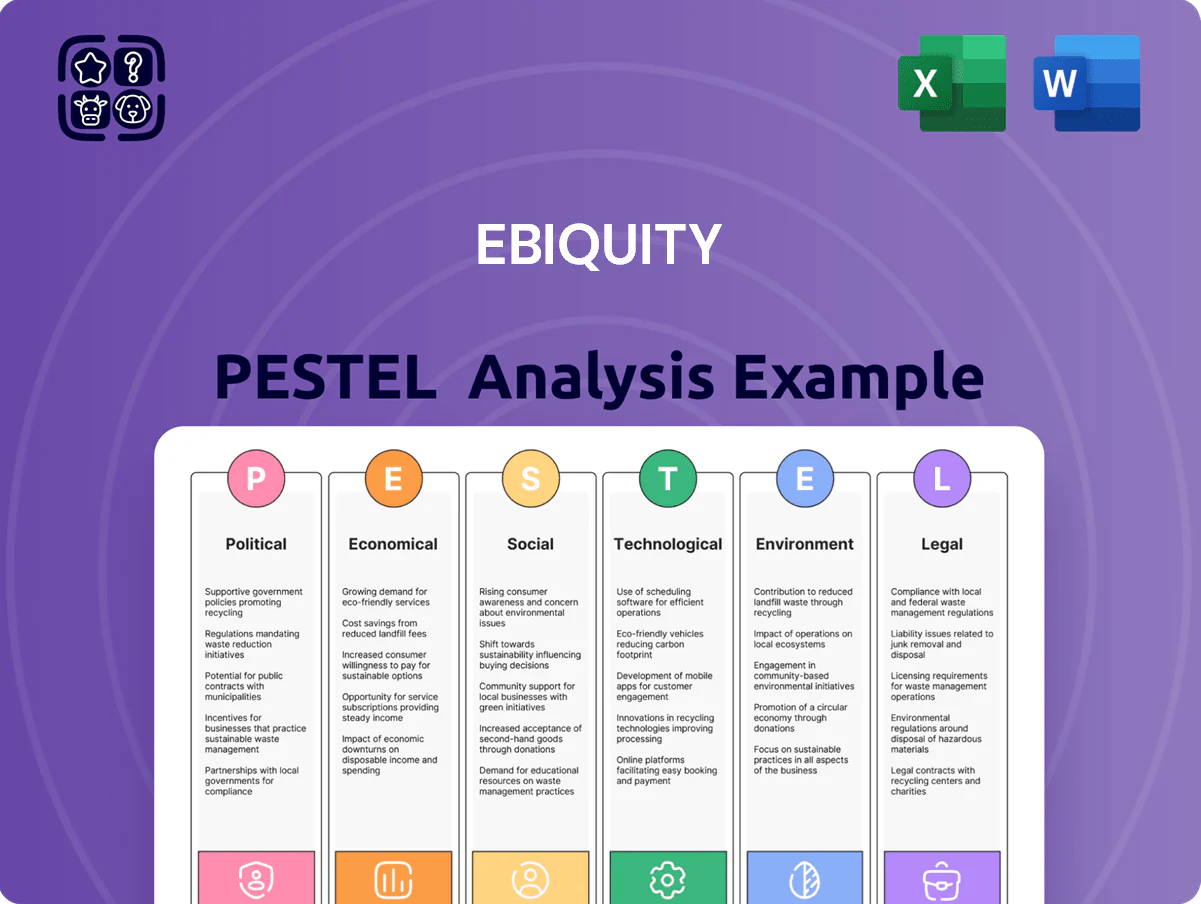

Ebiquity PESTLE Analysis

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and evolving tech trends are reshaping Ebiquity’s competitive landscape—our concise PESTLE snapshot highlights the key external drivers and strategic risks you need to know; purchase the full PESTLE for a complete, actionable breakdown tailored to investors, consultants, and strategy teams.

Political factors

Global Geopolitical Stability

Geopolitical tensions in 2025 continue to reshape media allocation, with 34% of global CMOs reporting reduced spend in high-risk emerging markets; Ebiquity must manage rapid client pullbacks after events like the 2024–25 trade disputes that cut regional ad spend by an estimated $6.7bn. A flexible advisory model is needed to respond to shifting alliances, sanctions and rising trade barriers that can alter campaign viability overnight.

Government Media Regulation

Rising government intervention in digital competition, including EU DMA enforcement and US antitrust scrutiny, reshapes Google and Meta operations and increases demand for ad transparency; 2024 CMA actions and ~30% rise in regulatory cases boosted market need for verification.

Data Sovereignty Laws

Nationalistic data residency laws—over 80 countries had data localization requirements by 2024—force cross-border handling limits for media performance data, affecting programmatic measurement and campaign attribution for global clients.

Ebiquity must align analytics, storage and processing with localized political mandates (e.g., EU GDPR, India’s PDPB drafts), increasing compliance costs but reducing legal risk for advertisers.

This regulatory complexity boosts the strategic value of Ebiquity’s 25+ market footprint and local teams, enabling compliant insights for international advertisers and supporting revenue resilience—global compliance services can command premium rates, improving margins.

Public Sector Advertising Trends

Changes in government leadership frequently reallocate public sector communication budgets; UK central government marketing spend fell 12% in 2023 to £1.1bn, illustrating volatility governments face.

Ebiquity can help optimize taxpayer-funded campaigns through media investment analysis, with typical public-sector consulting contracts ranging from £200k–£5m annually.

Political instability can pause or fast-track procurement cycles—contract awards rose 18% in stable periods versus freezes during transitions.

- Leadership changes → budget reallocation (UK marketing spend -12% in 2023 to £1.1bn)

- Ebiquity value → optimize spend; public-sector contracts £200k–£5m

- Stability impact → +18% contract awards in stable periods vs freezes

Trade Policy and Protectionism

Trade disputes between major economies (US-China tariffs added $100–150bn in annual costs globally in 2019–21) can raise input prices for Ebiquity’s retail and automotive clients, compressing margins and prompting cuts to marketing spend.

When client margins are squeezed, marketing budgets are often audited first; 2023 IAB data showed 28% of firms reduced ad spend during tariff shocks, increasing demand for efficiency audits.

Ebiquity’s ROI-focused services become critical—clients seeking to reallocate reduced marketing budgets drove a 12% rise in consultancy engagements in 2024, underscoring value during political-economic friction.

- Tariff-induced cost shocks: $100–150bn global impact (2019–21)

- 28% of firms cut ad spend in tariff-related downturns (2023 IAB)

- Ebiquity saw +12% consultancy demand in 2024 for ROI optimization

Regulatory shocks drive Ebiquity consultancy surge as $6.7bn ad cuts reshape markets

Political shifts (trade disputes, sanctions, data laws) increased demand for Ebiquity’s compliance and ROI services; 2024–25 effects: regional ad spend cuts $6.7bn, 25+ market footprint, +12% consultancy demand (2024), >80 countries with data residency by 2024, UK govt marketing -12% to £1.1bn (2023).

| Metric | Value |

|---|---|

| Regional ad cuts | $6.7bn |

| Consultancy demand | +12% (2024) |

| Data residency laws | >80 countries (2024) |

| UK gov marketing | £1.1bn (-12%) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ebiquity across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and investors identify threats, opportunities, and strategic responses tailored to the company’s market and industry.

Concise PESTLE summary tailored for Ebiquity that segments political, economic, social, technological, legal and environmental insights for quick meeting use, easily dropped into presentations or shared across teams to streamline external risk discussions and client-facing reports.

Economic factors

Inflationary Pressures on Media Costs

Rising costs of media inventory—up ~12% year-on-year for premium digital and 8–15% for high-demand TV slots in 2024—force brands to scrutinize spend; Ebiquity’s benchmarking showed average overpayment of 6–10% across clients, helping confirm fair market value during inflationary cycles.

Global Interest Rate Environment

As central banks tightened policy into 2025—global policy rates averaged about 4.2% in Q1 2025—higher cost of capital is squeezing marketing budgets and pushing clients toward short-term performance tactics over long-term brand investment; Ebiquity’s ROI and econometric benchmarks (showing average long-term brand ROI uplift of 20–35% over three years) enable clients to rebalance spend by quantifying sustained value versus immediate returns.

Currency Exchange Volatility

Operating across 25+ markets, Ebiquity faces GBP volatility versus USD and EUR; between 2023–2025 GBP moved roughly 8–12% against the dollar, amplifying revenue translation risk for FY24 where 30%+ of fees were USD-linked.

For multinational clients, currency swings can change reported CPMs and ROI by up to 10–15%, distorting perceived efficiency of global media buys during 2024’s policy- and rate-driven FX moves.

Ebiquity’s normalized, multi-market analysis—using constant-currency reporting and hedging-adjusted metrics—removes FX noise, enabling accurate cross-border financial reporting and client benchmarking.

Shift to Retail Media Investment

The rapid growth of retail media networks redirected advertiser spend, with estimates showing retail media ad revenues reaching about $60bn globally in 2024, forcing Ebiquity to reallocate auditing focus toward POS, first‑party data and closed‑loop attribution.

Ebiquity must update audit frameworks to measure ROI inside closed ecosystems, integrating on‑site sales lift, A/B test results and first‑party match rates to prove value.

This economic shift opens a revenue stream: specialist measurement services for retail media, where premium fees can capture higher CPMs and attribution engagements growing double digits year‑on‑year (c.20%+ in 2023–24).

- Retail media revenues ~ $60bn (2024)

- Attribution services growing ~20% YoY (2023–24)

- Need for first‑party data, POS lift, closed‑loop metrics

Consumer Spending Patterns

Economic downturns and shifts in disposable income reduce advertising intensity in consumer sectors; UK retail sales fell 0.8% month-on-month in Dec 2025, pressuring ad spend.

Ebiquity’s counter-cyclical model benefits as brands pursue efficiency—client demand for ROI measurement rose 22% in 2024–25.

Analyzing marketing-spend elasticity vs consumer demand remains core; Ebiquity benchmarks show average ad spend elasticity of 1.4 in FMCG during 2023–25.

- Lower disposable income → reduced ad intensity (UK retail −0.8% MoM Dec 2025)

- Counter-cyclical demand ↑ for efficiency services (+22% client demand 2024–25)

- Core offering: ad spend elasticity analysis (FMCG elasticity ~1.4, 2023–25)

Rising media costs, rate hikes & FX volatility drive demand for ROI benchmarking

Rising media costs (premium digital +12% y/y; TV 8–15% in 2024) and higher policy rates (global avg ~4.2% Q1 2025) squeeze budgets, increasing demand for Ebiquity’s ROI benchmarking (long-term brand ROI +20–35% over 3 years); retail media growth (~$60bn 2024) fuels attribution services (+~20% YoY); FX moves (GBP vs USD/EUR ±8–12% 2023–25) necessitate constant‑currency reporting.

| Metric | Value |

|---|---|

| Premium digital cost rise | +12% (2024) |

| TV high‑demand slots | 8–15% (2024) |

| Global policy rate | 4.2% (Q1 2025) |

| Retail media revenue | $60bn (2024) |

| Attribution growth | ~20% YoY (2023–24) |

| GBP vs USD volatility | ±8–12% (2023–25) |

What You See Is What You Get

Ebiquity PESTLE Analysis

The preview shown here is the exact Ebiquity PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, and evolving tech trends are reshaping Ebiquity’s competitive landscape—our concise PESTLE snapshot highlights the key external drivers and strategic risks you need to know; purchase the full PESTLE for a complete, actionable breakdown tailored to investors, consultants, and strategy teams.

Political factors

Global Geopolitical Stability

Geopolitical tensions in 2025 continue to reshape media allocation, with 34% of global CMOs reporting reduced spend in high-risk emerging markets; Ebiquity must manage rapid client pullbacks after events like the 2024–25 trade disputes that cut regional ad spend by an estimated $6.7bn. A flexible advisory model is needed to respond to shifting alliances, sanctions and rising trade barriers that can alter campaign viability overnight.

Government Media Regulation

Rising government intervention in digital competition, including EU DMA enforcement and US antitrust scrutiny, reshapes Google and Meta operations and increases demand for ad transparency; 2024 CMA actions and ~30% rise in regulatory cases boosted market need for verification.

Data Sovereignty Laws

Nationalistic data residency laws—over 80 countries had data localization requirements by 2024—force cross-border handling limits for media performance data, affecting programmatic measurement and campaign attribution for global clients.

Ebiquity must align analytics, storage and processing with localized political mandates (e.g., EU GDPR, India’s PDPB drafts), increasing compliance costs but reducing legal risk for advertisers.

This regulatory complexity boosts the strategic value of Ebiquity’s 25+ market footprint and local teams, enabling compliant insights for international advertisers and supporting revenue resilience—global compliance services can command premium rates, improving margins.

Public Sector Advertising Trends

Changes in government leadership frequently reallocate public sector communication budgets; UK central government marketing spend fell 12% in 2023 to £1.1bn, illustrating volatility governments face.

Ebiquity can help optimize taxpayer-funded campaigns through media investment analysis, with typical public-sector consulting contracts ranging from £200k–£5m annually.

Political instability can pause or fast-track procurement cycles—contract awards rose 18% in stable periods versus freezes during transitions.

- Leadership changes → budget reallocation (UK marketing spend -12% in 2023 to £1.1bn)

- Ebiquity value → optimize spend; public-sector contracts £200k–£5m

- Stability impact → +18% contract awards in stable periods vs freezes

Trade Policy and Protectionism

Trade disputes between major economies (US-China tariffs added $100–150bn in annual costs globally in 2019–21) can raise input prices for Ebiquity’s retail and automotive clients, compressing margins and prompting cuts to marketing spend.

When client margins are squeezed, marketing budgets are often audited first; 2023 IAB data showed 28% of firms reduced ad spend during tariff shocks, increasing demand for efficiency audits.

Ebiquity’s ROI-focused services become critical—clients seeking to reallocate reduced marketing budgets drove a 12% rise in consultancy engagements in 2024, underscoring value during political-economic friction.

- Tariff-induced cost shocks: $100–150bn global impact (2019–21)

- 28% of firms cut ad spend in tariff-related downturns (2023 IAB)

- Ebiquity saw +12% consultancy demand in 2024 for ROI optimization

Regulatory shocks drive Ebiquity consultancy surge as $6.7bn ad cuts reshape markets

Political shifts (trade disputes, sanctions, data laws) increased demand for Ebiquity’s compliance and ROI services; 2024–25 effects: regional ad spend cuts $6.7bn, 25+ market footprint, +12% consultancy demand (2024), >80 countries with data residency by 2024, UK govt marketing -12% to £1.1bn (2023).

| Metric | Value |

|---|---|

| Regional ad cuts | $6.7bn |

| Consultancy demand | +12% (2024) |

| Data residency laws | >80 countries (2024) |

| UK gov marketing | £1.1bn (-12%) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ebiquity across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and investors identify threats, opportunities, and strategic responses tailored to the company’s market and industry.

Concise PESTLE summary tailored for Ebiquity that segments political, economic, social, technological, legal and environmental insights for quick meeting use, easily dropped into presentations or shared across teams to streamline external risk discussions and client-facing reports.

Economic factors

Inflationary Pressures on Media Costs

Rising costs of media inventory—up ~12% year-on-year for premium digital and 8–15% for high-demand TV slots in 2024—force brands to scrutinize spend; Ebiquity’s benchmarking showed average overpayment of 6–10% across clients, helping confirm fair market value during inflationary cycles.

Global Interest Rate Environment

As central banks tightened policy into 2025—global policy rates averaged about 4.2% in Q1 2025—higher cost of capital is squeezing marketing budgets and pushing clients toward short-term performance tactics over long-term brand investment; Ebiquity’s ROI and econometric benchmarks (showing average long-term brand ROI uplift of 20–35% over three years) enable clients to rebalance spend by quantifying sustained value versus immediate returns.

Currency Exchange Volatility

Operating across 25+ markets, Ebiquity faces GBP volatility versus USD and EUR; between 2023–2025 GBP moved roughly 8–12% against the dollar, amplifying revenue translation risk for FY24 where 30%+ of fees were USD-linked.

For multinational clients, currency swings can change reported CPMs and ROI by up to 10–15%, distorting perceived efficiency of global media buys during 2024’s policy- and rate-driven FX moves.

Ebiquity’s normalized, multi-market analysis—using constant-currency reporting and hedging-adjusted metrics—removes FX noise, enabling accurate cross-border financial reporting and client benchmarking.

Shift to Retail Media Investment

The rapid growth of retail media networks redirected advertiser spend, with estimates showing retail media ad revenues reaching about $60bn globally in 2024, forcing Ebiquity to reallocate auditing focus toward POS, first‑party data and closed‑loop attribution.

Ebiquity must update audit frameworks to measure ROI inside closed ecosystems, integrating on‑site sales lift, A/B test results and first‑party match rates to prove value.

This economic shift opens a revenue stream: specialist measurement services for retail media, where premium fees can capture higher CPMs and attribution engagements growing double digits year‑on‑year (c.20%+ in 2023–24).

- Retail media revenues ~ $60bn (2024)

- Attribution services growing ~20% YoY (2023–24)

- Need for first‑party data, POS lift, closed‑loop metrics

Consumer Spending Patterns

Economic downturns and shifts in disposable income reduce advertising intensity in consumer sectors; UK retail sales fell 0.8% month-on-month in Dec 2025, pressuring ad spend.

Ebiquity’s counter-cyclical model benefits as brands pursue efficiency—client demand for ROI measurement rose 22% in 2024–25.

Analyzing marketing-spend elasticity vs consumer demand remains core; Ebiquity benchmarks show average ad spend elasticity of 1.4 in FMCG during 2023–25.

- Lower disposable income → reduced ad intensity (UK retail −0.8% MoM Dec 2025)

- Counter-cyclical demand ↑ for efficiency services (+22% client demand 2024–25)

- Core offering: ad spend elasticity analysis (FMCG elasticity ~1.4, 2023–25)

Rising media costs, rate hikes & FX volatility drive demand for ROI benchmarking

Rising media costs (premium digital +12% y/y; TV 8–15% in 2024) and higher policy rates (global avg ~4.2% Q1 2025) squeeze budgets, increasing demand for Ebiquity’s ROI benchmarking (long-term brand ROI +20–35% over 3 years); retail media growth (~$60bn 2024) fuels attribution services (+~20% YoY); FX moves (GBP vs USD/EUR ±8–12% 2023–25) necessitate constant‑currency reporting.

| Metric | Value |

|---|---|

| Premium digital cost rise | +12% (2024) |

| TV high‑demand slots | 8–15% (2024) |

| Global policy rate | 4.2% (Q1 2025) |

| Retail media revenue | $60bn (2024) |

| Attribution growth | ~20% YoY (2023–24) |

| GBP vs USD volatility | ±8–12% (2023–25) |

What You See Is What You Get

Ebiquity PESTLE Analysis

The preview shown here is the exact Ebiquity PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.