Dycom Porter's Five Forces Analysis

Don't Miss the Bigger Picture

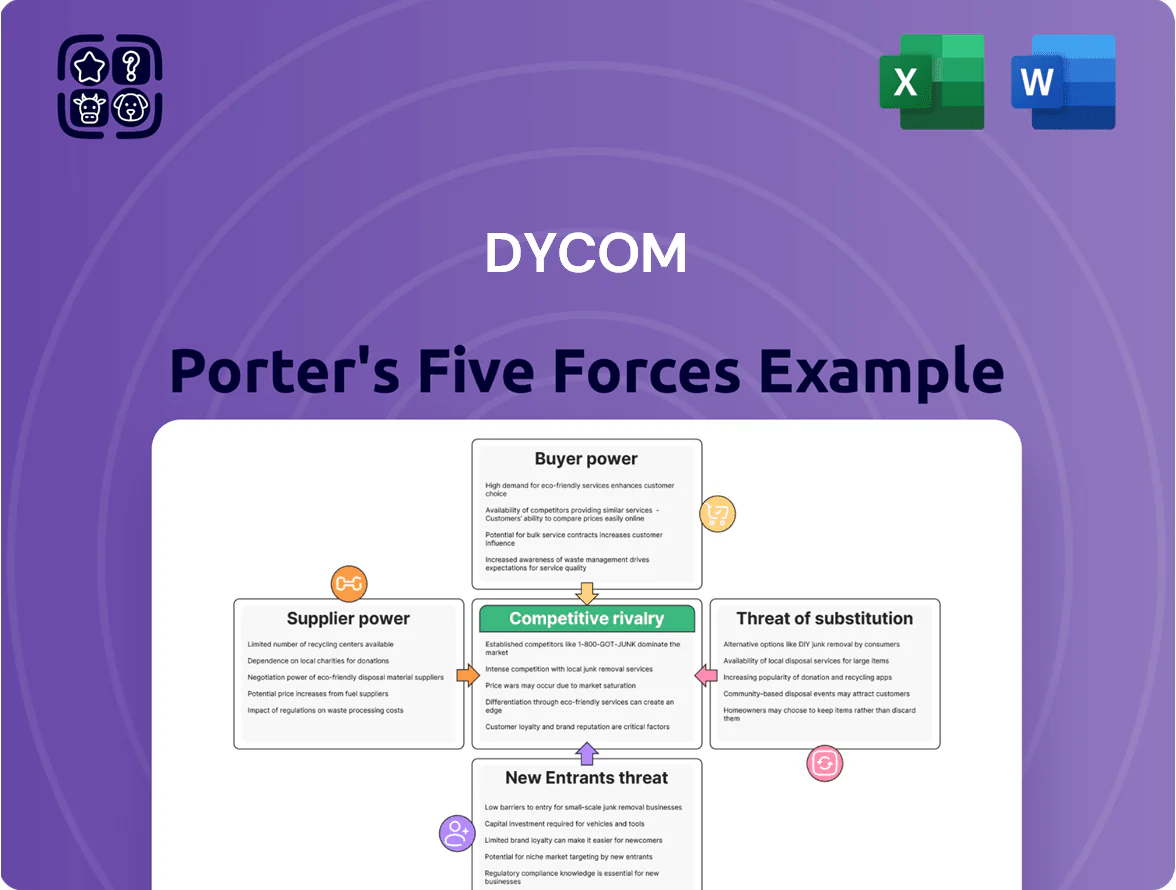

Dycom operates in a capital-intensive, contractor-driven telecom services market where buyer concentration and competitive rivalry amplify margin pressure, while supplier power and technological shifts raise execution risk.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dycom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Shortage of Skilled Labor Force

Labor scarcity for fiber splicers and 5G tower technicians is a critical input cost driver; industry vacancy rates hit 8.4% in Q3 2025 and average specialized-tech wages rose 9.2% year-over-year, raising Dycom’s labor-related operating margin pressure.

Reliance on Specialized Construction Equipment

Dycom depends on heavy machinery and niche tools from few global suppliers, giving those vendors pricing leverage; equipment makers like Caterpillar and Komatsu held global market shares near 40% in 2024 for certain construction segments, tightening options for buyers.

Lead times rose to 20–30 weeks in 2021–23 during supply shocks and still average 12–18 weeks in 2025, while spare-part inflation of ~6–9% since 2021 raises maintenance costs.

When US infrastructure spending surged—Bipartisan Infrastructure Law allocations top $110B for broadband and power projects through 2026—vendors sustained firm pricing amid heightened demand, compressing Dycom’s margin flexibility.

Fuel and Commodity Price Volatility

Dycom’s vast fleet and heavy machinery make it highly exposed to fuel and raw-material price swings; diesel accounts for a meaningful portion of operating costs and copper/conduit price moves directly raise project margins. Some contracts permit passthroughs or escalators, but spot-market suppliers still set prices short-term—US diesel rack prices rose ~28% from 2020–2024. Sustained inflation into 2025 has strengthened energy and material suppliers’ leverage, squeezing contractors’ bargaining power.

Utilization of Third-Party Subcontractors

Dycom frequently hires small subcontractors to scale labor during project surges and geographic expansion; in 2024 subcontracted field labor accounted for roughly 22% of project hours on large national jobs.

When several national contracts bid for the same specialized crews, subcontractors have pushed rates up 8–12% in 2023–2024, raising prime contractor costs and schedule risk.

This dynamic gives local firms leverage to set terms, increasing supplier bargaining power and squeezing Dycom’s margins on peak work.

- Subcontracted field hours ≈22% (2024)

- Rate spikes 8–12% (2023–2024)

- Higher schedule risk and margin pressure

Technological Software and Mapping Providers

Modern infrastructure deployment relies on proprietary GIS mapping and project-management software for accuracy and efficiency; top vendors like Esri report global GIS market revenues of about $9.4B in 2023, underscoring supplier scale.

These providers hold leverage over Dycom because deep platform integration raises switching costs—implementations can exceed $1M and take 6–12 months—so Dycom faces vendor dependency.

Dycom must keep subscriptions to meet telco reporting standards and SLAs; failing to renew risks noncompliance with client requirements and potential contract penalties tied to service-level breaches.

- High supplier leverage: large vendor market share (~$9.4B GIS market)

- Switching cost: implementations often $500k–$1M+, 6–12 months

- Contract risk: subscriptions required for telco reporting and SLAs

Suppliers Squeeze Margins: Labor, Rates & Diesel Surge Tighten Supply Chain

Suppliers hold high bargaining power: labor scarcity (8.4% vacancy Q3 2025), specialized wages +9.2% YoY, subcontractor hours ≈22% (2024) with 8–12% rate spikes (2023–24); equipment vendors concentrate ~40% share in key segments; lead times 12–18 weeks (2025); diesel +28% (2020–24) boosting input costs and compressing Dycom margins.

| Metric | Value |

|---|---|

| Labor vacancy | 8.4% (Q3 2025) |

| Wage growth | +9.2% YoY (2025) |

| Subcontracted hours | 22% (2024) |

| Subcontractor rate spikes | 8–12% (2023–24) |

| Equipment supplier share | ~40% (2024) |

| Lead times | 12–18 weeks (2025) |

| Diesel price change | +28% (2020–24) |

What is included in the product

Tailored exclusively for Dycom, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer influence on pricing, threats from entrants and substitutes, and highlights disruptive forces and entry barriers shaping Dycom’s market position.

A concise Dycom Porter's Five Forces one-sheet that highlights supplier, buyer, and competitor pressures—ideal for rapid strategic decisions and investor briefings.

Customers Bargaining Power

High Concentration of Major Telecom Clients

Rigorous Competitive Bidding Processes

Most large infrastructure contracts use transparent RFPs, letting customers pit contractors to cut prices and tighten terms; for example, U.S. federal and state procurements saw average bid spreads compress to 6.8% in 2024, pressuring margins. By late 2025, stricter transparency rules for government-funded projects—eg, expanded disclosure and vendor scorecards—have increased bidding pressure, boosting award volatility and favoring low-cost bidders.

Long-Term Master Service Agreements

Long-term master service agreements give Dycom revenue visibility but lock pricing for years, so it can’t quickly pass through sudden input-cost rises; for example, 2024 gross margin pressure hit contractors as steel and labor rose 8–12% while contract rates stayed fixed. Customers leverage these contracts to secure price stability and push faster, higher-quality deployments, effectively capping buyer infrastructure spend despite 5–7% annual CPI inflation trends.

Influence of Government Funding Constraints

Government grants under BEAD (Broadband Equity, Access, and Deployment) force customers to demand strict cost-efficiency; many projects require documented unit cost savings and audit trails to qualify for payments.

That shifts bargaining power to customers and grant managers, who push Dycom for lean staffing, fixed-price scopes, and penalties for cost overruns—raising price pressure and margin risk.

The public funding adds scrutiny: BEAD awards totaled about $42.45 billion (2023–25 estimates), amplifying oversight and leverage over contractors.

- Customers demand documented cost-savings

- BEAD pool ~$42.45B increases buyer leverage

- Push for fixed-price/penalty clauses

Low Switching Costs Between Major Contractors

Large telecoms like AT&T and Verizon routinely contract with several national contractors—Dycom included—to spread operational risk, and industry surveys in 2024 show 68% of carriers keep three or more approved vendors.

If Dycom misses metrics (safety, uptime, schedule), clients can reallocate future work to rivals with similar scale, shifting revenues quickly; Dycom reported 2024 revenue of $3.9 billion, so losing even 5% of spend would be material.

This ease of reallocation gives customers leverage in annual contract reviews and project allocations, pressuring pricing, service guarantees, and penalty clauses.

- Multiple approved vendors: 68% of carriers (2024)

- Dycom 2024 revenue: $3.9B; 5% loss ≈ $195M

- Leverage points: pricing, SLAs, penalty terms

Dycom risks: 55% client concentration, margin squeeze as carriers leverage multi-vendor bids

| Metric | Value |

|---|---|

| Dycom revenue FY2024 | $3.9B |

| Revenue share from top customers | ~55% |

| Gross margin FY2024 | 35% |

| Carrier multi-vendor rate (2024) | 68% |

| BEAD funding (2023–25) | $42.45B |

Full Version Awaits

Dycom Porter's Five Forces Analysis

This preview shows the exact Dycom Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready to download the moment you purchase with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Dycom operates in a capital-intensive, contractor-driven telecom services market where buyer concentration and competitive rivalry amplify margin pressure, while supplier power and technological shifts raise execution risk.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dycom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Shortage of Skilled Labor Force

Labor scarcity for fiber splicers and 5G tower technicians is a critical input cost driver; industry vacancy rates hit 8.4% in Q3 2025 and average specialized-tech wages rose 9.2% year-over-year, raising Dycom’s labor-related operating margin pressure.

Reliance on Specialized Construction Equipment

Dycom depends on heavy machinery and niche tools from few global suppliers, giving those vendors pricing leverage; equipment makers like Caterpillar and Komatsu held global market shares near 40% in 2024 for certain construction segments, tightening options for buyers.

Lead times rose to 20–30 weeks in 2021–23 during supply shocks and still average 12–18 weeks in 2025, while spare-part inflation of ~6–9% since 2021 raises maintenance costs.

When US infrastructure spending surged—Bipartisan Infrastructure Law allocations top $110B for broadband and power projects through 2026—vendors sustained firm pricing amid heightened demand, compressing Dycom’s margin flexibility.

Fuel and Commodity Price Volatility

Dycom’s vast fleet and heavy machinery make it highly exposed to fuel and raw-material price swings; diesel accounts for a meaningful portion of operating costs and copper/conduit price moves directly raise project margins. Some contracts permit passthroughs or escalators, but spot-market suppliers still set prices short-term—US diesel rack prices rose ~28% from 2020–2024. Sustained inflation into 2025 has strengthened energy and material suppliers’ leverage, squeezing contractors’ bargaining power.

Utilization of Third-Party Subcontractors

Dycom frequently hires small subcontractors to scale labor during project surges and geographic expansion; in 2024 subcontracted field labor accounted for roughly 22% of project hours on large national jobs.

When several national contracts bid for the same specialized crews, subcontractors have pushed rates up 8–12% in 2023–2024, raising prime contractor costs and schedule risk.

This dynamic gives local firms leverage to set terms, increasing supplier bargaining power and squeezing Dycom’s margins on peak work.

- Subcontracted field hours ≈22% (2024)

- Rate spikes 8–12% (2023–2024)

- Higher schedule risk and margin pressure

Technological Software and Mapping Providers

Modern infrastructure deployment relies on proprietary GIS mapping and project-management software for accuracy and efficiency; top vendors like Esri report global GIS market revenues of about $9.4B in 2023, underscoring supplier scale.

These providers hold leverage over Dycom because deep platform integration raises switching costs—implementations can exceed $1M and take 6–12 months—so Dycom faces vendor dependency.

Dycom must keep subscriptions to meet telco reporting standards and SLAs; failing to renew risks noncompliance with client requirements and potential contract penalties tied to service-level breaches.

- High supplier leverage: large vendor market share (~$9.4B GIS market)

- Switching cost: implementations often $500k–$1M+, 6–12 months

- Contract risk: subscriptions required for telco reporting and SLAs

Suppliers Squeeze Margins: Labor, Rates & Diesel Surge Tighten Supply Chain

Suppliers hold high bargaining power: labor scarcity (8.4% vacancy Q3 2025), specialized wages +9.2% YoY, subcontractor hours ≈22% (2024) with 8–12% rate spikes (2023–24); equipment vendors concentrate ~40% share in key segments; lead times 12–18 weeks (2025); diesel +28% (2020–24) boosting input costs and compressing Dycom margins.

| Metric | Value |

|---|---|

| Labor vacancy | 8.4% (Q3 2025) |

| Wage growth | +9.2% YoY (2025) |

| Subcontracted hours | 22% (2024) |

| Subcontractor rate spikes | 8–12% (2023–24) |

| Equipment supplier share | ~40% (2024) |

| Lead times | 12–18 weeks (2025) |

| Diesel price change | +28% (2020–24) |

What is included in the product

Tailored exclusively for Dycom, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer influence on pricing, threats from entrants and substitutes, and highlights disruptive forces and entry barriers shaping Dycom’s market position.

A concise Dycom Porter's Five Forces one-sheet that highlights supplier, buyer, and competitor pressures—ideal for rapid strategic decisions and investor briefings.

Customers Bargaining Power

High Concentration of Major Telecom Clients

Rigorous Competitive Bidding Processes

Most large infrastructure contracts use transparent RFPs, letting customers pit contractors to cut prices and tighten terms; for example, U.S. federal and state procurements saw average bid spreads compress to 6.8% in 2024, pressuring margins. By late 2025, stricter transparency rules for government-funded projects—eg, expanded disclosure and vendor scorecards—have increased bidding pressure, boosting award volatility and favoring low-cost bidders.

Long-Term Master Service Agreements

Long-term master service agreements give Dycom revenue visibility but lock pricing for years, so it can’t quickly pass through sudden input-cost rises; for example, 2024 gross margin pressure hit contractors as steel and labor rose 8–12% while contract rates stayed fixed. Customers leverage these contracts to secure price stability and push faster, higher-quality deployments, effectively capping buyer infrastructure spend despite 5–7% annual CPI inflation trends.

Influence of Government Funding Constraints

Government grants under BEAD (Broadband Equity, Access, and Deployment) force customers to demand strict cost-efficiency; many projects require documented unit cost savings and audit trails to qualify for payments.

That shifts bargaining power to customers and grant managers, who push Dycom for lean staffing, fixed-price scopes, and penalties for cost overruns—raising price pressure and margin risk.

The public funding adds scrutiny: BEAD awards totaled about $42.45 billion (2023–25 estimates), amplifying oversight and leverage over contractors.

- Customers demand documented cost-savings

- BEAD pool ~$42.45B increases buyer leverage

- Push for fixed-price/penalty clauses

Low Switching Costs Between Major Contractors

Large telecoms like AT&T and Verizon routinely contract with several national contractors—Dycom included—to spread operational risk, and industry surveys in 2024 show 68% of carriers keep three or more approved vendors.

If Dycom misses metrics (safety, uptime, schedule), clients can reallocate future work to rivals with similar scale, shifting revenues quickly; Dycom reported 2024 revenue of $3.9 billion, so losing even 5% of spend would be material.

This ease of reallocation gives customers leverage in annual contract reviews and project allocations, pressuring pricing, service guarantees, and penalty clauses.

- Multiple approved vendors: 68% of carriers (2024)

- Dycom 2024 revenue: $3.9B; 5% loss ≈ $195M

- Leverage points: pricing, SLAs, penalty terms

Dycom risks: 55% client concentration, margin squeeze as carriers leverage multi-vendor bids

| Metric | Value |

|---|---|

| Dycom revenue FY2024 | $3.9B |

| Revenue share from top customers | ~55% |

| Gross margin FY2024 | 35% |

| Carrier multi-vendor rate (2024) | 68% |

| BEAD funding (2023–25) | $42.45B |

Full Version Awaits

Dycom Porter's Five Forces Analysis

This preview shows the exact Dycom Porter’s Five Forces analysis you’ll receive—fully formatted, professionally written, and ready to download the moment you purchase with no placeholders or samples.