Echo Global Logistics Porter's Five Forces Analysis

Don't Miss the Bigger Picture

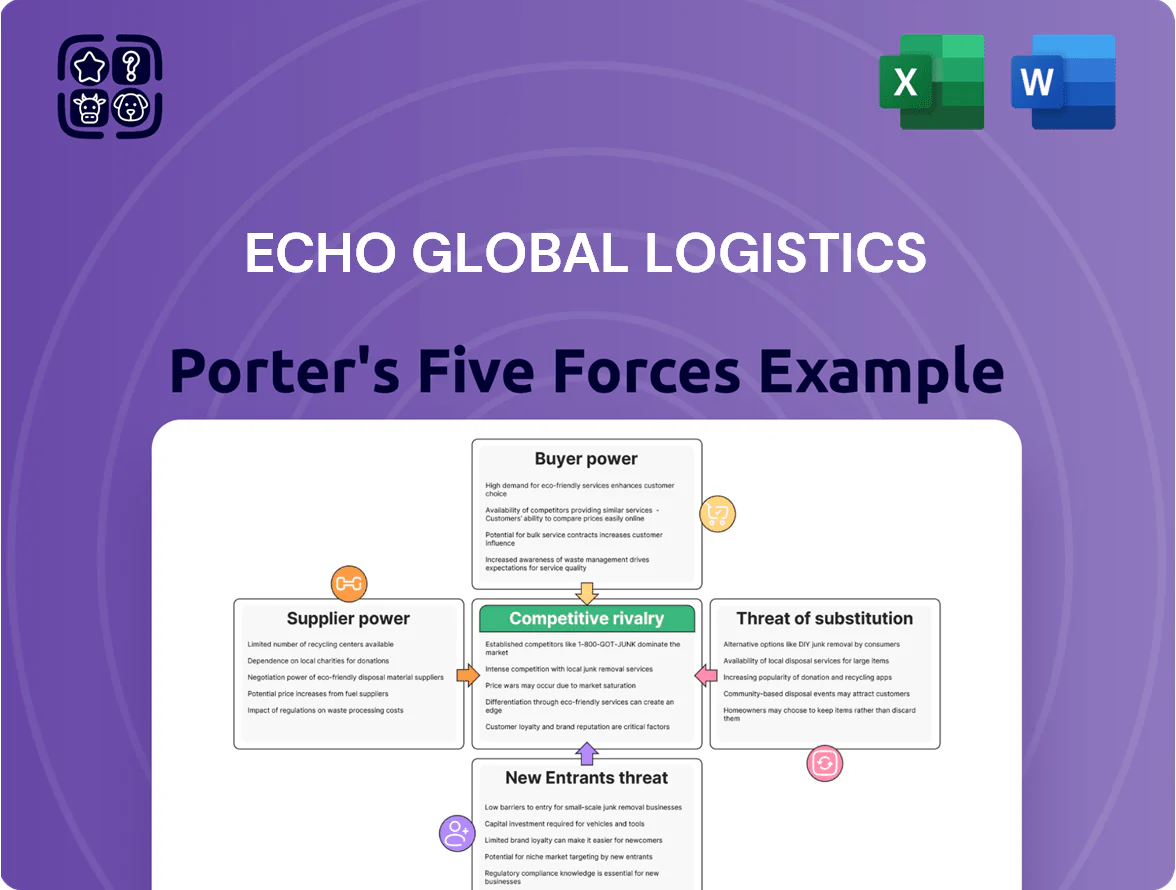

Echo Global Logistics faces moderate supplier leverage, intense buyer price sensitivity, and significant competitive rivalry from asset-light and asset-heavy players; this snapshot highlights strategic pressures but omits force-by-force ratings and modeling.

This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Echo Global Logistics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Carrier Network

Echo Global Logistics sources capacity from a fragmented pool of over 60,000 US carriers (2024), mostly small-to-mid fleets, so no single carrier holds meaningful market share and Echo keeps negotiating leverage. This dispersion lowers individual supplier bargaining power, allowing Echo to secure blended spot and contract rates that preserved gross margins around 22% in FY2024. Still, regional tightness can spike spot rates short-term, so Echo hedges via diversified contracts and volume discounts.

Dependence on Echo's Technology

Many small carriers depend on Echo’s proprietary platform and digital freight-matching tools to find loads and cut deadhead miles, with Echo reporting over 60,000 contracted carriers in 2024 and platform-enabled utilization improving yields by ~8% for carriers per Echo’s 2024 filings.

By supplying essential volume and back-office efficiency—Echo handled $3.8B in revenue freight brokerage in 2024—Echo becomes a critical partner, creating switching costs and reducing carriers’ leverage.

Fuel Price Volatility

Carriers shoulder fuel and maintenance costs, and US diesel prices jumped ~38% in 2021–2022, pushing spot rates up; in sharp cost spikes suppliers try to pass increases to brokers via higher base rates. Echo’s brokerage model reduces that leverage because its 2024 TMS and real-time analytics cut empty miles and improve load-matching, lowering fuel spend by an estimated 6–10% per load. Still, sustained fuel shocks raise carrier bargaining power during tight capacity windows.

Driver Shortages and Regulatory Impact

- Driver capacity down 5–8% (2024)

- Spot rates up 3–12% when tight

- Echo carrier pool: 80,000+ (2025)

Low Switching Costs for Echo

Echo Global Logistics (Echo) faces low supplier power because it is not tied to specific carriers and shifted roughly 18% of freight volume among top carriers in 2024 to chase better rates and service, per company disclosures.

This flexibility forces carriers to offer competitive pricing and meet performance KPIs or risk losing lanes, which weakens carriers’ bargaining leverage.

The lack of material switching costs—Echo’s multi-carrier platform and spot-market access—reduces supplier power and supports margin capture.

- Echo shifted ~18% volume among carriers in 2024

- Multi-carrier model lowers switching costs

- Carriers must compete on price and KPIs

Echo retains supplier leverage—22% GM despite spot-rate spikes and tighter driver hours

Echo faces low-to-moderate supplier power: fragmented 80,000+ carrier pool (2025) and 18% volume shifting in 2024 give Echo leverage, preserving ~22% gross margin in FY2024; driver-hours down 5–8% (2024) and spot-rate spikes of 3–12% raise temporary carrier power.

| Metric | Value |

|---|---|

| Contracted carriers | 80,000+ (2025) |

| Volume shifted | ~18% (2024) |

| Gross margin | ~22% (FY2024) |

| Driver-hours change | -5–8% (2024) |

| Spot rate spike | +3–12% (tight periods) |

What is included in the product

Tailored Porter's Five Forces analysis for Echo Global Logistics, uncovering competitive intensity, buyer/supplier power, entry barriers, substitute threats, and strategic implications for pricing and market position.

A concise Porter's Five Forces snapshot for Echo Global Logistics—quickly spot where competitive pressures bite and which levers relieve margin squeeze.

Customers Bargaining Power

High Customer Concentration Risks

Large enterprise shippers can account for over 30% of Echo Global Logistics’ revenue in some contracts, giving them leverage to demand volume discounts and cut per-shipment margins by 10–20%.

These buyers run dedicated procurement teams and RFPs; industry data shows 70% of RFPs use reverse auctions, pushing spot margins down for providers like Echo.

Echo must balance these low-margin, high-volume accounts with smaller transactional customers—often 40–60% higher gross margin—to preserve overall profitability.

Low Switching Costs for Shippers

The logistics market has low switching costs: industry surveys show 62% of shippers had no exclusive carrier contracts in 2024, letting them shift volumes quickly if price or service improves elsewhere.

Shippers can pilot new brokers and digital freight platforms within weeks; digital bidding reduced onboarding time by 40% in 2023, increasing churn risk.

Echo counters this by selling managed transportation and deeper tech integration—Echo's TMS and API links raised customer retention to ~84% for managed accounts in 2024.

Price Sensitivity in Commodity Markets

Many customers treat freight as a commodity, making price the main choice factor; spot rates fell ~18% YoY in 2023 during excess capacity, pressuring Echo Global Logistics’ (ECHO) gross margins toward the 8–10% range in weak quarters.

This price sensitivity forces persistent downward margin pressure, notably when GDP slows or truck utilization drops below 90%. Echo counters by selling visibility and reliability—technology-led tracking and service SLAs—to reduce reliance on price competition and protect yield.

Access to Real-Time Market Data

Modern shippers use benchmarking tools and digital platforms that show real-time freight rates, and in 2025 spot market indices (DAT, FreightWaves) reported month-to-month rate volatility of 8–15%, giving customers data parity to challenge Echo Global Logistics pricing.

Echo must deploy advanced analytics and proprietary rate intelligence to justify premiums and demonstrate savings; firms using predictive pricing cut procurement costs by ~5–12% per McKinsey 2024 supply-chain reports.

Failing to show clear, quantified value risks rate erosion as 42% of shippers (2023 Coyote/UPS survey) switch brokers within 12 months for better transparency.

- Real-time indices: 8–15% monthly volatility

- Potential savings with analytics: 5–12%

- Switching risk: 42% churn within 12 months

Demand for Value-Added Services

Customers now expect analytics, carbon tracking, and end-to-end visibility alongside freight; global shippers using tech-driven providers grew 18% in 2024, raising expectations on Echo Global Logistics (Echo).

That makes Echo more central to operations but shifts negotiating power to buyers who can demand these features as standard; if Echo lags, clients may push rates down or switch to rivals with richer services.

- Demand rise: 18% more tech-driven shippers (2024)

- Risk: lost leverage if innovation lags

- Need: standardize analytics, carbon, visibility

Echo must quantify value: cut costs 5–12%, retain 84% amid high shipper power

Large shippers can be >30% of revenue and force 10–20% lower margins; 62% had no exclusivity in 2024, enabling quick switching. Spot volatility 8–15% monthly (DAT/FreightWaves 2025) and 42% broker churn within 12 months raise buyer power. Echo’s managed accounts show ~84% retention (2024), and predictive pricing can save buyers 5–12% (McKinsey 2024), so Echo must prove quantified value.

| Metric | Value |

|---|---|

| Large-shipper revenue share | >30% |

| Non-exclusive shippers (2024) | 62% |

| Spot volatility (2025) | 8–15% m/m |

| Broker churn | 42% yr |

| Managed-account retention (Echo 2024) | ~84% |

| Procurement savings via analytics | 5–12% |

Preview the Actual Deliverable

Echo Global Logistics Porter's Five Forces Analysis

This preview displays the exact Echo Global Logistics Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready to download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Echo Global Logistics faces moderate supplier leverage, intense buyer price sensitivity, and significant competitive rivalry from asset-light and asset-heavy players; this snapshot highlights strategic pressures but omits force-by-force ratings and modeling.

This brief preview only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Echo Global Logistics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Fragmented Carrier Network

Echo Global Logistics sources capacity from a fragmented pool of over 60,000 US carriers (2024), mostly small-to-mid fleets, so no single carrier holds meaningful market share and Echo keeps negotiating leverage. This dispersion lowers individual supplier bargaining power, allowing Echo to secure blended spot and contract rates that preserved gross margins around 22% in FY2024. Still, regional tightness can spike spot rates short-term, so Echo hedges via diversified contracts and volume discounts.

Dependence on Echo's Technology

Many small carriers depend on Echo’s proprietary platform and digital freight-matching tools to find loads and cut deadhead miles, with Echo reporting over 60,000 contracted carriers in 2024 and platform-enabled utilization improving yields by ~8% for carriers per Echo’s 2024 filings.

By supplying essential volume and back-office efficiency—Echo handled $3.8B in revenue freight brokerage in 2024—Echo becomes a critical partner, creating switching costs and reducing carriers’ leverage.

Fuel Price Volatility

Carriers shoulder fuel and maintenance costs, and US diesel prices jumped ~38% in 2021–2022, pushing spot rates up; in sharp cost spikes suppliers try to pass increases to brokers via higher base rates. Echo’s brokerage model reduces that leverage because its 2024 TMS and real-time analytics cut empty miles and improve load-matching, lowering fuel spend by an estimated 6–10% per load. Still, sustained fuel shocks raise carrier bargaining power during tight capacity windows.

Driver Shortages and Regulatory Impact

- Driver capacity down 5–8% (2024)

- Spot rates up 3–12% when tight

- Echo carrier pool: 80,000+ (2025)

Low Switching Costs for Echo

Echo Global Logistics (Echo) faces low supplier power because it is not tied to specific carriers and shifted roughly 18% of freight volume among top carriers in 2024 to chase better rates and service, per company disclosures.

This flexibility forces carriers to offer competitive pricing and meet performance KPIs or risk losing lanes, which weakens carriers’ bargaining leverage.

The lack of material switching costs—Echo’s multi-carrier platform and spot-market access—reduces supplier power and supports margin capture.

- Echo shifted ~18% volume among carriers in 2024

- Multi-carrier model lowers switching costs

- Carriers must compete on price and KPIs

Echo retains supplier leverage—22% GM despite spot-rate spikes and tighter driver hours

Echo faces low-to-moderate supplier power: fragmented 80,000+ carrier pool (2025) and 18% volume shifting in 2024 give Echo leverage, preserving ~22% gross margin in FY2024; driver-hours down 5–8% (2024) and spot-rate spikes of 3–12% raise temporary carrier power.

| Metric | Value |

|---|---|

| Contracted carriers | 80,000+ (2025) |

| Volume shifted | ~18% (2024) |

| Gross margin | ~22% (FY2024) |

| Driver-hours change | -5–8% (2024) |

| Spot rate spike | +3–12% (tight periods) |

What is included in the product

Tailored Porter's Five Forces analysis for Echo Global Logistics, uncovering competitive intensity, buyer/supplier power, entry barriers, substitute threats, and strategic implications for pricing and market position.

A concise Porter's Five Forces snapshot for Echo Global Logistics—quickly spot where competitive pressures bite and which levers relieve margin squeeze.

Customers Bargaining Power

High Customer Concentration Risks

Large enterprise shippers can account for over 30% of Echo Global Logistics’ revenue in some contracts, giving them leverage to demand volume discounts and cut per-shipment margins by 10–20%.

These buyers run dedicated procurement teams and RFPs; industry data shows 70% of RFPs use reverse auctions, pushing spot margins down for providers like Echo.

Echo must balance these low-margin, high-volume accounts with smaller transactional customers—often 40–60% higher gross margin—to preserve overall profitability.

Low Switching Costs for Shippers

The logistics market has low switching costs: industry surveys show 62% of shippers had no exclusive carrier contracts in 2024, letting them shift volumes quickly if price or service improves elsewhere.

Shippers can pilot new brokers and digital freight platforms within weeks; digital bidding reduced onboarding time by 40% in 2023, increasing churn risk.

Echo counters this by selling managed transportation and deeper tech integration—Echo's TMS and API links raised customer retention to ~84% for managed accounts in 2024.

Price Sensitivity in Commodity Markets

Many customers treat freight as a commodity, making price the main choice factor; spot rates fell ~18% YoY in 2023 during excess capacity, pressuring Echo Global Logistics’ (ECHO) gross margins toward the 8–10% range in weak quarters.

This price sensitivity forces persistent downward margin pressure, notably when GDP slows or truck utilization drops below 90%. Echo counters by selling visibility and reliability—technology-led tracking and service SLAs—to reduce reliance on price competition and protect yield.

Access to Real-Time Market Data

Modern shippers use benchmarking tools and digital platforms that show real-time freight rates, and in 2025 spot market indices (DAT, FreightWaves) reported month-to-month rate volatility of 8–15%, giving customers data parity to challenge Echo Global Logistics pricing.

Echo must deploy advanced analytics and proprietary rate intelligence to justify premiums and demonstrate savings; firms using predictive pricing cut procurement costs by ~5–12% per McKinsey 2024 supply-chain reports.

Failing to show clear, quantified value risks rate erosion as 42% of shippers (2023 Coyote/UPS survey) switch brokers within 12 months for better transparency.

- Real-time indices: 8–15% monthly volatility

- Potential savings with analytics: 5–12%

- Switching risk: 42% churn within 12 months

Demand for Value-Added Services

Customers now expect analytics, carbon tracking, and end-to-end visibility alongside freight; global shippers using tech-driven providers grew 18% in 2024, raising expectations on Echo Global Logistics (Echo).

That makes Echo more central to operations but shifts negotiating power to buyers who can demand these features as standard; if Echo lags, clients may push rates down or switch to rivals with richer services.

- Demand rise: 18% more tech-driven shippers (2024)

- Risk: lost leverage if innovation lags

- Need: standardize analytics, carbon, visibility

Echo must quantify value: cut costs 5–12%, retain 84% amid high shipper power

Large shippers can be >30% of revenue and force 10–20% lower margins; 62% had no exclusivity in 2024, enabling quick switching. Spot volatility 8–15% monthly (DAT/FreightWaves 2025) and 42% broker churn within 12 months raise buyer power. Echo’s managed accounts show ~84% retention (2024), and predictive pricing can save buyers 5–12% (McKinsey 2024), so Echo must prove quantified value.

| Metric | Value |

|---|---|

| Large-shipper revenue share | >30% |

| Non-exclusive shippers (2024) | 62% |

| Spot volatility (2025) | 8–15% m/m |

| Broker churn | 42% yr |

| Managed-account retention (Echo 2024) | ~84% |

| Procurement savings via analytics | 5–12% |

Preview the Actual Deliverable

Echo Global Logistics Porter's Five Forces Analysis

This preview displays the exact Echo Global Logistics Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready to download with no placeholders or samples.