Echostar Porter's Five Forces Analysis

From Overview to Strategy Blueprint

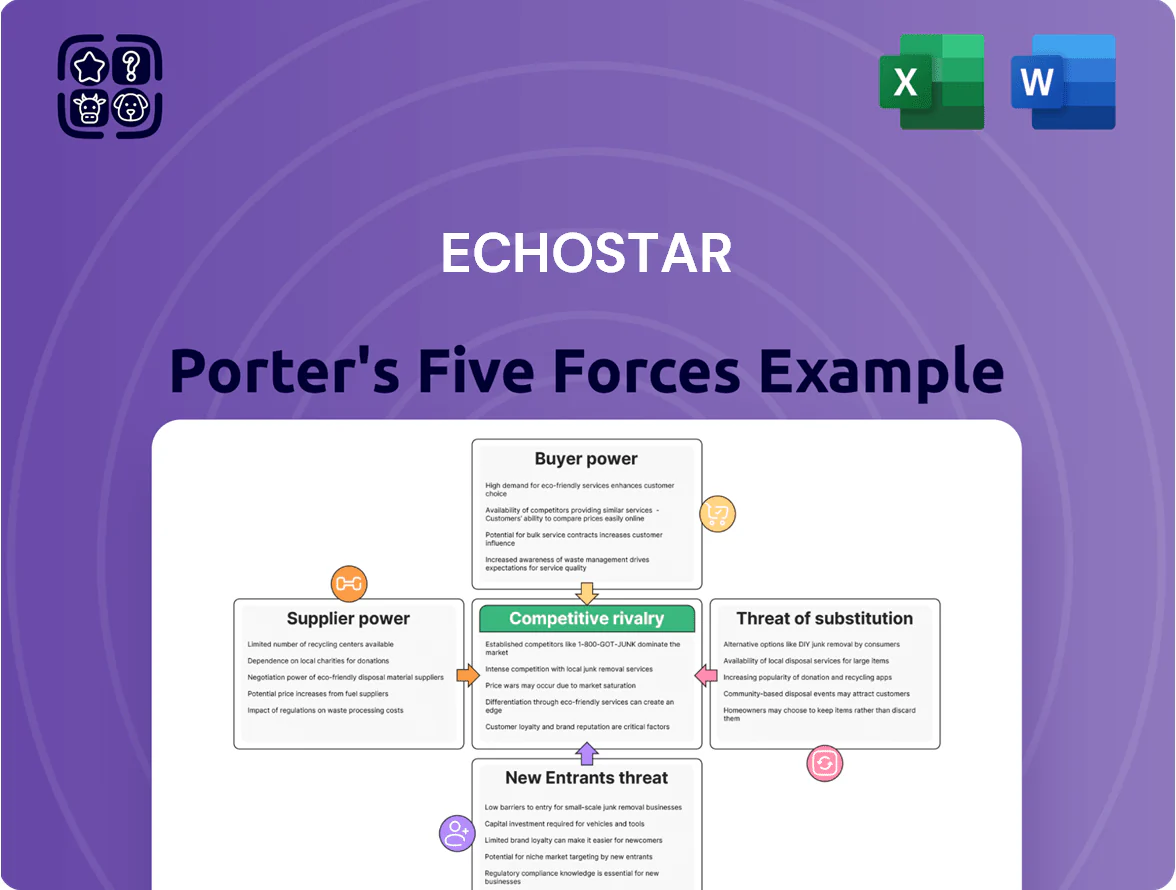

Echostar operates in a high-capital, tech-driven market where supplier leverage and competitive rivalry are significant, buyer power varies between consumer and wholesale channels, and substitutes (streaming/cloud platforms) pose growing threats—yet strong IP, spectrum assets, and service integration offer defensive advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Echostar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Satellite Launch Providers

The heavy-lift launch market is concentrated: SpaceX captured ~70% of global orbital launches in 2024 and Blue Origin and ULA control much of the rest, limiting EchoStar’s bargaining leverage.

As EchoStar refreshes its orbital fleet, it depends on those providers’ schedules and published price bands—Falcon Heavy quoted ~$150M–$250M per launch in 2024—so timing and cost risk are external.

Concentration lets suppliers set contract terms and prioritize internal or higher‑paying government missions, raising delay and price exposure for EchoStar.

Specialized Semiconductor and Equipment Vendors

EchoStar depends on a small set of specialized semiconductor and equipment vendors for HughesNet modems and 5G Open RAN kit; in 2024 global chip shortages pushed lead times from 12 to 28 weeks, raising procurement costs by an estimated 8–12% for comms hardware suppliers.

Any vendor strategy shift or supply-chain disruption can force EchoStar to absorb higher component prices or face deployment delays that slow subscriber growth and CAPEX schedules.

Because these chipsets are highly specialized, switching suppliers needs months of re-engineering and validation, plus non-recurring engineering costs often exceeding $5–10M per platform, which strengthens supplier bargaining power.

Media Content Licensing for Pay-TV Operations

The DISH merger leaves EchoStar highly dependent on major media conglomerates for live-sports and hit-entertainment rights; top rights deals now command carriage fees that rose ~8–12% annually in 2024, squeezing EchoStar's pay-TV margins (EchoStar reported consolidated gross margin pressure of ~150–250 bp in FY2024).

Terrestrial Spectrum and Infrastructure Partners

EchoStar holds substantial spectrum but depends on tower operators and backhaul firms for terrestrial 5G sites; long-term leases and site control in top 50 US MSAs give suppliers leverage.

Commercial real estate and energy cost rises—US CPI energy up ~8.5% in 2024 and industrial rents +6%—let suppliers pass inflation to EchoStar via lease escalators and higher power/backhaul fees.

Suppliers can increase switching costs and delay rollouts, raising EchoStar’s capex by an estimated 10–15% per new urban site.

- Long-term leases concentrate power in top tower firms

- Top 50 MSAs drive pricing pressure

- Energy CPI +8.5% (2024) empowers pass-throughs

- Estimated 10–15% higher capex per urban site

Global Regulatory and Licensing Authorities

Government agencies and international bodies allocate orbital slots and spectrum, acting as non-commercial but powerful suppliers; ITU coordination delays can add months and cost operators millions—EchoStar reported $1.2B capex in 2024, partly driven by spectrum and slot fees.

EchoStar must meet evolving mandates across jurisdictions, raising compliance costs and limiting flexibility; multi-jurisdiction filings and licenses can exceed $50M per satellite program in legal and regulatory expenses.

Shifts in national security rules or stricter space-debris rules (e.g., 25-year deorbit guidelines and growing ESA/US DoD scrutiny) can restrict asset availability and delay launches.

- ITU and national regulators control scarce spectrum/orbital resources

- Regulatory compliance adds millions—EchoStar capex and legal costs visible in 2024 filings

- Policy shifts on security/debris can quickly tighten access or raise costs

Supplier concentration drives EchoStar cost, timing and margin risk

Suppliers wield strong leverage over EchoStar: launch firms (SpaceX ~70% share 2024) and specialized chip vendors drive price and timing risk—Falcon Heavy ~$150M–$250M/launch (2024); chip lead times rose 12→28 weeks, adding ~8–12% hardware cost; content rights rose ~8–12% YoY (2024), and energy CPI +8.5% (2024) raised site OPEX.

| Supplier | Key 2024 Metric | Impact |

|---|---|---|

| Launch providers | SpaceX ~70% global launches; Falcon Heavy $150M–$250M | Schedule & price risk |

| Chip vendors | Lead times 12→28 wks; costs +8–12% | Procurement delays, NRE $5–10M |

| Content rights | Fees +8–12% YoY | Margin pressure (~150–250 bp FY2024) |

| Energy/real estate | Energy CPI +8.5%; rents +6% | Higher OPEX, +10–15% urban site CAPEX |

| Regulators | Slot/spectrum fees in 2024; $1.2B capex cited | Licensing delays, compliance costs $50M+ |

What is included in the product

Tailored Porter's Five Forces assessment for Echostar that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic risks to inform investor and management decisions.

A concise Porter's Five Forces one-sheet for EchoStar—quickly highlights supplier, buyer, and competitive pressures to guide strategic moves and investor decisions.

Customers Bargaining Power

Low Switching Costs in the Retail Wireless Market

US mobile users face low switching costs due to number portability and promos; churn averaged 1.1% monthly for prepaid in 2024, so Boost Mobile (EchoStar) must match aggressive pricing and unlimited data tiers to retain subscribers.

Increased Availability of High-Speed Alternatives

Rural broadband customers, long captive to EchoStar’s Hughes Network Systems, now choose LEO alternatives like SpaceX Starlink, which had ~1.5 million subscribers worldwide by end-2024, eroding EchoStar’s pricing power.

This competition forced EchoStar to raise monthly data caps and cut latency—Hughes’ JUPITER 3 improvements trimmed latency by ~20% in 2023—so customers compare Mbps, latency, and price when switching.

Negotiation Leverage of Government and Enterprise Clients

Large government and enterprise buyers use competitive bids prioritizing cost; in 2024 US federal satellite procurements averaged discounts around 12–18% off list, boosting their leverage.

These buyers demand custom solutions, strict SLAs, and volume discounts; EchoStar’s Satellite Services posted $1.9B revenue in 2024, so losing one major contract (often >5–10% of segment sales) would hit stability.

Price Sensitivity in the Linear Television Segment

As streaming overtakes linear TV, remaining satellite subscribers are highly price-sensitive; Nielsen reported in 2024 that U.S. pay-TV households fell to 45%, down from 70% in 2014, pressuring churn when prices rise.

Customers often cancel or downgrade after increases because comparable content appears on cheaper OTT platforms; DISH reported Q4 2024 net pay-TV losses of ~120,000 subscribers, constraining EchoStar’s ability to pass on rising content costs.

- 45% U.S. pay-TV households (2024)

- ~120,000 DISH pay-TV net losses (Q4 2024)

- High churn on price hikes vs cheaper OTT

Empowerment through Digital Comparison Tools

Proliferation of online review platforms and comparison engines gives consumers real-time visibility into network latency, uptime and throughput, so EchoStar faces public metrics showing Dish Network/Loral satellites often report 99.7% uptime industry-wide in 2024.

This transparency forces EchoStar to sustain high customer service and technical reliability to protect brand reputation; public outages drop NPS by ~10 points on average within 48 hours.

Informed customers cite benchmarked performance during retention calls to extract discounts or faster provisioning, raising churn negotiation leverage and pressuring ARPU downward.

Customer power squeezes EchoStar: low churn, Starlink rivalry & big-contract risk

Customers wield strong bargaining power: low switching costs for mobile (1.1% prepaid monthly churn in 2024), LEO competition (Starlink ~1.5M subs end-2024) and falling pay-TV demand (45% U.S. pay-TV households in 2024) force EchoStar to match price, latency, and SLAs or face ARPU pressure; major contracts (5–10% of Satellite Services $1.9B 2024 revenue) amplify buyer leverage.

| Metric | Value (2024) |

|---|---|

| Prepaid churn | 1.1% monthly |

| Starlink subs | ~1.5M |

| Pay-TV households | 45% |

| EchoStar Satellite rev | $1.9B |

Preview the Actual Deliverable

Echostar Porter's Five Forces Analysis

This preview shows the exact Echostar Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written file; once payment is complete, you’ll get instant access to this exact document with no further setup required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Echostar operates in a high-capital, tech-driven market where supplier leverage and competitive rivalry are significant, buyer power varies between consumer and wholesale channels, and substitutes (streaming/cloud platforms) pose growing threats—yet strong IP, spectrum assets, and service integration offer defensive advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Echostar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Satellite Launch Providers

The heavy-lift launch market is concentrated: SpaceX captured ~70% of global orbital launches in 2024 and Blue Origin and ULA control much of the rest, limiting EchoStar’s bargaining leverage.

As EchoStar refreshes its orbital fleet, it depends on those providers’ schedules and published price bands—Falcon Heavy quoted ~$150M–$250M per launch in 2024—so timing and cost risk are external.

Concentration lets suppliers set contract terms and prioritize internal or higher‑paying government missions, raising delay and price exposure for EchoStar.

Specialized Semiconductor and Equipment Vendors

EchoStar depends on a small set of specialized semiconductor and equipment vendors for HughesNet modems and 5G Open RAN kit; in 2024 global chip shortages pushed lead times from 12 to 28 weeks, raising procurement costs by an estimated 8–12% for comms hardware suppliers.

Any vendor strategy shift or supply-chain disruption can force EchoStar to absorb higher component prices or face deployment delays that slow subscriber growth and CAPEX schedules.

Because these chipsets are highly specialized, switching suppliers needs months of re-engineering and validation, plus non-recurring engineering costs often exceeding $5–10M per platform, which strengthens supplier bargaining power.

Media Content Licensing for Pay-TV Operations

The DISH merger leaves EchoStar highly dependent on major media conglomerates for live-sports and hit-entertainment rights; top rights deals now command carriage fees that rose ~8–12% annually in 2024, squeezing EchoStar's pay-TV margins (EchoStar reported consolidated gross margin pressure of ~150–250 bp in FY2024).

Terrestrial Spectrum and Infrastructure Partners

EchoStar holds substantial spectrum but depends on tower operators and backhaul firms for terrestrial 5G sites; long-term leases and site control in top 50 US MSAs give suppliers leverage.

Commercial real estate and energy cost rises—US CPI energy up ~8.5% in 2024 and industrial rents +6%—let suppliers pass inflation to EchoStar via lease escalators and higher power/backhaul fees.

Suppliers can increase switching costs and delay rollouts, raising EchoStar’s capex by an estimated 10–15% per new urban site.

- Long-term leases concentrate power in top tower firms

- Top 50 MSAs drive pricing pressure

- Energy CPI +8.5% (2024) empowers pass-throughs

- Estimated 10–15% higher capex per urban site

Global Regulatory and Licensing Authorities

Government agencies and international bodies allocate orbital slots and spectrum, acting as non-commercial but powerful suppliers; ITU coordination delays can add months and cost operators millions—EchoStar reported $1.2B capex in 2024, partly driven by spectrum and slot fees.

EchoStar must meet evolving mandates across jurisdictions, raising compliance costs and limiting flexibility; multi-jurisdiction filings and licenses can exceed $50M per satellite program in legal and regulatory expenses.

Shifts in national security rules or stricter space-debris rules (e.g., 25-year deorbit guidelines and growing ESA/US DoD scrutiny) can restrict asset availability and delay launches.

- ITU and national regulators control scarce spectrum/orbital resources

- Regulatory compliance adds millions—EchoStar capex and legal costs visible in 2024 filings

- Policy shifts on security/debris can quickly tighten access or raise costs

Supplier concentration drives EchoStar cost, timing and margin risk

Suppliers wield strong leverage over EchoStar: launch firms (SpaceX ~70% share 2024) and specialized chip vendors drive price and timing risk—Falcon Heavy ~$150M–$250M/launch (2024); chip lead times rose 12→28 weeks, adding ~8–12% hardware cost; content rights rose ~8–12% YoY (2024), and energy CPI +8.5% (2024) raised site OPEX.

| Supplier | Key 2024 Metric | Impact |

|---|---|---|

| Launch providers | SpaceX ~70% global launches; Falcon Heavy $150M–$250M | Schedule & price risk |

| Chip vendors | Lead times 12→28 wks; costs +8–12% | Procurement delays, NRE $5–10M |

| Content rights | Fees +8–12% YoY | Margin pressure (~150–250 bp FY2024) |

| Energy/real estate | Energy CPI +8.5%; rents +6% | Higher OPEX, +10–15% urban site CAPEX |

| Regulators | Slot/spectrum fees in 2024; $1.2B capex cited | Licensing delays, compliance costs $50M+ |

What is included in the product

Tailored Porter's Five Forces assessment for Echostar that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic risks to inform investor and management decisions.

A concise Porter's Five Forces one-sheet for EchoStar—quickly highlights supplier, buyer, and competitive pressures to guide strategic moves and investor decisions.

Customers Bargaining Power

Low Switching Costs in the Retail Wireless Market

US mobile users face low switching costs due to number portability and promos; churn averaged 1.1% monthly for prepaid in 2024, so Boost Mobile (EchoStar) must match aggressive pricing and unlimited data tiers to retain subscribers.

Increased Availability of High-Speed Alternatives

Rural broadband customers, long captive to EchoStar’s Hughes Network Systems, now choose LEO alternatives like SpaceX Starlink, which had ~1.5 million subscribers worldwide by end-2024, eroding EchoStar’s pricing power.

This competition forced EchoStar to raise monthly data caps and cut latency—Hughes’ JUPITER 3 improvements trimmed latency by ~20% in 2023—so customers compare Mbps, latency, and price when switching.

Negotiation Leverage of Government and Enterprise Clients

Large government and enterprise buyers use competitive bids prioritizing cost; in 2024 US federal satellite procurements averaged discounts around 12–18% off list, boosting their leverage.

These buyers demand custom solutions, strict SLAs, and volume discounts; EchoStar’s Satellite Services posted $1.9B revenue in 2024, so losing one major contract (often >5–10% of segment sales) would hit stability.

Price Sensitivity in the Linear Television Segment

As streaming overtakes linear TV, remaining satellite subscribers are highly price-sensitive; Nielsen reported in 2024 that U.S. pay-TV households fell to 45%, down from 70% in 2014, pressuring churn when prices rise.

Customers often cancel or downgrade after increases because comparable content appears on cheaper OTT platforms; DISH reported Q4 2024 net pay-TV losses of ~120,000 subscribers, constraining EchoStar’s ability to pass on rising content costs.

- 45% U.S. pay-TV households (2024)

- ~120,000 DISH pay-TV net losses (Q4 2024)

- High churn on price hikes vs cheaper OTT

Empowerment through Digital Comparison Tools

Proliferation of online review platforms and comparison engines gives consumers real-time visibility into network latency, uptime and throughput, so EchoStar faces public metrics showing Dish Network/Loral satellites often report 99.7% uptime industry-wide in 2024.

This transparency forces EchoStar to sustain high customer service and technical reliability to protect brand reputation; public outages drop NPS by ~10 points on average within 48 hours.

Informed customers cite benchmarked performance during retention calls to extract discounts or faster provisioning, raising churn negotiation leverage and pressuring ARPU downward.

Customer power squeezes EchoStar: low churn, Starlink rivalry & big-contract risk

Customers wield strong bargaining power: low switching costs for mobile (1.1% prepaid monthly churn in 2024), LEO competition (Starlink ~1.5M subs end-2024) and falling pay-TV demand (45% U.S. pay-TV households in 2024) force EchoStar to match price, latency, and SLAs or face ARPU pressure; major contracts (5–10% of Satellite Services $1.9B 2024 revenue) amplify buyer leverage.

| Metric | Value (2024) |

|---|---|

| Prepaid churn | 1.1% monthly |

| Starlink subs | ~1.5M |

| Pay-TV households | 45% |

| EchoStar Satellite rev | $1.9B |

Preview the Actual Deliverable

Echostar Porter's Five Forces Analysis

This preview shows the exact Echostar Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written file; once payment is complete, you’ll get instant access to this exact document with no further setup required.