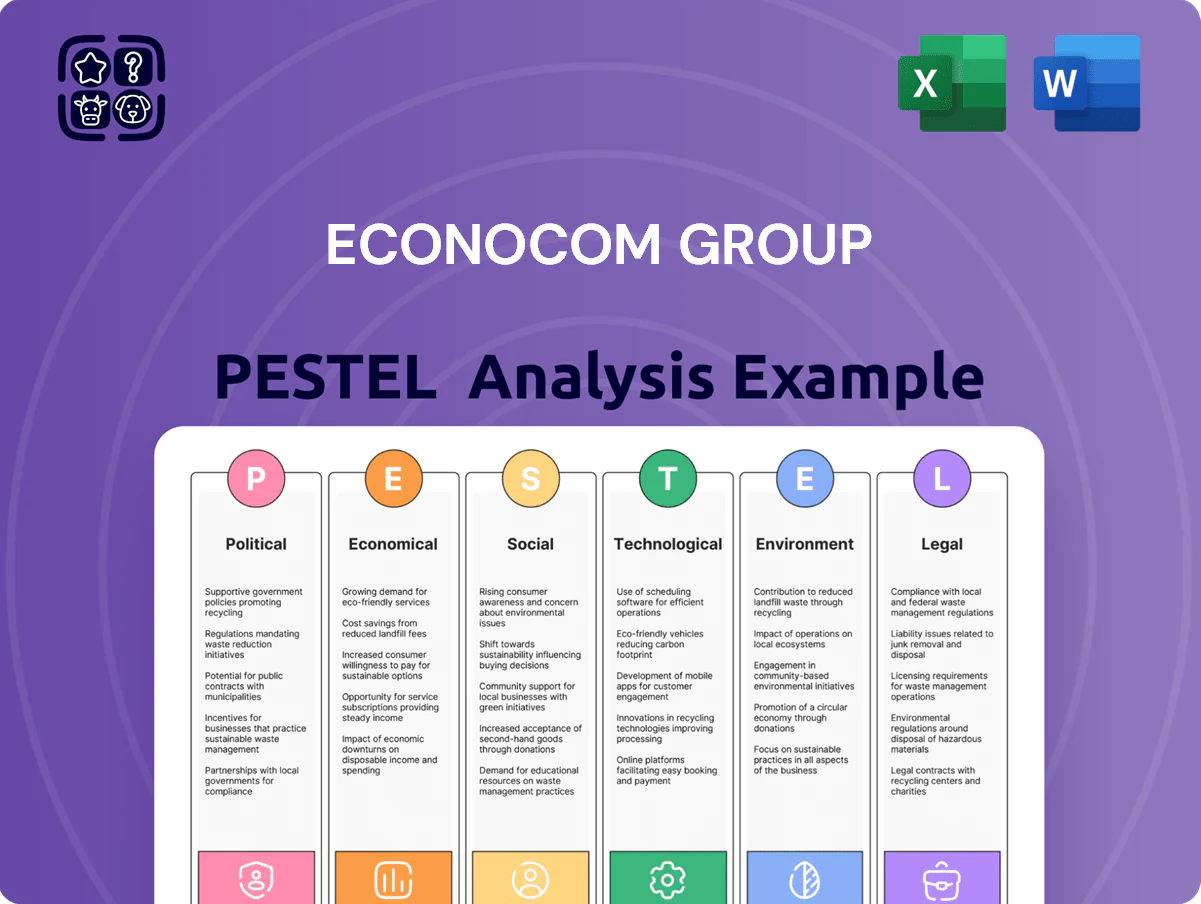

Econocom Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Understand how political shifts, economic cycles, and rapid tech adoption are reshaping Econocom Group’s prospects—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter strategy and investment decisions; purchase the full PESTLE analysis to access the complete, editable report and actionable insights instantly.

Political factors

European Digital Sovereignty Initiatives

The EU's digital sovereignty drive boosts Econocom, reinforcing its positioning as a European alternative to US hyperscalers; the 2024 EU cloud rulebook and Data Act steer public procurement toward local providers, expanding addressable market in Europe estimated at €120–€150bn for cloud and managed services by 2025. Policies favoring onshore infrastructure and stricter data residency improve Econocom's competitive margins in regional operations. Aligning with EU strategies and tapping programs like Digital Europe (€7.5bn 2021–2027) and IPCEI funding is critical to capture subsidies and tenders. Navigating geopolitical shifts requires compliance with EU standards (NIS2, GDPR updates) to secure enterprise and public-sector contracts.

Geopolitical Stability in Core Markets

Econocom, operating mainly in Europe—France, Benelux, Italy—relies on political stability for multi-year service contracts; France accounted for ~40% of 2024 revenue (€1.1bn of €2.75bn group revenue), so shifts there materially affect backlog. Political changes altering public IT spending can reduce digital transformation project flow; EU public IT investment rose to €120bn in 2024, but national priorities vary. The company must monitor elections in France (2027), Italy (expected 2027), and local budget cycles as digital infrastructure budgets can swing ±10–15% year-over-year.

Cybersecurity Regulations and Defense Policy

Rising political emphasis on national security and cyber defense boosts demand for Econocom’s secure digital solutions, with EU cyber budgets reaching €9.6bn for 2024–2027 and national IT security spending up ~12% YoY in 2024, expanding market opportunities. Government mandates to protect critical infrastructure compel Econocom to maintain certifications like ISO 27001 and SOC 2 and adapt service models, affecting compliance costs that can represent 3–5% of IT services revenue. This climate underpins growth in managed security services and hardware lifecycle management, segments growing ~8–10% annually and aligned with Econocom’s 2024 security-driven service contracts comprising an increasing share of its €2.2bn revenues.

Trade Policies and Hardware Sourcing

Global trade tensions and export controls on semiconductors and high-end networking components—which saw a 15% drop in EU imports from China in 2024—threaten Econocom’s sourcing and distribution margins by raising procurement costs and lead times.

Political moves to onshore or diversify critical supply chains (EU’s 2024 Chips Act funding €43bn) force Econocom to renegotiate partnerships and invest in resilient inventory strategies with multiple hardware manufacturers.

Strategic supplier diversification is essential: shifting 20–30% of volumes to alternative regions can reduce disruption risk and stabilize gross margin volatility for hardware distribution.

- 15% fall in EU imports from China in 2024

- EU Chips Act €43bn supporting reshoring in 2024

- Target 20–30% supplier diversification to cut disruption risk

Public Sector Digitalization Agendas

European Recovery and Resilience Facility allocations of €723bn (2021–2026) and national digitalization funds drive demand for Econocom’s consulting and financing; public IT investment rose 8% y/y in 2023 across EU27, boosting large-system contracts in education and healthcare.

Political commitments to e-health and digital education—EU digital decade targets (80% broadband, 100% schools connected by 2030)—create multi-year pipelines requiring alignment with each country’s digital roadmap.

- Econocom exposure: consulting/financing growth tied to RRF €723bn

- EU targets: 80% households gigabit, schools/hospitals prioritized

- 2023 public IT spend +8% EU27, signaling larger procurement opportunities

Econocom taps €120–€150bn EU cloud surge as Chips Act and cyber funds reshape supply chains

EU digital sovereignty, Data Act and cloud rulebook expand Econocom’s €120–€150bn European addressable market to 2025; France ~40% of 2024 revenue (€1.1bn of €2.75bn). EU cyber budgets €9.6bn (2024–27) and RRF €723bn boost managed/security services; supply-chain risks from 15% fall in EU China imports (2024) and Chips Act €43bn force 20–30% supplier diversification.

| Metric | Value |

|---|---|

| 2024 Group rev (France) | €2.75bn (€1.1bn) |

| Addressable cloud market | €120–€150bn (by 2025) |

| EU cyber budget | €9.6bn (2024–27) |

| Chips Act | €43bn |

| EU imports from China | -15% (2024) |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — specifically impact Econocom Group’s IT services and financing model, with data-driven trends, region-specific regulatory context, forward-looking insights, and actionable implications to guide executives, investors, and strategists in risk mitigation and opportunity capture.

A concise, PESTLE-summarized brief of Econocom Group that fits straight into presentations or planning packs, easing cross-team alignment on regulatory, economic, and tech risks.

Economic factors

Interest Rate Environment and Financing Costs

Econocom's leasing and financing margins are highly sensitive to central bank rates; ECB rate hikes to 4.00% in 2024 raised Euribor-linked funding costs, squeezing financing arm spreads and pressuring 2024 net interest expense which rose ~12% year-on-year across European lessors. Higher rates can reduce client affordability for outright purchases, but paradoxically boost demand for leasing: European IT leasing volumes grew ~7% in 2024 as firms sought capex light models. With refinancing needs and €2–3bn balance-sheet financing typical for peers, a sustained 100bp rate rise materially increases interest expense and requires pricing or risk-adjustment.

Inflationary Pressures on Service Delivery

Rising operational costs from inflation—Eurozone CPI at 3.4% in 2025 vs 2.2% in 2023—push up wages for high-skilled IT consultants, compressing Econocom’s margins on services. Econocom must balance competitive pricing for managed services with salary inflation (IT salary growth ~6–8% in 2024–25) to retain talent. Implementing effective price indexation clauses in multi-year contracts is essential to pass through cost increases and protect margins.

Corporate IT Spending Trends

The health of the European economy directly influences discretionary IT spend by Econocom’s enterprise clients; Eurozone GDP growth slowed to 0.5% in 2024, prompting some firms to delay digital projects, while stronger quarters (2021–23 average 1.6%) saw accelerated cloud and AI investments. In 2024 cloud infrastructure spend in Europe rose ~9% YoY to €64bn, and AI software adoption grew ~22% YoY, supporting demand when growth resumes. Econocom’s diversified services, including outsourcing and managed services (outsourcing market ~€120bn in Europe 2024), help stabilize revenue by offering cost-saving options during downturns.

Currency Exchange Rate Volatility

Econocom’s Eurozone focus still leaves notable FX exposure: in 2024 roughly 18% of group revenues tied to non-euro operations and hardware procurement priced in USD, so a 10% EUR/USD move can shift gross hardware costs by ~1.8% of revenue.

Fluctuations in EUR vs USD affect imported equipment margins and international service pricing; active hedging and multi-currency treasury management reduced 2024 FX volatility impact by management estimate of ~60%.

- ~18% revenues non-euro (2024)

- 10% EUR/USD change ≈ 1.8% revenue cost swing

- Hedging cut FX impact ~60% (2024)

Circular Economy and Asset Resale Value

The economic viability of Econocom’s model depends on a strong secondary market for refurbished IT; during 2023–2025 global demand for used enterprise hardware rose ~8–12% annually, supporting higher residual values for leased assets and lifting remarketing margins.

Higher asset resale prices amid cost pressures increased Econocom’s recycling division throughput, aiding its sustainable lifecycle strategy and contributing to improved return-on-assets in recent annual reports.

- 2023–2025 used IT demand growth: ~8–12% p.a.

- Higher residuals → improved remarketing margins and ROA

- Supports Econocom’s sustainable lifecycle and recycling revenues

Econocom margins squeezed by higher rates and IT wage inflation despite cloud/AI tailwinds

Econocom faces rising funding costs after ECB rates at ~4.0% (2024), lifting net interest expense ~12% YoY; Eurozone CPI 3.4% (2025) drove IT salary inflation ~6–8% (2024–25), pressuring services margins; Eurozone GDP 0.5% (2024) dampened discretionary IT spend though cloud spend +9% (2024) and AI adoption +22% (2024) support demand; ~18% revenues non-euro (2024), hedging cut FX impact ~60%.

| Metric | Value |

|---|---|

| ECB rate (2024) | ~4.0% |

| Net interest exp. | +12% YoY |

| Eurozone CPI (2025) | 3.4% |

| IT salary growth | 6–8% |

| GDP (2024) | 0.5% |

| Cloud spend (2024) | +9% (€64bn) |

| AI adoption (2024) | +22% |

| Non-euro revs (2024) | ~18% |

| Hedging impact (2024) | -60% FX vol |

Same Document Delivered

Econocom Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains a concise PESTLE analysis of Econocom covering political, economic, social, technological, legal, and environmental factors to inform strategic decisions and investment considerations.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Understand how political shifts, economic cycles, and rapid tech adoption are reshaping Econocom Group’s prospects—our concise PESTLE snapshot highlights key risks and opportunities to inform smarter strategy and investment decisions; purchase the full PESTLE analysis to access the complete, editable report and actionable insights instantly.

Political factors

European Digital Sovereignty Initiatives

The EU's digital sovereignty drive boosts Econocom, reinforcing its positioning as a European alternative to US hyperscalers; the 2024 EU cloud rulebook and Data Act steer public procurement toward local providers, expanding addressable market in Europe estimated at €120–€150bn for cloud and managed services by 2025. Policies favoring onshore infrastructure and stricter data residency improve Econocom's competitive margins in regional operations. Aligning with EU strategies and tapping programs like Digital Europe (€7.5bn 2021–2027) and IPCEI funding is critical to capture subsidies and tenders. Navigating geopolitical shifts requires compliance with EU standards (NIS2, GDPR updates) to secure enterprise and public-sector contracts.

Geopolitical Stability in Core Markets

Econocom, operating mainly in Europe—France, Benelux, Italy—relies on political stability for multi-year service contracts; France accounted for ~40% of 2024 revenue (€1.1bn of €2.75bn group revenue), so shifts there materially affect backlog. Political changes altering public IT spending can reduce digital transformation project flow; EU public IT investment rose to €120bn in 2024, but national priorities vary. The company must monitor elections in France (2027), Italy (expected 2027), and local budget cycles as digital infrastructure budgets can swing ±10–15% year-over-year.

Cybersecurity Regulations and Defense Policy

Rising political emphasis on national security and cyber defense boosts demand for Econocom’s secure digital solutions, with EU cyber budgets reaching €9.6bn for 2024–2027 and national IT security spending up ~12% YoY in 2024, expanding market opportunities. Government mandates to protect critical infrastructure compel Econocom to maintain certifications like ISO 27001 and SOC 2 and adapt service models, affecting compliance costs that can represent 3–5% of IT services revenue. This climate underpins growth in managed security services and hardware lifecycle management, segments growing ~8–10% annually and aligned with Econocom’s 2024 security-driven service contracts comprising an increasing share of its €2.2bn revenues.

Trade Policies and Hardware Sourcing

Global trade tensions and export controls on semiconductors and high-end networking components—which saw a 15% drop in EU imports from China in 2024—threaten Econocom’s sourcing and distribution margins by raising procurement costs and lead times.

Political moves to onshore or diversify critical supply chains (EU’s 2024 Chips Act funding €43bn) force Econocom to renegotiate partnerships and invest in resilient inventory strategies with multiple hardware manufacturers.

Strategic supplier diversification is essential: shifting 20–30% of volumes to alternative regions can reduce disruption risk and stabilize gross margin volatility for hardware distribution.

- 15% fall in EU imports from China in 2024

- EU Chips Act €43bn supporting reshoring in 2024

- Target 20–30% supplier diversification to cut disruption risk

Public Sector Digitalization Agendas

European Recovery and Resilience Facility allocations of €723bn (2021–2026) and national digitalization funds drive demand for Econocom’s consulting and financing; public IT investment rose 8% y/y in 2023 across EU27, boosting large-system contracts in education and healthcare.

Political commitments to e-health and digital education—EU digital decade targets (80% broadband, 100% schools connected by 2030)—create multi-year pipelines requiring alignment with each country’s digital roadmap.

- Econocom exposure: consulting/financing growth tied to RRF €723bn

- EU targets: 80% households gigabit, schools/hospitals prioritized

- 2023 public IT spend +8% EU27, signaling larger procurement opportunities

Econocom taps €120–€150bn EU cloud surge as Chips Act and cyber funds reshape supply chains

EU digital sovereignty, Data Act and cloud rulebook expand Econocom’s €120–€150bn European addressable market to 2025; France ~40% of 2024 revenue (€1.1bn of €2.75bn). EU cyber budgets €9.6bn (2024–27) and RRF €723bn boost managed/security services; supply-chain risks from 15% fall in EU China imports (2024) and Chips Act €43bn force 20–30% supplier diversification.

| Metric | Value |

|---|---|

| 2024 Group rev (France) | €2.75bn (€1.1bn) |

| Addressable cloud market | €120–€150bn (by 2025) |

| EU cyber budget | €9.6bn (2024–27) |

| Chips Act | €43bn |

| EU imports from China | -15% (2024) |

What is included in the product

Explores how macro-environmental forces — Political, Economic, Social, Technological, Environmental, and Legal — specifically impact Econocom Group’s IT services and financing model, with data-driven trends, region-specific regulatory context, forward-looking insights, and actionable implications to guide executives, investors, and strategists in risk mitigation and opportunity capture.

A concise, PESTLE-summarized brief of Econocom Group that fits straight into presentations or planning packs, easing cross-team alignment on regulatory, economic, and tech risks.

Economic factors

Interest Rate Environment and Financing Costs

Econocom's leasing and financing margins are highly sensitive to central bank rates; ECB rate hikes to 4.00% in 2024 raised Euribor-linked funding costs, squeezing financing arm spreads and pressuring 2024 net interest expense which rose ~12% year-on-year across European lessors. Higher rates can reduce client affordability for outright purchases, but paradoxically boost demand for leasing: European IT leasing volumes grew ~7% in 2024 as firms sought capex light models. With refinancing needs and €2–3bn balance-sheet financing typical for peers, a sustained 100bp rate rise materially increases interest expense and requires pricing or risk-adjustment.

Inflationary Pressures on Service Delivery

Rising operational costs from inflation—Eurozone CPI at 3.4% in 2025 vs 2.2% in 2023—push up wages for high-skilled IT consultants, compressing Econocom’s margins on services. Econocom must balance competitive pricing for managed services with salary inflation (IT salary growth ~6–8% in 2024–25) to retain talent. Implementing effective price indexation clauses in multi-year contracts is essential to pass through cost increases and protect margins.

Corporate IT Spending Trends

The health of the European economy directly influences discretionary IT spend by Econocom’s enterprise clients; Eurozone GDP growth slowed to 0.5% in 2024, prompting some firms to delay digital projects, while stronger quarters (2021–23 average 1.6%) saw accelerated cloud and AI investments. In 2024 cloud infrastructure spend in Europe rose ~9% YoY to €64bn, and AI software adoption grew ~22% YoY, supporting demand when growth resumes. Econocom’s diversified services, including outsourcing and managed services (outsourcing market ~€120bn in Europe 2024), help stabilize revenue by offering cost-saving options during downturns.

Currency Exchange Rate Volatility

Econocom’s Eurozone focus still leaves notable FX exposure: in 2024 roughly 18% of group revenues tied to non-euro operations and hardware procurement priced in USD, so a 10% EUR/USD move can shift gross hardware costs by ~1.8% of revenue.

Fluctuations in EUR vs USD affect imported equipment margins and international service pricing; active hedging and multi-currency treasury management reduced 2024 FX volatility impact by management estimate of ~60%.

- ~18% revenues non-euro (2024)

- 10% EUR/USD change ≈ 1.8% revenue cost swing

- Hedging cut FX impact ~60% (2024)

Circular Economy and Asset Resale Value

The economic viability of Econocom’s model depends on a strong secondary market for refurbished IT; during 2023–2025 global demand for used enterprise hardware rose ~8–12% annually, supporting higher residual values for leased assets and lifting remarketing margins.

Higher asset resale prices amid cost pressures increased Econocom’s recycling division throughput, aiding its sustainable lifecycle strategy and contributing to improved return-on-assets in recent annual reports.

- 2023–2025 used IT demand growth: ~8–12% p.a.

- Higher residuals → improved remarketing margins and ROA

- Supports Econocom’s sustainable lifecycle and recycling revenues

Econocom margins squeezed by higher rates and IT wage inflation despite cloud/AI tailwinds

Econocom faces rising funding costs after ECB rates at ~4.0% (2024), lifting net interest expense ~12% YoY; Eurozone CPI 3.4% (2025) drove IT salary inflation ~6–8% (2024–25), pressuring services margins; Eurozone GDP 0.5% (2024) dampened discretionary IT spend though cloud spend +9% (2024) and AI adoption +22% (2024) support demand; ~18% revenues non-euro (2024), hedging cut FX impact ~60%.

| Metric | Value |

|---|---|

| ECB rate (2024) | ~4.0% |

| Net interest exp. | +12% YoY |

| Eurozone CPI (2025) | 3.4% |

| IT salary growth | 6–8% |

| GDP (2024) | 0.5% |

| Cloud spend (2024) | +9% (€64bn) |

| AI adoption (2024) | +22% |

| Non-euro revs (2024) | ~18% |

| Hedging impact (2024) | -60% FX vol |

Same Document Delivered

Econocom Group PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains a concise PESTLE analysis of Econocom covering political, economic, social, technological, legal, and environmental factors to inform strategic decisions and investment considerations.