EastGroup Properties Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

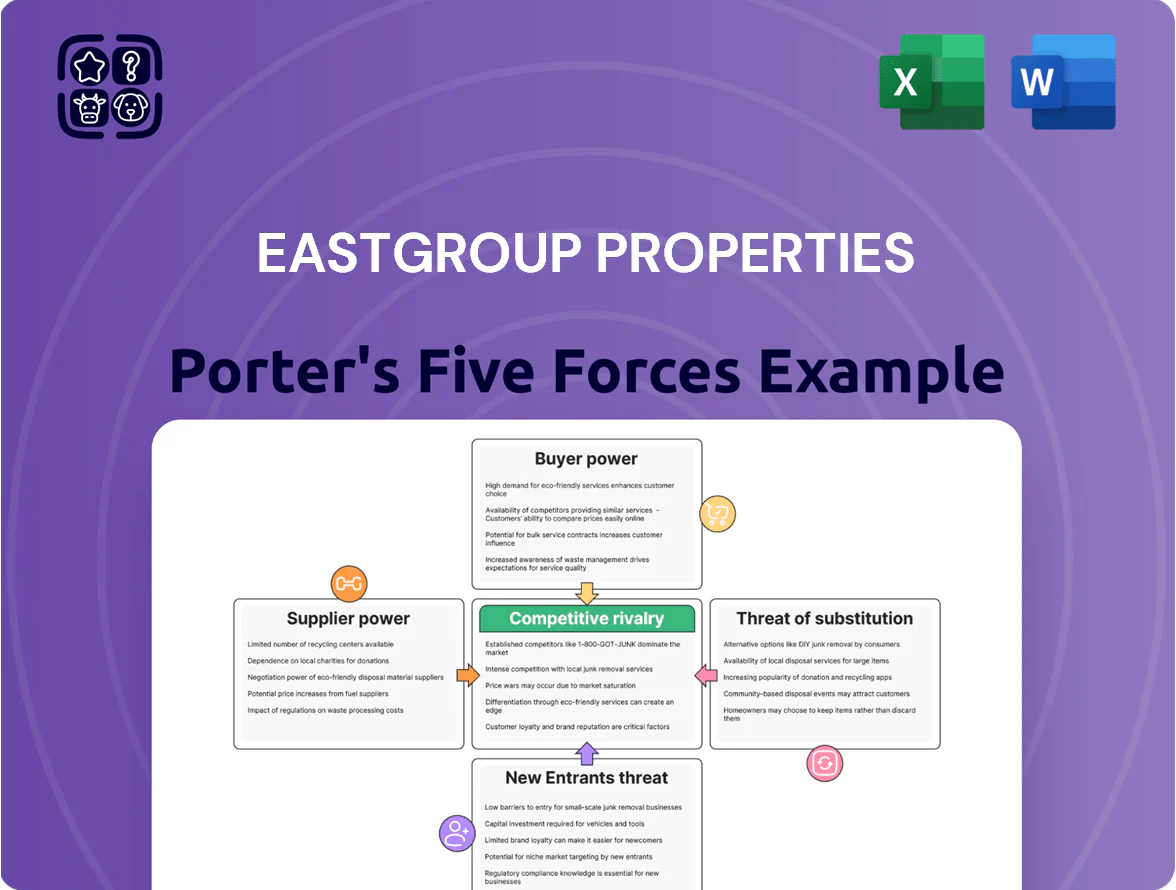

EastGroup Properties operates in a specialized industrial REIT niche where strong tenant demand and limited specialized supply raise barriers for new entrants, while moderate buyer and supplier power balance rent negotiation dynamics and construction cost risks.

Competitive rivalry centers on location, logistics connectivity, and development pipeline, with substitution threats low but regulatory and interest-rate sensitivity notable for valuation and cash flow stability.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore EastGroup Properties’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Infill Land Sites

Scarcity of infill land in Sunbelt high-growth metros gives landowners strong leverage; CBRE reported in 2024 that available industrial land in top 12 Sunbelt markets fell by 18% year-over-year, pushing average per-acre prices up 12% to $1.2m in 2024.

Construction Material and Labor Costs

Construction material and labor costs—steel up ~18% and ready-mix concrete up ~9% year-over-year in 2024—drive volatility for REITs like EastGroup Properties (EGP). Suppliers can squeeze margins during tight regional demand; US industrial construction spending rose 6.5% in 2024, raising bid prices. EastGroup must keep strong contractor ties and fixed-price clauses to limit delays and cost overruns in its 2025 development pipeline.

Regulatory and Municipal Constraints

Local governments function as gatekeeper suppliers: permits and zoning control access to developable land, and in 2024 Sunbelt metros saw a 12–18% drop in available industrial parcels per CoStar data, tightening supply.

Tighter environmental rules—like California’s 2024 CEQA updates and rising stormwater fees (up 9% median in 2023)—raise approval times and capex, giving municipalities leverage over project costs and schedules.

Access to Institutional Capital

As a REIT, EastGroup Properties relies on equity and debt markets for acquisitions and development; banks and institutional investors thus hold real bargaining power that rises when interest rates climb and liquidity tightens.

By late 2025, higher U.S. Treasury yields (10y ~4.5% in Dec 2025) and bank lending spreads push EastGroup's blended cost of debt above its 2021–2023 range, constraining new deal IRRs and pressuring share issuance terms.

Capital access limits growth when debt service coverage falls or share dilution becomes costly; maintaining leverage near its 30–40% targeted debt-to-market-cap range helps, but markets drive timing and price.

- Dependence: equity + debt fund growth

- Drivers: interest rates, liquidity (10y ~4.5% Dec 2025)

- Impact: higher debt service, tougher share issuance

- Mitigation: keep leverage ~30–40%

Utility and Infrastructure Providers

Industrial properties need reliable power, water, and high-speed data to satisfy modern logistics tenants, and regional utility monopolies leave EastGroup Properties little leverage over pricing or service terms.

Automated warehouses and EV charging raise site energy demand; U.S. warehouse electricity use rose ~25% from 2015–2020 and EV charging forecasts project >3x growth by 2030, increasing supplier importance.

EastGroup faces concentrated supplier risk that can raise operating costs and capex for grid upgrades, often passed to tenants or absorbed in higher landlord investment.

Suppliers squeeze EastGroup: scarce Sunbelt land, rising materials, and tighter capital

Suppliers hold meaningful power over EastGroup: scarce Sunbelt land (industrial land down 18% YoY; avg $1.2m/acre in 2024), rising materials (steel +18%, concrete +9% in 2024), utility monopolies driving higher site energy needs (+25% warehouse electricity 2015–2020), and capital markets tightening (10y ~4.5% Dec 2025) that raise debt costs and constrain growth.

| Metric | Value |

|---|---|

| Land availability | -18% YoY (2024) |

| Avg land price | $1.2m/acre (2024) |

| Steel | +18% (2024) |

| 10y Treasury | ~4.5% (Dec 2025) |

What is included in the product

Tailored exclusively for EastGroup Properties, this Porter's Five Forces overview uncovers competitive pressures, buyer/supplier influence, entry barriers, substitutes, and disruptive threats shaping the company’s industrial REIT positioning.

A concise, one-sheet Porter's Five Forces summary for EastGroup Properties—ideal for rapid strategic decisions and boardroom slides.

Customers Bargaining Power

Tenant Concentration and Diversification

EastGroup Properties keeps tenant concentration low: top-10 tenants accounted for about 11% of ABR (annual base rent) in 2024, cutting single-customer leverage and lowering bargaining power.

By targeting small-to-mid box industrial spaces (median unit ~30,000 sq ft), EastGroup avoids dependence on big e-commerce tenants that pushed concessions elsewhere in 2023–24.

This granular, multi-tenant mix supported rent growth of ~6% in 2024 and helped sustain pricing power across its distribution portfolio.

High Switching Costs for Logistics

Moving a distribution center costs carriers and shippers an average of $350,000–$1.2M per facility for inventory relocation, racking and specialized equipment, plus 6–12 weeks of downtime, per industry surveys in 2023–2024. These high switching costs deter tenants from leaving EastGroup Properties for minor rent cuts, boosting retention: EastGroup reported same-store cash NOI growth of 5.6% in 2024, reflecting sticky occupancy. Customers tied to local delivery routes—last-mile operators—show >90% renewal propensity, so EastGroup captures steady cash flow and lower leasing churn.

Strategic Importance of Location

EastGroup tenants—primarily logistics and light industrial firms—pay a premium for Sunbelt infill locations near ports, interstates, and metros; 2025 leasing surveys show Sunbelt rents ran 12–18% above national averages.

Because EastGroup (EGP) focuses on scarce infill sites, tenants face limited substitutes, lowering renewal bargaining power; EGP reported 95% occupancy in 2024, supporting stable rent resets.

Economic Health of the Small Business Sector

A large share of EastGroup Properties tenants are local and regional distributors whose bargaining power tracks the small-business sector’s health; US small business revenue fell 3.7% in 2023 but grew 4.1% in 2024, so tenant willingness to accept market-rate renewals recovered last year. In a strong economy these distributors accept rent increases to secure functional, flexible industrial space; during downturns they lobby for rent relief or smaller footprints, increasing tenant leverage. Rent abatements and shorter lease terms rose 12% across industrial portfolios in 2024, a sign of negotiating strength when needed.

- 2024 small-business revenue +4.1%

- 2023 small-business revenue -3.7%

- Industrial rent abatements +12% in 2024

Availability of Competing Industrial Inventory

Customer bargaining power rises when submarket vacancy climbs—Phoenix, Dallas, and Orlando saw industrial vacancy averages of about 5.0%, 6.2%, and 4.8% respectively in Q4 2025, giving tenants more leverage as new supply arrives.

Tenants can pit landlords for concessions on rents and TI (tenant improvements), but EastGroup’s portfolio of high-quality, functional buildings in supply-constrained corridors—where submarket vacancy often sits 200–400 bps below the metro average—reduces that pressure.

- Q4 2025 vacancy: Phoenix 5.0%, Dallas 6.2%, Orlando 4.8%

- New supply increases tenant leverage on rents and concessions

- EastGroup focus: quality assets in constrained submarkets; vacancy 2–4% lower

EastGroup: Strong tenant lock-in but rising abatements give occasional leverage

EastGroup faces moderate customer bargaining power: low tenant concentration (top-10 = ~11% ABR in 2024), high switching costs ($350k–$1.2M, 6–12 weeks), 95% occupancy and 5.6% same-store NOI growth in 2024 limit tenant leverage, but rising submarket vacancy and 12% uptick in abatements in 2024 give tenants episodic negotiating power.

| Metric | Value |

|---|---|

| Top-10 ABR | ~11% (2024) |

| Occupancy | 95% (2024) |

| Same-store NOI | +5.6% (2024) |

| Switching cost | $350k–$1.2M (2023–24) |

| Rent abatements | +12% (2024) |

Preview the Actual Deliverable

EastGroup Properties Porter's Five Forces Analysis

This preview shows the exact EastGroup Properties Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy, fully formatted and professionally written.

No mockups or samples: this is the actual, final deliverable available instantly after payment, ready for immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

EastGroup Properties operates in a specialized industrial REIT niche where strong tenant demand and limited specialized supply raise barriers for new entrants, while moderate buyer and supplier power balance rent negotiation dynamics and construction cost risks.

Competitive rivalry centers on location, logistics connectivity, and development pipeline, with substitution threats low but regulatory and interest-rate sensitivity notable for valuation and cash flow stability.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore EastGroup Properties’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of Infill Land Sites

Scarcity of infill land in Sunbelt high-growth metros gives landowners strong leverage; CBRE reported in 2024 that available industrial land in top 12 Sunbelt markets fell by 18% year-over-year, pushing average per-acre prices up 12% to $1.2m in 2024.

Construction Material and Labor Costs

Construction material and labor costs—steel up ~18% and ready-mix concrete up ~9% year-over-year in 2024—drive volatility for REITs like EastGroup Properties (EGP). Suppliers can squeeze margins during tight regional demand; US industrial construction spending rose 6.5% in 2024, raising bid prices. EastGroup must keep strong contractor ties and fixed-price clauses to limit delays and cost overruns in its 2025 development pipeline.

Regulatory and Municipal Constraints

Local governments function as gatekeeper suppliers: permits and zoning control access to developable land, and in 2024 Sunbelt metros saw a 12–18% drop in available industrial parcels per CoStar data, tightening supply.

Tighter environmental rules—like California’s 2024 CEQA updates and rising stormwater fees (up 9% median in 2023)—raise approval times and capex, giving municipalities leverage over project costs and schedules.

Access to Institutional Capital

As a REIT, EastGroup Properties relies on equity and debt markets for acquisitions and development; banks and institutional investors thus hold real bargaining power that rises when interest rates climb and liquidity tightens.

By late 2025, higher U.S. Treasury yields (10y ~4.5% in Dec 2025) and bank lending spreads push EastGroup's blended cost of debt above its 2021–2023 range, constraining new deal IRRs and pressuring share issuance terms.

Capital access limits growth when debt service coverage falls or share dilution becomes costly; maintaining leverage near its 30–40% targeted debt-to-market-cap range helps, but markets drive timing and price.

- Dependence: equity + debt fund growth

- Drivers: interest rates, liquidity (10y ~4.5% Dec 2025)

- Impact: higher debt service, tougher share issuance

- Mitigation: keep leverage ~30–40%

Utility and Infrastructure Providers

Industrial properties need reliable power, water, and high-speed data to satisfy modern logistics tenants, and regional utility monopolies leave EastGroup Properties little leverage over pricing or service terms.

Automated warehouses and EV charging raise site energy demand; U.S. warehouse electricity use rose ~25% from 2015–2020 and EV charging forecasts project >3x growth by 2030, increasing supplier importance.

EastGroup faces concentrated supplier risk that can raise operating costs and capex for grid upgrades, often passed to tenants or absorbed in higher landlord investment.

Suppliers squeeze EastGroup: scarce Sunbelt land, rising materials, and tighter capital

Suppliers hold meaningful power over EastGroup: scarce Sunbelt land (industrial land down 18% YoY; avg $1.2m/acre in 2024), rising materials (steel +18%, concrete +9% in 2024), utility monopolies driving higher site energy needs (+25% warehouse electricity 2015–2020), and capital markets tightening (10y ~4.5% Dec 2025) that raise debt costs and constrain growth.

| Metric | Value |

|---|---|

| Land availability | -18% YoY (2024) |

| Avg land price | $1.2m/acre (2024) |

| Steel | +18% (2024) |

| 10y Treasury | ~4.5% (Dec 2025) |

What is included in the product

Tailored exclusively for EastGroup Properties, this Porter's Five Forces overview uncovers competitive pressures, buyer/supplier influence, entry barriers, substitutes, and disruptive threats shaping the company’s industrial REIT positioning.

A concise, one-sheet Porter's Five Forces summary for EastGroup Properties—ideal for rapid strategic decisions and boardroom slides.

Customers Bargaining Power

Tenant Concentration and Diversification

EastGroup Properties keeps tenant concentration low: top-10 tenants accounted for about 11% of ABR (annual base rent) in 2024, cutting single-customer leverage and lowering bargaining power.

By targeting small-to-mid box industrial spaces (median unit ~30,000 sq ft), EastGroup avoids dependence on big e-commerce tenants that pushed concessions elsewhere in 2023–24.

This granular, multi-tenant mix supported rent growth of ~6% in 2024 and helped sustain pricing power across its distribution portfolio.

High Switching Costs for Logistics

Moving a distribution center costs carriers and shippers an average of $350,000–$1.2M per facility for inventory relocation, racking and specialized equipment, plus 6–12 weeks of downtime, per industry surveys in 2023–2024. These high switching costs deter tenants from leaving EastGroup Properties for minor rent cuts, boosting retention: EastGroup reported same-store cash NOI growth of 5.6% in 2024, reflecting sticky occupancy. Customers tied to local delivery routes—last-mile operators—show >90% renewal propensity, so EastGroup captures steady cash flow and lower leasing churn.

Strategic Importance of Location

EastGroup tenants—primarily logistics and light industrial firms—pay a premium for Sunbelt infill locations near ports, interstates, and metros; 2025 leasing surveys show Sunbelt rents ran 12–18% above national averages.

Because EastGroup (EGP) focuses on scarce infill sites, tenants face limited substitutes, lowering renewal bargaining power; EGP reported 95% occupancy in 2024, supporting stable rent resets.

Economic Health of the Small Business Sector

A large share of EastGroup Properties tenants are local and regional distributors whose bargaining power tracks the small-business sector’s health; US small business revenue fell 3.7% in 2023 but grew 4.1% in 2024, so tenant willingness to accept market-rate renewals recovered last year. In a strong economy these distributors accept rent increases to secure functional, flexible industrial space; during downturns they lobby for rent relief or smaller footprints, increasing tenant leverage. Rent abatements and shorter lease terms rose 12% across industrial portfolios in 2024, a sign of negotiating strength when needed.

- 2024 small-business revenue +4.1%

- 2023 small-business revenue -3.7%

- Industrial rent abatements +12% in 2024

Availability of Competing Industrial Inventory

Customer bargaining power rises when submarket vacancy climbs—Phoenix, Dallas, and Orlando saw industrial vacancy averages of about 5.0%, 6.2%, and 4.8% respectively in Q4 2025, giving tenants more leverage as new supply arrives.

Tenants can pit landlords for concessions on rents and TI (tenant improvements), but EastGroup’s portfolio of high-quality, functional buildings in supply-constrained corridors—where submarket vacancy often sits 200–400 bps below the metro average—reduces that pressure.

- Q4 2025 vacancy: Phoenix 5.0%, Dallas 6.2%, Orlando 4.8%

- New supply increases tenant leverage on rents and concessions

- EastGroup focus: quality assets in constrained submarkets; vacancy 2–4% lower

EastGroup: Strong tenant lock-in but rising abatements give occasional leverage

EastGroup faces moderate customer bargaining power: low tenant concentration (top-10 = ~11% ABR in 2024), high switching costs ($350k–$1.2M, 6–12 weeks), 95% occupancy and 5.6% same-store NOI growth in 2024 limit tenant leverage, but rising submarket vacancy and 12% uptick in abatements in 2024 give tenants episodic negotiating power.

| Metric | Value |

|---|---|

| Top-10 ABR | ~11% (2024) |

| Occupancy | 95% (2024) |

| Same-store NOI | +5.6% (2024) |

| Switching cost | $350k–$1.2M (2023–24) |

| Rent abatements | +12% (2024) |

Preview the Actual Deliverable

EastGroup Properties Porter's Five Forces Analysis

This preview shows the exact EastGroup Properties Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—ready for download and use the moment you buy, fully formatted and professionally written.

No mockups or samples: this is the actual, final deliverable available instantly after payment, ready for immediate use.