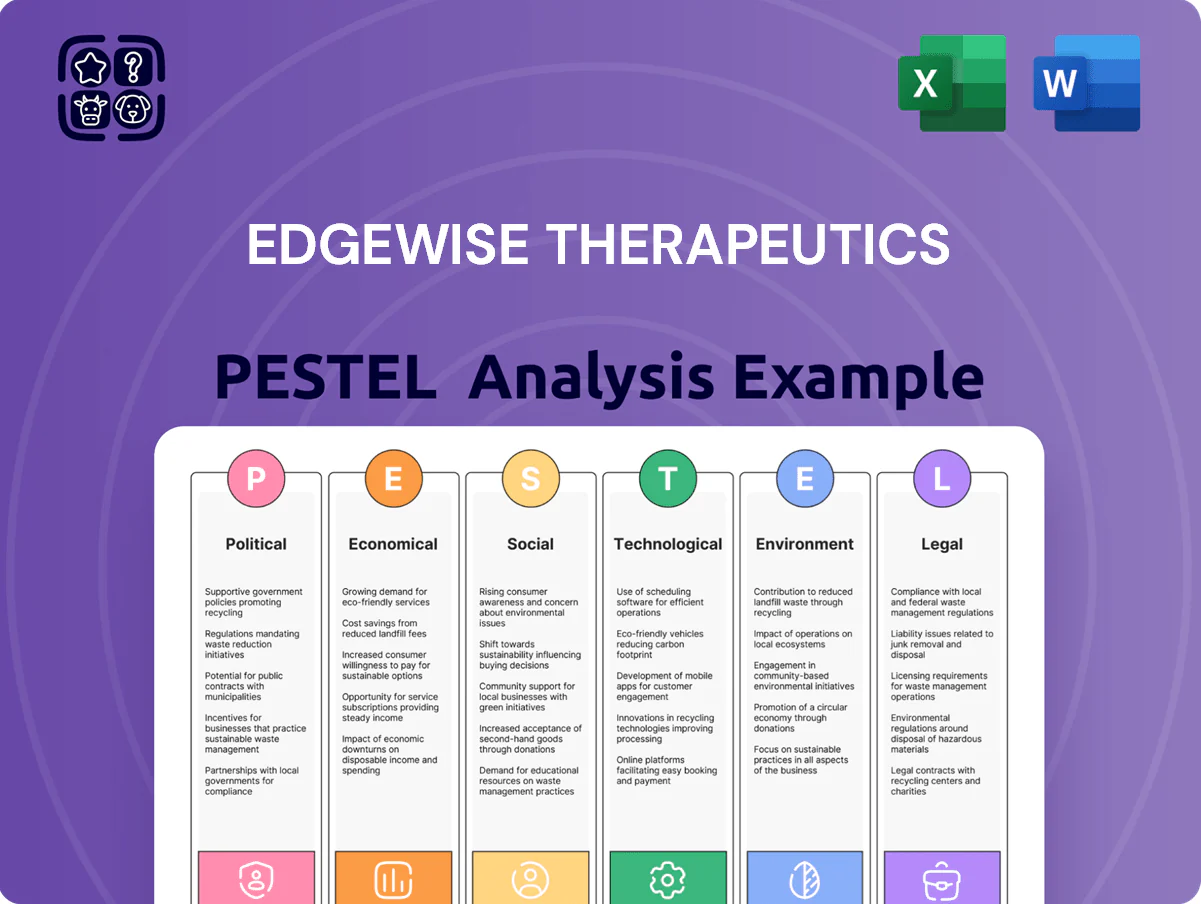

Edgewise Therapeutics PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE snapshot reveals how regulation, biotech funding cycles, and rapid tech advances shape Edgewise Therapeutics’ strategic risks and opportunities—concise, actionable, and investor-focused. Purchase the full PESTLE to access detailed legal, economic, and scientific drivers, scenario analysis, and ready-to-use slides for decisions and pitches.

Political factors

FDA Regulatory Environment

FDA emphasis on accelerated pathways for rare diseases remains a key political driver; by end-2025, the agency reported 65% of orphan drug designations using expedited programs, pressuring sponsors to adapt.

Political focus on Duchenne and Becker has led to broader acceptance of surrogate and functional endpoints; FDA advisory trends show 18% more flexibility in 2024–25 reviews.

Edgewise must align its small-molecule program with evolving endpoint standards and demonstrate safety/efficacy to satisfy federal requirements and potential accelerated approvals.

Drug Pricing Legislation

The Inflation Reduction Act’s drug negotiation program, which could begin targeting select drugs by 2026 and has already projected federal savings of $100+ billion through 2029, forces biopharma to assume price pressure in long-term planning.

Debate over orphan drug exemptions persists in Congress, with proposals in 2024–25 seeking to narrow eligibility after orphan-designated products accounted for roughly 10% of US drug spend in recent years.

Edgewise must track potential adjustments to the Small Molecule Penalty—changes could materially reduce net pricing for oral therapies and compress long-term revenue forecasts used in DCF models.

Federal Research Funding

Federal support via NIH and federal grants underpins rare disease work; NIH funding to musculoskeletal research rose to about $1.9B in FY2023 but faces variability as budget committee shifts in Congress can cut or redirect allocations.

International Trade and Supply Chain

Political stability in APAC and India, which supply roughly 60% of global active pharmaceutical ingredients, is critical for Edgewise Therapeutics to maintain clinical and commercial supply continuity.

Trade policies and tariffs projected through end-2025—including potential US tariffs of up to 10% on certain chemicals—could raise small-molecule input costs, impacting gross margins on drug candidates.

Rising geopolitical tensions prompt a shift toward diversified or regionalized sourcing; relocating 20–30% of API volumes could reduce disruption risk but raise logistics and capex.

- 60% of APIs sourced from APAC/India

- Potential tariffs up to 10% by end-2025

- Consider shifting 20–30% of API volume for resilience

Patient Advocacy Lobbying

Powerful advocacy groups like Parent Project Muscular Dystrophy, which helped secure >$1.2B in U.S. federal rare disease funding in 2024, exert strong influence on drug approval priorities and insurance mandates, accelerating pathways for therapies targeting Duchenne and related disorders.

These organizations lobby for legislative changes—such as expanded accelerated approval and coverage mandates—boosting access to breakthrough treatments and shortening time-to-market for companies like Edgewise.

Edgewise benefits from this political momentum: sustained advocacy keeps rare muscle disorders prioritized in federal research budgets and payer discussions, improving commercial prospects and reimbursement visibility.

- Advocacy-driven $1.2B+ rare disease funding (2024)

- Stronger push for accelerated approval and coverage mandates

- Increased political visibility enhances Edgewise commercialization and reimbursement prospects

Edgewise Poised by Rare‑Disease Tailwinds but Faces Pricing, Supply & Evidence Risks

Regulatory emphasis on accelerated rare-disease pathways (65% orphan expedited use by end-2025) and flexible Duchenne endpoints (+18% in 2024–25) favors Edgewise but raises evidentiary demands; IRA negotiation and orphan reform debates threaten pricing; API sourcing (≈60% APAC/India) and potential tariffs (up to 10%) pose supply/cost risks; advocacy drove $1.2B+ rare-disease funding in 2024, aiding reimbursement visibility.

| Metric | Value |

|---|---|

| Orphan expedited use (end-2025) | 65% |

| Duchenne endpoint flexibility (2024–25) | +18% |

| API sourcing from APAC/India | ≈60% |

| Potential tariffs | up to 10% |

| Advocacy-driven funding (2024) | $1.2B+ |

What is included in the product

Explores how macro-environmental forces uniquely affect Edgewise Therapeutics across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current industry trends and data to identify risks and opportunities.

Concise PESTLE summary of Edgewise Therapeutics highlighting regulatory, market, technological, and socio-economic factors to streamline risk discussions and strategic planning during meetings.

Economic factors

Capital Market Access

The cost of capital is critical for clinical-stage Edgewise, which had cash and equivalents of about $158.6m as of 9/30/2025, given estimated Phase 3 costs often exceeding $200–300m per program.

By late 2025, Fed funds near 5.25–5.50% and constrained biotech IPOs/secondary activity reduce investor appetite for high-risk biotech, affecting timing of follow-on offerings.

Maintaining a strong balance sheet is vital to fund late-stage trials without dilutive equity raises; Edgewise’s burn rate and runway metrics will determine dilution risk amid market volatility.

Orphan Drug Commercialization Costs

Bringing a rare disease drug to market incurs specialized marketing and distribution costs often 2–5x higher than primary care drugs; orphan launch costs can exceed $150–250M due to targeted outreach and logistics.

Edgewise’s economic model depends on premium pricing—U.S. orphan drug list prices averaged over $200,000/year in 2024—contingent on demonstrating clear clinical benefit vs standard of care.

Strategic plans must budget for high patient-identification costs (registry and genetic testing spend) and a specialized sales force targeting neuromuscular specialists, where payer access efforts raise pre-launch expenses by tens of millions.

Payer Reimbursement Trends

Insurance firms and PBMs are increasingly scrutinizing high-cost orphan drugs; in 2024, 78% of US payers reported stricter review policies for speciality therapies, pressuring Edgewise on pricing and outcomes.

By 2025 the shift to value-based care means Edgewise must show reduced hospitalizations or total cost of care; CMS and commercial pilots tie outcomes to rebates and shared savings, affecting revenue realization.

Economic success depends on favorable formulary placement and managing prior authorization burdens—70% of specialty prescriptions face PA delays—making payer contracting and real-world evidence generation critical.

Global Inflationary Pressures

Persistent global inflation—headline CPI around 3.4% in 2024 in major markets—raises costs for clinical trial supplies, shipping, and specialist staff, increasing per-patient trial expenses for Edgewise Therapeutics.

Higher wage inflation and supplier price increases can accelerate burn rate, risking a shortened cash runway unless capital planning is tightened; biotech median cash runway was ~18 months in 2024.

Contract Research Organization fees rose an estimated 5–8% YoY in 2024, forcing Edgewise to adopt stricter financial forecasting and cost-containment measures such as milestone-based contracts and renegotiation.

- Inflation increases trial input costs and wages

- Median biotech cash runway ~18 months (2024)

- CRO fees up ~5–8% YoY (2024)

- Need for tighter forecasting, milestone contracts

Biotech Sector M&A Activity

The pharmaceutical sector's economic health drives M&A; Big Pharma completed $210B in life-science deals in 2024–25, increasing odds Edgewise is bought or partners with a larger firm to refill pipelines facing patent cliffs.

Late-2025 valuation for Edgewise hinges on consolidation trends and premiums for rare-disease assets, where median deal premiums reached ~45% in 2024 for rare-asset transactions.

- Big Pharma deal flow: $210B (2024–25)

- Median premium for rare-disease assets: ~45% (2024)

- Patent-cliff-driven acquisitions rising

Edgewise faces dilution risk as cash falls short of Phase 3 amid tight market and payers

High cost of capital and ~18-month median biotech runway (2024) heighten dilution risk for Edgewise; cash $158.6M (9/30/2025) vs Phase 3 needs $200–300M. Fed funds ~5.25–5.50% (late‑2025) and weak IPO/secondary markets constrain follow‑on timing. Orphan pricing potential >$200k/year (2024) offset by payer scrutiny (78% tighter reviews, 2024) and value‑based reimbursement shifts.

| Metric | Value |

|---|---|

| Cash | $158.6M (9/30/2025) |

| Median runway | ~18 months (2024) |

| Phase 3 cost | $200–300M/program |

| Orphan list price | >$200,000/yr (2024) |

| Payer scrutiny | 78% tighter reviews (2024) |

What You See Is What You Get

Edgewise Therapeutics PESTLE Analysis

The preview shown here is the exact Edgewise Therapeutics PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; it includes the same content, insights, and layout visible now with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Our PESTLE snapshot reveals how regulation, biotech funding cycles, and rapid tech advances shape Edgewise Therapeutics’ strategic risks and opportunities—concise, actionable, and investor-focused. Purchase the full PESTLE to access detailed legal, economic, and scientific drivers, scenario analysis, and ready-to-use slides for decisions and pitches.

Political factors

FDA Regulatory Environment

FDA emphasis on accelerated pathways for rare diseases remains a key political driver; by end-2025, the agency reported 65% of orphan drug designations using expedited programs, pressuring sponsors to adapt.

Political focus on Duchenne and Becker has led to broader acceptance of surrogate and functional endpoints; FDA advisory trends show 18% more flexibility in 2024–25 reviews.

Edgewise must align its small-molecule program with evolving endpoint standards and demonstrate safety/efficacy to satisfy federal requirements and potential accelerated approvals.

Drug Pricing Legislation

The Inflation Reduction Act’s drug negotiation program, which could begin targeting select drugs by 2026 and has already projected federal savings of $100+ billion through 2029, forces biopharma to assume price pressure in long-term planning.

Debate over orphan drug exemptions persists in Congress, with proposals in 2024–25 seeking to narrow eligibility after orphan-designated products accounted for roughly 10% of US drug spend in recent years.

Edgewise must track potential adjustments to the Small Molecule Penalty—changes could materially reduce net pricing for oral therapies and compress long-term revenue forecasts used in DCF models.

Federal Research Funding

Federal support via NIH and federal grants underpins rare disease work; NIH funding to musculoskeletal research rose to about $1.9B in FY2023 but faces variability as budget committee shifts in Congress can cut or redirect allocations.

International Trade and Supply Chain

Political stability in APAC and India, which supply roughly 60% of global active pharmaceutical ingredients, is critical for Edgewise Therapeutics to maintain clinical and commercial supply continuity.

Trade policies and tariffs projected through end-2025—including potential US tariffs of up to 10% on certain chemicals—could raise small-molecule input costs, impacting gross margins on drug candidates.

Rising geopolitical tensions prompt a shift toward diversified or regionalized sourcing; relocating 20–30% of API volumes could reduce disruption risk but raise logistics and capex.

- 60% of APIs sourced from APAC/India

- Potential tariffs up to 10% by end-2025

- Consider shifting 20–30% of API volume for resilience

Patient Advocacy Lobbying

Powerful advocacy groups like Parent Project Muscular Dystrophy, which helped secure >$1.2B in U.S. federal rare disease funding in 2024, exert strong influence on drug approval priorities and insurance mandates, accelerating pathways for therapies targeting Duchenne and related disorders.

These organizations lobby for legislative changes—such as expanded accelerated approval and coverage mandates—boosting access to breakthrough treatments and shortening time-to-market for companies like Edgewise.

Edgewise benefits from this political momentum: sustained advocacy keeps rare muscle disorders prioritized in federal research budgets and payer discussions, improving commercial prospects and reimbursement visibility.

- Advocacy-driven $1.2B+ rare disease funding (2024)

- Stronger push for accelerated approval and coverage mandates

- Increased political visibility enhances Edgewise commercialization and reimbursement prospects

Edgewise Poised by Rare‑Disease Tailwinds but Faces Pricing, Supply & Evidence Risks

Regulatory emphasis on accelerated rare-disease pathways (65% orphan expedited use by end-2025) and flexible Duchenne endpoints (+18% in 2024–25) favors Edgewise but raises evidentiary demands; IRA negotiation and orphan reform debates threaten pricing; API sourcing (≈60% APAC/India) and potential tariffs (up to 10%) pose supply/cost risks; advocacy drove $1.2B+ rare-disease funding in 2024, aiding reimbursement visibility.

| Metric | Value |

|---|---|

| Orphan expedited use (end-2025) | 65% |

| Duchenne endpoint flexibility (2024–25) | +18% |

| API sourcing from APAC/India | ≈60% |

| Potential tariffs | up to 10% |

| Advocacy-driven funding (2024) | $1.2B+ |

What is included in the product

Explores how macro-environmental forces uniquely affect Edgewise Therapeutics across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section grounded in current industry trends and data to identify risks and opportunities.

Concise PESTLE summary of Edgewise Therapeutics highlighting regulatory, market, technological, and socio-economic factors to streamline risk discussions and strategic planning during meetings.

Economic factors

Capital Market Access

The cost of capital is critical for clinical-stage Edgewise, which had cash and equivalents of about $158.6m as of 9/30/2025, given estimated Phase 3 costs often exceeding $200–300m per program.

By late 2025, Fed funds near 5.25–5.50% and constrained biotech IPOs/secondary activity reduce investor appetite for high-risk biotech, affecting timing of follow-on offerings.

Maintaining a strong balance sheet is vital to fund late-stage trials without dilutive equity raises; Edgewise’s burn rate and runway metrics will determine dilution risk amid market volatility.

Orphan Drug Commercialization Costs

Bringing a rare disease drug to market incurs specialized marketing and distribution costs often 2–5x higher than primary care drugs; orphan launch costs can exceed $150–250M due to targeted outreach and logistics.

Edgewise’s economic model depends on premium pricing—U.S. orphan drug list prices averaged over $200,000/year in 2024—contingent on demonstrating clear clinical benefit vs standard of care.

Strategic plans must budget for high patient-identification costs (registry and genetic testing spend) and a specialized sales force targeting neuromuscular specialists, where payer access efforts raise pre-launch expenses by tens of millions.

Payer Reimbursement Trends

Insurance firms and PBMs are increasingly scrutinizing high-cost orphan drugs; in 2024, 78% of US payers reported stricter review policies for speciality therapies, pressuring Edgewise on pricing and outcomes.

By 2025 the shift to value-based care means Edgewise must show reduced hospitalizations or total cost of care; CMS and commercial pilots tie outcomes to rebates and shared savings, affecting revenue realization.

Economic success depends on favorable formulary placement and managing prior authorization burdens—70% of specialty prescriptions face PA delays—making payer contracting and real-world evidence generation critical.

Global Inflationary Pressures

Persistent global inflation—headline CPI around 3.4% in 2024 in major markets—raises costs for clinical trial supplies, shipping, and specialist staff, increasing per-patient trial expenses for Edgewise Therapeutics.

Higher wage inflation and supplier price increases can accelerate burn rate, risking a shortened cash runway unless capital planning is tightened; biotech median cash runway was ~18 months in 2024.

Contract Research Organization fees rose an estimated 5–8% YoY in 2024, forcing Edgewise to adopt stricter financial forecasting and cost-containment measures such as milestone-based contracts and renegotiation.

- Inflation increases trial input costs and wages

- Median biotech cash runway ~18 months (2024)

- CRO fees up ~5–8% YoY (2024)

- Need for tighter forecasting, milestone contracts

Biotech Sector M&A Activity

The pharmaceutical sector's economic health drives M&A; Big Pharma completed $210B in life-science deals in 2024–25, increasing odds Edgewise is bought or partners with a larger firm to refill pipelines facing patent cliffs.

Late-2025 valuation for Edgewise hinges on consolidation trends and premiums for rare-disease assets, where median deal premiums reached ~45% in 2024 for rare-asset transactions.

- Big Pharma deal flow: $210B (2024–25)

- Median premium for rare-disease assets: ~45% (2024)

- Patent-cliff-driven acquisitions rising

Edgewise faces dilution risk as cash falls short of Phase 3 amid tight market and payers

High cost of capital and ~18-month median biotech runway (2024) heighten dilution risk for Edgewise; cash $158.6M (9/30/2025) vs Phase 3 needs $200–300M. Fed funds ~5.25–5.50% (late‑2025) and weak IPO/secondary markets constrain follow‑on timing. Orphan pricing potential >$200k/year (2024) offset by payer scrutiny (78% tighter reviews, 2024) and value‑based reimbursement shifts.

| Metric | Value |

|---|---|

| Cash | $158.6M (9/30/2025) |

| Median runway | ~18 months (2024) |

| Phase 3 cost | $200–300M/program |

| Orphan list price | >$200,000/yr (2024) |

| Payer scrutiny | 78% tighter reviews (2024) |

What You See Is What You Get

Edgewise Therapeutics PESTLE Analysis

The preview shown here is the exact Edgewise Therapeutics PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use; it includes the same content, insights, and layout visible now with no placeholders or surprises.