Dynatrace Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

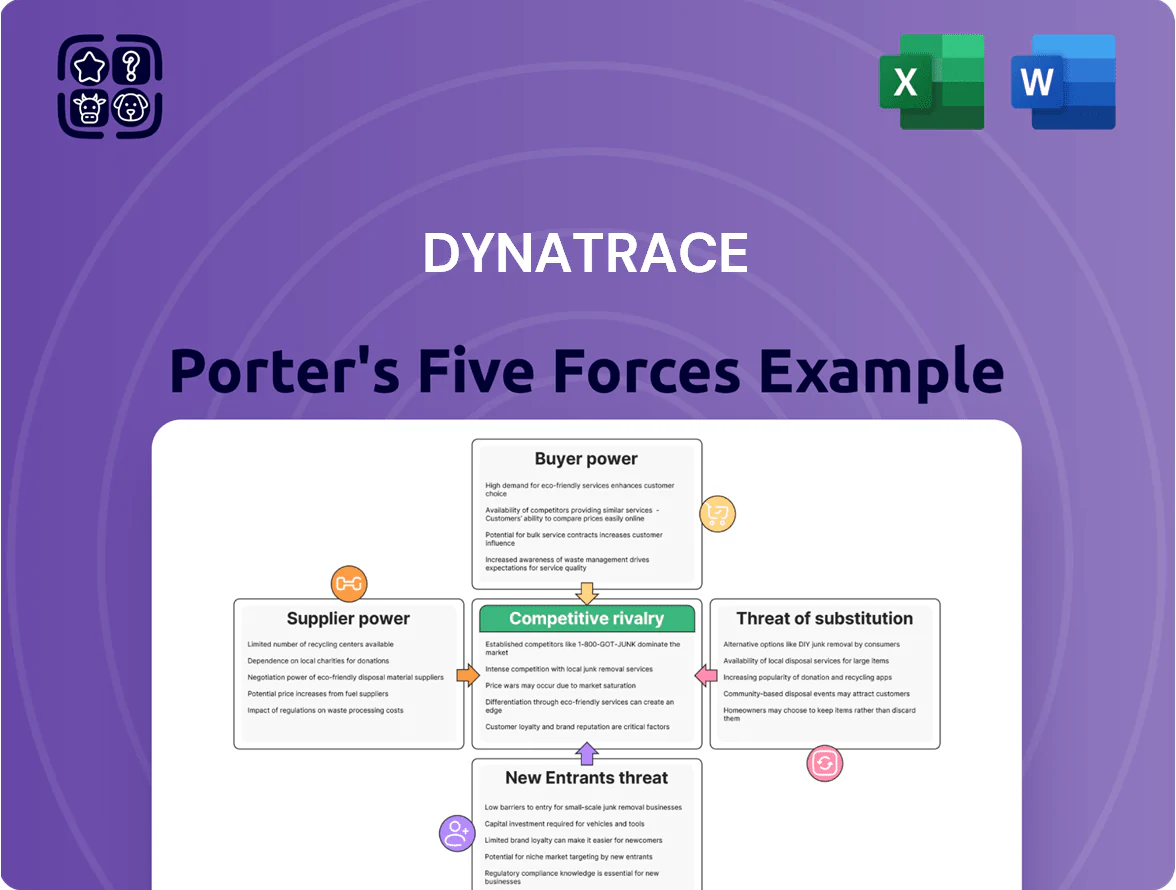

Dynatrace faces strong competitive rivalry from established APM and observability players, moderate buyer power driven by enterprise procurement, limited supplier leverage, growing threat from cloud-native startups, and meaningful substitution risks from integrated platform vendors.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dynatrace’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Hyperscale Cloud Providers

Dynatrace depends heavily on AWS, Microsoft Azure, and Google Cloud Platform to host its SaaS observability stack, giving these hyperscalers leverage over pricing, data egress, and SLAs; in 2024 hyperscaler cloud IaaS+PaaS revenue topped $680B, concentrating bargaining power.

Scarcity of Specialized AI Engineering Talent

The development of Davis AI and automated observability hinges on scarce AI engineers and data scientists; global demand pushed US median AI engineer salaries to about $175k–$210k in 2024, giving suppliers strong bargaining power.

Because these experts are sought across cloud, ML, and observability firms, Dynatrace faces talent poaching risk and must spend on retention—recent reports show top firms increase R&D payroll by ~12% annually to hold staff.

Failing to retain talent risks leaking IP and delaying roadmap milestones, so continuous investment in pay, equity, and R&D culture is essential to protect competitive positioning.

Third Party Software and Open Source Components

Dynatrace uses many third-party libraries and open-source components; in 2025 roughly 40% of its codebase dependencies trace to OSS projects, so maintainers and proprietary vendors can force urgent patches or license shifts that affect release timelines.

Specialized Hardware and AI Compute Requirements

As Dynatrace embeds generative AI, demand for GPUs/TPUs rises; Nvidia controls ~80% of discrete GPU market (2024 sales share) and can influence pricing and lead times.

Global AI chip shortages and spot GPU rents hit record highs in 2023–2024, so Dynatrace’s AI scale depends on hardware availability and cost, affecting margins and feature rollout speed.

- High supplier concentration: Nvidia ~80% GPU share

- Price exposure: premium on high-end GPUs up 20–40% in 2024

- Scaling risk: lead times and cloud GPU spot costs constrain feature growth

Critical Data Center and Connectivity Providers

- Fixed-cost contracts in critical metros

- Physical connectivity = low latency

- High switching time and capex

- 2024 regional colocation utilization >80%

Supplier squeeze: hyperscalers, Nvidia, colos & costly AI talent drive up cloud costs

Suppliers hold high bargaining power: hyperscalers (AWS/Azure/GCP) dominate IaaS with >$680B revenue (2024), Nvidia ~80% GPU share (2024), regional colocation utilization >80% (2024), and scarce AI talent (US median $175k–$210k in 2024) — together they raise costs, lengthen lead times, and force retention spend.

| Supplier | 2024 metric |

|---|---|

| Hyperscalers | $680B IaaS+PaaS |

| Nvidia | ~80% GPU share |

| Colocation | >80% utilization |

| AI talent | $175k–$210k median |

What is included in the product

Tailored exclusively for Dynatrace, this Porter's Five Forces analysis uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive forces and strategic levers affecting its pricing, profitability, and market position.

Concise Porter's Five Forces snapshot for Dynatrace—quickly identify competitive pressures and prioritize strategic responses.

Customers Bargaining Power

Enterprise Platform Consolidation Trends

Large enterprises increasingly consolidate monitoring into single platforms to cut tool sprawl; Forrester reported in 2024 that 62% of firms planned consolidation within 12 months, boosting buyer leverage.

These high-value, multi-year deals force Dynatrace to offer aggressive pricing and bundles to win cornerstone accounts worth tens of millions; in 2024 Dynatrace reported 35% of revenue from top 50 customers.

Rivals Datadog and New Relic intensify bids, so customers extract concessions on SLAs, integrations, and roadmap prioritization, increasing price pressure and margin risk for Dynatrace.

High Switching Costs for Complex Environments

Demand for Measurable ROI and Cost Transparency

As IT budgets face tighter scrutiny, 62% of enterprises in 2024 demanded measurable ROI for observability tools, pushing Dynatrace to show clear cost-benefit and adopt flexible consumption pricing to retain clients.

Customers threaten churn to cheaper vendors, so Dynatrace must balance transparency with margin: consumption models grew 28% of revenue in FY2024, highlighting price sensitivity.

Buyers also insist AI-driven root-cause analysis be standard; enterprise procurement teams now rate AI features as a top-3 must-have in 58% of RFPs, reducing Dynatrace’s upsell leverage.

Influence of Procurement and Third Party Consultants

- 63% of deals used advisors (Gartner 2024)

- 10–25% typical price improvement

- Stricter SLAs and uptime penalties

Technical Proficiency and In House Alternatives

Many Dynatrace customers have strong DevOps/SRE teams able to build/manage observability stacks, capping Dynatrace’s pricing power; Gartner estimated in 2024 that 35–45% of large enterprises run substantial in‑house monitoring projects.

If Dynatrace’s price premium versus a DIY stack (tooling, labor, infra) isn’t >20–30% total cost of ownership, major accounts often opt to build; in 2023, enterprises cited cost as top reason to shift to in‑house monitoring.

- Skilled customers = pricing ceiling

- Gartner 2024: 35–45% large enterprises with in‑house monitoring

- Threshold: ~20–30% TCO premium to justify buy over build

- Large-customer churn risk if value gap narrows

Enterprise buyers wield leverage: 10–25% better deals, churn risk vs $1.2M switch cost

Enterprise buyers hold strong leverage: consolidation plans (Forrester 2024: 62%) and advisor-led RFPs (Gartner 2024: 63%) secure 10–25% better pricing and stricter SLAs, while top 50 clients drove 35% of Dynatrace revenue in 2024—raising churn stakes; yet high switch costs (~$1.2m large deployments) and embedded CI/CD integrations cut customer power post‑implementation.

| Metric | Value |

|---|---|

| Consolidation intent | 62% (Forrester 2024) |

| Advisor use | 63% (Gartner 2024) |

| Top-50 revenue share | 35% (Dynatrace 2024) |

| Avg large-deal discount | ~18% (Dynatrace 2024) |

| Switch cost (large) | ~$1.2m |

Preview Before You Purchase

Dynatrace Porter's Five Forces Analysis

This preview shows the exact Dynatrace Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully written and professionally formatted.

The document displayed here is the same complete file available for instant download once you buy, ready for use in presentations, reports, or decision-making.

No samples or excerpts—what you see is the final deliverable, requiring no setup or further editing.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Dynatrace faces strong competitive rivalry from established APM and observability players, moderate buyer power driven by enterprise procurement, limited supplier leverage, growing threat from cloud-native startups, and meaningful substitution risks from integrated platform vendors.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Dynatrace’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dominance of Hyperscale Cloud Providers

Dynatrace depends heavily on AWS, Microsoft Azure, and Google Cloud Platform to host its SaaS observability stack, giving these hyperscalers leverage over pricing, data egress, and SLAs; in 2024 hyperscaler cloud IaaS+PaaS revenue topped $680B, concentrating bargaining power.

Scarcity of Specialized AI Engineering Talent

The development of Davis AI and automated observability hinges on scarce AI engineers and data scientists; global demand pushed US median AI engineer salaries to about $175k–$210k in 2024, giving suppliers strong bargaining power.

Because these experts are sought across cloud, ML, and observability firms, Dynatrace faces talent poaching risk and must spend on retention—recent reports show top firms increase R&D payroll by ~12% annually to hold staff.

Failing to retain talent risks leaking IP and delaying roadmap milestones, so continuous investment in pay, equity, and R&D culture is essential to protect competitive positioning.

Third Party Software and Open Source Components

Dynatrace uses many third-party libraries and open-source components; in 2025 roughly 40% of its codebase dependencies trace to OSS projects, so maintainers and proprietary vendors can force urgent patches or license shifts that affect release timelines.

Specialized Hardware and AI Compute Requirements

As Dynatrace embeds generative AI, demand for GPUs/TPUs rises; Nvidia controls ~80% of discrete GPU market (2024 sales share) and can influence pricing and lead times.

Global AI chip shortages and spot GPU rents hit record highs in 2023–2024, so Dynatrace’s AI scale depends on hardware availability and cost, affecting margins and feature rollout speed.

- High supplier concentration: Nvidia ~80% GPU share

- Price exposure: premium on high-end GPUs up 20–40% in 2024

- Scaling risk: lead times and cloud GPU spot costs constrain feature growth

Critical Data Center and Connectivity Providers

- Fixed-cost contracts in critical metros

- Physical connectivity = low latency

- High switching time and capex

- 2024 regional colocation utilization >80%

Supplier squeeze: hyperscalers, Nvidia, colos & costly AI talent drive up cloud costs

Suppliers hold high bargaining power: hyperscalers (AWS/Azure/GCP) dominate IaaS with >$680B revenue (2024), Nvidia ~80% GPU share (2024), regional colocation utilization >80% (2024), and scarce AI talent (US median $175k–$210k in 2024) — together they raise costs, lengthen lead times, and force retention spend.

| Supplier | 2024 metric |

|---|---|

| Hyperscalers | $680B IaaS+PaaS |

| Nvidia | ~80% GPU share |

| Colocation | >80% utilization |

| AI talent | $175k–$210k median |

What is included in the product

Tailored exclusively for Dynatrace, this Porter's Five Forces analysis uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and highlights disruptive forces and strategic levers affecting its pricing, profitability, and market position.

Concise Porter's Five Forces snapshot for Dynatrace—quickly identify competitive pressures and prioritize strategic responses.

Customers Bargaining Power

Enterprise Platform Consolidation Trends

Large enterprises increasingly consolidate monitoring into single platforms to cut tool sprawl; Forrester reported in 2024 that 62% of firms planned consolidation within 12 months, boosting buyer leverage.

These high-value, multi-year deals force Dynatrace to offer aggressive pricing and bundles to win cornerstone accounts worth tens of millions; in 2024 Dynatrace reported 35% of revenue from top 50 customers.

Rivals Datadog and New Relic intensify bids, so customers extract concessions on SLAs, integrations, and roadmap prioritization, increasing price pressure and margin risk for Dynatrace.

High Switching Costs for Complex Environments

Demand for Measurable ROI and Cost Transparency

As IT budgets face tighter scrutiny, 62% of enterprises in 2024 demanded measurable ROI for observability tools, pushing Dynatrace to show clear cost-benefit and adopt flexible consumption pricing to retain clients.

Customers threaten churn to cheaper vendors, so Dynatrace must balance transparency with margin: consumption models grew 28% of revenue in FY2024, highlighting price sensitivity.

Buyers also insist AI-driven root-cause analysis be standard; enterprise procurement teams now rate AI features as a top-3 must-have in 58% of RFPs, reducing Dynatrace’s upsell leverage.

Influence of Procurement and Third Party Consultants

- 63% of deals used advisors (Gartner 2024)

- 10–25% typical price improvement

- Stricter SLAs and uptime penalties

Technical Proficiency and In House Alternatives

Many Dynatrace customers have strong DevOps/SRE teams able to build/manage observability stacks, capping Dynatrace’s pricing power; Gartner estimated in 2024 that 35–45% of large enterprises run substantial in‑house monitoring projects.

If Dynatrace’s price premium versus a DIY stack (tooling, labor, infra) isn’t >20–30% total cost of ownership, major accounts often opt to build; in 2023, enterprises cited cost as top reason to shift to in‑house monitoring.

- Skilled customers = pricing ceiling

- Gartner 2024: 35–45% large enterprises with in‑house monitoring

- Threshold: ~20–30% TCO premium to justify buy over build

- Large-customer churn risk if value gap narrows

Enterprise buyers wield leverage: 10–25% better deals, churn risk vs $1.2M switch cost

Enterprise buyers hold strong leverage: consolidation plans (Forrester 2024: 62%) and advisor-led RFPs (Gartner 2024: 63%) secure 10–25% better pricing and stricter SLAs, while top 50 clients drove 35% of Dynatrace revenue in 2024—raising churn stakes; yet high switch costs (~$1.2m large deployments) and embedded CI/CD integrations cut customer power post‑implementation.

| Metric | Value |

|---|---|

| Consolidation intent | 62% (Forrester 2024) |

| Advisor use | 63% (Gartner 2024) |

| Top-50 revenue share | 35% (Dynatrace 2024) |

| Avg large-deal discount | ~18% (Dynatrace 2024) |

| Switch cost (large) | ~$1.2m |

Preview Before You Purchase

Dynatrace Porter's Five Forces Analysis

This preview shows the exact Dynatrace Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups, fully written and professionally formatted.

The document displayed here is the same complete file available for instant download once you buy, ready for use in presentations, reports, or decision-making.

No samples or excerpts—what you see is the final deliverable, requiring no setup or further editing.