EDF Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

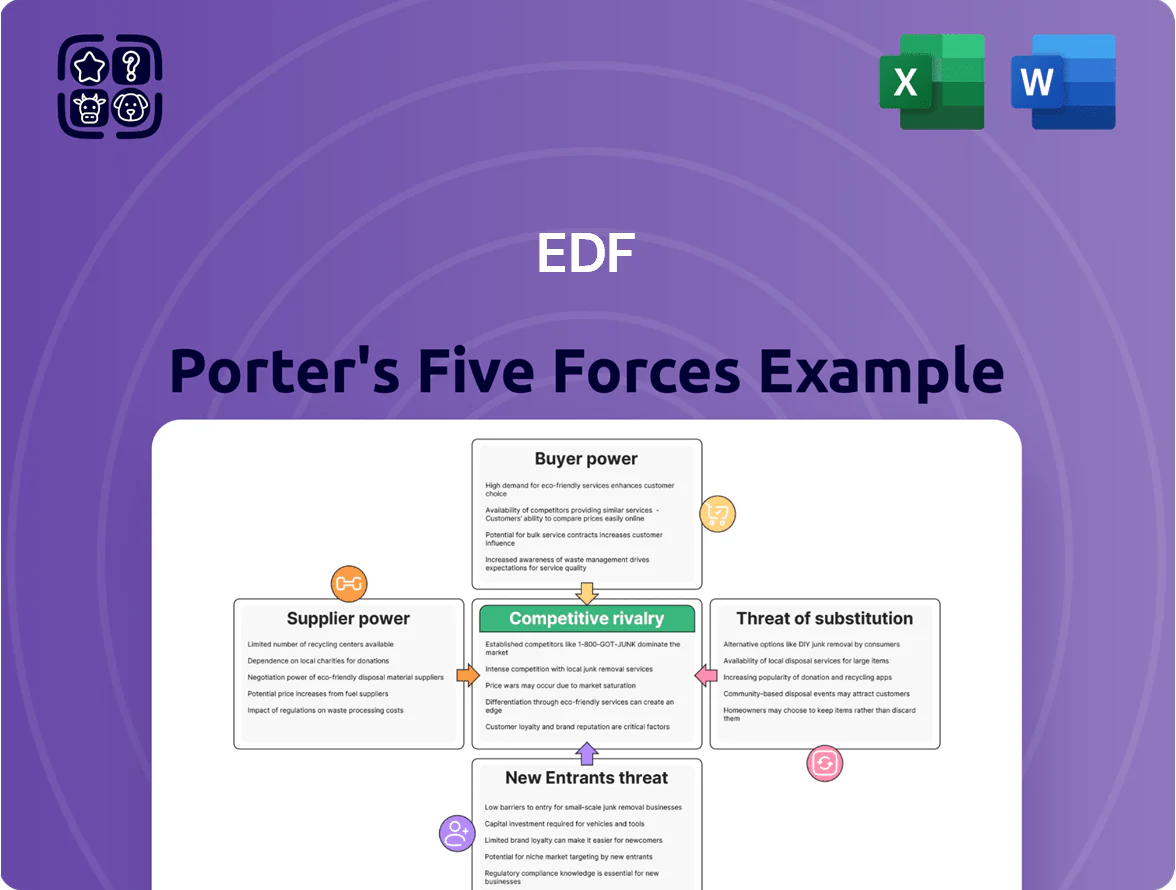

EDF faces complex competitive dynamics—from regulated utility pressures and strong supplier relationships to rising threats from renewables and evolving customer expectations—shaping strategy and margins.

Suppliers Bargaining Power

Nuclear Fuel Chain Concentration

The global nuclear fuel chain is highly concentrated: in 2024 the top five uranium producers (Kazatomprom, Cameco, Orano, Rio Tinto, CNNC) supplied over 70% of mined uranium, and enrichment services are dominated by state-backed firms in Russia, China, and France. EDF, with Europe's largest nuclear fleet (56 GW operational in 2025), depends on imports from Kazakhstan, Canada, and Australia, creating strategic exposure. Long-term contracts cover much demand, but a 2025 supply shock or geopolitical tension could raise fuel costs by an estimated 10–20% and force costly reactor allocation or market purchases.

Specialized Engineering and Technical Expertise

Maintenance and construction of EPR reactors need rare engineering services and components few firms supply; even after EDF fully integrated Framatome (2017 acquisition completed, 2024 revenue for Framatome ~€3.8bn), EDF still depends on third-party vendors for high‑tech sensors and heavy forgings, sourced from ~5 specialized global suppliers, giving these suppliers moderate leverage during life‑extension programs affecting ~56 reactors and €20–30bn capex through 2035.

Labor Union Influence and Specialized Workforce

Volatility in Raw Construction Materials

- Steel +18% (2020–2025)

- Copper +24% (2020–2025)

- Specialized cement +15% (2023)

- CAPEX uncertainty >5%

Fossil Fuel Procurement for Peak Demand

EDF runs gas-fired plants for peak demand and grid stability despite its nuclear base; in 2024 thermal generation accounted for about 15% of EDF Group output, mainly gas peakers.

European gas suppliers hold pricing power in winter—TTF monthly futures spiked to ~€60/MWh in Jan 2024—raising EDF’s fuel costs and compressing margins on thermal units.

EDF must hedge and optimize dispatch to protect profitability while cutting emissions to meet its 2035 decarbonization targets; in 2024 EDF invested ~€1.5bn in gas-to-renewables switching.

- Thermal ≈15% of output (2024)

- TTF winter peak ≈€60/MWh (Jan 2024)

- €1.5bn 2024 investment in gas-to-renewables

Supply bottlenecks, rising wages and tech shortages threaten EDF's nuclear output and costs

Suppliers hold moderate-to-high power: top 5 uranium miners >70% (2024), enrichment dominated by state firms, EDF nuclear fleet 56 GW (2025) relies on imports; specialized reactor parts from ~5 suppliers raise capex risk (€20–30bn to 2035). Labor unions won 6.8% wage rise (2024–25); 22% technician shortfall (2025) inflates wages 12–18% and caused ~4.5 TWh lost/yr (2023–25).

| Metric | Value |

|---|---|

| Uranium top‑5 share (2024) | >70% |

| EDF nuclear capacity (2025) | 56 GW |

| Technician shortfall (2025) | 22% |

| Wage rise (2024–25) | 6.8% |

What is included in the product

Tailored exclusively for EDF, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, barriers to entry, and substitutes, identifying disruptive threats and strategic levers that impact pricing, profitability, and market share.

A concise Porter's Five Forces one-sheet for EDF—quickly spot where competitive pressure hurts margins and prioritize relief strategies like supplier consolidation or regulatory engagement.

Customers Bargaining Power

State-Regulated Retail Tariffs

In France the government sets regulated retail electricity tariffs to protect household purchasing power, capping prices for about 25 million regulated customers; this limits EDF’s ability to pass on higher fuel or operating costs. By end-2025 these caps compress residential margins—EDF reported regulated sales roughly €20–22 billion annually (2024 figures) so even small tariff freezes shave percentage points off EBITDA. What this hides: exposure to volatility in wholesale and nuclear maintenance costs.

Industrial Power Purchase Agreements

Large industrial customers wield strong bargaining power: in 2024 global corporate PPA volume hit ~43 GW, so EDF faces tough negotiation vs buyers who can sign long-term PPAs or switch suppliers; many (top 500 industrials) invest in on-site generation—captive solar/wind or gas—or demand-response to cut costs, lowering average load by ~5–12%. To keep them, EDF must match market PPA rates (often below regional LMPs) and offer bespoke energy-management and financing.

Retail Market Competition and Switching Costs

The liberalization of the EU retail energy market cut switching barriers; EU-wide switching rates hit 12% in 2023 and 14% in France for small customers in 2024, so residential and small-business clients move suppliers easily.

Digital-first challengers use sub-€30 acquisition promos and instant onboarding apps; aggressive pricing pressures average residential tariffs down ~4% Y/Y in 2024, raising churn risk.

EDF must spend more on service and loyalty: EDF Group reported €1.2bn in customer-related OPEX in 2024 and launched retention offers to curb churn, or face continued margin erosion.

Energy Efficiency and Self-Generation Trends

Residential solar and efficiency cut EDF's retail volumes; by 2025 prosumers (households that produce electricity) reduced peak grid draw by about 4–6% in France, and rooftop PV capacity hit ~18 GW (CRE data).

EDF must shift from selling kilowatt-hours to selling grid services, storage, demand response, and subscription models to protect margin as volumetric sales decline.

- Prosumers: ~2.5 million French homes with PV by 2025

- Rooftop PV: ~18 GW installed (2025)

- Volume impact: ~4–6% peak demand reduction

- Strategy: pivot to services, storage, demand-response

Public Service Obligations and Universal Access

As a state-backed utility, EDF must provide universal electricity access, legally restricting customer selection and forcing service to low-profit and remote areas where delivery costs often exceed revenue; in 2024 EDF reported 8% of grid costs attributed to social tariffs and rural subsidies.

These public service obligations convert consumers into indirect powerholders: collective demand influences tariff-setting, regulation, and government support—France’s CRE approved a 2025 residential tariff freeze impacting EDF’s margins by an estimated €900m.

- Mandatory universal service limits customer selectivity

- Service to loss-making areas raises operating costs (8% grid cost, 2024)

- Consumers exert political/regulatory leverage

- 2025 tariff freeze cut EDF margins ~€900m

Regulated caps, rising prosumers and PPAs squeeze EDF margins—pivot to services & storage

Customers hold high bargaining power: regulated residential caps (≈€20–22bn regulated sales, 2024) and a 2025 tariff freeze (~€900m margin hit) limit pass-through; industrials shift to PPAs (~43GW global 2024) or on-site generation, cutting load 5–12%; switching rates rose to 14% (France, 2024); prosumers (~2.5m homes, 18GW PV by 2025) cut peak demand 4–6%, forcing EDF to pivot to services and storage.

| Metric | Value |

|---|---|

| Regulated sales (2024) | €20–22bn |

| 2025 tariff freeze impact | ≈€900m |

| Industrial PPA volume (2024) | ~43GW |

| Rooftop PV (2025) | ~18GW |

| Prosumers (2025) | ~2.5m homes |

What You See Is What You Get

EDF Porter's Five Forces Analysis

This preview shows the exact EDF Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

The document displayed is the same professionally written file available for instant download upon payment, containing complete insights on competitive rivalry, supplier and buyer power, threats of entry and substitution.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

EDF faces complex competitive dynamics—from regulated utility pressures and strong supplier relationships to rising threats from renewables and evolving customer expectations—shaping strategy and margins.

Suppliers Bargaining Power

Nuclear Fuel Chain Concentration

The global nuclear fuel chain is highly concentrated: in 2024 the top five uranium producers (Kazatomprom, Cameco, Orano, Rio Tinto, CNNC) supplied over 70% of mined uranium, and enrichment services are dominated by state-backed firms in Russia, China, and France. EDF, with Europe's largest nuclear fleet (56 GW operational in 2025), depends on imports from Kazakhstan, Canada, and Australia, creating strategic exposure. Long-term contracts cover much demand, but a 2025 supply shock or geopolitical tension could raise fuel costs by an estimated 10–20% and force costly reactor allocation or market purchases.

Specialized Engineering and Technical Expertise

Maintenance and construction of EPR reactors need rare engineering services and components few firms supply; even after EDF fully integrated Framatome (2017 acquisition completed, 2024 revenue for Framatome ~€3.8bn), EDF still depends on third-party vendors for high‑tech sensors and heavy forgings, sourced from ~5 specialized global suppliers, giving these suppliers moderate leverage during life‑extension programs affecting ~56 reactors and €20–30bn capex through 2035.

Labor Union Influence and Specialized Workforce

Volatility in Raw Construction Materials

- Steel +18% (2020–2025)

- Copper +24% (2020–2025)

- Specialized cement +15% (2023)

- CAPEX uncertainty >5%

Fossil Fuel Procurement for Peak Demand

EDF runs gas-fired plants for peak demand and grid stability despite its nuclear base; in 2024 thermal generation accounted for about 15% of EDF Group output, mainly gas peakers.

European gas suppliers hold pricing power in winter—TTF monthly futures spiked to ~€60/MWh in Jan 2024—raising EDF’s fuel costs and compressing margins on thermal units.

EDF must hedge and optimize dispatch to protect profitability while cutting emissions to meet its 2035 decarbonization targets; in 2024 EDF invested ~€1.5bn in gas-to-renewables switching.

- Thermal ≈15% of output (2024)

- TTF winter peak ≈€60/MWh (Jan 2024)

- €1.5bn 2024 investment in gas-to-renewables

Supply bottlenecks, rising wages and tech shortages threaten EDF's nuclear output and costs

Suppliers hold moderate-to-high power: top 5 uranium miners >70% (2024), enrichment dominated by state firms, EDF nuclear fleet 56 GW (2025) relies on imports; specialized reactor parts from ~5 suppliers raise capex risk (€20–30bn to 2035). Labor unions won 6.8% wage rise (2024–25); 22% technician shortfall (2025) inflates wages 12–18% and caused ~4.5 TWh lost/yr (2023–25).

| Metric | Value |

|---|---|

| Uranium top‑5 share (2024) | >70% |

| EDF nuclear capacity (2025) | 56 GW |

| Technician shortfall (2025) | 22% |

| Wage rise (2024–25) | 6.8% |

What is included in the product

Tailored exclusively for EDF, this Porter's Five Forces analysis uncovers key competitive drivers, supplier and buyer power, barriers to entry, and substitutes, identifying disruptive threats and strategic levers that impact pricing, profitability, and market share.

A concise Porter's Five Forces one-sheet for EDF—quickly spot where competitive pressure hurts margins and prioritize relief strategies like supplier consolidation or regulatory engagement.

Customers Bargaining Power

State-Regulated Retail Tariffs

In France the government sets regulated retail electricity tariffs to protect household purchasing power, capping prices for about 25 million regulated customers; this limits EDF’s ability to pass on higher fuel or operating costs. By end-2025 these caps compress residential margins—EDF reported regulated sales roughly €20–22 billion annually (2024 figures) so even small tariff freezes shave percentage points off EBITDA. What this hides: exposure to volatility in wholesale and nuclear maintenance costs.

Industrial Power Purchase Agreements

Large industrial customers wield strong bargaining power: in 2024 global corporate PPA volume hit ~43 GW, so EDF faces tough negotiation vs buyers who can sign long-term PPAs or switch suppliers; many (top 500 industrials) invest in on-site generation—captive solar/wind or gas—or demand-response to cut costs, lowering average load by ~5–12%. To keep them, EDF must match market PPA rates (often below regional LMPs) and offer bespoke energy-management and financing.

Retail Market Competition and Switching Costs

The liberalization of the EU retail energy market cut switching barriers; EU-wide switching rates hit 12% in 2023 and 14% in France for small customers in 2024, so residential and small-business clients move suppliers easily.

Digital-first challengers use sub-€30 acquisition promos and instant onboarding apps; aggressive pricing pressures average residential tariffs down ~4% Y/Y in 2024, raising churn risk.

EDF must spend more on service and loyalty: EDF Group reported €1.2bn in customer-related OPEX in 2024 and launched retention offers to curb churn, or face continued margin erosion.

Energy Efficiency and Self-Generation Trends

Residential solar and efficiency cut EDF's retail volumes; by 2025 prosumers (households that produce electricity) reduced peak grid draw by about 4–6% in France, and rooftop PV capacity hit ~18 GW (CRE data).

EDF must shift from selling kilowatt-hours to selling grid services, storage, demand response, and subscription models to protect margin as volumetric sales decline.

- Prosumers: ~2.5 million French homes with PV by 2025

- Rooftop PV: ~18 GW installed (2025)

- Volume impact: ~4–6% peak demand reduction

- Strategy: pivot to services, storage, demand-response

Public Service Obligations and Universal Access

As a state-backed utility, EDF must provide universal electricity access, legally restricting customer selection and forcing service to low-profit and remote areas where delivery costs often exceed revenue; in 2024 EDF reported 8% of grid costs attributed to social tariffs and rural subsidies.

These public service obligations convert consumers into indirect powerholders: collective demand influences tariff-setting, regulation, and government support—France’s CRE approved a 2025 residential tariff freeze impacting EDF’s margins by an estimated €900m.

- Mandatory universal service limits customer selectivity

- Service to loss-making areas raises operating costs (8% grid cost, 2024)

- Consumers exert political/regulatory leverage

- 2025 tariff freeze cut EDF margins ~€900m

Regulated caps, rising prosumers and PPAs squeeze EDF margins—pivot to services & storage

Customers hold high bargaining power: regulated residential caps (≈€20–22bn regulated sales, 2024) and a 2025 tariff freeze (~€900m margin hit) limit pass-through; industrials shift to PPAs (~43GW global 2024) or on-site generation, cutting load 5–12%; switching rates rose to 14% (France, 2024); prosumers (~2.5m homes, 18GW PV by 2025) cut peak demand 4–6%, forcing EDF to pivot to services and storage.

| Metric | Value |

|---|---|

| Regulated sales (2024) | €20–22bn |

| 2025 tariff freeze impact | ≈€900m |

| Industrial PPA volume (2024) | ~43GW |

| Rooftop PV (2025) | ~18GW |

| Prosumers (2025) | ~2.5m homes |

What You See Is What You Get

EDF Porter's Five Forces Analysis

This preview shows the exact EDF Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

The document displayed is the same professionally written file available for instant download upon payment, containing complete insights on competitive rivalry, supplier and buyer power, threats of entry and substitution.