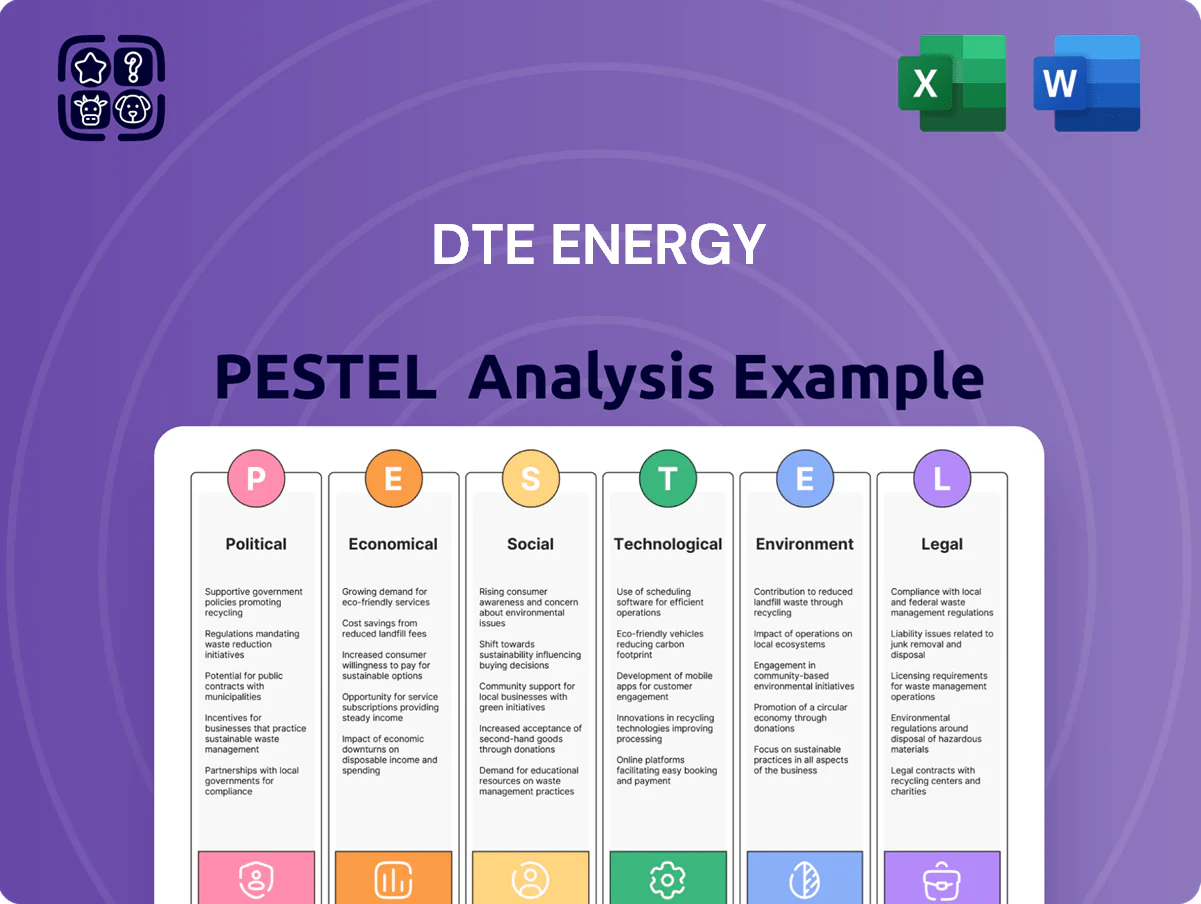

DTE Energy PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Explore how regulatory shifts, decarbonization trends, and technological innovation are reshaping DTE Energy’s strategic outlook—our concise PESTLE snapshot highlights key risks and opportunities for investors and planners. Purchase the full PESTLE analysis to access detailed insights, actionable scenarios, and ready-to-use slides that accelerate decision-making.

Political factors

Michigan Public Service Commission Regulatory Environment

The Michigan Public Service Commission (MPSC) controls DTE Energy’s revenue by approving rate cases and capital plans; DTE recovered $1.2 billion in rate increases in its most recent 2024/2025 filings and seeks multi-year recovery for ~$7.5 billion in grid investments through 2027.

Late-2025 political appointments to the MPSC emphasize grid reliability and affordable rates, aligning regulators with state clean-energy targets and influencing allowed ROE and depreciation policies that affect cash flow.

Navigating MPSC proceedings is vital for timely cost recovery and credit metrics; denied or delayed rate relief could trim adjusted EBITDA margin and pressure DTE’s investment-grade ratings, which were BBB+/Baa2 range in 2024–2025.

Federal Energy Policy and Tax Incentives

The Inflation Reduction Act’s tax credits and production incentives—supporting up to 30% ITC for solar and expanded PTC for wind—remain central to DTE’s renewable CAPEX plans, enabling DTE to target roughly $8–10 billion in clean investments through 2030 per its 2024 plan.

Bipartisan Infrastructure Law Implementation

Ongoing federal funding from the Bipartisan Infrastructure Law, which allocated about $65 billion for grid modernization and EV infrastructure through 2026, gives DTE tangible opportunities to upgrade its Michigan grid and expand EV charging; DTE projected $10–12 billion in capital investments through 2026, with a portion targeting these programs. Political backing for domestic energy security and resilience shapes grant distribution at federal and state levels, benefiting utilities prioritized for hardening and resiliency projects. Securing and deploying these funds efficiently is a key political and strategic priority for DTE to meet reliability targets and leverage matched funding.

Local Government Relations and Zoning

- Permitting delays: 9–14 months (2023–2025)

- Cost impact: up to 15% overruns

- DTE target: 8,000 MW by 2040; $9–11B investments through 2030

- Local engagement cut permitting by ~6 months (2024 case)

State Legislative Mandates for Clean Energy

Michigan targets carbon neutrality by 2050 and a 50% renewable energy standard by 2030, driving DTE’s generation shift—DTE plans $8–10 billion in clean energy investments through 2024–2028 to meet mandates and retire coal units.

Political shifts in Lansing could accelerate decarbonization or alter net metering; DTE’s lobbying and regulatory filings seek flexible timelines and cost-recovery mechanisms to protect rates and capital returns.

- 2050 carbon-neutral goal; 50% RE by 2030

- $8–10B planned clean investments (2024–2028)

- Risk: legislative changes to timelines/net metering

- Company action: active lobbying and regulatory advocacy

DTE seeks $7.5B recovery as $8–10B clean capex races past permitting delays

MPSC rate approvals and late-2025 appointments shape allowed ROE/depreciation; DTE recovered $1.2B (2024/25) and seeks ~$7.5B multi-year recovery to 2027. IRA/PTC/ITC enable ~30% incentives supporting DTE’s $8–10B clean capex through 2030; BIL grants (~$65B nationwide) and local permitting delays (9–14 months; up to 15% cost overruns) materially affect timelines and returns.

| Metric | Value |

|---|---|

| Recovered rates (2024/25) | $1.2B |

| Requested recovery to 2027 | $7.5B |

| Clean capex target | $8–10B (to 2030) |

| Permitting delays | 9–14 months; +15% cost |

What is included in the product

Explores how macro-environmental factors uniquely affect DTE Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise, PESTLE-segmented summary of DTE Energy that’s easy to drop into presentations or share across teams, enabling quick alignment on regulatory risks, market drivers, and strategic opportunities.

Economic factors

Interest Rate Environment and Capital Costs

As a capital-intensive utility, DTE Energy is highly sensitive to interest-rate swings; a 1 percentage-point rise in borrowing costs can add roughly $100–150 million annually in financing expenses on its ~$10–15 billion debt base. By late 2025, Fed-driven rate stabilization around 4.5–5.0% improved visibility for financing DTE’s multi-billion-dollar clean-energy transition, though sustained higher rates still risk compressing margins if returns fail to cover elevated cost of capital.

Inflationary Pressures on Operations

Persistent inflation raised DTE Energy's input costs in 2024–2025: materials and equipment up ~6–8% and labor wage inflation near 4–5%, increasing O&M and capital spend for grid and gas system upgrades.

DTE counters via supply‑chain optimization and $350m+ annual operational efficiency programs, aiming to limit bill impacts.

Cost recovery depends on Michigan regulatory approvals; authorized rate cases and economic conditions in Southeast Michigan constrain passthrough timing and magnitude.

Regional Economic Health and Industrial Demand

DTE Energy’s revenue closely tracks Michigan’s economy; Michigan GDP was about $520 billion in 2023 and the state’s manufacturing sector—which accounts for roughly 17% of employment—drives major industrial load. Economic slowdowns or a 1–2% dip in manufacturing output can cut industrial energy demand and raise uncollectible accounts; DTE reported $176 million in uncollectible expenses in 2023. Growth in battery and EV supply chains (>$10 billion in announced investments in Michigan by 2025) supports sustained load growth.

Energy Commodity Price Volatility

Fluctuations in natural gas and purchased-power prices directly affect DTE's retail rates; U.S. Henry Hub natural gas averaged about 3.60 USD/MMBtu in 2024, up from 2.50 in 2023, raising procurement costs and upward pressure on customer bills.

DTE uses hedging and regulatory recovery mechanisms; however, spikes like the 2022–24 global energy disruptions can still strain consumers and utilities despite hedges covering a significant portion of near-term volumes.

Maintaining a balanced portfolio—in 2024 DTE reported ~40% generation from natural gas and growing renewables—helps insulate customers and the company from global market shocks.

- 2024 Henry Hub ~3.60 USD/MMBtu; 2023 ~2.50

- Hedging and regulatory recovery mitigate but do not eliminate risk

- ~40% gas-fired generation in 2024; renewables increasing

Labor Market Trends and Wage Growth

- Michigan unemployment 3.8% (2024) — tighter labor supply

- Private wage growth 4.1% (2024) — higher labor costs

- Personnel costs +5–7% on renewables projects

- Energy tech roles +6% YoY; specialized salaries +8–12%

DTE margins under pressure: rising financing, inflation, labor and gas procurement risks

DTE's financing cost sensitivity (1pp ↑ ≈ $100–150m on $10–15bn debt) and 2024–25 inflation (materials +6–8%, wages +4–5%) raise O&M and capex; Michigan GDP ~$520bn (2023) ties revenue to industrial load; 2024 Henry Hub ~$3.60/MMBtu and ~40% gas generation shift procurement risk despite hedges; Michigan unemployment 3.8% (2024) tightens skilled labor, raising personnel costs.

| Metric | Value |

|---|---|

| Financing sensitivity | $100–150m per 1pp |

| Materials inflation | +6–8% (2024–25) |

| Wage inflation | +4–5% (2024) |

| Henry Hub | $3.60/MMBtu (2024) |

| Gas generation | ~40% (2024) |

| Michigan GDP | $520bn (2023) |

| Unemployment | 3.8% (2024) |

Same Document Delivered

DTE Energy PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This DTE Energy PESTLE Analysis provides concise, actionable insights into political, economic, social, technological, legal, and environmental factors affecting the company. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Explore how regulatory shifts, decarbonization trends, and technological innovation are reshaping DTE Energy’s strategic outlook—our concise PESTLE snapshot highlights key risks and opportunities for investors and planners. Purchase the full PESTLE analysis to access detailed insights, actionable scenarios, and ready-to-use slides that accelerate decision-making.

Political factors

Michigan Public Service Commission Regulatory Environment

The Michigan Public Service Commission (MPSC) controls DTE Energy’s revenue by approving rate cases and capital plans; DTE recovered $1.2 billion in rate increases in its most recent 2024/2025 filings and seeks multi-year recovery for ~$7.5 billion in grid investments through 2027.

Late-2025 political appointments to the MPSC emphasize grid reliability and affordable rates, aligning regulators with state clean-energy targets and influencing allowed ROE and depreciation policies that affect cash flow.

Navigating MPSC proceedings is vital for timely cost recovery and credit metrics; denied or delayed rate relief could trim adjusted EBITDA margin and pressure DTE’s investment-grade ratings, which were BBB+/Baa2 range in 2024–2025.

Federal Energy Policy and Tax Incentives

The Inflation Reduction Act’s tax credits and production incentives—supporting up to 30% ITC for solar and expanded PTC for wind—remain central to DTE’s renewable CAPEX plans, enabling DTE to target roughly $8–10 billion in clean investments through 2030 per its 2024 plan.

Bipartisan Infrastructure Law Implementation

Ongoing federal funding from the Bipartisan Infrastructure Law, which allocated about $65 billion for grid modernization and EV infrastructure through 2026, gives DTE tangible opportunities to upgrade its Michigan grid and expand EV charging; DTE projected $10–12 billion in capital investments through 2026, with a portion targeting these programs. Political backing for domestic energy security and resilience shapes grant distribution at federal and state levels, benefiting utilities prioritized for hardening and resiliency projects. Securing and deploying these funds efficiently is a key political and strategic priority for DTE to meet reliability targets and leverage matched funding.

Local Government Relations and Zoning

- Permitting delays: 9–14 months (2023–2025)

- Cost impact: up to 15% overruns

- DTE target: 8,000 MW by 2040; $9–11B investments through 2030

- Local engagement cut permitting by ~6 months (2024 case)

State Legislative Mandates for Clean Energy

Michigan targets carbon neutrality by 2050 and a 50% renewable energy standard by 2030, driving DTE’s generation shift—DTE plans $8–10 billion in clean energy investments through 2024–2028 to meet mandates and retire coal units.

Political shifts in Lansing could accelerate decarbonization or alter net metering; DTE’s lobbying and regulatory filings seek flexible timelines and cost-recovery mechanisms to protect rates and capital returns.

- 2050 carbon-neutral goal; 50% RE by 2030

- $8–10B planned clean investments (2024–2028)

- Risk: legislative changes to timelines/net metering

- Company action: active lobbying and regulatory advocacy

DTE seeks $7.5B recovery as $8–10B clean capex races past permitting delays

MPSC rate approvals and late-2025 appointments shape allowed ROE/depreciation; DTE recovered $1.2B (2024/25) and seeks ~$7.5B multi-year recovery to 2027. IRA/PTC/ITC enable ~30% incentives supporting DTE’s $8–10B clean capex through 2030; BIL grants (~$65B nationwide) and local permitting delays (9–14 months; up to 15% cost overruns) materially affect timelines and returns.

| Metric | Value |

|---|---|

| Recovered rates (2024/25) | $1.2B |

| Requested recovery to 2027 | $7.5B |

| Clean capex target | $8–10B (to 2030) |

| Permitting delays | 9–14 months; +15% cost |

What is included in the product

Explores how macro-environmental factors uniquely affect DTE Energy across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise, PESTLE-segmented summary of DTE Energy that’s easy to drop into presentations or share across teams, enabling quick alignment on regulatory risks, market drivers, and strategic opportunities.

Economic factors

Interest Rate Environment and Capital Costs

As a capital-intensive utility, DTE Energy is highly sensitive to interest-rate swings; a 1 percentage-point rise in borrowing costs can add roughly $100–150 million annually in financing expenses on its ~$10–15 billion debt base. By late 2025, Fed-driven rate stabilization around 4.5–5.0% improved visibility for financing DTE’s multi-billion-dollar clean-energy transition, though sustained higher rates still risk compressing margins if returns fail to cover elevated cost of capital.

Inflationary Pressures on Operations

Persistent inflation raised DTE Energy's input costs in 2024–2025: materials and equipment up ~6–8% and labor wage inflation near 4–5%, increasing O&M and capital spend for grid and gas system upgrades.

DTE counters via supply‑chain optimization and $350m+ annual operational efficiency programs, aiming to limit bill impacts.

Cost recovery depends on Michigan regulatory approvals; authorized rate cases and economic conditions in Southeast Michigan constrain passthrough timing and magnitude.

Regional Economic Health and Industrial Demand

DTE Energy’s revenue closely tracks Michigan’s economy; Michigan GDP was about $520 billion in 2023 and the state’s manufacturing sector—which accounts for roughly 17% of employment—drives major industrial load. Economic slowdowns or a 1–2% dip in manufacturing output can cut industrial energy demand and raise uncollectible accounts; DTE reported $176 million in uncollectible expenses in 2023. Growth in battery and EV supply chains (>$10 billion in announced investments in Michigan by 2025) supports sustained load growth.

Energy Commodity Price Volatility

Fluctuations in natural gas and purchased-power prices directly affect DTE's retail rates; U.S. Henry Hub natural gas averaged about 3.60 USD/MMBtu in 2024, up from 2.50 in 2023, raising procurement costs and upward pressure on customer bills.

DTE uses hedging and regulatory recovery mechanisms; however, spikes like the 2022–24 global energy disruptions can still strain consumers and utilities despite hedges covering a significant portion of near-term volumes.

Maintaining a balanced portfolio—in 2024 DTE reported ~40% generation from natural gas and growing renewables—helps insulate customers and the company from global market shocks.

- 2024 Henry Hub ~3.60 USD/MMBtu; 2023 ~2.50

- Hedging and regulatory recovery mitigate but do not eliminate risk

- ~40% gas-fired generation in 2024; renewables increasing

Labor Market Trends and Wage Growth

- Michigan unemployment 3.8% (2024) — tighter labor supply

- Private wage growth 4.1% (2024) — higher labor costs

- Personnel costs +5–7% on renewables projects

- Energy tech roles +6% YoY; specialized salaries +8–12%

DTE margins under pressure: rising financing, inflation, labor and gas procurement risks

DTE's financing cost sensitivity (1pp ↑ ≈ $100–150m on $10–15bn debt) and 2024–25 inflation (materials +6–8%, wages +4–5%) raise O&M and capex; Michigan GDP ~$520bn (2023) ties revenue to industrial load; 2024 Henry Hub ~$3.60/MMBtu and ~40% gas generation shift procurement risk despite hedges; Michigan unemployment 3.8% (2024) tightens skilled labor, raising personnel costs.

| Metric | Value |

|---|---|

| Financing sensitivity | $100–150m per 1pp |

| Materials inflation | +6–8% (2024–25) |

| Wage inflation | +4–5% (2024) |

| Henry Hub | $3.60/MMBtu (2024) |

| Gas generation | ~40% (2024) |

| Michigan GDP | $520bn (2023) |

| Unemployment | 3.8% (2024) |

Same Document Delivered

DTE Energy PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This DTE Energy PESTLE Analysis provides concise, actionable insights into political, economic, social, technological, legal, and environmental factors affecting the company. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders, no teasers—this is the real, ready-to-use file you’ll get upon purchase.