EDF PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unpack the external forces reshaping EDF with our concise PESTLE Analysis—covering regulatory shifts, market dynamics, and technological trends that affect strategy and valuation; buy the full report to access actionable insights, ready-made charts, and editable files for immediate use.

Political factors

Full State Ownership and Strategic Alignment

Following France's 2023 nationalization, EDF functions as a direct tool of state energy policy, enabling multidecade planning and supporting its €55–100 billion 2030–2050 investment needs for nuclear refurbishment and renewables without short-term shareholder pressure.

State ownership facilitates alignment with France's target of 50% low-carbon electricity by 2035 and supports agreements like the 2024 regulated tariff interventions.

Conversely, EDF faces political interference risks: government decisions on pricing and executive appointments have intensified around electoral cycles, constraining commercial autonomy and potentially affecting credit metrics despite a 2024 state guarantee program.

Nuclear Renaissance Program Implementation

The French government’s commitment to build at least six EPR2 reactors through 2050 signals a decisive political shift toward nuclear reliance, giving EDF a state-backed mandate for a ~€50–€70 billion multi-decade expansion program (government estimates and EDF capex plans through 2035).

State support includes direct financing, regulated asset base (RAB) frameworks and potential equity injections, reducing financing costs for projects forecasted to add ~14–20 GW by 2050.

Political stability is critical: changes in government could alter timelines or funding; continuity across administrations has kept project delivery on track since the 2022 policy revamp.

European Union Market Design Reforms

Geopolitical Energy Security and Uranium Sourcing

Geopolitical tensions have pushed EDF to diversify nuclear fuel supply chains away from volatile regions, reducing reliance on Kazakhstan (which supplied about 41% of global uranium production in 2024) and Russia; EDF increased non-Russian procurement and domestic processing contracts to safeguard French energy sovereignty.

EDF now manages diplomatic relationships across Africa and Central Asia to secure uranium, signing deals that target multi-year contracts covering an estimated 30–40% of its fuel needs and coordinating with France’s strategic reserves.

Strategic stockpiling and international partnerships are prioritized: France’s uranium stockpile rose toward covering roughly 2–3 years of reactor needs by 2025, while EDF pursues joint ventures and long-term offtakes to mitigate supply disruptions from conflicts.

- Reduced reliance on Russia/Kazakhstan; diversified suppliers

- Multi-year contracts covering ~30–40% of EDF’s fuel needs

- National stockpile ~2–3 years of reactor fuel (by 2025)

- Increased joint ventures and long-term offtake agreements

Cross-Border Infrastructure and UK Relations

EDF is central to UK nuclear capacity via Hinkley Point C (project cost ~£25–30bn) and planned Sizewell C; UK political and regulatory shifts—seen in 2024 debates over subsidy models and the 2025 energy security white paper—directly affect project licences and timelines.

Strong Franco‑British relations and stable UK policy are essential: delays or subsidy cuts would increase EDF’s reported net debt (EDF Group net debt ~€43.5bn in 2024) and capital expenditure risk.

Changes in UK stance on state support or energy strategy materially affect EDF’s international balance sheet and cashflow forecasts for decades.

- Hinkley Point C cost ~£25–30bn; Sizewell C funding uncertainty

- EDF net debt ~€43.5bn (2024)

- UK subsidy/policy shifts in 2024–25 raise timeline and financing risk

EDF’s state‑backed €55–100bn green push: political risks, EU reform & fuel security

State ownership anchors EDF’s €55–100bn 2030–2050 capex plan and enables RAB/equity support, aligning with France’s 50% low‑carbon by 2035 goal while exposing EDF to political pricing, appointment and subsidy risk; EU market reforms (end‑2025) may cut baseload margins ~15% and cost EBITDA low‑hundreds EURm/yr; uranium diversification reduced Russian/Kazakh reliance, with stockpile ~2–3 years and multi‑year contracts covering ~30–40% of needs.

| Metric | Value |

|---|---|

| EDF net debt (2024) | €43.5bn |

| 2030–2050 capex | €55–100bn |

| France low‑carbon target | 50% by 2035 |

| Nuclear output | ~380 TWh/yr |

| Uranium stockpile (2025) | ~2–3 years |

| Fuel contracts | 30–40% multi‑year |

What is included in the product

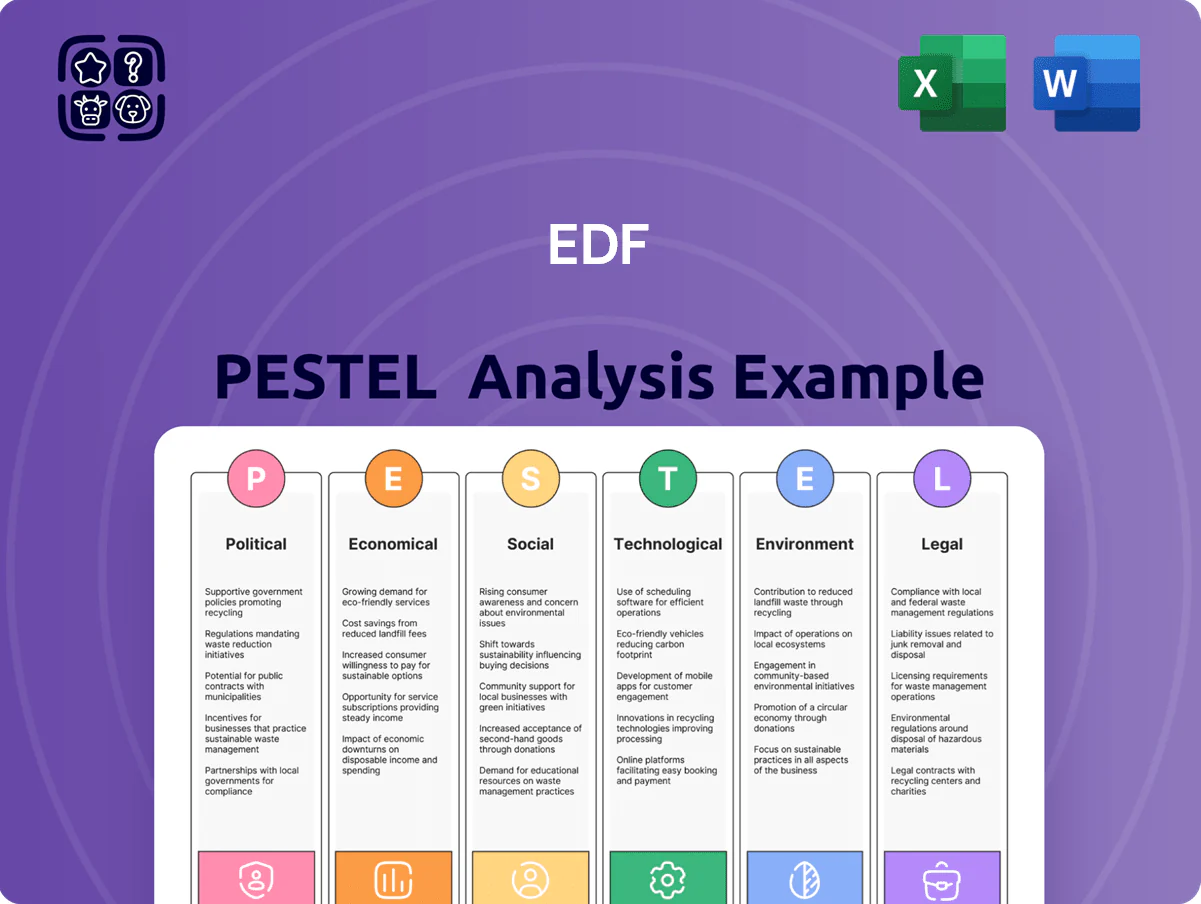

Explores how external macro-environmental factors uniquely affect EDF across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by relevant data and trends to highlight threats and opportunities for executives, consultants, and entrepreneurs.

Condenses EDF's full PESTLE into a clean, shareable summary that highlights key political, regulatory, economic, technological, social, and environmental risks for quick alignment in meetings or strategy decks.

Economic factors

Financing the Grand Carenage and New Builds

EDF faces a roughly €60–€100 billion tab to complete the Grand Carénage life-extension programme and build initial EPR2 units, with 2024 estimates centering near €80 billion for reactors and upgrades through 2050.

The group depends heavily on state-guaranteed loans and financing vehicles such as EDF Invest and Nuclear NewCo, with France committing guarantees exceeding €50 billion by 2025 to de-risk projects.

Economic viability hinges on negotiated strike prices or regulated tariffs: EDF targets returns that cover long-run levelized costs near €60–€80/MWh for new nuclear capacity under current modelling.

Debt Management and Credit Ratings

Despite majority state ownership, EDF carried net debt of about 46.6 billion euros at end-2024, requiring disciplined management to preserve investment-grade ratings from S&P (A-/stable) and Moody’s (Baa1/positive).

Higher euro-area policy rates in 2023–2024 pushed EDF’s average cost of debt upward, tightening free cash flow and increasing 2024 net finance costs versus prior years.

EDF’s financial plan prioritises deleveraging via asset disposals (targeting several billion euros) and readiness for state-backed capital injections, as evidenced by prior 2022–2024 recapitalisation support commitments.

Revenue Impact of New Price Regulation

The ARENH expiry led to a 2024–25 pricing framework tying nuclear tariffs to a regulated contract and a cost-recovery mechanism; regulators set a baseline price near €70/MWh while allowing top-ups linked to capital expenditure, aiming to cap consumer volatility and let EDF recoup rising EPR costs—EDF reported guidance in 2025 expecting regulated nuclear revenues to stabilize ~€36–40bn annually, supporting EBITDA margin recovery to ~30% if realized.

Inflationary Pressures on Construction Costs

- Raw material inflation +20% (2021–2023)

- Skilled labor premiums ≈+15% (2022–2024)

- EDF hedges 60–80% of inputs via long-term contracts

- High overrun risk on flagship nuclear sites

Wholesale Market Volatility and Hedging

Fluctuations in European wholesale power prices remain significant, with day-ahead averages in 2024 near €110/MWh in Western Europe versus €60–80/MWh historically, pressuring EDF’s merchant sales and trading desk results.

EDF uses forward contracts, power purchase agreements and options to hedge exposure, reducing volatility risk—hedges covered roughly 60–80% of 2025 volumes per company guidance.

Economic performance hinges on accurate demand forecasting and optimizing dispatch across nuclear, hydro and thermal assets to capture spreads and manage imbalance costs.

- 2024 day-ahead avg ≈ €110/MWh in Western Europe

- Hedge coverage ~60–80% of 2025 volumes

- Revenue sensitivity tied to generation mix and forecast accuracy

EDF faces €80bn capex, €47bn debt with LCOC €60–80 vs 2024 prices ≈€110/MWh

EDF faces ~€80bn capex to 2050 for Grand Carénage and EPR2; net debt €46.6bn end-2024; state guarantees >€50bn by 2025; target LCOC €60–80/MWh; 2024 day-ahead ≈€110/MWh; hedge coverage ~60–80% of 2025 volumes; raw material +20% (2021–23); skilled labor +15% (2022–24).

| Metric | Value |

|---|---|

| Capex to 2050 | ~€80bn |

| Net debt (2024) | €46.6bn |

| State guarantees | >€50bn |

| LCOC | €60–80/MWh |

| Day-ahead (2024) | ≈€110/MWh |

| Hedge coverage | 60–80% |

Preview Before You Purchase

EDF PESTLE Analysis

The preview shown here is the exact EDF PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are identical to the downloadable file delivered immediately after payment. No placeholders or teasers—this is the final, professionally structured report. What you see is what you’ll own and apply right away.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unpack the external forces reshaping EDF with our concise PESTLE Analysis—covering regulatory shifts, market dynamics, and technological trends that affect strategy and valuation; buy the full report to access actionable insights, ready-made charts, and editable files for immediate use.

Political factors

Full State Ownership and Strategic Alignment

Following France's 2023 nationalization, EDF functions as a direct tool of state energy policy, enabling multidecade planning and supporting its €55–100 billion 2030–2050 investment needs for nuclear refurbishment and renewables without short-term shareholder pressure.

State ownership facilitates alignment with France's target of 50% low-carbon electricity by 2035 and supports agreements like the 2024 regulated tariff interventions.

Conversely, EDF faces political interference risks: government decisions on pricing and executive appointments have intensified around electoral cycles, constraining commercial autonomy and potentially affecting credit metrics despite a 2024 state guarantee program.

Nuclear Renaissance Program Implementation

The French government’s commitment to build at least six EPR2 reactors through 2050 signals a decisive political shift toward nuclear reliance, giving EDF a state-backed mandate for a ~€50–€70 billion multi-decade expansion program (government estimates and EDF capex plans through 2035).

State support includes direct financing, regulated asset base (RAB) frameworks and potential equity injections, reducing financing costs for projects forecasted to add ~14–20 GW by 2050.

Political stability is critical: changes in government could alter timelines or funding; continuity across administrations has kept project delivery on track since the 2022 policy revamp.

European Union Market Design Reforms

Geopolitical Energy Security and Uranium Sourcing

Geopolitical tensions have pushed EDF to diversify nuclear fuel supply chains away from volatile regions, reducing reliance on Kazakhstan (which supplied about 41% of global uranium production in 2024) and Russia; EDF increased non-Russian procurement and domestic processing contracts to safeguard French energy sovereignty.

EDF now manages diplomatic relationships across Africa and Central Asia to secure uranium, signing deals that target multi-year contracts covering an estimated 30–40% of its fuel needs and coordinating with France’s strategic reserves.

Strategic stockpiling and international partnerships are prioritized: France’s uranium stockpile rose toward covering roughly 2–3 years of reactor needs by 2025, while EDF pursues joint ventures and long-term offtakes to mitigate supply disruptions from conflicts.

- Reduced reliance on Russia/Kazakhstan; diversified suppliers

- Multi-year contracts covering ~30–40% of EDF’s fuel needs

- National stockpile ~2–3 years of reactor fuel (by 2025)

- Increased joint ventures and long-term offtake agreements

Cross-Border Infrastructure and UK Relations

EDF is central to UK nuclear capacity via Hinkley Point C (project cost ~£25–30bn) and planned Sizewell C; UK political and regulatory shifts—seen in 2024 debates over subsidy models and the 2025 energy security white paper—directly affect project licences and timelines.

Strong Franco‑British relations and stable UK policy are essential: delays or subsidy cuts would increase EDF’s reported net debt (EDF Group net debt ~€43.5bn in 2024) and capital expenditure risk.

Changes in UK stance on state support or energy strategy materially affect EDF’s international balance sheet and cashflow forecasts for decades.

- Hinkley Point C cost ~£25–30bn; Sizewell C funding uncertainty

- EDF net debt ~€43.5bn (2024)

- UK subsidy/policy shifts in 2024–25 raise timeline and financing risk

EDF’s state‑backed €55–100bn green push: political risks, EU reform & fuel security

State ownership anchors EDF’s €55–100bn 2030–2050 capex plan and enables RAB/equity support, aligning with France’s 50% low‑carbon by 2035 goal while exposing EDF to political pricing, appointment and subsidy risk; EU market reforms (end‑2025) may cut baseload margins ~15% and cost EBITDA low‑hundreds EURm/yr; uranium diversification reduced Russian/Kazakh reliance, with stockpile ~2–3 years and multi‑year contracts covering ~30–40% of needs.

| Metric | Value |

|---|---|

| EDF net debt (2024) | €43.5bn |

| 2030–2050 capex | €55–100bn |

| France low‑carbon target | 50% by 2035 |

| Nuclear output | ~380 TWh/yr |

| Uranium stockpile (2025) | ~2–3 years |

| Fuel contracts | 30–40% multi‑year |

What is included in the product

Explores how external macro-environmental factors uniquely affect EDF across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by relevant data and trends to highlight threats and opportunities for executives, consultants, and entrepreneurs.

Condenses EDF's full PESTLE into a clean, shareable summary that highlights key political, regulatory, economic, technological, social, and environmental risks for quick alignment in meetings or strategy decks.

Economic factors

Financing the Grand Carenage and New Builds

EDF faces a roughly €60–€100 billion tab to complete the Grand Carénage life-extension programme and build initial EPR2 units, with 2024 estimates centering near €80 billion for reactors and upgrades through 2050.

The group depends heavily on state-guaranteed loans and financing vehicles such as EDF Invest and Nuclear NewCo, with France committing guarantees exceeding €50 billion by 2025 to de-risk projects.

Economic viability hinges on negotiated strike prices or regulated tariffs: EDF targets returns that cover long-run levelized costs near €60–€80/MWh for new nuclear capacity under current modelling.

Debt Management and Credit Ratings

Despite majority state ownership, EDF carried net debt of about 46.6 billion euros at end-2024, requiring disciplined management to preserve investment-grade ratings from S&P (A-/stable) and Moody’s (Baa1/positive).

Higher euro-area policy rates in 2023–2024 pushed EDF’s average cost of debt upward, tightening free cash flow and increasing 2024 net finance costs versus prior years.

EDF’s financial plan prioritises deleveraging via asset disposals (targeting several billion euros) and readiness for state-backed capital injections, as evidenced by prior 2022–2024 recapitalisation support commitments.

Revenue Impact of New Price Regulation

The ARENH expiry led to a 2024–25 pricing framework tying nuclear tariffs to a regulated contract and a cost-recovery mechanism; regulators set a baseline price near €70/MWh while allowing top-ups linked to capital expenditure, aiming to cap consumer volatility and let EDF recoup rising EPR costs—EDF reported guidance in 2025 expecting regulated nuclear revenues to stabilize ~€36–40bn annually, supporting EBITDA margin recovery to ~30% if realized.

Inflationary Pressures on Construction Costs

- Raw material inflation +20% (2021–2023)

- Skilled labor premiums ≈+15% (2022–2024)

- EDF hedges 60–80% of inputs via long-term contracts

- High overrun risk on flagship nuclear sites

Wholesale Market Volatility and Hedging

Fluctuations in European wholesale power prices remain significant, with day-ahead averages in 2024 near €110/MWh in Western Europe versus €60–80/MWh historically, pressuring EDF’s merchant sales and trading desk results.

EDF uses forward contracts, power purchase agreements and options to hedge exposure, reducing volatility risk—hedges covered roughly 60–80% of 2025 volumes per company guidance.

Economic performance hinges on accurate demand forecasting and optimizing dispatch across nuclear, hydro and thermal assets to capture spreads and manage imbalance costs.

- 2024 day-ahead avg ≈ €110/MWh in Western Europe

- Hedge coverage ~60–80% of 2025 volumes

- Revenue sensitivity tied to generation mix and forecast accuracy

EDF faces €80bn capex, €47bn debt with LCOC €60–80 vs 2024 prices ≈€110/MWh

EDF faces ~€80bn capex to 2050 for Grand Carénage and EPR2; net debt €46.6bn end-2024; state guarantees >€50bn by 2025; target LCOC €60–80/MWh; 2024 day-ahead ≈€110/MWh; hedge coverage ~60–80% of 2025 volumes; raw material +20% (2021–23); skilled labor +15% (2022–24).

| Metric | Value |

|---|---|

| Capex to 2050 | ~€80bn |

| Net debt (2024) | €46.6bn |

| State guarantees | >€50bn |

| LCOC | €60–80/MWh |

| Day-ahead (2024) | ≈€110/MWh |

| Hedge coverage | 60–80% |

Preview Before You Purchase

EDF PESTLE Analysis

The preview shown here is the exact EDF PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, layout, and structure visible are identical to the downloadable file delivered immediately after payment. No placeholders or teasers—this is the final, professionally structured report. What you see is what you’ll own and apply right away.