East West Bancorp PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unpack how political shifts, economic cycles, and technological disruption are reshaping East West Bancorp’s competitive edge—our concise PESTLE highlights key external risks and opportunities to inform investment and strategy decisions; purchase the full analysis for the complete, actionable roadmap.

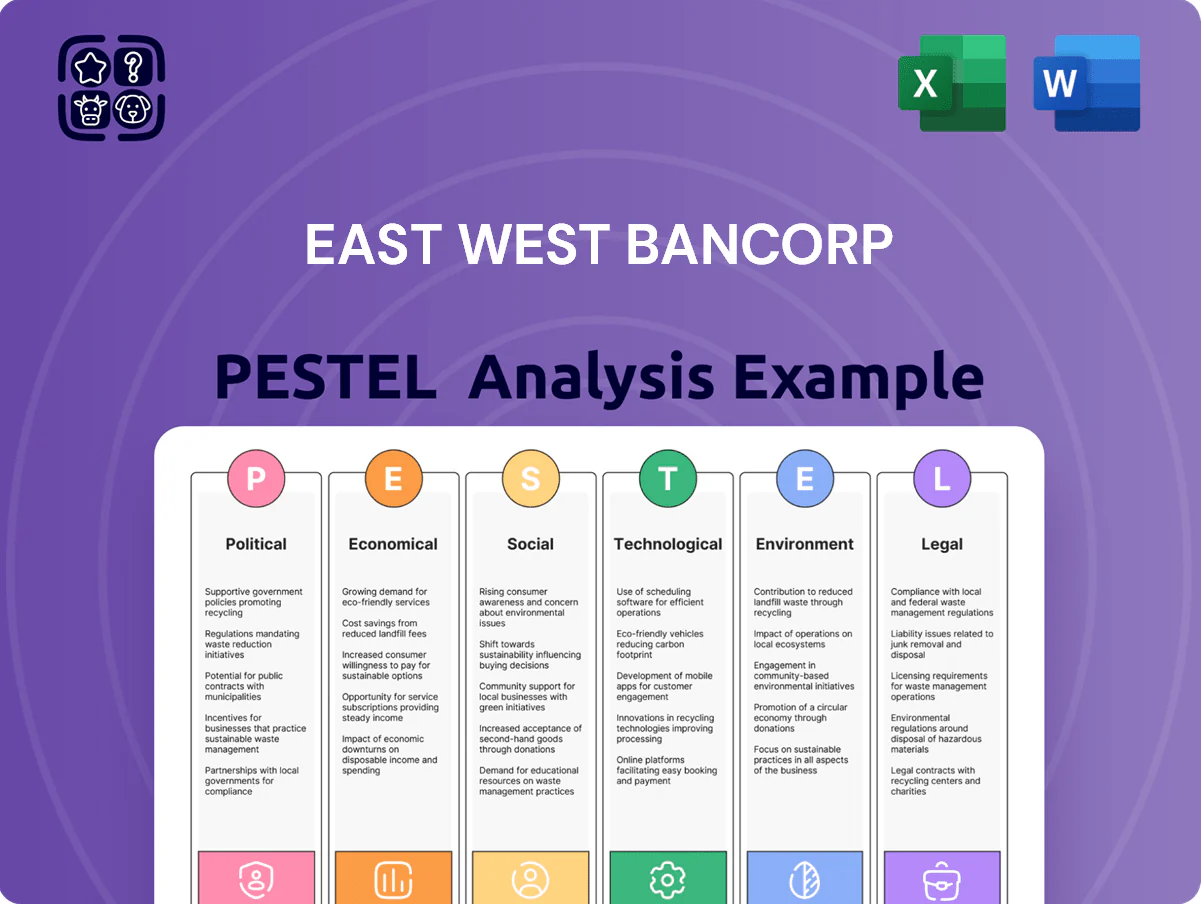

Political factors

U.S. and China Geopolitical Relations

The ongoing U.S.-China tensions materially affect East West Bancorp, given its focus on cross-border trade: in 2024 trade finance revenue exposed to China-related flows represented an estimated 22% of its international segment. Sudden diplomatic shifts have in past years triggered capital flow controls and altered demand for letters of credit, reducing transaction volumes by up to 15% quarter-over-quarter in stress periods. The bank must manage regulatory uncertainty as political rhetoric often tightens cross-border payment processing and correspondent relationships, influencing net interest income and fee generation.

Trade Policy and Tariffs

Changes in trade agreements or new tariffs directly affect East West Bancorp’s commercial clients in import/export: in 2024 US-China tariffs and supply-chain reshoring raised trade compliance costs by an estimated 8-12%, pressuring transaction volumes for the bank’s Pacific Rim portfolio.

As a primary facilitator of Pacific Rim trade, East West is sensitive to protectionist policies that could reduce fee income; cross-border wire volumes fell about 6% YoY in 2023 in comparable regional corridors.

Strategic planning requires real-time monitoring of legislative shifts—Congress and major trade partners introduced 15+ tariff or subsidy changes in 2022–2024—that can materially alter profitability across manufacturing and logistics sectors linked to the bank’s loan book.

Regulatory Scrutiny on Foreign Investment

Heightened national-security scrutiny has driven a 40% rise in CFIUS filings since 2018, constraining Chinese FDI into US banks and real estate and reducing cross-border deal flow; for East West Bancorp this pressures advisory fees and syndicated lending tied to inbound deals—cross-border loan exposure represented about 12% of commercial real-estate-related assets in 2024—so adhering to evolving CFIUS rules is critical to avoid transaction blocks and preserve operational stability.

U.S. Domestic Banking Policy

As of late 2025, shifts in U.S. banking policy—debates over higher capital requirements and enhanced oversight for regional banks—are shaping East West Bancorp’s growth strategy, with potential impacts on loan-to-deposit ratios and return on equity targets.

Legislative discussions on defining systemic importance could raise compliance costs by an estimated 5–15% for affected regional banks, constraining lending capacity and capital allocation.

East West must align lobbying and risk management in Washington D.C.; 2024–2025 regulatory filings show industry engagement increased 22% as banks prepared for possible rule changes.

- Potential 5–15% uptick in compliance costs

- 22% rise in industry regulatory engagement (2024–2025)

- Impacts on loan-to-deposit and ROE planning

Taxation Policies

Corporate tax rates and shifts in international tax treaties can materially affect East West Bancorp’s net income; a 1 percentage-point rise in statutory rates could lower after-tax ROE by several hundred basis points given the bank’s $1.9B pre-tax income in FY2024.

Revisions to cross-border taxation influence the bank’s structure and product design for multinational clients, notably impacting foreign deposit flows and fee income tied to Asia-US corridors where 60% of revenue is region-linked.

Analysts track legislative trends to model long-term net income and capital allocation; stress tests now incorporate scenario reductions in after-tax earnings of 5–10% over three years based on recent OECD BEPS updates and US tax proposals.

- 1 pp corporate tax rise could cut ROE by several hundred bps (based on $1.9B FY2024 pre-tax income)

- 60% of revenue linked to Asia-US corridors—sensitive to cross-border tax rules

- Stress-test scenarios model 5–10% after-tax earnings decline over three years

US–China political risk hits East West Bancorp: 60% Asia revenue, compliance +5–15%

Political risks—US-China tensions, tariffs, CFIUS scrutiny, and potential higher bank capital/regulatory burdens—directly pressure East West Bancorp’s cross-border trade revenue, compliance costs, loan-to-deposit management, and ROE; 2024–2025 data: ~22% international trade exposure to China flows, 12% cross-border CRE loan exposure, 60% revenue linked to Asia-US corridors, 22% rise in regulatory engagement, and estimated 5–15% compliance cost uptick.

| Metric | Value (2024–25) |

|---|---|

| China-related trade revenue share | 22% |

| Cross-border CRE loan exposure | 12% |

| Revenue linked to Asia-US corridors | 60% |

| Regulatory engagement change | +22% |

| Estimated compliance cost rise | 5–15% |

What is included in the product

Explores how macro-environmental factors uniquely affect East West Bancorp across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications tailored for executives, investors, and strategists.

A concise, PESTLE-segmented summary of East West Bancorp that’s presentation-ready, easily shareable, and editable for team notes—ideal for quick alignment, client reports, and on-the-go strategic discussions.

Economic factors

Interest Rate Environment

By end-2025 the Federal Reserve signaled a gradual easing with fed funds projected around 4.25%–4.75%, directly shaping East West Bancorp’s net interest margin and profitability; a 25–50 bps cut scenario could compress short-term funding spreads. Changes in rates alter deposit costs and loan yields, notably stressing commercial real estate lending where average loan yields were ~5.2% in 2024. Management must manage a loan-to-deposit ratio near 80% to stay resilient against rate volatility and potential economic slowdown.

Currency Exchange Rate Volatility

Given East West Bancorp’s focus on U.S.-China trade, fluctuations in the USD-CNY rate—which moved from about 6.30 to 7.30 between 2021–2023 and traded near 7.10 in 2024—directly affect client purchasing power and cross-border asset valuations.

Volatility increases credit and market risk: a 10% CNY depreciation can materially reduce repatriated revenues for importers and lower collateral values on China-linked loans.

The bank offers FX forwards, swaps and options to hedge exposure, but extreme moves—like rapid 5–10% swings—can still dampen trade volumes and lower fee income derived from transaction banking.

Economic Growth in Greater China

China’s 2024 GDP growth slowed to about 4.5% YoY and industrial output rose 3.8% through Q3 2024, weighing on cross-border trade volumes that drive East West Bancorp’s trade finance and commercial lending exposure.

Weaker import demand and supply-chain softness can reduce fee income from trade services and wealth flows from Chinese clients, while a rebound—GDP growth above 5% and manufacturing PMI expansion—would boost loan origination and wealth-management inflows in East West’s niche market.

U.S. Real Estate Market Conditions

A significant portion of East West Bancorp’s loan book is concentrated in commercial and residential real estate across major U.S. metros, exposing credit quality to shifts in vacancy rates, valuations, and construction costs.

By late 2025 the bank monitors urban recoveries and remote-work reductions in office demand; U.S. office vacancy averaged ~17% nationally in 2024, while national home prices rose ~3% year-over-year through 2024.

Rising construction costs (+6–8% in 2024) and localized valuation corrections can tighten LTVs and increase charge-off risk.

- Office vacancy ~17% (2024)

- Home prices +3% YoY (2024)

- Construction costs +6–8% (2024)

Inflation and Labor Costs

- US CPI 3.4% (2025); sector wage growth ~5–7% (2024–25)

- East West 2024 efficiency ratio 56%—margin sensitivity

- Tech investments target OPEX growth < wage inflation

Rising rates, tight CRE and China FX drag bank margins amid inflation and wage pressure

Economic pressures—Fed funds ~4.25–4.75% (end-2025), US CPI 3.4% (2025), wage growth 5–7% (2024–25)—drive NIM and costs; CRE exposure (office vacancy ~17%, home prices +3% YoY, construction costs +6–8% in 2024) raises credit risk; China growth ~4.5% (2024) and USD/CNY ~7.10 (2024) affect trade fees and FX income.

| Metric | Value |

|---|---|

| Fed funds | 4.25–4.75% |

| US CPI (2025) | 3.4% |

| Office vacancy (2024) | ~17% |

| USD/CNY (2024) | ~7.10 |

Preview Before You Purchase

East West Bancorp PESTLE Analysis

The preview shown here is the exact East West Bancorp PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

No placeholders, no teasers—this is the real, professionally structured file you’ll own upon checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unpack how political shifts, economic cycles, and technological disruption are reshaping East West Bancorp’s competitive edge—our concise PESTLE highlights key external risks and opportunities to inform investment and strategy decisions; purchase the full analysis for the complete, actionable roadmap.

Political factors

U.S. and China Geopolitical Relations

The ongoing U.S.-China tensions materially affect East West Bancorp, given its focus on cross-border trade: in 2024 trade finance revenue exposed to China-related flows represented an estimated 22% of its international segment. Sudden diplomatic shifts have in past years triggered capital flow controls and altered demand for letters of credit, reducing transaction volumes by up to 15% quarter-over-quarter in stress periods. The bank must manage regulatory uncertainty as political rhetoric often tightens cross-border payment processing and correspondent relationships, influencing net interest income and fee generation.

Trade Policy and Tariffs

Changes in trade agreements or new tariffs directly affect East West Bancorp’s commercial clients in import/export: in 2024 US-China tariffs and supply-chain reshoring raised trade compliance costs by an estimated 8-12%, pressuring transaction volumes for the bank’s Pacific Rim portfolio.

As a primary facilitator of Pacific Rim trade, East West is sensitive to protectionist policies that could reduce fee income; cross-border wire volumes fell about 6% YoY in 2023 in comparable regional corridors.

Strategic planning requires real-time monitoring of legislative shifts—Congress and major trade partners introduced 15+ tariff or subsidy changes in 2022–2024—that can materially alter profitability across manufacturing and logistics sectors linked to the bank’s loan book.

Regulatory Scrutiny on Foreign Investment

Heightened national-security scrutiny has driven a 40% rise in CFIUS filings since 2018, constraining Chinese FDI into US banks and real estate and reducing cross-border deal flow; for East West Bancorp this pressures advisory fees and syndicated lending tied to inbound deals—cross-border loan exposure represented about 12% of commercial real-estate-related assets in 2024—so adhering to evolving CFIUS rules is critical to avoid transaction blocks and preserve operational stability.

U.S. Domestic Banking Policy

As of late 2025, shifts in U.S. banking policy—debates over higher capital requirements and enhanced oversight for regional banks—are shaping East West Bancorp’s growth strategy, with potential impacts on loan-to-deposit ratios and return on equity targets.

Legislative discussions on defining systemic importance could raise compliance costs by an estimated 5–15% for affected regional banks, constraining lending capacity and capital allocation.

East West must align lobbying and risk management in Washington D.C.; 2024–2025 regulatory filings show industry engagement increased 22% as banks prepared for possible rule changes.

- Potential 5–15% uptick in compliance costs

- 22% rise in industry regulatory engagement (2024–2025)

- Impacts on loan-to-deposit and ROE planning

Taxation Policies

Corporate tax rates and shifts in international tax treaties can materially affect East West Bancorp’s net income; a 1 percentage-point rise in statutory rates could lower after-tax ROE by several hundred basis points given the bank’s $1.9B pre-tax income in FY2024.

Revisions to cross-border taxation influence the bank’s structure and product design for multinational clients, notably impacting foreign deposit flows and fee income tied to Asia-US corridors where 60% of revenue is region-linked.

Analysts track legislative trends to model long-term net income and capital allocation; stress tests now incorporate scenario reductions in after-tax earnings of 5–10% over three years based on recent OECD BEPS updates and US tax proposals.

- 1 pp corporate tax rise could cut ROE by several hundred bps (based on $1.9B FY2024 pre-tax income)

- 60% of revenue linked to Asia-US corridors—sensitive to cross-border tax rules

- Stress-test scenarios model 5–10% after-tax earnings decline over three years

US–China political risk hits East West Bancorp: 60% Asia revenue, compliance +5–15%

Political risks—US-China tensions, tariffs, CFIUS scrutiny, and potential higher bank capital/regulatory burdens—directly pressure East West Bancorp’s cross-border trade revenue, compliance costs, loan-to-deposit management, and ROE; 2024–2025 data: ~22% international trade exposure to China flows, 12% cross-border CRE loan exposure, 60% revenue linked to Asia-US corridors, 22% rise in regulatory engagement, and estimated 5–15% compliance cost uptick.

| Metric | Value (2024–25) |

|---|---|

| China-related trade revenue share | 22% |

| Cross-border CRE loan exposure | 12% |

| Revenue linked to Asia-US corridors | 60% |

| Regulatory engagement change | +22% |

| Estimated compliance cost rise | 5–15% |

What is included in the product

Explores how macro-environmental factors uniquely affect East West Bancorp across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking implications tailored for executives, investors, and strategists.

A concise, PESTLE-segmented summary of East West Bancorp that’s presentation-ready, easily shareable, and editable for team notes—ideal for quick alignment, client reports, and on-the-go strategic discussions.

Economic factors

Interest Rate Environment

By end-2025 the Federal Reserve signaled a gradual easing with fed funds projected around 4.25%–4.75%, directly shaping East West Bancorp’s net interest margin and profitability; a 25–50 bps cut scenario could compress short-term funding spreads. Changes in rates alter deposit costs and loan yields, notably stressing commercial real estate lending where average loan yields were ~5.2% in 2024. Management must manage a loan-to-deposit ratio near 80% to stay resilient against rate volatility and potential economic slowdown.

Currency Exchange Rate Volatility

Given East West Bancorp’s focus on U.S.-China trade, fluctuations in the USD-CNY rate—which moved from about 6.30 to 7.30 between 2021–2023 and traded near 7.10 in 2024—directly affect client purchasing power and cross-border asset valuations.

Volatility increases credit and market risk: a 10% CNY depreciation can materially reduce repatriated revenues for importers and lower collateral values on China-linked loans.

The bank offers FX forwards, swaps and options to hedge exposure, but extreme moves—like rapid 5–10% swings—can still dampen trade volumes and lower fee income derived from transaction banking.

Economic Growth in Greater China

China’s 2024 GDP growth slowed to about 4.5% YoY and industrial output rose 3.8% through Q3 2024, weighing on cross-border trade volumes that drive East West Bancorp’s trade finance and commercial lending exposure.

Weaker import demand and supply-chain softness can reduce fee income from trade services and wealth flows from Chinese clients, while a rebound—GDP growth above 5% and manufacturing PMI expansion—would boost loan origination and wealth-management inflows in East West’s niche market.

U.S. Real Estate Market Conditions

A significant portion of East West Bancorp’s loan book is concentrated in commercial and residential real estate across major U.S. metros, exposing credit quality to shifts in vacancy rates, valuations, and construction costs.

By late 2025 the bank monitors urban recoveries and remote-work reductions in office demand; U.S. office vacancy averaged ~17% nationally in 2024, while national home prices rose ~3% year-over-year through 2024.

Rising construction costs (+6–8% in 2024) and localized valuation corrections can tighten LTVs and increase charge-off risk.

- Office vacancy ~17% (2024)

- Home prices +3% YoY (2024)

- Construction costs +6–8% (2024)

Inflation and Labor Costs

- US CPI 3.4% (2025); sector wage growth ~5–7% (2024–25)

- East West 2024 efficiency ratio 56%—margin sensitivity

- Tech investments target OPEX growth < wage inflation

Rising rates, tight CRE and China FX drag bank margins amid inflation and wage pressure

Economic pressures—Fed funds ~4.25–4.75% (end-2025), US CPI 3.4% (2025), wage growth 5–7% (2024–25)—drive NIM and costs; CRE exposure (office vacancy ~17%, home prices +3% YoY, construction costs +6–8% in 2024) raises credit risk; China growth ~4.5% (2024) and USD/CNY ~7.10 (2024) affect trade fees and FX income.

| Metric | Value |

|---|---|

| Fed funds | 4.25–4.75% |

| US CPI (2025) | 3.4% |

| Office vacancy (2024) | ~17% |

| USD/CNY (2024) | ~7.10 |

Preview Before You Purchase

East West Bancorp PESTLE Analysis

The preview shown here is the exact East West Bancorp PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

No placeholders, no teasers—this is the real, professionally structured file you’ll own upon checkout.