Eagers Automotive Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

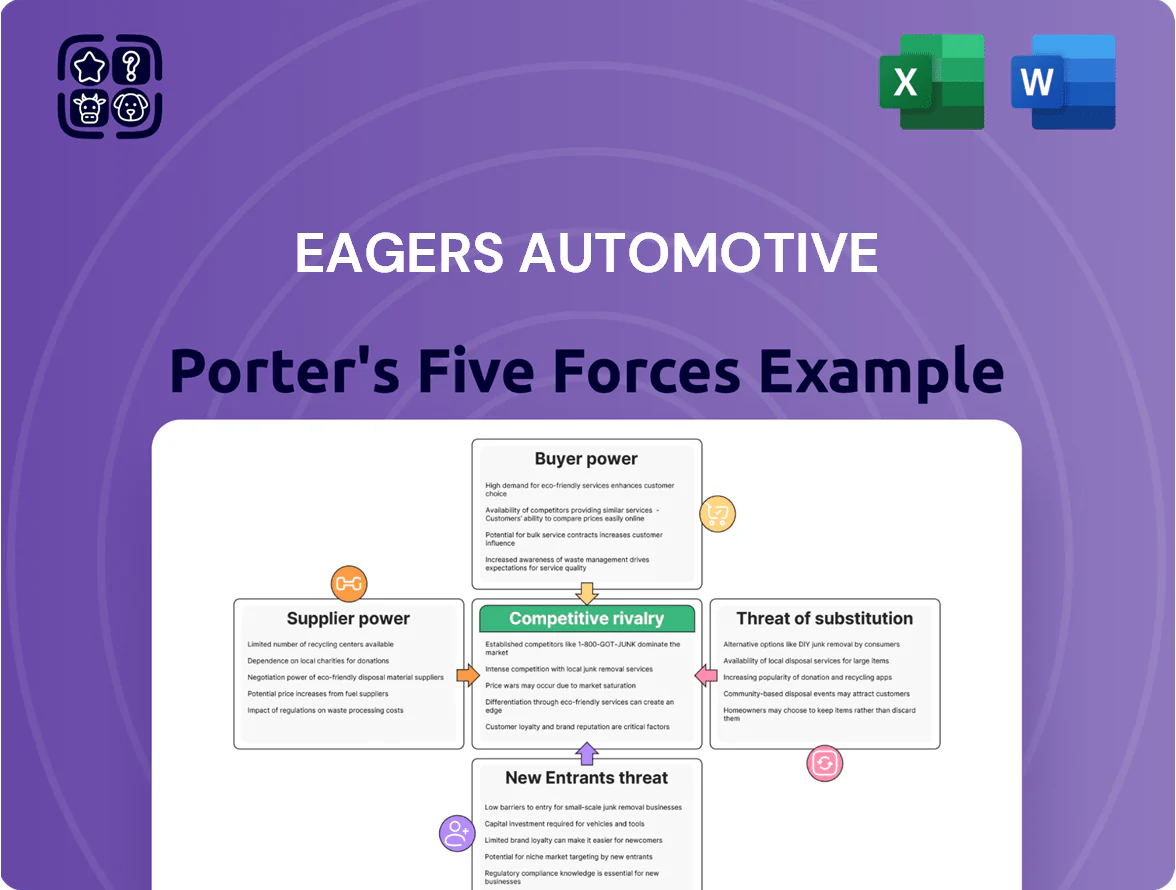

Eagers Automotive faces moderate supplier power, high buyer price sensitivity, intense rivalry among dealership groups, low threat of new entrants but rising substitution from online platforms; this snapshot highlights key pressures on margins and growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to Eagers Automotive.

Suppliers Bargaining Power

OEM Brand Concentration

Global OEMs wield high supplier power: Toyota and BYD accounted for about 38% of Eagers Automotive’s new-vehicle supply in FY2024, so their model allocations and brand strategy shape margins and footfall.

Maintaining dealer agreements with Toyota Motor Corporation and BYD Company Limited is critical—supply cuts or global production shifts can trim Eagers’ inventory days (currently ~38 days) and reduce FY2024 revenue exposure (~55% from new-car sales).

Transition to Agency Model

EV Inventory Control

As EVs rise, suppliers wield more power via batteries and software; global battery shortages in 2024 tightened allocations, letting OEMs prioritize dealers—Eagers reported EV mix rising to ~8% of group sales in FY2025, so supplier allocation affects which franchises get high-demand models. OEMs can set dealer terms and limited allocations, forcing Eagers to invest: the group disclosed ~A$15–20m capex 2024–25 for EV charging and facility upgrades to meet supplier standards.

Exclusive Distribution Rights

Exclusive territorial rights shield Eagers Automotive from local rivals for a brand but raise supplier power by tying significant revenue to that brand’s performance; in FY2024 Eagers reported motor vehicle sales of AU$9.2bn, leaving concentrated exposure where one weak brand could cut a material share of sales.

Limited recourse exists if a brand loses appeal because finding a replacement supplier or renegotiating territory clauses takes months and can reduce same-store sales sharply; dealer inventory and marketing spend also remain vendor-dependent.

- Protects local market share

- Creates dependency on supplier brand health

- FY2024 vehicle sales AU$9.2bn — material risk

- Replacement or renegotiation is slow, reducing short-term options

Parts and Component Monopolies

Genuine parts for repairs and maintenance are tightly controlled by original equipment manufacturers, forcing Eagers Automotive to buy branded components to preserve warranties and service quality.

That reliance boosts supplier leverage over margins in the after-sales parts segment; in FY2024 Eagers reported 32% gross margin in after-sales where parts sales contribute ~28% of aftermarket revenue, so supplier pricing shifts materially affect profit.

- OEM control raises switching costs

- After-sales ~28% revenue, 32% gross margin (FY2024)

- Suppliers can compress dealer margins

Supplier concentration hits dealers: Toyota+BYD 38%, margins down, EV shift rising

Suppliers hold high leverage: Toyota and BYD supplied ~38% of new cars to Eagers in FY2024, and OEM moves to agency models cut dealer pricing power—industry gross margins fell ~1.2 ppt in FY2024. EV battery/software allocation and branded parts raise switching costs; EV mix ~8% FY2025 and A$15–20m capex 2024–25. FY2024 vehicle sales AU$9.2bn; after-sales ~28% revenue, 32% gross margin.

| Metric | Value |

|---|---|

| Toyota+BYD share (new cars) | ~38% |

| Inventory days | ~38 days |

| EV mix | ~8% (FY2025) |

| FY2024 vehicle sales | AU$9.2bn |

| After-sales revenue / margin | ~28% / 32% |

| Capex for EV readiness | A$15–20m (2024–25) |

What is included in the product

Provides a concise Porter’s Five Forces overview for Eagers Automotive, highlighting competitive rivalry, buyer/supplier power, entry barriers, and substitute threats with strategic implications for pricing and profitability.

A concise Porter's Five Forces snapshot for Eagers Automotive—quickly gauge competitive threats and supplier/buyer leverage to streamline strategic choices.

Customers Bargaining Power

Information Symmetry and Price Transparency

Modern buyers use tools like Carsales and Autotrader to compare prices instantly, and Australian online listings rose 18% YoY in 2024, tightening price transparency and reducing Eagers Automotive’s scope to charge premiums without clear value adds.

With new-vehicle gross margins at ~6–8% industry-wide (2024 RBNZ/industry data) and used-car price indices down 3.5% in 2024, well-informed customers know market value, trade-in benchmarks, and typical dealer margins, strengthening their bargaining position.

Low Switching Costs

There is minimal financial cost for buyers to switch dealers or brands, so price, stock availability and immediate finance deals drive choices; in Australia 2024 data showed 62% of new-car buyers cited price or incentives as the primary purchase factor. Eagers must therefore invest in superior customer experience and services—aftercare, fast finance approvals, and digital retailing—to reduce churn; every 1% retention lift can add roughly A$15–25m in annual gross profit given Eagers’ ~A$1.5–2.5bn annual gross profit range.

Financing and Insurance Sensitivity

Buyers can choose third-party banks and fintech lenders for financing; in Australia fintech market lending grew ~18% in 2024, increasing outside options for Eagers Automotive customers. If Eagers offers higher rates or rigid terms, customers will unbundle finance and insurance (F&I) services and use external lenders. F&I commissions—often 3–7% of vehicle margin—face pressure as lenders and brokers capture more volume. In 2024 dealer-originated loans fell ~4% industry-wide, signaling rising customer sensitivity.

Used Car Market Alternatives

Peer-to-peer platforms let buyers bypass dealerships; private listings grew 18% in Australian used-vehicle listings in 2024, eroding foot traffic to Eagers Automotive.

Customers compare Eagers’ retail stock directly with Carsales and Facebook Marketplace, where median private-sale prices were ~12% lower in 2024, raising price sensitivity.

To justify margins, Eagers must offer longer certified reconditioning and warranties—industry cert warranties averaging 3 years add perceived value and support higher prices.

- Private listings +18% (2024)

- Median private price ~12% below dealer (2024)

- Certified warranty ~3 years common

Fleet Buyer Negotiating Leverage

- Fleet discounts typically 20–30%

- Fleet share ~18% of new-vehicle volume (FY2024)

- Group gross profit margin ~6.1% (FY2024)

- Risk: high volume, thin margins

Pricing Pressure: Online Listings +18% and Fleet Discounts Squeeze Eagers’ Margins

Customers have strong bargaining power: online listings rose 18% YoY (2024) and median private prices were ~12% lower, while new-vehicle margins sat at ~6–8% and group gross profit was ~6.1% (FY2024), so price, finance and fast service drive buys; fleet buyers (~18% of new volume) demand 20–30% discounts, pressuring margins and forcing Eagers to add warranties and digital retailing to retain customers.

| Metric | 2024/ FY2024 |

|---|---|

| Online listings growth | +18% YoY |

| Median private vs dealer price | ~12% lower |

| New-vehicle gross margins (industry) | ~6–8% |

| Eagers group gross profit margin | ~6.1% |

| Fleet share of new volume | ~18% |

| Fleet discount range | 20–30% |

Full Version Awaits

Eagers Automotive Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Eagers Automotive you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is part of the full, professionally written report you’ll get—fully formatted and ready for download the moment you buy.

No mockups or samples: the file you see here is the final deliverable and will be available to you instantly after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Eagers Automotive faces moderate supplier power, high buyer price sensitivity, intense rivalry among dealership groups, low threat of new entrants but rising substitution from online platforms; this snapshot highlights key pressures on margins and growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and strategic implications tailored to Eagers Automotive.

Suppliers Bargaining Power

OEM Brand Concentration

Global OEMs wield high supplier power: Toyota and BYD accounted for about 38% of Eagers Automotive’s new-vehicle supply in FY2024, so their model allocations and brand strategy shape margins and footfall.

Maintaining dealer agreements with Toyota Motor Corporation and BYD Company Limited is critical—supply cuts or global production shifts can trim Eagers’ inventory days (currently ~38 days) and reduce FY2024 revenue exposure (~55% from new-car sales).

Transition to Agency Model

EV Inventory Control

As EVs rise, suppliers wield more power via batteries and software; global battery shortages in 2024 tightened allocations, letting OEMs prioritize dealers—Eagers reported EV mix rising to ~8% of group sales in FY2025, so supplier allocation affects which franchises get high-demand models. OEMs can set dealer terms and limited allocations, forcing Eagers to invest: the group disclosed ~A$15–20m capex 2024–25 for EV charging and facility upgrades to meet supplier standards.

Exclusive Distribution Rights

Exclusive territorial rights shield Eagers Automotive from local rivals for a brand but raise supplier power by tying significant revenue to that brand’s performance; in FY2024 Eagers reported motor vehicle sales of AU$9.2bn, leaving concentrated exposure where one weak brand could cut a material share of sales.

Limited recourse exists if a brand loses appeal because finding a replacement supplier or renegotiating territory clauses takes months and can reduce same-store sales sharply; dealer inventory and marketing spend also remain vendor-dependent.

- Protects local market share

- Creates dependency on supplier brand health

- FY2024 vehicle sales AU$9.2bn — material risk

- Replacement or renegotiation is slow, reducing short-term options

Parts and Component Monopolies

Genuine parts for repairs and maintenance are tightly controlled by original equipment manufacturers, forcing Eagers Automotive to buy branded components to preserve warranties and service quality.

That reliance boosts supplier leverage over margins in the after-sales parts segment; in FY2024 Eagers reported 32% gross margin in after-sales where parts sales contribute ~28% of aftermarket revenue, so supplier pricing shifts materially affect profit.

- OEM control raises switching costs

- After-sales ~28% revenue, 32% gross margin (FY2024)

- Suppliers can compress dealer margins

Supplier concentration hits dealers: Toyota+BYD 38%, margins down, EV shift rising

Suppliers hold high leverage: Toyota and BYD supplied ~38% of new cars to Eagers in FY2024, and OEM moves to agency models cut dealer pricing power—industry gross margins fell ~1.2 ppt in FY2024. EV battery/software allocation and branded parts raise switching costs; EV mix ~8% FY2025 and A$15–20m capex 2024–25. FY2024 vehicle sales AU$9.2bn; after-sales ~28% revenue, 32% gross margin.

| Metric | Value |

|---|---|

| Toyota+BYD share (new cars) | ~38% |

| Inventory days | ~38 days |

| EV mix | ~8% (FY2025) |

| FY2024 vehicle sales | AU$9.2bn |

| After-sales revenue / margin | ~28% / 32% |

| Capex for EV readiness | A$15–20m (2024–25) |

What is included in the product

Provides a concise Porter’s Five Forces overview for Eagers Automotive, highlighting competitive rivalry, buyer/supplier power, entry barriers, and substitute threats with strategic implications for pricing and profitability.

A concise Porter's Five Forces snapshot for Eagers Automotive—quickly gauge competitive threats and supplier/buyer leverage to streamline strategic choices.

Customers Bargaining Power

Information Symmetry and Price Transparency

Modern buyers use tools like Carsales and Autotrader to compare prices instantly, and Australian online listings rose 18% YoY in 2024, tightening price transparency and reducing Eagers Automotive’s scope to charge premiums without clear value adds.

With new-vehicle gross margins at ~6–8% industry-wide (2024 RBNZ/industry data) and used-car price indices down 3.5% in 2024, well-informed customers know market value, trade-in benchmarks, and typical dealer margins, strengthening their bargaining position.

Low Switching Costs

There is minimal financial cost for buyers to switch dealers or brands, so price, stock availability and immediate finance deals drive choices; in Australia 2024 data showed 62% of new-car buyers cited price or incentives as the primary purchase factor. Eagers must therefore invest in superior customer experience and services—aftercare, fast finance approvals, and digital retailing—to reduce churn; every 1% retention lift can add roughly A$15–25m in annual gross profit given Eagers’ ~A$1.5–2.5bn annual gross profit range.

Financing and Insurance Sensitivity

Buyers can choose third-party banks and fintech lenders for financing; in Australia fintech market lending grew ~18% in 2024, increasing outside options for Eagers Automotive customers. If Eagers offers higher rates or rigid terms, customers will unbundle finance and insurance (F&I) services and use external lenders. F&I commissions—often 3–7% of vehicle margin—face pressure as lenders and brokers capture more volume. In 2024 dealer-originated loans fell ~4% industry-wide, signaling rising customer sensitivity.

Used Car Market Alternatives

Peer-to-peer platforms let buyers bypass dealerships; private listings grew 18% in Australian used-vehicle listings in 2024, eroding foot traffic to Eagers Automotive.

Customers compare Eagers’ retail stock directly with Carsales and Facebook Marketplace, where median private-sale prices were ~12% lower in 2024, raising price sensitivity.

To justify margins, Eagers must offer longer certified reconditioning and warranties—industry cert warranties averaging 3 years add perceived value and support higher prices.

- Private listings +18% (2024)

- Median private price ~12% below dealer (2024)

- Certified warranty ~3 years common

Fleet Buyer Negotiating Leverage

- Fleet discounts typically 20–30%

- Fleet share ~18% of new-vehicle volume (FY2024)

- Group gross profit margin ~6.1% (FY2024)

- Risk: high volume, thin margins

Pricing Pressure: Online Listings +18% and Fleet Discounts Squeeze Eagers’ Margins

Customers have strong bargaining power: online listings rose 18% YoY (2024) and median private prices were ~12% lower, while new-vehicle margins sat at ~6–8% and group gross profit was ~6.1% (FY2024), so price, finance and fast service drive buys; fleet buyers (~18% of new volume) demand 20–30% discounts, pressuring margins and forcing Eagers to add warranties and digital retailing to retain customers.

| Metric | 2024/ FY2024 |

|---|---|

| Online listings growth | +18% YoY |

| Median private vs dealer price | ~12% lower |

| New-vehicle gross margins (industry) | ~6–8% |

| Eagers group gross profit margin | ~6.1% |

| Fleet share of new volume | ~18% |

| Fleet discount range | 20–30% |

Full Version Awaits

Eagers Automotive Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Eagers Automotive you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is part of the full, professionally written report you’ll get—fully formatted and ready for download the moment you buy.

No mockups or samples: the file you see here is the final deliverable and will be available to you instantly after payment.