Ebiquity Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

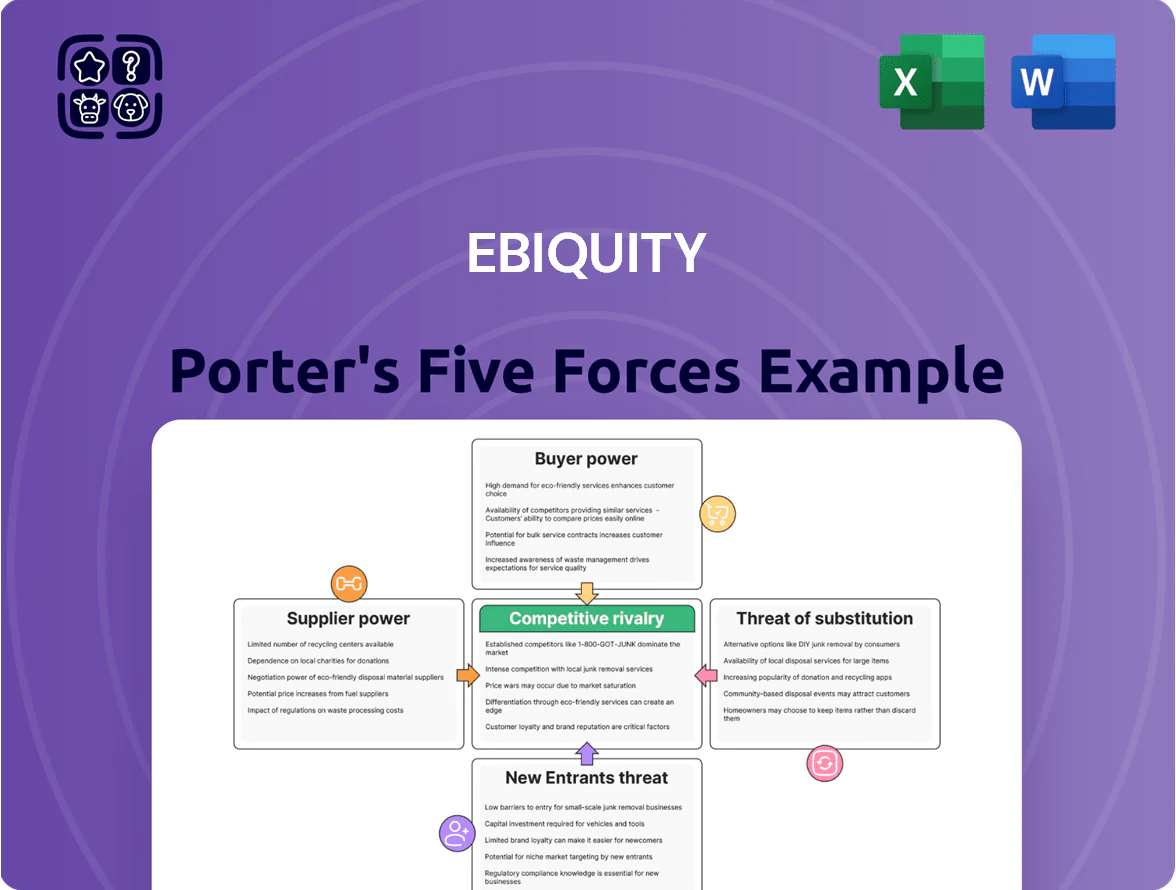

Ebiquity faces moderate supplier and buyer power, niche rivalry from specialized agencies, evolving tech-driven substitutes, and steady barriers to entry—creating a dynamic yet navigable competitive landscape that rewards strategic differentiation and scale.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ebiquity’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Proprietary Media Benchmarking Data

Ebiquity depends on data feeds from media agencies, platforms, and third-party providers to run its benchmarking and analytics; about 60–70% of its usable inputs come from these external sources, so output quality mirrors supplier cooperation and data integrity. As platforms tighten access—walled gardens like Google and Meta control ~80% of global digital ad spend—supplier leverage rises, raising input costs and risking gaps in comparability that could reduce Ebiquity’s addressable analytics scope and revenue per client.

Specialized Human Capital and Analytical Talent

The primary resource for Ebiquity is its pool of media auditors and data scientists, and in 2025 UK median data scientist pay rose to ~95,000 GBP, boosting supplier (talent) leverage on pay and conditions.

In a tight labor market—UK tech vacancies down 18% in 2024 but specialist analytics roles still scarce—these professionals can demand higher compensation and remote/flex terms.

Retaining top talent is critical: 2024 client retention linked to audit quality shows firms with low analyst turnover (≤10%) keep 5–8% more revenue.

Technology and Infrastructure Providers

As Ebiquity scales digital services, dependence on cloud providers (AWS, Azure, Google Cloud) and niche ad-tech vendors rises, giving suppliers pricing leverage; enterprise cloud spend can be 10–18% of comparable martech firms’ OPEX, so small price moves matter. Switching integrated data systems often costs millions and months of migration, locking Ebiquity into vendor terms and impacting margins and time-to-market for new analytics features.

Global Media Transparency Standards

Regulatory bodies and industry associations, like ISBA (UK) and ANA (US), act as indirect suppliers by setting media-audit standards that give Ebiquity legitimacy and a framework to operate.

Compliance with evolving global standards—e.g., 2024 IAB measurement updates and ANA media transparency guidelines—remains non-negotiable for Ebiquity to keep its position as a trusted intermediary.

These entities set the rules of the game; Ebiquity must follow them to keep services relevant, protect revenues (Ebiquity reported £72.3m revenue in FY 2024) and retain client trust.

- Standards = legitimacy

- Must comply with 2024 IAB/ANA updates

- Non-compliance risks revenue and trust

Fragmented Niche Data Sources

Ebiquity relies on dozens of regional data vendors to cover 85+ markets; each small supplier has low individual leverage but together they create dependency for global reports, raising coordination costs and risk of gaps.

Maintaining consistent, accurate local feeds is a logistical and financial priority—contracting, QA, and data-mapping can add 3–5% to operating costs and slow delivery by 7–14 days.

- Global coverage: 85+ markets

- Collective dependence: dozens of vendors

- Added cost: ~3–5% of ops

- Potential delay: 7–14 days

Supplier squeeze: 80% platform control, high cloud/talent costs risk margins & rollout

Ebiquity faces moderate–high supplier power: platforms (Google/Meta) control ~80% digital spend access, cloud vendors can be 10–18% of OPEX, and 60–70% of usable inputs come from external data; talent costs rose (UK median data scientist £95,000 in 2025). Collective regional vendors cover 85+ markets, adding ~3–5% ops cost and 7–14 day delays, so supplier moves can squeeze margins and slow product rollout.

| Metric | Value |

|---|---|

| Platform control | ~80% |

| External data inputs | 60–70% |

| Cloud OPEX share | 10–18% |

| Data scientist median pay (UK, 2025) | £95,000 |

| Market coverage | 85+ markets |

| Added ops cost | 3–5% |

| Delivery delay | 7–14 days |

What is included in the product

Concise Porter’s Five Forces assessment of Ebiquity, revealing competitive intensity, buyer/supplier leverage, entry barriers, substitute risks, and strategic vulnerabilities specific to its media and advertising analytics market.

Compact five-forces snapshot tailored for Ebiquity—instantly diagnose competitive pressures and export a polished slide-ready summary for faster, more confident strategic decisions.

Customers Bargaining Power

Concentration of Global Brand Spend

Ebiquity’s clients are top global advertisers controlling roughly 60–70% of industry spend in key markets, giving them strong negotiating power; in 2024, the top 10 clients contributed an estimated 35% of Ebiquity’s revenue, so they can demand bespoke solutions and price concessions. Large-volume buyers squeeze margins and leverage long contracts, and losing a single blue-chip client can cut regional revenue by double-digit percentages within a fiscal year.

Low Switching Costs for Auditing Services

While Ebiquity brings deep media-audit expertise, low switching costs let brands put audits out to pitch quickly; 2024 IPA data shows 28% of UK advertisers reviewed agency contracts annually, raising churn risk. Clients can move to competitors or boutiques if they see lower ROI or less innovation, and Ebiquity faces pressure to justify fees—average media audit fees fell 6% in 2023 across Europe. That forces continuous delivery of measurable ROI and service upgrades to retain clients.

In-housing of Data Analytics Capabilities

A rising number of major advertisers are building in-house analytics: 42% of Global 2000 marketers surveyed in 2024 reported expanding proprietary data stacks, lowering dependence on third-party measurement firms like Ebiquity.

As clients internalize measurement, Ebiquity faces reduced bargaining power from customers for routine services and must shift to higher-margin strategic advisory, creative media strategy, and audit work to sustain revenue—Ebiquity reported 2024 advisory growth of 12% versus flat execution fees.

Demand for Real-Time Performance Transparency

Modern marketers now demand real-time performance transparency—live dashboards and streaming metrics—so firms offering instantaneous insights gain leverage; a 2024 Forrester survey found 62% of CMOs prioritize real-time analytics over monthly audits.

Clients prefer automated, tech-led solutions to manual consultancy, driving bargaining power to vendors with scalable platforms; programmatic analytics platforms grew 18% YoY in 2024, showing this shift.

Ebiquity must evolve its product suite continuously—investing in live dashboards and automation—to retain clients and limit churn, since firms replacing legacy audits cut external consultancy spend by ~12% in 2024.

- 62% of CMOs prioritize real-time analytics (Forrester 2024)

- Programmatic analytics market +18% YoY (2024)

- Legacy-to-digital shifts cut consultancy spend ~12% (2024)

Price Sensitivity in Economic Downturns

- 67% of firms cut marketing spend in 2023

- 22% rise in outcome-based contract demand (2024)

- 10–15% potential discounting risk for premium firms

Clients dictate terms: top advertisers, in‑house analytics and programmatic shift Ebiquity to advisory

Clients hold strong bargaining power: top advertisers drive 60–70% of spend and the top 10 made ~35% of Ebiquity’s 2024 revenue, enabling price concessions and bespoke demands; low switching costs, 28% annual contract reviews (IPA 2024), and 42% of Global 2000 building in-house analytics cut dependence on third parties. Real-time analytics (62% CMOs, Forrester 2024) and programmatic tools (+18% YoY) push demand for automated, outcome-based (↑22% 2024) contracts, forcing Ebiquity toward higher-margin advisory services.

| Metric | 2023–24 Data |

|---|---|

| Top-client revenue share | ~35% |

| Advertiser market control | 60–70% |

| Annual contract reviews | 28% (IPA 2024) |

| In-house analytics | 42% (Global 2000, 2024) |

| CMOs prioritizing real-time | 62% (Forrester 2024) |

| Programmatic market growth | +18% YoY (2024) |

| Outcome-based demand rise | +22% (2024) |

What You See Is What You Get

Ebiquity Porter's Five Forces Analysis

This preview shows the exact Ebiquity Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the file is fully formatted and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Ebiquity faces moderate supplier and buyer power, niche rivalry from specialized agencies, evolving tech-driven substitutes, and steady barriers to entry—creating a dynamic yet navigable competitive landscape that rewards strategic differentiation and scale.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ebiquity’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Access to Proprietary Media Benchmarking Data

Ebiquity depends on data feeds from media agencies, platforms, and third-party providers to run its benchmarking and analytics; about 60–70% of its usable inputs come from these external sources, so output quality mirrors supplier cooperation and data integrity. As platforms tighten access—walled gardens like Google and Meta control ~80% of global digital ad spend—supplier leverage rises, raising input costs and risking gaps in comparability that could reduce Ebiquity’s addressable analytics scope and revenue per client.

Specialized Human Capital and Analytical Talent

The primary resource for Ebiquity is its pool of media auditors and data scientists, and in 2025 UK median data scientist pay rose to ~95,000 GBP, boosting supplier (talent) leverage on pay and conditions.

In a tight labor market—UK tech vacancies down 18% in 2024 but specialist analytics roles still scarce—these professionals can demand higher compensation and remote/flex terms.

Retaining top talent is critical: 2024 client retention linked to audit quality shows firms with low analyst turnover (≤10%) keep 5–8% more revenue.

Technology and Infrastructure Providers

As Ebiquity scales digital services, dependence on cloud providers (AWS, Azure, Google Cloud) and niche ad-tech vendors rises, giving suppliers pricing leverage; enterprise cloud spend can be 10–18% of comparable martech firms’ OPEX, so small price moves matter. Switching integrated data systems often costs millions and months of migration, locking Ebiquity into vendor terms and impacting margins and time-to-market for new analytics features.

Global Media Transparency Standards

Regulatory bodies and industry associations, like ISBA (UK) and ANA (US), act as indirect suppliers by setting media-audit standards that give Ebiquity legitimacy and a framework to operate.

Compliance with evolving global standards—e.g., 2024 IAB measurement updates and ANA media transparency guidelines—remains non-negotiable for Ebiquity to keep its position as a trusted intermediary.

These entities set the rules of the game; Ebiquity must follow them to keep services relevant, protect revenues (Ebiquity reported £72.3m revenue in FY 2024) and retain client trust.

- Standards = legitimacy

- Must comply with 2024 IAB/ANA updates

- Non-compliance risks revenue and trust

Fragmented Niche Data Sources

Ebiquity relies on dozens of regional data vendors to cover 85+ markets; each small supplier has low individual leverage but together they create dependency for global reports, raising coordination costs and risk of gaps.

Maintaining consistent, accurate local feeds is a logistical and financial priority—contracting, QA, and data-mapping can add 3–5% to operating costs and slow delivery by 7–14 days.

- Global coverage: 85+ markets

- Collective dependence: dozens of vendors

- Added cost: ~3–5% of ops

- Potential delay: 7–14 days

Supplier squeeze: 80% platform control, high cloud/talent costs risk margins & rollout

Ebiquity faces moderate–high supplier power: platforms (Google/Meta) control ~80% digital spend access, cloud vendors can be 10–18% of OPEX, and 60–70% of usable inputs come from external data; talent costs rose (UK median data scientist £95,000 in 2025). Collective regional vendors cover 85+ markets, adding ~3–5% ops cost and 7–14 day delays, so supplier moves can squeeze margins and slow product rollout.

| Metric | Value |

|---|---|

| Platform control | ~80% |

| External data inputs | 60–70% |

| Cloud OPEX share | 10–18% |

| Data scientist median pay (UK, 2025) | £95,000 |

| Market coverage | 85+ markets |

| Added ops cost | 3–5% |

| Delivery delay | 7–14 days |

What is included in the product

Concise Porter’s Five Forces assessment of Ebiquity, revealing competitive intensity, buyer/supplier leverage, entry barriers, substitute risks, and strategic vulnerabilities specific to its media and advertising analytics market.

Compact five-forces snapshot tailored for Ebiquity—instantly diagnose competitive pressures and export a polished slide-ready summary for faster, more confident strategic decisions.

Customers Bargaining Power

Concentration of Global Brand Spend

Ebiquity’s clients are top global advertisers controlling roughly 60–70% of industry spend in key markets, giving them strong negotiating power; in 2024, the top 10 clients contributed an estimated 35% of Ebiquity’s revenue, so they can demand bespoke solutions and price concessions. Large-volume buyers squeeze margins and leverage long contracts, and losing a single blue-chip client can cut regional revenue by double-digit percentages within a fiscal year.

Low Switching Costs for Auditing Services

While Ebiquity brings deep media-audit expertise, low switching costs let brands put audits out to pitch quickly; 2024 IPA data shows 28% of UK advertisers reviewed agency contracts annually, raising churn risk. Clients can move to competitors or boutiques if they see lower ROI or less innovation, and Ebiquity faces pressure to justify fees—average media audit fees fell 6% in 2023 across Europe. That forces continuous delivery of measurable ROI and service upgrades to retain clients.

In-housing of Data Analytics Capabilities

A rising number of major advertisers are building in-house analytics: 42% of Global 2000 marketers surveyed in 2024 reported expanding proprietary data stacks, lowering dependence on third-party measurement firms like Ebiquity.

As clients internalize measurement, Ebiquity faces reduced bargaining power from customers for routine services and must shift to higher-margin strategic advisory, creative media strategy, and audit work to sustain revenue—Ebiquity reported 2024 advisory growth of 12% versus flat execution fees.

Demand for Real-Time Performance Transparency

Modern marketers now demand real-time performance transparency—live dashboards and streaming metrics—so firms offering instantaneous insights gain leverage; a 2024 Forrester survey found 62% of CMOs prioritize real-time analytics over monthly audits.

Clients prefer automated, tech-led solutions to manual consultancy, driving bargaining power to vendors with scalable platforms; programmatic analytics platforms grew 18% YoY in 2024, showing this shift.

Ebiquity must evolve its product suite continuously—investing in live dashboards and automation—to retain clients and limit churn, since firms replacing legacy audits cut external consultancy spend by ~12% in 2024.

- 62% of CMOs prioritize real-time analytics (Forrester 2024)

- Programmatic analytics market +18% YoY (2024)

- Legacy-to-digital shifts cut consultancy spend ~12% (2024)

Price Sensitivity in Economic Downturns

- 67% of firms cut marketing spend in 2023

- 22% rise in outcome-based contract demand (2024)

- 10–15% potential discounting risk for premium firms

Clients dictate terms: top advertisers, in‑house analytics and programmatic shift Ebiquity to advisory

Clients hold strong bargaining power: top advertisers drive 60–70% of spend and the top 10 made ~35% of Ebiquity’s 2024 revenue, enabling price concessions and bespoke demands; low switching costs, 28% annual contract reviews (IPA 2024), and 42% of Global 2000 building in-house analytics cut dependence on third parties. Real-time analytics (62% CMOs, Forrester 2024) and programmatic tools (+18% YoY) push demand for automated, outcome-based (↑22% 2024) contracts, forcing Ebiquity toward higher-margin advisory services.

| Metric | 2023–24 Data |

|---|---|

| Top-client revenue share | ~35% |

| Advertiser market control | 60–70% |

| Annual contract reviews | 28% (IPA 2024) |

| In-house analytics | 42% (Global 2000, 2024) |

| CMOs prioritizing real-time | 62% (Forrester 2024) |

| Programmatic market growth | +18% YoY (2024) |

| Outcome-based demand rise | +22% (2024) |

What You See Is What You Get

Ebiquity Porter's Five Forces Analysis

This preview shows the exact Ebiquity Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the file is fully formatted and ready for download and use the moment you buy.