Edgewise Therapeutics Porter's Five Forces Analysis

Don't Miss the Bigger Picture

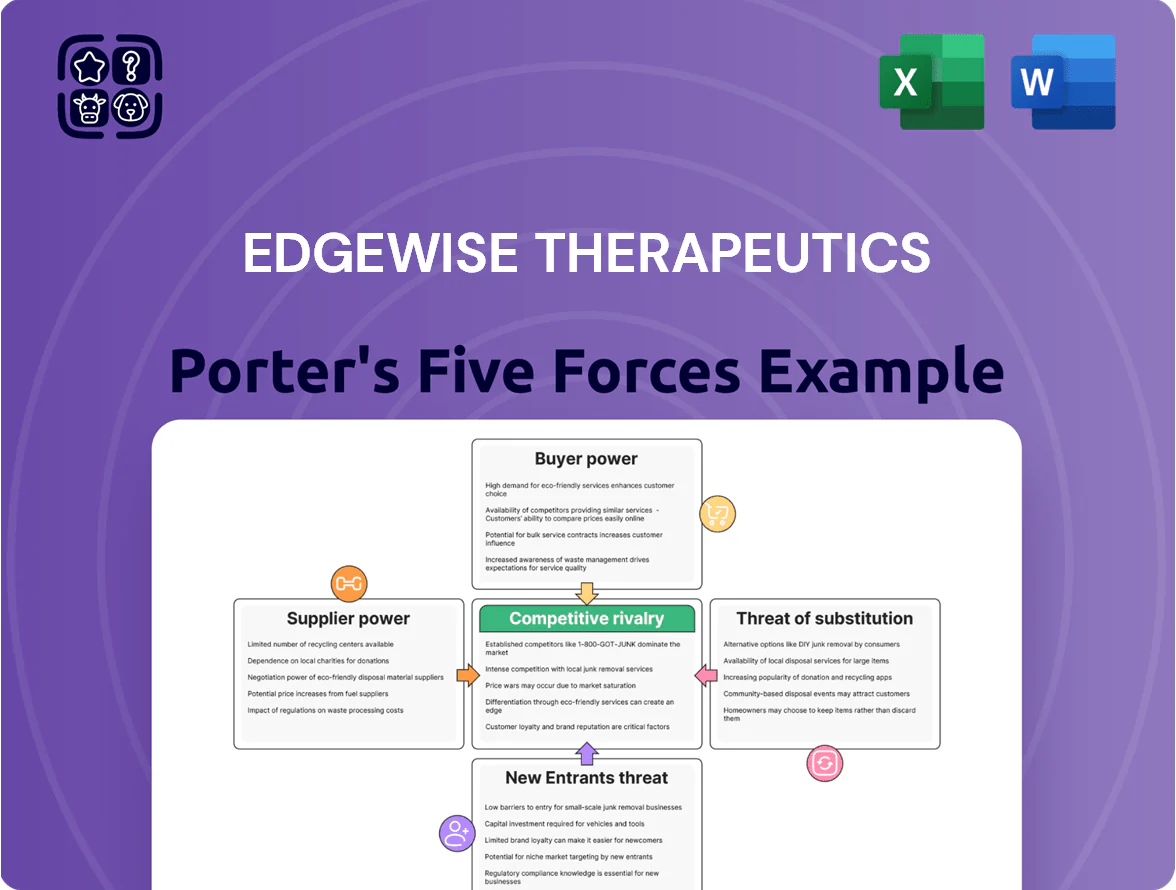

Edgewise Therapeutics faces moderate buyer power, high regulatory barriers, and intense substitute threats from established neuromuscular and neuropathic pain treatments, while supplier leverage and rivalry among biotech peers shape its strategic posture.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Edgewise Therapeutics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Contract Manufacturing Organizations

Edgewise Therapeutics depends on specialized contract manufacturing organizations (CMOs) for complex small molecules like sevasemten; as of late 2025 only about 30–40 global facilities meet stringent GMP standards for orphan drugs, giving CMOs strong leverage to demand premium pricing and priority slotting—industry surveys show CMO day rates up ~18% since 2022—so supply constraints can delay timelines and raise COGS significantly.

Highly Skilled Scientific Talent

The biotech sector has a persistent shortage of specialists for rare muscle diseases like Duchenne (DMD) and Becker (BMD); NIH data shows ~40% of rare-disease clinical roles remain hard-to-fill in 2024, boosting supplier power.

These experts hold outsized leverage because their know-how is critical for complex trials and FDA/EMA filings; losing one lead clinician can delay programs by 6–12 months.

Edgewise must offer competitive pay and equity—market median total comp for senior rare-disease scientists was $280k–$420k in 2025—to retain talent through 2026.

Clinical Research Organization Dependency

Conducting global rare-disease trials needs specialized Clinical Research Organizations (CROs) that supply site networks, patient registries, and regulatory-grade data systems; in 2024 top CROs captured ~46% of biotech outsourced R&D spend, concentrating power.

CROs control trial logistics and data management critical for FDA and EMA milestones, and median cost to replace a CRO mid-study exceeds $5–10M plus 6–12 months delay, so switching is rarely viable.

This lock-in gives CROs high bargaining power over Edgewise Therapeutics, raising contract pricing and milestone-risk exposure during its clinical-stage programs.

Proprietary Research Equipment and Reagents

Proprietary lab instruments and ultra-pure reagents are critical for Edgewise Therapeutics’ oral small-molecule programs; top suppliers like Thermo Fisher Scientific and Merck hold patents and exclusive lines that limit substitution.

In 2025, specialized reagent lead times averaged 12–20 weeks and single-vendor dependency raised R&D delay risk; a supply interruption could push 2026 milestones by quarters and raise costs by an estimated 8–15%.

- High supplier concentration: few patent holders

- Lead times 12–20 weeks (2025 data)

- Potential 8–15% R&D cost increase if disrupted

- Delays could shift 2026 timelines by multiple quarters

Intellectual Property and Licensing Partners

Edgewise often licenses foundational chemistries from universities or biotechs; these licensors set royalty rates and milestone structures that can take 5–15% of net sales and $1m–$50m in development milestones, directly squeezing long‑term margins as Edgewise nears commercialization in rare diseases.

Keeping strong IP partnerships is critical: renegotiation risks, exclusivity terms, and sublicense rights affect launch timing, valuation, and investor returns—royalties can lower peak free cash flow by millions annually.

- Typical royalty range: 5–15% of net sales

- Common milestones: $1m–$50m per program

- Impact: reduces peak FCF and valuation multiples

Supplier squeeze: limited GMP CMOs, rising rates, long lead times, high CRO costs

Suppliers hold high bargaining power: few GMP CMOs (30–40 global), CMO day rates +18% since 2022, reagent lead times 12–20 weeks, CROs captured ~46% of outsourced R&D spend (2024), replacing a CRO costs $5–10M +6–12 months, typical royalties 5–15% of net sales, potential R&D cost uplift 8–15% if disrupted.

| Metric | 2024–25 Data |

|---|---|

| GMP CMOs | 30–40 |

| CMO rate change | +18% |

| Reagent lead time | 12–20 wks |

| CRO market share | 46% |

| CRO switch cost | $5–10M,+6–12m |

| Royalties | 5–15% |

| R&D cost risk | +8–15% |

What is included in the product

Tailored exclusively for Edgewise Therapeutics, this Porter's Five Forces overview uncovers competitive drivers, customer and supplier power, entry barriers, substitutes, and emerging threats shaping its market position and strategic options.

A concise Porter's Five Forces snapshot for Edgewise Therapeutics—ideal for rapid strategic decisions and slide-ready use in meetings.

Customers Bargaining Power

Concentration of Third Party Payers

Government Healthcare Reimbursement Policies

Government programs like Medicare and Medicaid act as pivotal customers, setting benchmark prices and reimbursement that influence private payers; Medicare Part B/Part D and Medicaid account for roughly 40% of US prescription spending as of 2024. Recent legislation through 2024–2025 introduced Medicare drug price negotiations for top-spend drugs and inflation rebates, which could cap Edgewise Therapeutics’ revenue for high-cost therapies. If Edgewise fails to secure favorable reimbursement codes or add-on payments, patient access and market penetration may be sharply limited, cutting potential peak sales by an estimated 20–40% in modeled scenarios.

Influence of Patient Advocacy Groups

Pharmacy Benefit Manager Formulary Control

Pharmacy Benefit Managers (PBMs) decide which drugs sit on preferred formularies for ~200 million insured US lives, so excluding sevasemten or placing it in a high-cost tier could cut Edgewise’s addressable market dramatically.

Securing preferred placement is critical as sevasemten nears launch; PBM-negotiated rebates often exceed 20–40% for specialty drugs, directly reducing net price and revenue.

Without formulary access, commercial uptake, prescribing rates, and peak sales forecasts (tens to hundreds of millions annually) would be materially impaired.

- PBMs control formulary access for ~200M US lives

- Typical specialty rebates: 20–40%

- Formulary exclusion = major hit to peak sales

- Favorable placement required for sevasemten launch

Limited Orphan Disease Patient Pool

Limited patient pools for Duchenne (DMD) and Becker (BMD)—prevalence ~1 in 3,600–6,000 male births for DMD and lower for BMD—mean losing a few percent of patients to competitors can cut revenue sharply; a 5% share shift in a 10,000-patient addressable market equals 500 patients and large revenue swings for Edgewise.

Scarcity increases collective buyer power: payers, advocacy groups, and centers of excellence can steer treatment choice, so Edgewise must show superior safety and efficacy in trials and real-world data to win and keep this concentrated cohort.

- Addressable market ~8,000–12,000 patients (US+EU).

- 5% loss ≈ 400–600 patients—material revenue impact.

- Decisions influenced by centers of excellence and payers.

Payers squeeze Edgewise: 20–40%+ rebates, $100–150k/QALY caps threaten 400–600 patients

| Metric | Value |

|---|---|

| Rebates (specialty) | 20–40% |

| ICER thresholds | $100–150k/QALY |

| Addressable patients | 8,000–12,000 |

| 5% share shift | 400–600 patients |

What You See Is What You Get

Edgewise Therapeutics Porter's Five Forces Analysis

This preview shows the exact Edgewise Therapeutics Porter’s Five Forces analysis you’ll receive immediately after purchase—no mockups or placeholders; the final, fully formatted document is ready for instant download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Edgewise Therapeutics faces moderate buyer power, high regulatory barriers, and intense substitute threats from established neuromuscular and neuropathic pain treatments, while supplier leverage and rivalry among biotech peers shape its strategic posture.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Edgewise Therapeutics’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Contract Manufacturing Organizations

Edgewise Therapeutics depends on specialized contract manufacturing organizations (CMOs) for complex small molecules like sevasemten; as of late 2025 only about 30–40 global facilities meet stringent GMP standards for orphan drugs, giving CMOs strong leverage to demand premium pricing and priority slotting—industry surveys show CMO day rates up ~18% since 2022—so supply constraints can delay timelines and raise COGS significantly.

Highly Skilled Scientific Talent

The biotech sector has a persistent shortage of specialists for rare muscle diseases like Duchenne (DMD) and Becker (BMD); NIH data shows ~40% of rare-disease clinical roles remain hard-to-fill in 2024, boosting supplier power.

These experts hold outsized leverage because their know-how is critical for complex trials and FDA/EMA filings; losing one lead clinician can delay programs by 6–12 months.

Edgewise must offer competitive pay and equity—market median total comp for senior rare-disease scientists was $280k–$420k in 2025—to retain talent through 2026.

Clinical Research Organization Dependency

Conducting global rare-disease trials needs specialized Clinical Research Organizations (CROs) that supply site networks, patient registries, and regulatory-grade data systems; in 2024 top CROs captured ~46% of biotech outsourced R&D spend, concentrating power.

CROs control trial logistics and data management critical for FDA and EMA milestones, and median cost to replace a CRO mid-study exceeds $5–10M plus 6–12 months delay, so switching is rarely viable.

This lock-in gives CROs high bargaining power over Edgewise Therapeutics, raising contract pricing and milestone-risk exposure during its clinical-stage programs.

Proprietary Research Equipment and Reagents

Proprietary lab instruments and ultra-pure reagents are critical for Edgewise Therapeutics’ oral small-molecule programs; top suppliers like Thermo Fisher Scientific and Merck hold patents and exclusive lines that limit substitution.

In 2025, specialized reagent lead times averaged 12–20 weeks and single-vendor dependency raised R&D delay risk; a supply interruption could push 2026 milestones by quarters and raise costs by an estimated 8–15%.

- High supplier concentration: few patent holders

- Lead times 12–20 weeks (2025 data)

- Potential 8–15% R&D cost increase if disrupted

- Delays could shift 2026 timelines by multiple quarters

Intellectual Property and Licensing Partners

Edgewise often licenses foundational chemistries from universities or biotechs; these licensors set royalty rates and milestone structures that can take 5–15% of net sales and $1m–$50m in development milestones, directly squeezing long‑term margins as Edgewise nears commercialization in rare diseases.

Keeping strong IP partnerships is critical: renegotiation risks, exclusivity terms, and sublicense rights affect launch timing, valuation, and investor returns—royalties can lower peak free cash flow by millions annually.

- Typical royalty range: 5–15% of net sales

- Common milestones: $1m–$50m per program

- Impact: reduces peak FCF and valuation multiples

Supplier squeeze: limited GMP CMOs, rising rates, long lead times, high CRO costs

Suppliers hold high bargaining power: few GMP CMOs (30–40 global), CMO day rates +18% since 2022, reagent lead times 12–20 weeks, CROs captured ~46% of outsourced R&D spend (2024), replacing a CRO costs $5–10M +6–12 months, typical royalties 5–15% of net sales, potential R&D cost uplift 8–15% if disrupted.

| Metric | 2024–25 Data |

|---|---|

| GMP CMOs | 30–40 |

| CMO rate change | +18% |

| Reagent lead time | 12–20 wks |

| CRO market share | 46% |

| CRO switch cost | $5–10M,+6–12m |

| Royalties | 5–15% |

| R&D cost risk | +8–15% |

What is included in the product

Tailored exclusively for Edgewise Therapeutics, this Porter's Five Forces overview uncovers competitive drivers, customer and supplier power, entry barriers, substitutes, and emerging threats shaping its market position and strategic options.

A concise Porter's Five Forces snapshot for Edgewise Therapeutics—ideal for rapid strategic decisions and slide-ready use in meetings.

Customers Bargaining Power

Concentration of Third Party Payers

Government Healthcare Reimbursement Policies

Government programs like Medicare and Medicaid act as pivotal customers, setting benchmark prices and reimbursement that influence private payers; Medicare Part B/Part D and Medicaid account for roughly 40% of US prescription spending as of 2024. Recent legislation through 2024–2025 introduced Medicare drug price negotiations for top-spend drugs and inflation rebates, which could cap Edgewise Therapeutics’ revenue for high-cost therapies. If Edgewise fails to secure favorable reimbursement codes or add-on payments, patient access and market penetration may be sharply limited, cutting potential peak sales by an estimated 20–40% in modeled scenarios.

Influence of Patient Advocacy Groups

Pharmacy Benefit Manager Formulary Control

Pharmacy Benefit Managers (PBMs) decide which drugs sit on preferred formularies for ~200 million insured US lives, so excluding sevasemten or placing it in a high-cost tier could cut Edgewise’s addressable market dramatically.

Securing preferred placement is critical as sevasemten nears launch; PBM-negotiated rebates often exceed 20–40% for specialty drugs, directly reducing net price and revenue.

Without formulary access, commercial uptake, prescribing rates, and peak sales forecasts (tens to hundreds of millions annually) would be materially impaired.

- PBMs control formulary access for ~200M US lives

- Typical specialty rebates: 20–40%

- Formulary exclusion = major hit to peak sales

- Favorable placement required for sevasemten launch

Limited Orphan Disease Patient Pool

Limited patient pools for Duchenne (DMD) and Becker (BMD)—prevalence ~1 in 3,600–6,000 male births for DMD and lower for BMD—mean losing a few percent of patients to competitors can cut revenue sharply; a 5% share shift in a 10,000-patient addressable market equals 500 patients and large revenue swings for Edgewise.

Scarcity increases collective buyer power: payers, advocacy groups, and centers of excellence can steer treatment choice, so Edgewise must show superior safety and efficacy in trials and real-world data to win and keep this concentrated cohort.

- Addressable market ~8,000–12,000 patients (US+EU).

- 5% loss ≈ 400–600 patients—material revenue impact.

- Decisions influenced by centers of excellence and payers.

Payers squeeze Edgewise: 20–40%+ rebates, $100–150k/QALY caps threaten 400–600 patients

| Metric | Value |

|---|---|

| Rebates (specialty) | 20–40% |

| ICER thresholds | $100–150k/QALY |

| Addressable patients | 8,000–12,000 |

| 5% share shift | 400–600 patients |

What You See Is What You Get

Edgewise Therapeutics Porter's Five Forces Analysis

This preview shows the exact Edgewise Therapeutics Porter’s Five Forces analysis you’ll receive immediately after purchase—no mockups or placeholders; the final, fully formatted document is ready for instant download and use.