DSM-Firmenich Boston Consulting Group Matrix

Unlock Strategic Clarity

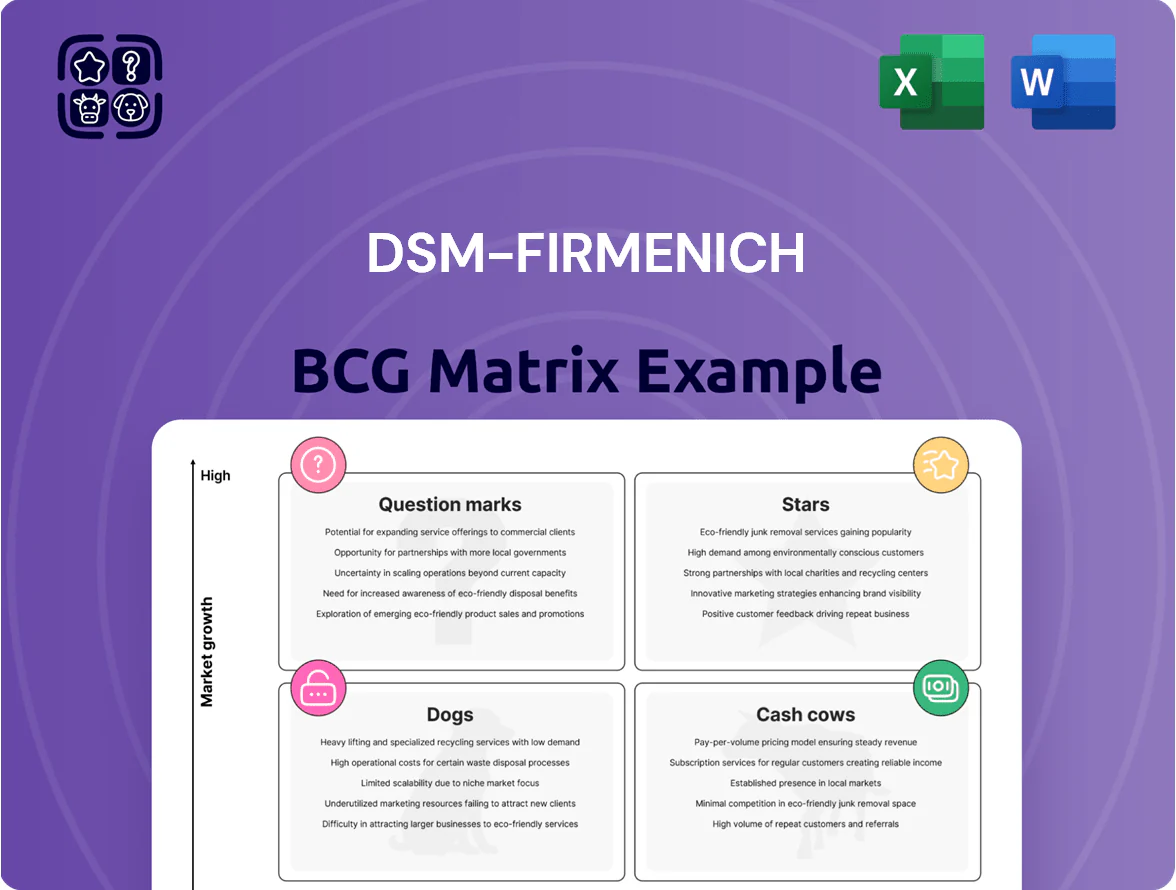

DSM‑Firmenich’s BCG Matrix preview highlights how its fragrance and nutrition portfolios balance growth and market share, hinting at Stars driving future expansion and Cash Cows funding R&D—while select lines may require divestment or repositioning.

Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Natural Fragrance and Beauty Ingredients

As clean-beauty demand peaks in late 2025, DSM-Firmenich’s Natural Fragrance and Beauty Ingredients (Stars) leads via sustainable extraction, capturing ~28% of the premium natural ingredients market and driving €420m in 2025 revenue for Perfumery & Beauty.

Firmenich perfumery plus DSM science secures leadership; R&D spend rose 22% YoY to €65m in 2025 to fend off biotech entrants and sustain product premiums.

High capex continues: €90m committed for 2026 facilities and bioprocess scale-up, keeping this unit the primary top-line growth engine within Perfumery & Beauty.

Plant-Based Texture and Taste Solutions

The shift to sustainable proteins grows ~20% CAGR (2024–30), and DSM-Firmenich has captured a leading share by closing the taste-texture gap in meat alternatives with enzymatic texturants plus advanced flavor systems.

The unit is the preferred partner for global food makers, supplying formulations used in over 35% of top-50 plant-based SKUs and driving €220m in segment revenue in 2025.

Significant capex—€150m planned 2025–27—scales fermentation and blending capacity to match rising demand and SKU churn.

As the alt-protein market matures toward 2030, this high-growth Stars unit is projected to convert to a cash cow with stable margins and >€300m annual EBITDA potential.

Biotech-Derived Human Milk Oligosaccharides

The HMO portfolio is a star: high-growth frontier in infant nutrition and adult gut health where DSM-Firmenich holds a pioneering market position, with global HMO market projected to reach $3.5bn by 2028 (CAGR ~12% from 2023). Advanced fermentation yields higher gross margins (estimated 25–35%) versus chemical routes and supports scalable supply. Ongoing R&D and ~€60–80m annual investment are needed to build clinical evidence and win approvals across APAC and LATAM. As gut health mainstreams, this star requires continued strategic capex and commercial focus.

Personalized Nutrition Platforms

Personalized Nutrition Platforms leverages data-driven diagnostics plus tailored supplement delivery to target the bespoke wellness market, using DSM-Firmenich’s 2024 ingredient library of >8,000 SKUs and 25%+ gross margins in direct-to-consumer models.

Digital health grew ~20% CAGR 2021–25, so DSM-Firmenich invests heavily in software and CAC; unit is cash-consuming but holds unrivaled market leadership and strategic tech-bio synergy.

- High growth: ~20% digital health CAGR (2021–25)

- Ingredient library: >8,000 SKUs (2024)

- Margins: 25%+ gross in DTC models

- Risks: high R&D and CAC, heavy cash burn

- Strategic: tech-biology synergy guides capex

Premium Fine Fragrance and Luxury Scent

Post-merger synergy with Firmenich has cemented DSM-Firmenich as a global leader in premium fine fragrance, capturing an estimated 22% luxury-market share in 2024 and benefiting from 6–8% CAGR in emerging markets (2020–24).

Exclusive contracts with top fashion houses sustain high barriers to entry; the unit reported ~€1.1bn revenue in FY2024 and double-digit gross margins, while ongoing marketing spend preserves brand premium.

Investment prioritizes creative talent and sustainable sourcing: 35% supplier traceability for key raw materials in 2024 and a €45m sustainability R&D budget through 2025 to protect prestige.

- Market share ~22% (2024)

- Unit revenue ~€1.1bn (FY2024)

- Emerging-market CAGR 6–8% (2020–24)

- €45m sustainability R&D through 2025

- 35% supplier traceability (2024)

DSM‑Firmenich Stars: €1.94bn revenue in 2025; >€300m EBITDA potential by 2030

DSM-Firmenich Stars: high-growth natural ingredients, alt-protein, HMO, and personalized nutrition units drove €1.94bn revenue in 2025, ~28% share in premium naturals, €420m Perfumery & Beauty, €220m plant-based, €300m HMO+personalized, R&D €65m, capex planned €240m (2025–27); projected >€300m annual EBITDA by 2030 as units mature.

| Metric | 2025 |

|---|---|

| Revenue (Stars) | €1.94bn |

| Premium naturals share | ~28% |

| Perfumery & Beauty | €420m |

| Plant-based | €220m |

| R&D spend | €65m |

| Planned capex 2025–27 | €240m |

| EBITDA potential (2030) | >€300m |

What is included in the product

BCG Matrix review of DSM‑Firmenich: quadrant summaries, strategic moves to invest, hold or divest, and trend‑driven competitive insights.

One-page DSM-Firmenich BCG Matrix placing each business unit in a quadrant for rapid portfolio decisions

Cash Cows

Core Vitamin and Mineral Premixes

Core Vitamin and Mineral Premixes sit as DSM-Firmenich cash cows: they hold a dominant global market share in essential human nutrition within a mature market, generating steady free cash flow—DSM-Firmenich’s nutrition division reported €2.1bn sales in 2024, with premixes a large contributor.

These products need little marketing or capex, so margins stay high; operating margin for vitamins was ~18% in 2024, funding R&D for question marks and stars.

Ongoing efficiency moves and supply-chain optimization cut COGS by an estimated 3–4% in 2023–24, further boosting EBITDA and enabling targeted innovation spend.

Classic Food Enzymes and Cultures

In mature dairy and baking markets, DSM-Firmenich’s Classic Food Enzymes and Cultures hold a dominant share—about 30–35% in specialty dairy cultures and ~25% in baking enzymes—supplying global food giants and ensuring steady, predictable demand.

With market growth under 3% annually, the unit emphasizes cash harvesting and high service levels, generating roughly €450–520 million EBITDA contribution in 2024 to fund debt service and dividends.

Standard Beverage Flavor Systems

Standard Beverage Flavor Systems sits in a saturated, low-growth market (~1–2% CAGR globally for traditional beverage flavors in 2024), yet DSM-Firmenich retains a large, loyal customer base across major soft drink and dairy makers.

High gross margins (mid-30s %) persist via long-term contracts and switching costs; customers face reformulation and regulatory retesting expenses often >$1m, keeping churn low.

Minimal capex needed—maintenance and incremental R&D only—so the unit reliably generates free cash flow, contributing roughly 18–22% of the Taste, Texture and Health division’s EBITDA in 2024.

Dietary Supplement Ingredients

Dietary Supplement Ingredients: DSM-Firmenich holds a leading volume position in mature categories like omega-3s and basic antioxidants, with global market share estimates around 12–15% for encapsulated omega-3s as of 2025 and mid-single-digit CAGR demand growth; scale and an integrated supply chain cut costs, helping protect margins despite intense price pressure.

These high-volume sales generate steady cash flow—estimated free cash conversion above 20% in 2024 for the nutrition segment—funding corporate infrastructure while capex is kept to essential maintenance and small process innovations to sustain efficiency.

- Leading volume position: ~12–15% omega-3s market share (2025)

- Demand growth: mid-single-digit CAGR

- Free cash conversion: >20% (2024, nutrition segment)

- Capex: limited to maintenance and process tweaks

Established Aroma Chemicals

Established Aroma Chemicals are a cash cow for DSM-Firmenich, supplying base aroma compounds for household and personal care with roughly 60% global market penetration and stable FY2024 sales near EUR 1.1bn, driven by massive scale and low unit costs.

Market growth is low (~2% CAGR 2024–2026), so management focuses on operational excellence, margin expansion, and free-cash-flow extraction rather than heavy promotion, since these ingredients need little marketing versus high-growth beauty lines.

- ~EUR 1.1bn sales (FY2024)

- ~60% market penetration

- 2% CAGR (2024–2026)

- High scale, low promo spend

DSM‑Firmenich cash cows: €2.1bn premixes, €1.1bn aromas, high margins & >20% FCF

DSM-Firmenich cash cows: Vitamin/mineral premixes (€2.1bn nutrition sales 2024), classic food enzymes & cultures (30–35% dairy, €450–520m EBITDA 2024), beverage flavors (1–2% CAGR, mid-30s% gross margin), aroma chemicals (€1.1bn sales 2024, ~60% penetration); free cash conversion >20% (2024), capex limited to maintenance.

| Unit | Key metric 2024/25 |

|---|---|

| Premixes | €2.1bn sales |

| Enzymes & cultures | 30–35% share; €450–520m EBITDA |

| Beverage flavors | 1–2% CAGR; mid-30s% GM |

| Aroma chemicals | €1.1bn sales; ~60% penetration |

What You’re Viewing Is Included

DSM-Firmenich BCG Matrix

The file you're previewing is the exact DSM‑Firmenich BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready‑to‑use strategic analysis designed for clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

DSM‑Firmenich’s BCG Matrix preview highlights how its fragrance and nutrition portfolios balance growth and market share, hinting at Stars driving future expansion and Cash Cows funding R&D—while select lines may require divestment or repositioning.

Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

Natural Fragrance and Beauty Ingredients

As clean-beauty demand peaks in late 2025, DSM-Firmenich’s Natural Fragrance and Beauty Ingredients (Stars) leads via sustainable extraction, capturing ~28% of the premium natural ingredients market and driving €420m in 2025 revenue for Perfumery & Beauty.

Firmenich perfumery plus DSM science secures leadership; R&D spend rose 22% YoY to €65m in 2025 to fend off biotech entrants and sustain product premiums.

High capex continues: €90m committed for 2026 facilities and bioprocess scale-up, keeping this unit the primary top-line growth engine within Perfumery & Beauty.

Plant-Based Texture and Taste Solutions

The shift to sustainable proteins grows ~20% CAGR (2024–30), and DSM-Firmenich has captured a leading share by closing the taste-texture gap in meat alternatives with enzymatic texturants plus advanced flavor systems.

The unit is the preferred partner for global food makers, supplying formulations used in over 35% of top-50 plant-based SKUs and driving €220m in segment revenue in 2025.

Significant capex—€150m planned 2025–27—scales fermentation and blending capacity to match rising demand and SKU churn.

As the alt-protein market matures toward 2030, this high-growth Stars unit is projected to convert to a cash cow with stable margins and >€300m annual EBITDA potential.

Biotech-Derived Human Milk Oligosaccharides

The HMO portfolio is a star: high-growth frontier in infant nutrition and adult gut health where DSM-Firmenich holds a pioneering market position, with global HMO market projected to reach $3.5bn by 2028 (CAGR ~12% from 2023). Advanced fermentation yields higher gross margins (estimated 25–35%) versus chemical routes and supports scalable supply. Ongoing R&D and ~€60–80m annual investment are needed to build clinical evidence and win approvals across APAC and LATAM. As gut health mainstreams, this star requires continued strategic capex and commercial focus.

Personalized Nutrition Platforms

Personalized Nutrition Platforms leverages data-driven diagnostics plus tailored supplement delivery to target the bespoke wellness market, using DSM-Firmenich’s 2024 ingredient library of >8,000 SKUs and 25%+ gross margins in direct-to-consumer models.

Digital health grew ~20% CAGR 2021–25, so DSM-Firmenich invests heavily in software and CAC; unit is cash-consuming but holds unrivaled market leadership and strategic tech-bio synergy.

- High growth: ~20% digital health CAGR (2021–25)

- Ingredient library: >8,000 SKUs (2024)

- Margins: 25%+ gross in DTC models

- Risks: high R&D and CAC, heavy cash burn

- Strategic: tech-biology synergy guides capex

Premium Fine Fragrance and Luxury Scent

Post-merger synergy with Firmenich has cemented DSM-Firmenich as a global leader in premium fine fragrance, capturing an estimated 22% luxury-market share in 2024 and benefiting from 6–8% CAGR in emerging markets (2020–24).

Exclusive contracts with top fashion houses sustain high barriers to entry; the unit reported ~€1.1bn revenue in FY2024 and double-digit gross margins, while ongoing marketing spend preserves brand premium.

Investment prioritizes creative talent and sustainable sourcing: 35% supplier traceability for key raw materials in 2024 and a €45m sustainability R&D budget through 2025 to protect prestige.

- Market share ~22% (2024)

- Unit revenue ~€1.1bn (FY2024)

- Emerging-market CAGR 6–8% (2020–24)

- €45m sustainability R&D through 2025

- 35% supplier traceability (2024)

DSM‑Firmenich Stars: €1.94bn revenue in 2025; >€300m EBITDA potential by 2030

DSM-Firmenich Stars: high-growth natural ingredients, alt-protein, HMO, and personalized nutrition units drove €1.94bn revenue in 2025, ~28% share in premium naturals, €420m Perfumery & Beauty, €220m plant-based, €300m HMO+personalized, R&D €65m, capex planned €240m (2025–27); projected >€300m annual EBITDA by 2030 as units mature.

| Metric | 2025 |

|---|---|

| Revenue (Stars) | €1.94bn |

| Premium naturals share | ~28% |

| Perfumery & Beauty | €420m |

| Plant-based | €220m |

| R&D spend | €65m |

| Planned capex 2025–27 | €240m |

| EBITDA potential (2030) | >€300m |

What is included in the product

BCG Matrix review of DSM‑Firmenich: quadrant summaries, strategic moves to invest, hold or divest, and trend‑driven competitive insights.

One-page DSM-Firmenich BCG Matrix placing each business unit in a quadrant for rapid portfolio decisions

Cash Cows

Core Vitamin and Mineral Premixes

Core Vitamin and Mineral Premixes sit as DSM-Firmenich cash cows: they hold a dominant global market share in essential human nutrition within a mature market, generating steady free cash flow—DSM-Firmenich’s nutrition division reported €2.1bn sales in 2024, with premixes a large contributor.

These products need little marketing or capex, so margins stay high; operating margin for vitamins was ~18% in 2024, funding R&D for question marks and stars.

Ongoing efficiency moves and supply-chain optimization cut COGS by an estimated 3–4% in 2023–24, further boosting EBITDA and enabling targeted innovation spend.

Classic Food Enzymes and Cultures

In mature dairy and baking markets, DSM-Firmenich’s Classic Food Enzymes and Cultures hold a dominant share—about 30–35% in specialty dairy cultures and ~25% in baking enzymes—supplying global food giants and ensuring steady, predictable demand.

With market growth under 3% annually, the unit emphasizes cash harvesting and high service levels, generating roughly €450–520 million EBITDA contribution in 2024 to fund debt service and dividends.

Standard Beverage Flavor Systems

Standard Beverage Flavor Systems sits in a saturated, low-growth market (~1–2% CAGR globally for traditional beverage flavors in 2024), yet DSM-Firmenich retains a large, loyal customer base across major soft drink and dairy makers.

High gross margins (mid-30s %) persist via long-term contracts and switching costs; customers face reformulation and regulatory retesting expenses often >$1m, keeping churn low.

Minimal capex needed—maintenance and incremental R&D only—so the unit reliably generates free cash flow, contributing roughly 18–22% of the Taste, Texture and Health division’s EBITDA in 2024.

Dietary Supplement Ingredients

Dietary Supplement Ingredients: DSM-Firmenich holds a leading volume position in mature categories like omega-3s and basic antioxidants, with global market share estimates around 12–15% for encapsulated omega-3s as of 2025 and mid-single-digit CAGR demand growth; scale and an integrated supply chain cut costs, helping protect margins despite intense price pressure.

These high-volume sales generate steady cash flow—estimated free cash conversion above 20% in 2024 for the nutrition segment—funding corporate infrastructure while capex is kept to essential maintenance and small process innovations to sustain efficiency.

- Leading volume position: ~12–15% omega-3s market share (2025)

- Demand growth: mid-single-digit CAGR

- Free cash conversion: >20% (2024, nutrition segment)

- Capex: limited to maintenance and process tweaks

Established Aroma Chemicals

Established Aroma Chemicals are a cash cow for DSM-Firmenich, supplying base aroma compounds for household and personal care with roughly 60% global market penetration and stable FY2024 sales near EUR 1.1bn, driven by massive scale and low unit costs.

Market growth is low (~2% CAGR 2024–2026), so management focuses on operational excellence, margin expansion, and free-cash-flow extraction rather than heavy promotion, since these ingredients need little marketing versus high-growth beauty lines.

- ~EUR 1.1bn sales (FY2024)

- ~60% market penetration

- 2% CAGR (2024–2026)

- High scale, low promo spend

DSM‑Firmenich cash cows: €2.1bn premixes, €1.1bn aromas, high margins & >20% FCF

DSM-Firmenich cash cows: Vitamin/mineral premixes (€2.1bn nutrition sales 2024), classic food enzymes & cultures (30–35% dairy, €450–520m EBITDA 2024), beverage flavors (1–2% CAGR, mid-30s% gross margin), aroma chemicals (€1.1bn sales 2024, ~60% penetration); free cash conversion >20% (2024), capex limited to maintenance.

| Unit | Key metric 2024/25 |

|---|---|

| Premixes | €2.1bn sales |

| Enzymes & cultures | 30–35% share; €450–520m EBITDA |

| Beverage flavors | 1–2% CAGR; mid-30s% GM |

| Aroma chemicals | €1.1bn sales; ~60% penetration |

What You’re Viewing Is Included

DSM-Firmenich BCG Matrix

The file you're previewing is the exact DSM‑Firmenich BCG Matrix report you'll receive after purchase—no watermarks, no demo content, just a fully formatted, ready‑to‑use strategic analysis designed for clarity and professional presentation.