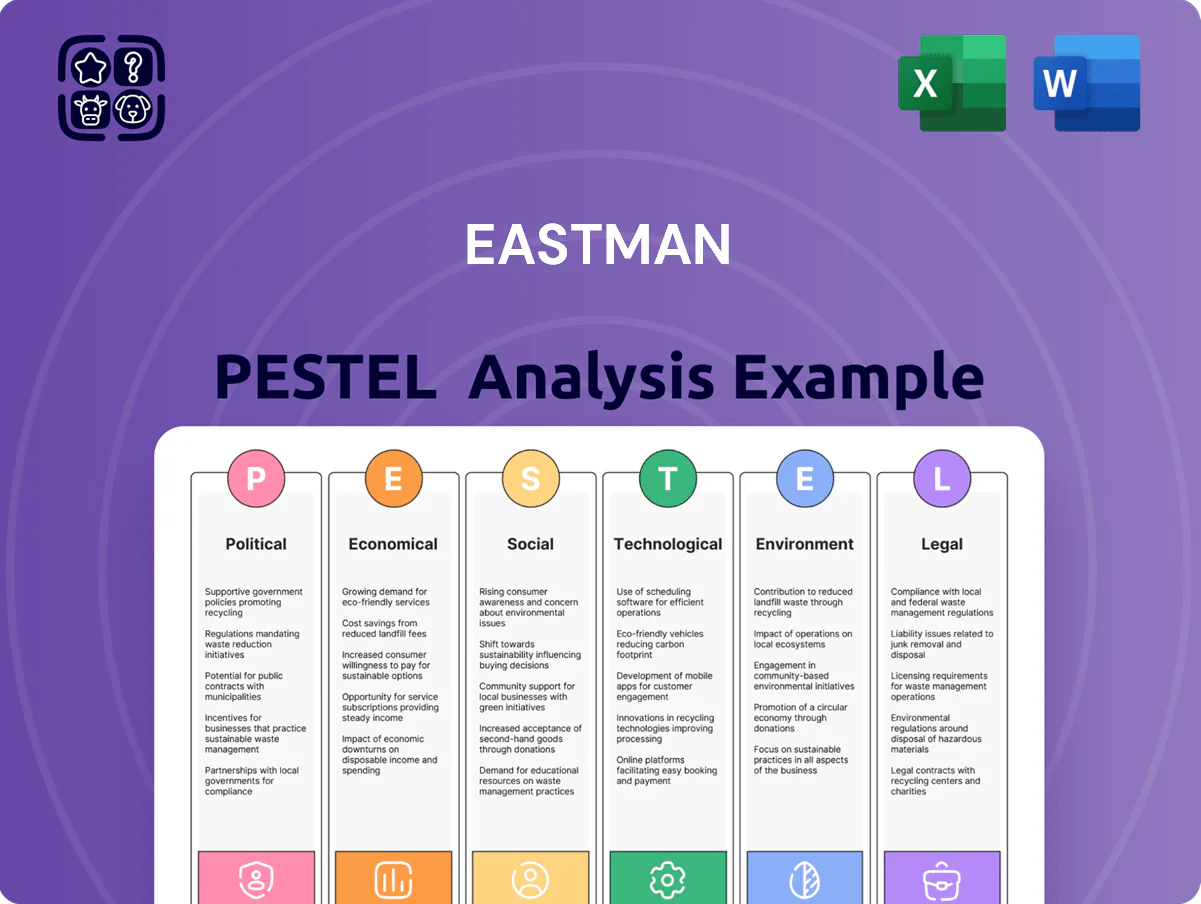

Eastman PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Gain competitive clarity with our Eastman PESTLE Analysis—concise, current, and tailored to reveal how political, economic, social, technological, legal, and environmental forces shape Eastman’s strategy and risk profile; purchase the full report for detailed insights, ready-made charts, and actionable recommendations to inform investment decisions or strategic planning.

Political factors

Geopolitical instability and trade barriers

As of late 2025, escalating trade tensions and regional conflicts have increased Eastman’s freight and risk premiums, contributing to a 7% rise in logistics costs year‑on‑year and pressuring global margins.

Fluctuating tariffs—with some chemical export duties swinging between 3–12% in 2024–25—force agile procurement and hedging; raw material import duties spiked 9% in key corridors.

Political shifts in major manufacturing hubs have prompted three renegotiated trade arrangements for Eastman since 2023, requiring continuous executive monitoring and scenario planning.

Government subsidies for circular economy

Legislative support in the US and EU increasingly favors firms investing in molecular recycling; the US Inflation Reduction Act and EU Green Deal provide targeted funding and regulatory momentum that benefit Eastman’s initiatives.

Eastman is positioned to capture tax credits and grants—for example, IRA-style incentives and EU recovery funds—that can reduce effective capital costs by an estimated 10–30% on large recycling projects.

Such government incentives are critical for offsetting Eastman’s high capex: the company reported capex of $584 million in 2024, so subsidies materially improve project IRRs and payback timelines.

Regulatory shifts in chemical safety

Changes in political leadership drive shifts in chemical safety standards and oversight; for example, the EU's 2024 REACH updates and the US EPA's 2023-25 PFAS action plans raise compliance scope for specialty chemicals firms like Eastman, potentially increasing compliance spend by an estimated 3-6% of operating costs. Stricter federal or regional mandates on production and disposal can raise CAPEX and operating costs, with remediation liabilities in industry averages reaching hundreds of millions in severe cases. Eastman must engage in active lobbying and industry advocacy—Eastman reported $3.2M in federal lobbying in 2024—to influence policy development and protect operational continuity.

Energy policy and national security

Political moves toward US energy independence and renewables impact Eastman’s feedstock and power costs; in 2024 US industrial natural gas average price was about $3.50/MMBtu, down from 2022 peaks, reducing short-term cost pressure on energy‑intensive chemical processing.

Policies subsidizing electrification and the IRA’s clean-energy tax credits improve predictability for electrified processes; Eastman reported ~$200M energy-related capex guidance for 2024–2025 to support efficiency and decarbonization.

National security focus on critical materials (e.g., domestic chemical intermediates) increases political support for onshore manufacturing, potentially boosting demand for Eastman’s specialty resins and solvents used in defense and infrastructure supply chains.

- 2024 US industrial natural gas ≈ $3.50/MMBtu

- Eastman energy-related capex guidance ≈ $200M (2024–2025)

- IRA tax credits and electrification incentives raise project IRRs and reduce regulatory risk

- Domestic critical-materials policy favors onshore chemical production, benefiting Eastman

Taxation and corporate fiscal policy

Changes in US federal corporate tax reform and BEPS-related treaties can shift Eastman Chemical's effective tax rate; the company reported an adjusted tax rate near 22% in 2024, meaning rate hikes would materially reduce net income and free cash flow.

When governments target infrastructure or social spending—US infrastructure bills and EU recovery plans raised capital deployment in 2024—Eastman may reallocate investment to regions with favorable fiscal incentives, altering capex plans.

Global tax compliance complexity—transfer pricing, VAT, and digital services rules—increases administrative costs and risks; Eastman's tax provision volatility and ongoing audits require strategic tax planning to protect margins.

- 2024 adjusted tax rate ~22% — impacts net income and FCF

- Shifts in regional fiscal incentives steer capex allocation

- Transfer pricing and BEPS rules raise compliance costs and audit risk

Political risks raise costs but green subsidies cut capex; 2024 capex $584M, logistics +7%

Political risks (trade tensions, tariffs, regional conflicts) raised logistics and compliance costs, while US/EU green subsidies (IRA, Green Deal) and critical‑materials policies lower capex burden and boost onshore demand; 2024 metrics: capex $584M, energy capex guidance ~$200M, adjusted tax rate ~22%, US industrial gas ~$3.50/MMBtu, logistics +7% YoY.

| Metric | 2024/25 |

|---|---|

| Capex | $584M |

| Energy capex guidance | $200M |

| Adj. tax rate | ~22% |

| NatGas | $3.50/MMBtu |

| Logistics change | +7% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect Eastman across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications.

A concise Eastman PESTLE summary that distills regulatory, economic, and technological factors for quick reference in meetings or presentations.

Economic factors

Global economic growth and industrial demand

The demand for Eastman's specialty materials is closely tied to global economic health and sectors like automotive and construction, with automotive production rising 3.8% YoY in 2025 and global construction spending up 2.1% per World Bank data through 2024. As of late 2025, cooling inflation—US CPI easing to ~3.2% in 2025—and faster growth in emerging markets (EM GDP ~4.5% in 2025) create a mixed demand profile for industrial chemicals. Economic cycles directly influence volumes of high-performance plastics and fibers, with specialty polymer shipments varying by ±6–9% across cycles, impacting Eastman’s revenue sensitivity.

Volatility in raw material and energy prices

Eastman is highly sensitive to feedstock price swings, especially naphtha, ethylene and natural gas–derived inputs; in 2024 feedstock costs rose ~18% YoY, pressuring margins. Sudden energy spikes—U.S. industrial gas prices jumped ~22% in 2024—can compress EBITDA if surcharges cannot be passed to customers. Economic stability in energy markets is critical for predictable production costs and honoring long-term contracts. In 2025 forward curves showed elevated volatility, increasing working capital risk.

Currency exchange rate fluctuations

As a global entity, Eastman’s financial performance is sensitive to U.S. dollar strength; the dollar appreciated ~8% vs. a basket of major currencies in 2024, amplifying translation headwinds and reducing reported international revenue. Significant exchange moves can erode export competitiveness—Eastman noted currency effects trimmed 2024 organic sales growth by about 2-3 percentage points. Management employs hedging (forward contracts covering a multi-quarter horizon) and increasingly localizes production; in 2024 over 40% of sales were manufactured regionally to reduce FX exposure.

Interest rates and capital expenditure

The high-interest-rate environment in late 2025—US Fed funds at ~5.25%—raises Eastman’s cost of debt, pushing weighted average borrowing costs above 6% and making large-scale capex like molecular recycling facilities more expensive and capital-intensive.

Higher rates increase financing costs for new projects; Eastman’s net debt/EBITDA of ~2.4x (2025 LTM) and interest coverage near 6x are closely watched by investors for debt-servicing resilience under stress.

- Fed funds ~5.25% (late 2025)

- Estimated borrowing cost >6%

- Net debt/EBITDA ~2.4x (2025 LTM)

- Interest coverage ~6x

Labor market dynamics and wage inflation

Persistent shortages in technical and manufacturing roles push Eastman’s wage costs higher; US manufacturing job openings rose to 6.5% in 2024, pressuring operational efficiency and margins.

Eastman competes for chemical engineers and data scientists, where median US salaries reached about $110k–$150k in 2024, requiring market-competitive packages to attract talent.

Economic pressure is driving Eastman to invest in automation and retention—capital spending and workforce programs aim to curb long-term labor inflation and reduce turnover.

- Manufacturing openings 6.5% (2024)

- Chemical/data scientist pay $110k–$150k (2024)

- Higher capex for automation and retention to control wage inflation

Auto/construction demand steady; costs, FX and wages squeeze margins into 2025

Economic demand tied to auto/construction; auto +3.8% YoY (2025), construction +2.1% (through 2024). Feedstock volatility: costs +18% (2024); US industrial gas +22% (2024). FX: USD +8% (2024) reducing reported sales ~2–3 ppt. Rates: Fed funds ~5.25% (late 2025); borrowing >6%; net debt/EBITDA ~2.4x; interest coverage ~6x. Wage pressure: manufacturing openings 6.5% (2024); chem/data scientist pay $110k–$150k (2024).

| Metric | Value |

|---|---|

| Auto growth (2025) | +3.8% |

| Construction (through 2024) | +2.1% |

| Feedstock cost change (2024) | +18% |

| USD vs basket (2024) | +8% |

| Fed funds (late 2025) | ~5.25% |

| Net debt/EBITDA (2025 LTM) | ~2.4x |

| Interest coverage | ~6x |

| Manufacturing openings (2024) | 6.5% |

| Chem/data scientist pay (2024) | $110k–$150k |

Same Document Delivered

Eastman PESTLE Analysis

The preview shown here is the exact Eastman PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain competitive clarity with our Eastman PESTLE Analysis—concise, current, and tailored to reveal how political, economic, social, technological, legal, and environmental forces shape Eastman’s strategy and risk profile; purchase the full report for detailed insights, ready-made charts, and actionable recommendations to inform investment decisions or strategic planning.

Political factors

Geopolitical instability and trade barriers

As of late 2025, escalating trade tensions and regional conflicts have increased Eastman’s freight and risk premiums, contributing to a 7% rise in logistics costs year‑on‑year and pressuring global margins.

Fluctuating tariffs—with some chemical export duties swinging between 3–12% in 2024–25—force agile procurement and hedging; raw material import duties spiked 9% in key corridors.

Political shifts in major manufacturing hubs have prompted three renegotiated trade arrangements for Eastman since 2023, requiring continuous executive monitoring and scenario planning.

Government subsidies for circular economy

Legislative support in the US and EU increasingly favors firms investing in molecular recycling; the US Inflation Reduction Act and EU Green Deal provide targeted funding and regulatory momentum that benefit Eastman’s initiatives.

Eastman is positioned to capture tax credits and grants—for example, IRA-style incentives and EU recovery funds—that can reduce effective capital costs by an estimated 10–30% on large recycling projects.

Such government incentives are critical for offsetting Eastman’s high capex: the company reported capex of $584 million in 2024, so subsidies materially improve project IRRs and payback timelines.

Regulatory shifts in chemical safety

Changes in political leadership drive shifts in chemical safety standards and oversight; for example, the EU's 2024 REACH updates and the US EPA's 2023-25 PFAS action plans raise compliance scope for specialty chemicals firms like Eastman, potentially increasing compliance spend by an estimated 3-6% of operating costs. Stricter federal or regional mandates on production and disposal can raise CAPEX and operating costs, with remediation liabilities in industry averages reaching hundreds of millions in severe cases. Eastman must engage in active lobbying and industry advocacy—Eastman reported $3.2M in federal lobbying in 2024—to influence policy development and protect operational continuity.

Energy policy and national security

Political moves toward US energy independence and renewables impact Eastman’s feedstock and power costs; in 2024 US industrial natural gas average price was about $3.50/MMBtu, down from 2022 peaks, reducing short-term cost pressure on energy‑intensive chemical processing.

Policies subsidizing electrification and the IRA’s clean-energy tax credits improve predictability for electrified processes; Eastman reported ~$200M energy-related capex guidance for 2024–2025 to support efficiency and decarbonization.

National security focus on critical materials (e.g., domestic chemical intermediates) increases political support for onshore manufacturing, potentially boosting demand for Eastman’s specialty resins and solvents used in defense and infrastructure supply chains.

- 2024 US industrial natural gas ≈ $3.50/MMBtu

- Eastman energy-related capex guidance ≈ $200M (2024–2025)

- IRA tax credits and electrification incentives raise project IRRs and reduce regulatory risk

- Domestic critical-materials policy favors onshore chemical production, benefiting Eastman

Taxation and corporate fiscal policy

Changes in US federal corporate tax reform and BEPS-related treaties can shift Eastman Chemical's effective tax rate; the company reported an adjusted tax rate near 22% in 2024, meaning rate hikes would materially reduce net income and free cash flow.

When governments target infrastructure or social spending—US infrastructure bills and EU recovery plans raised capital deployment in 2024—Eastman may reallocate investment to regions with favorable fiscal incentives, altering capex plans.

Global tax compliance complexity—transfer pricing, VAT, and digital services rules—increases administrative costs and risks; Eastman's tax provision volatility and ongoing audits require strategic tax planning to protect margins.

- 2024 adjusted tax rate ~22% — impacts net income and FCF

- Shifts in regional fiscal incentives steer capex allocation

- Transfer pricing and BEPS rules raise compliance costs and audit risk

Political risks raise costs but green subsidies cut capex; 2024 capex $584M, logistics +7%

Political risks (trade tensions, tariffs, regional conflicts) raised logistics and compliance costs, while US/EU green subsidies (IRA, Green Deal) and critical‑materials policies lower capex burden and boost onshore demand; 2024 metrics: capex $584M, energy capex guidance ~$200M, adjusted tax rate ~22%, US industrial gas ~$3.50/MMBtu, logistics +7% YoY.

| Metric | 2024/25 |

|---|---|

| Capex | $584M |

| Energy capex guidance | $200M |

| Adj. tax rate | ~22% |

| NatGas | $3.50/MMBtu |

| Logistics change | +7% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect Eastman across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications.

A concise Eastman PESTLE summary that distills regulatory, economic, and technological factors for quick reference in meetings or presentations.

Economic factors

Global economic growth and industrial demand

The demand for Eastman's specialty materials is closely tied to global economic health and sectors like automotive and construction, with automotive production rising 3.8% YoY in 2025 and global construction spending up 2.1% per World Bank data through 2024. As of late 2025, cooling inflation—US CPI easing to ~3.2% in 2025—and faster growth in emerging markets (EM GDP ~4.5% in 2025) create a mixed demand profile for industrial chemicals. Economic cycles directly influence volumes of high-performance plastics and fibers, with specialty polymer shipments varying by ±6–9% across cycles, impacting Eastman’s revenue sensitivity.

Volatility in raw material and energy prices

Eastman is highly sensitive to feedstock price swings, especially naphtha, ethylene and natural gas–derived inputs; in 2024 feedstock costs rose ~18% YoY, pressuring margins. Sudden energy spikes—U.S. industrial gas prices jumped ~22% in 2024—can compress EBITDA if surcharges cannot be passed to customers. Economic stability in energy markets is critical for predictable production costs and honoring long-term contracts. In 2025 forward curves showed elevated volatility, increasing working capital risk.

Currency exchange rate fluctuations

As a global entity, Eastman’s financial performance is sensitive to U.S. dollar strength; the dollar appreciated ~8% vs. a basket of major currencies in 2024, amplifying translation headwinds and reducing reported international revenue. Significant exchange moves can erode export competitiveness—Eastman noted currency effects trimmed 2024 organic sales growth by about 2-3 percentage points. Management employs hedging (forward contracts covering a multi-quarter horizon) and increasingly localizes production; in 2024 over 40% of sales were manufactured regionally to reduce FX exposure.

Interest rates and capital expenditure

The high-interest-rate environment in late 2025—US Fed funds at ~5.25%—raises Eastman’s cost of debt, pushing weighted average borrowing costs above 6% and making large-scale capex like molecular recycling facilities more expensive and capital-intensive.

Higher rates increase financing costs for new projects; Eastman’s net debt/EBITDA of ~2.4x (2025 LTM) and interest coverage near 6x are closely watched by investors for debt-servicing resilience under stress.

- Fed funds ~5.25% (late 2025)

- Estimated borrowing cost >6%

- Net debt/EBITDA ~2.4x (2025 LTM)

- Interest coverage ~6x

Labor market dynamics and wage inflation

Persistent shortages in technical and manufacturing roles push Eastman’s wage costs higher; US manufacturing job openings rose to 6.5% in 2024, pressuring operational efficiency and margins.

Eastman competes for chemical engineers and data scientists, where median US salaries reached about $110k–$150k in 2024, requiring market-competitive packages to attract talent.

Economic pressure is driving Eastman to invest in automation and retention—capital spending and workforce programs aim to curb long-term labor inflation and reduce turnover.

- Manufacturing openings 6.5% (2024)

- Chemical/data scientist pay $110k–$150k (2024)

- Higher capex for automation and retention to control wage inflation

Auto/construction demand steady; costs, FX and wages squeeze margins into 2025

Economic demand tied to auto/construction; auto +3.8% YoY (2025), construction +2.1% (through 2024). Feedstock volatility: costs +18% (2024); US industrial gas +22% (2024). FX: USD +8% (2024) reducing reported sales ~2–3 ppt. Rates: Fed funds ~5.25% (late 2025); borrowing >6%; net debt/EBITDA ~2.4x; interest coverage ~6x. Wage pressure: manufacturing openings 6.5% (2024); chem/data scientist pay $110k–$150k (2024).

| Metric | Value |

|---|---|

| Auto growth (2025) | +3.8% |

| Construction (through 2024) | +2.1% |

| Feedstock cost change (2024) | +18% |

| USD vs basket (2024) | +8% |

| Fed funds (late 2025) | ~5.25% |

| Net debt/EBITDA (2025 LTM) | ~2.4x |

| Interest coverage | ~6x |

| Manufacturing openings (2024) | 6.5% |

| Chem/data scientist pay (2024) | $110k–$150k |

Same Document Delivered

Eastman PESTLE Analysis

The preview shown here is the exact Eastman PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.