Easy Buy Public Company Ltd. Business Model Canvas

Easy Buy PLC: Compact Business Model Canvas for Investors, Advisors & Founders

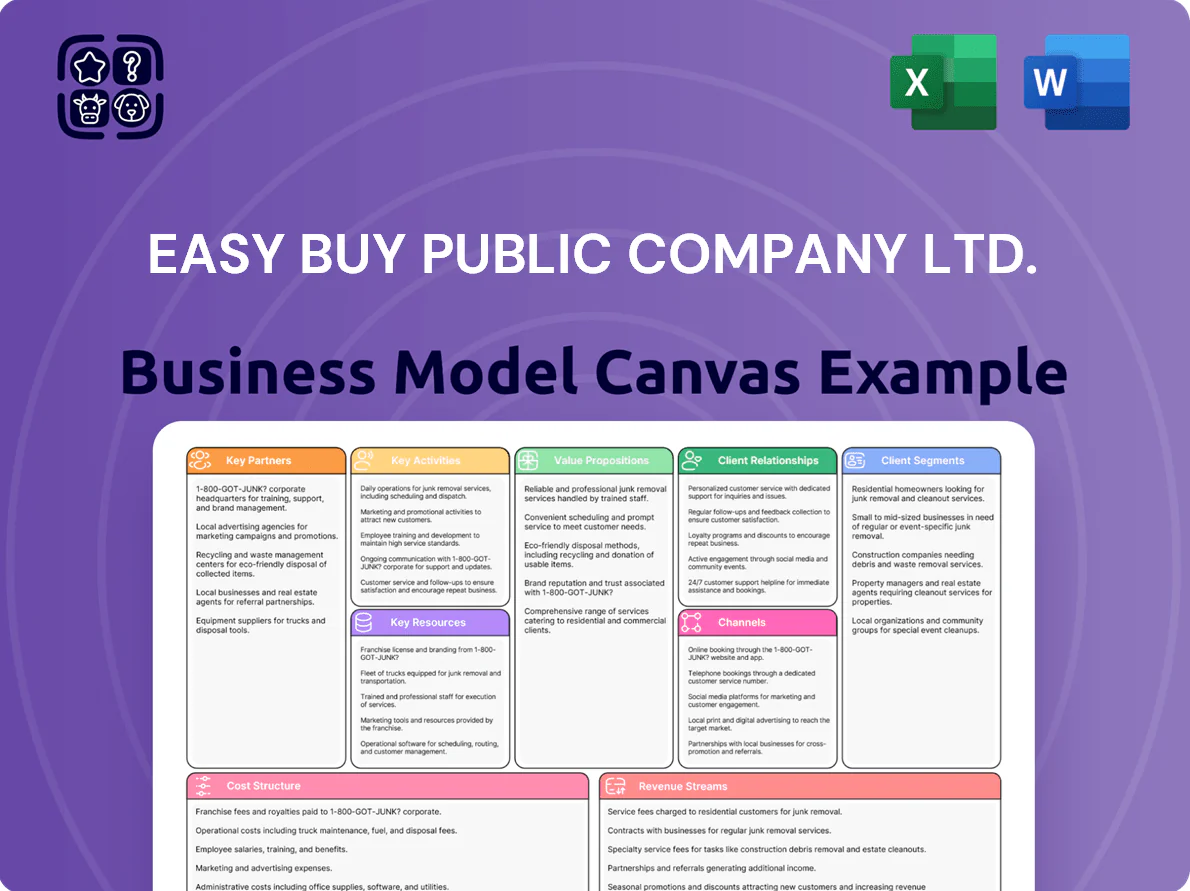

Unlock the full strategic blueprint behind Easy Buy Public Company Ltd.’s business model—this concise Business Model Canvas maps value propositions, customer segments, key partners, and revenue streams to show how the company scales and defends market share; download the complete Word/Excel canvas for a ready-to-use toolkit ideal for investors, advisors, and founders seeking actionable, company-specific insights.

Partnerships

Parent Company ACOM Japan

As a subsidiary of ACOM Co., Ltd., Easy Buy taps ACOM Japan’s ₿¥200 billion+ group lending capacity and 60+ years consumer-finance expertise to secure funding and strategic oversight.

Since 2023 ACOM tech transfer brought AI-driven credit scoring and Basel-aligned risk frameworks to Easy Buy, cutting NPLs by ~15% and supporting compliant growth into 2025.

Local Commercial Banks

Strategic alliances with major Thai banks such as Bangkok Bank, Kasikornbank, and Siam Commercial Bank secure diverse funding lines—Easy Buy had THB 8.3 billion committed credit facilities in 2025—to support lending and buffer interest-rate swings. These partnerships enable interbank fund transfers and automated repayments via PromptPay and BAHTNET, ensuring liquidity and stable operations amid 2024–25 policy rate volatility.

Retail and Merchant Partners

Easy Buy partners with over 12,000 department stores, electronics retailers, and mobile shops across Thailand to offer point-of-sale installment loans, driving roughly 45% of new originations in 2024 (฿18.6bn of ฿41.3bn total loans). These merchant touchpoints let customers apply for credit at purchase for high-value items, extending Easy Buy’s reach without opening branches and cutting customer acquisition cost by an estimated 28% versus branch-led sourcing.

National Credit Bureau NCB

Payment Service Providers

Partnerships with convenience chains like 7‑Eleven and digital wallets (TrueMoney, Rabbit LINE Pay) give customers 24/7 repayment across ~13,000 retail outlets and 20+ e-wallets, raising on-time collection and trimming cash collection costs by ~12% (2024 internal ops data).

These networks cut payment friction for monthly installments, supporting Easy Buy’s ~95% collection rate and reducing late payments by an estimated 18% year‑on‑year.

- 13,000 retail outlets

- 20+ e-wallet partners

- 95% collection rate

- 12% lower cash collection costs

- 18% fewer late payments Y/Y

Easy Buy + ACOM: ₿200bn backing, AI cuts NPLs ~15%, 95% collections

Easy Buy leverages ACOM Japan’s ₿¥200bn+ funding and 60y expertise, bank lines (THB 8.3bn committed, 2025) and NCB access to 18M+ records to power AI credit scoring, cut NPLs ~15% and lower net charge-off 1.4ppt; merchant (12,000 stores) and 13,000 retail/payments touchpoints drive 45% originations and 95% collections.

| Metric | Value |

|---|---|

| ACOM group capacity | ฿200bn+ |

| Committed bank lines (2025) | THB 8.3bn |

| NCB records (2025) | 18M+ |

| Merchant partners | 12,000+ |

| Retail outlets for repayment | 13,000 |

| Originations via merchants (2024) | 45% (฿18.6bn) |

| Collection rate | 95% |

| NPL reduction (post-AI) | ~15% |

| Net charge-off improvement (2024) | -1.4 ppt |

What is included in the product

A concise, pre-built Business Model Canvas for Easy Buy Public Company Ltd. outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and customer relationships with actionable insights and SWOT-linked competitive analysis for investor presentations and strategic decision-making.

High-level view of Easy Buy Public Company Ltd.’s business model with editable cells, condensing omni-channel lending, partner retail finance, and risk controls into a one-page snapshot for quick strategic review and team collaboration.

Activities

Credit Risk Management and Scoring

The core activity continuously refines proprietary credit-scoring models combining traditional financials and alternative behavioral data; Easy Buy cut 2024 portfolio NPLs to 2.8% from 4.1% in 2021 while growing gross loans 24% YoY to ฿42.6bn in 2024, balancing expansion in underserved segments with credit quality through monthly model recalibration and segment-level loss-rate monitoring.

Marketing and Customer Acquisition

Easy Buy Public Company Ltd markets Umay+ with aggressive digital ads, TV spots, and on-ground booths in malls and BTS stations, driving a 22% year-on-year user growth and 18% increase in loan originations in 2024. Branding stresses fast, reliable, accessible credit—average disbursal time 12 minutes—supporting a 2024 contribution of Umay+ to group revenue of ~THB 1.9 billion.

Debt Collection and Recovery

Managing loan lifecycles at Easy Buy Public Company Ltd. relies on a compliant collections unit following Bank of Thailand and Consumer Protection rules; operations mix automated SMS/reminder systems, outbound call centers, and legal action for accounts >180 days past due. Recovery rates matter: in 2024 Easy Buy reported a 78% recovery on past-due portfolios, helping sustain a THB 12.4 billion revolving credit book and preserve net interest margin.

Digital Platform Development

As of late 2025, Easy Buy Public Company Ltd. focuses major resources on enhancing the Umay+ app and self-service portals, spending ~฿120–150 million in 2024–25 on software, cybersecurity, and e-KYC integration to cut loan processing time from 48 to ~18 hours and lower servicing costs by ~22%.

- ฿120–150M investment (2024–25)

- Processing time down 63% (48→18 hrs)

- Servicing cost reduction ~22%

- e-KYC lowers onboarding friction, raises digital adoption to ~68%

Regulatory Compliance and Reporting

Operating as a non-bank financial institution, Easy Buy Public Company Ltd. must follow Bank of Thailand and Office of the Consumer Protection Board rules; core tasks include quarterly financial audits, clear interest-rate disclosures (current APR cap examples: ~28% consumer loans in Thailand 2024), and strict Personal Data Protection Act (PDPA) compliance to protect 1.2M+ customer records.

Staying ahead of rule changes preserves the SET listing and lending license; regulatory fines in Thailand reached ฿2.3bn in 2023 for financial sector breaches, so proactive compliance reduces legal and reputational risk.

- Quarterly audits and annual external audit

- Transparent APR and fee disclosures

- PDPA data controls for 1.2M customers

- Regulatory watch to protect SET listing

- Mitigate fines (sector fines ฿2.3bn in 2023)

Strong loan growth, 2.8% NPLs, Umay+ revenue ฿1.9bn and 78% recovery

Core activities: refine credit-scoring and monthly loss monitoring (NPLs 2.8% in 2024; loans ฿42.6bn, +24% YoY); market Umay+ (avg disbursal 12 min; 22% user growth, THB1.9bn revenue 2024); manage collections/compliance (78% recovery 2024; PDPA for 1.2M customers; ฿120–150M tech spend 2024–25 reducing processing 48→18 hrs).

| Metric | 2024 |

|---|---|

| NPLs | 2.8% |

| Gross loans | ฿42.6bn |

| Umay+ revenue | ฿1.9bn |

| Recovery rate | 78% |

| Tech spend | ฿120–150M |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Easy Buy Public Company Ltd. Business Model Canvas—not a mockup—and it matches the file you’ll receive after purchase; upon ordering, you’ll instantly get the complete, editable document in Word and Excel formats, structured and formatted exactly as shown.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Easy Buy PLC: Compact Business Model Canvas for Investors, Advisors & Founders

Unlock the full strategic blueprint behind Easy Buy Public Company Ltd.’s business model—this concise Business Model Canvas maps value propositions, customer segments, key partners, and revenue streams to show how the company scales and defends market share; download the complete Word/Excel canvas for a ready-to-use toolkit ideal for investors, advisors, and founders seeking actionable, company-specific insights.

Partnerships

Parent Company ACOM Japan

As a subsidiary of ACOM Co., Ltd., Easy Buy taps ACOM Japan’s ₿¥200 billion+ group lending capacity and 60+ years consumer-finance expertise to secure funding and strategic oversight.

Since 2023 ACOM tech transfer brought AI-driven credit scoring and Basel-aligned risk frameworks to Easy Buy, cutting NPLs by ~15% and supporting compliant growth into 2025.

Local Commercial Banks

Strategic alliances with major Thai banks such as Bangkok Bank, Kasikornbank, and Siam Commercial Bank secure diverse funding lines—Easy Buy had THB 8.3 billion committed credit facilities in 2025—to support lending and buffer interest-rate swings. These partnerships enable interbank fund transfers and automated repayments via PromptPay and BAHTNET, ensuring liquidity and stable operations amid 2024–25 policy rate volatility.

Retail and Merchant Partners

Easy Buy partners with over 12,000 department stores, electronics retailers, and mobile shops across Thailand to offer point-of-sale installment loans, driving roughly 45% of new originations in 2024 (฿18.6bn of ฿41.3bn total loans). These merchant touchpoints let customers apply for credit at purchase for high-value items, extending Easy Buy’s reach without opening branches and cutting customer acquisition cost by an estimated 28% versus branch-led sourcing.

National Credit Bureau NCB

Payment Service Providers

Partnerships with convenience chains like 7‑Eleven and digital wallets (TrueMoney, Rabbit LINE Pay) give customers 24/7 repayment across ~13,000 retail outlets and 20+ e-wallets, raising on-time collection and trimming cash collection costs by ~12% (2024 internal ops data).

These networks cut payment friction for monthly installments, supporting Easy Buy’s ~95% collection rate and reducing late payments by an estimated 18% year‑on‑year.

- 13,000 retail outlets

- 20+ e-wallet partners

- 95% collection rate

- 12% lower cash collection costs

- 18% fewer late payments Y/Y

Easy Buy + ACOM: ₿200bn backing, AI cuts NPLs ~15%, 95% collections

Easy Buy leverages ACOM Japan’s ₿¥200bn+ funding and 60y expertise, bank lines (THB 8.3bn committed, 2025) and NCB access to 18M+ records to power AI credit scoring, cut NPLs ~15% and lower net charge-off 1.4ppt; merchant (12,000 stores) and 13,000 retail/payments touchpoints drive 45% originations and 95% collections.

| Metric | Value |

|---|---|

| ACOM group capacity | ฿200bn+ |

| Committed bank lines (2025) | THB 8.3bn |

| NCB records (2025) | 18M+ |

| Merchant partners | 12,000+ |

| Retail outlets for repayment | 13,000 |

| Originations via merchants (2024) | 45% (฿18.6bn) |

| Collection rate | 95% |

| NPL reduction (post-AI) | ~15% |

| Net charge-off improvement (2024) | -1.4 ppt |

What is included in the product

A concise, pre-built Business Model Canvas for Easy Buy Public Company Ltd. outlining customer segments, channels, value propositions, revenue streams, key activities, resources, partners, cost structure, and customer relationships with actionable insights and SWOT-linked competitive analysis for investor presentations and strategic decision-making.

High-level view of Easy Buy Public Company Ltd.’s business model with editable cells, condensing omni-channel lending, partner retail finance, and risk controls into a one-page snapshot for quick strategic review and team collaboration.

Activities

Credit Risk Management and Scoring

The core activity continuously refines proprietary credit-scoring models combining traditional financials and alternative behavioral data; Easy Buy cut 2024 portfolio NPLs to 2.8% from 4.1% in 2021 while growing gross loans 24% YoY to ฿42.6bn in 2024, balancing expansion in underserved segments with credit quality through monthly model recalibration and segment-level loss-rate monitoring.

Marketing and Customer Acquisition

Easy Buy Public Company Ltd markets Umay+ with aggressive digital ads, TV spots, and on-ground booths in malls and BTS stations, driving a 22% year-on-year user growth and 18% increase in loan originations in 2024. Branding stresses fast, reliable, accessible credit—average disbursal time 12 minutes—supporting a 2024 contribution of Umay+ to group revenue of ~THB 1.9 billion.

Debt Collection and Recovery

Managing loan lifecycles at Easy Buy Public Company Ltd. relies on a compliant collections unit following Bank of Thailand and Consumer Protection rules; operations mix automated SMS/reminder systems, outbound call centers, and legal action for accounts >180 days past due. Recovery rates matter: in 2024 Easy Buy reported a 78% recovery on past-due portfolios, helping sustain a THB 12.4 billion revolving credit book and preserve net interest margin.

Digital Platform Development

As of late 2025, Easy Buy Public Company Ltd. focuses major resources on enhancing the Umay+ app and self-service portals, spending ~฿120–150 million in 2024–25 on software, cybersecurity, and e-KYC integration to cut loan processing time from 48 to ~18 hours and lower servicing costs by ~22%.

- ฿120–150M investment (2024–25)

- Processing time down 63% (48→18 hrs)

- Servicing cost reduction ~22%

- e-KYC lowers onboarding friction, raises digital adoption to ~68%

Regulatory Compliance and Reporting

Operating as a non-bank financial institution, Easy Buy Public Company Ltd. must follow Bank of Thailand and Office of the Consumer Protection Board rules; core tasks include quarterly financial audits, clear interest-rate disclosures (current APR cap examples: ~28% consumer loans in Thailand 2024), and strict Personal Data Protection Act (PDPA) compliance to protect 1.2M+ customer records.

Staying ahead of rule changes preserves the SET listing and lending license; regulatory fines in Thailand reached ฿2.3bn in 2023 for financial sector breaches, so proactive compliance reduces legal and reputational risk.

- Quarterly audits and annual external audit

- Transparent APR and fee disclosures

- PDPA data controls for 1.2M customers

- Regulatory watch to protect SET listing

- Mitigate fines (sector fines ฿2.3bn in 2023)

Strong loan growth, 2.8% NPLs, Umay+ revenue ฿1.9bn and 78% recovery

Core activities: refine credit-scoring and monthly loss monitoring (NPLs 2.8% in 2024; loans ฿42.6bn, +24% YoY); market Umay+ (avg disbursal 12 min; 22% user growth, THB1.9bn revenue 2024); manage collections/compliance (78% recovery 2024; PDPA for 1.2M customers; ฿120–150M tech spend 2024–25 reducing processing 48→18 hrs).

| Metric | 2024 |

|---|---|

| NPLs | 2.8% |

| Gross loans | ฿42.6bn |

| Umay+ revenue | ฿1.9bn |

| Recovery rate | 78% |

| Tech spend | ฿120–150M |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Easy Buy Public Company Ltd. Business Model Canvas—not a mockup—and it matches the file you’ll receive after purchase; upon ordering, you’ll instantly get the complete, editable document in Word and Excel formats, structured and formatted exactly as shown.