel and events—2020-2022 showed RevPAR declines up to 45% in shocks; a softening consumer confidence index (CFI down from 103 to 90 in 2024) signals downside risk.

By end-2025 monitor the wealth effect: US equity market cap fell ~6% in 2024, and a 10% equity decline historically reduces high-end travel demand materially for luxury resorts.

- Upscale demand tied to top-decile spending and corporate margins

- CFI and equity markets are leading indicators for luxury RevPAR

- Past shocks show RevPAR vulnerability (up to -45%)

Currency Fluctuations

A strong US dollar in 2024 reduced international inbound travel; US DOT data show international arrivals down 3.5% YoY through Q3 2024, pressuring DiamondRock’s gateway city hotels versus cheaper international alternatives and encouraging outbound U.S. travel.

Currency volatility shifted DiamondRock’s guest mix—domestic stays rose ~4% while international room nights declined—contributing to a 2.1% drag on RevPAR in 2024 vs. 2023.

Hedging options and targeted marketing in FX-impacted feeder markets can mitigate near-term RevPAR exposure as FX swings remain elevated, with USD trade-weighted index up ~6% year-over-year through Dec 2024.

- Intl arrivals -3.5% YoY (through Q3 2024)

- Domestic stays +4% for DiamondRock in 2024

- Estimated RevPAR impact -2.1% YoY

- USD trade-weighted index +6% YoY (Dec 2024)

Strong RevPAR and ADR offset rising rates and FX headwinds in FY2024

High rates raised FY2024 net interest expense to $110m; average fixed debt ~4.5%. 2024 ADR ~$200; RevPAR +8% (2024). US CPI +3.4% YTD 2024; labor costs +6% YoY 2024–25. Intl arrivals -3.5% through Q3 2024; domestic stays +4%; USD TWI +6% YoY (Dec 2024).

| Metric | Value |

|---|---|

| Net interest expense FY2024 | $110m |

| Avg fixed debt rate 2024 | 4.5% |

| ADR 2024 | $200 |

| RevPAR growth 2024 | +8% |

| CPI 2024 YTD | +3.4% |

| Intl arrivals | -3.5% (Q3 2024) |

| USD TWI Dec 2024 | +6% YoY |

Preview the Actual Deliverable

Diamondrock Hospitality PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains the complete PESTLE analysis of DiamondRock Hospitality with political, economic, social, technological, legal, and environmental factors clearly structured for immediate application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, and evolving consumer trends are reshaping Diamondrock Hospitality’s strategic landscape—our concise PESTLE highlights key risks and opportunities you need to know. Use these insights to refine investment theses, stress-test forecasts, or build competitive strategies. Buy the full PESTLE for the complete, actionable breakdown in editable formats and get instant clarity for smarter decisions.

Political factors

Federal Tax Policy and REIT Status

DiamondRock must strictly follow federal tax rules to retain REIT status and avoid entity-level taxation; in 2024 REITs distributed 90%+ of taxable income to shareholders to qualify, and any failure risks corporate tax at 21% federal rate.

By end-2025, proposed shifts to corporate tax rates or changes to the dividends paid deduction could alter free cash flow; a 1 percentage-point rise in effective tax could cut distributable cash by millions given DiamondRock’s 2024 FFO of roughly $1.10 per share.

Maintaining compliance preserves the pass-through tax advantage central to DiamondRock’s capital allocation and investor yield, where 2024 dividend yield averaged near 5.5% for lodging REIT peers.

Geopolitical Stability and International Travel

DiamondRock’s luxury urban portfolio is highly sensitive to geopolitical stability; Europe and Asia account for over 40% of inbound high-yield business and leisure travelers to major gateways, so political unrest can depress ADRs—London ADR fell 18% in Q3 2023 during strikes and instability, while Hong Kong ADR dropped 22% in 2019 protests.

Local Zoning and Land Use Regulations

Development and renovation projects in New York and Boston face layered zoning boards and community review; delays can add 12–24 months and 5–15% cost overruns, impacting DiamondRock Hospitality's planned capital expenditures (2024 capex guidance ~$90–110M). Changes in municipal leadership have recently tightened hotel conversion rules, risking reduced room counts and lower RevPAR in core markets. Proactive engagement with local councils is essential to protect NAV and execute $50–80M multi-year improvement plans.

Trade Policies and Supply Chain Costs

International trade agreements and tariffs affect the cost of FF&E for DiamondRock Hospitality; import duties added 8–12% to FF&E invoices in 2024–25, raising renovation costs across the portfolio.

Trade volatility in late 2025 forced a 6–9% increase in projected capital expenditures to preserve luxury standards, straining budgets for planned property upgrades.

Political tariff shifts risk causing single-project cost overruns of $0.5–2.0 million per hotel, depending on scope and sourcing.

- Tariff impact: +8–12% on FF&E (2024–25)

- CapEx uplift: +6–9% (late 2025)

- Potential overrun: $0.5–2.0M per property

Visa Processing and Immigration Reform

The hospitality sector depends on immigrant labor and guest-worker visas; U.S. H-2B caps (66,000 in 2024) and processing backlogs raised labor costs for operators like DiamondRock, where labor is ~30–40% of operating expenses in 2023–24 for the sector.

Delays in tourist visa processing reduced international arrivals; U.S. inbound travel was ~90% of 2019 levels by 2024, but group/convention recovery lags, cutting RevPAR recovery in major convention markets by ~5–10% vs. leisure-driven markets.

Policy shifts toward streamlined visa processing could lower recruitment costs and boost demand, while restrictive reforms would raise wages, increase F&B and housekeeping costs, and compress margins.

- H-2B cap 66,000 (2024)

- Labor ~30–40% of ops expenses

- U.S. inbound travel ~90% of 2019 by 2024

- Group/convention RevPAR -5–10% vs. leisure

DiamondRock Faces Tax, Tariff and Labor Risks Threatening 2024–25 FFO & Dividends

Political risks for DiamondRock include REIT tax compliance (2024: 90%+ distribution rule; federal corporate tax 21%), potential tax changes affecting FFO (~$1.10/sh 2024), tariff-driven FF&E cost uplifts (+8–12% 2024–25) and late-2025 capex increases (+6–9%), H-2B cap 66,000 (2024) raising labor costs (~30–40% of Opex) and visa/backlog-driven RevPAR headwinds (U.S. inbound ~90% of 2019 by 2024).

| Metric | Value |

|---|---|

| FFO per share (2024) | $1.10 |

| Dividend yield (lodging peers 2024) | ~5.5% |

| Tariff impact (FF&E) | +8–12% |

| CapEx uplift (late 2025) | +6–9% |

| H-2B cap (2024) | 66,000 |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental, and Legal—specifically shape DiamondRock Hospitality’s operating landscape, backed by current market data and regional regulatory trends to identify risks and growth opportunities.

A concise, shareable PESTLE summary of DiamondRock Hospitality that highlights key political, economic, social, technological, legal, and environmental impacts for quick team alignment and presentation-ready insertion.

Economic factors

Interest Rate Environment and Financing

As a capital-intensive REIT, DiamondRock is highly sensitive to Fed-driven rates; the Fed funds target rose to 5.25–5.50% by Dec 2023 and remained elevated through 2025, pushing 2024 interest expense higher—DiamondRock reported $110m net interest expense in FY2024. High rates increase costs on floating-rate debt and can compress cap rates on acquisitions, so strategic refinancing (locked fixed-rate debt; 4.5% average fixed debt reported 2024) and a strong balance sheet are critical to mitigate pressure.

Inflation and Pricing Power

Sustained inflation—US CPI rose 3.4% in 2024 YTD—raises DiamondRock Hospitality operating costs such as utilities, insurance, and F&B, compressing margins if unrecovered.

Daily dynamic pricing and revenue management enable room-rate adjustments; the company reported a 2024 ADR of about $200, helping offset cost inflation.

Luxury positioning supports premium ADR and RevPAR resilience: DiamondRock’s 2024 RevPAR growth of ~8% shows pricing power amid fluctuating consumer purchasing power.

Labor Market Dynamics and Wage Growth

The hospitality sector faces a tight labor market, with US leisure and hospitality employment still about 300k below pre‑pandemic levels as of Dec 2025, driving average hourly earnings up ~6% YoY in 2024–25; DiamondRock must work with third‑party operators to absorb or pass through wage inflation to protect property EBITDA margins (2024 FFO/share grew 8% but margin pressure persists). Labor shortages in resort markets like Maui and Aspen reduce service capacity and can lower RevPAR by several percentage points during peak season.

Consumer Discretionary Spending Trends

Demand for DiamondRock's upscale properties tracks high-end consumer spending and corporate margins; in 2024 US top 10% household consumption rose ~4.2% while corporate profit margins hovered near 11%, supporting premium ADRs.

Economic downturns cut leisure travel and events—2020-2022 showed RevPAR declines up to 45% in shocks; a softening consumer confidence index (CFI down from 103 to 90 in 2024) signals downside risk.

By end-2025 monitor the wealth effect: US equity market cap fell ~6% in 2024, and a 10% equity decline historically reduces high-end travel demand materially for luxury resorts.

- Upscale demand tied to top-decile spending and corporate margins

- CFI and equity markets are leading indicators for luxury RevPAR

- Past shocks show RevPAR vulnerability (up to -45%)

Currency Fluctuations

A strong US dollar in 2024 reduced international inbound travel; US DOT data show international arrivals down 3.5% YoY through Q3 2024, pressuring DiamondRock’s gateway city hotels versus cheaper international alternatives and encouraging outbound U.S. travel.

Currency volatility shifted DiamondRock’s guest mix—domestic stays rose ~4% while international room nights declined—contributing to a 2.1% drag on RevPAR in 2024 vs. 2023.

Hedging options and targeted marketing in FX-impacted feeder markets can mitigate near-term RevPAR exposure as FX swings remain elevated, with USD trade-weighted index up ~6% year-over-year through Dec 2024.

- Intl arrivals -3.5% YoY (through Q3 2024)

- Domestic stays +4% for DiamondRock in 2024

- Estimated RevPAR impact -2.1% YoY

- USD trade-weighted index +6% YoY (Dec 2024)

Strong RevPAR and ADR offset rising rates and FX headwinds in FY2024

High rates raised FY2024 net interest expense to $110m; average fixed debt ~4.5%. 2024 ADR ~$200; RevPAR +8% (2024). US CPI +3.4% YTD 2024; labor costs +6% YoY 2024–25. Intl arrivals -3.5% through Q3 2024; domestic stays +4%; USD TWI +6% YoY (Dec 2024).

| Metric | Value |

|---|---|

| Net interest expense FY2024 | $110m |

| Avg fixed debt rate 2024 | 4.5% |

| ADR 2024 | $200 |

| RevPAR growth 2024 | +8% |

| CPI 2024 YTD | +3.4% |

| Intl arrivals | -3.5% (Q3 2024) |

| USD TWI Dec 2024 | +6% YoY |

Preview the Actual Deliverable

Diamondrock Hospitality PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains the complete PESTLE analysis of DiamondRock Hospitality with political, economic, social, technological, legal, and environmental factors clearly structured for immediate application.