Edison International Boston Consulting Group Matrix

Download Your Competitive Advantage

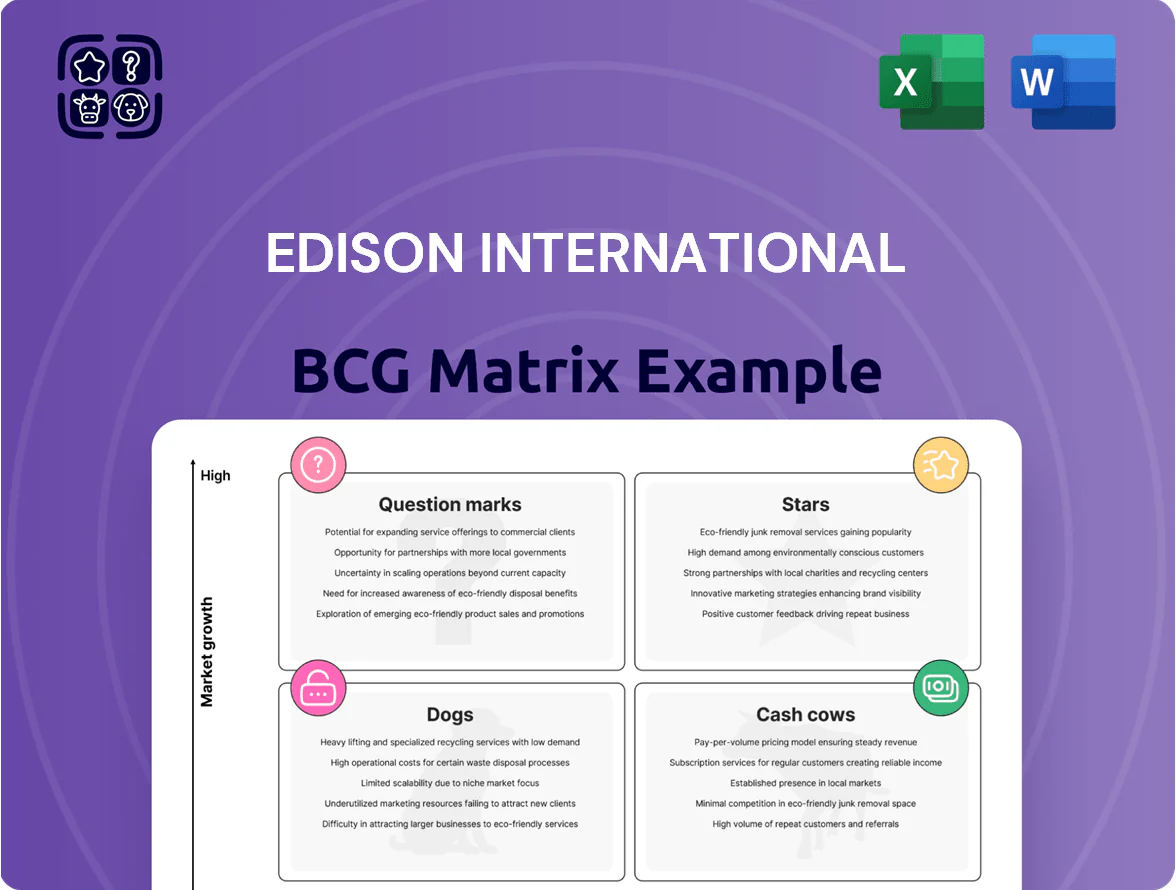

Edison International’s BCG Matrix preview highlights where its business lines—regulated electric utilities, grid modernization projects, and emerging clean-energy initiatives—likely sit across Stars, Cash Cows, Dogs, and Question Marks, revealing growth potential versus cash generation and resource drains; this snapshot helps prioritize capital allocation and strategic focus. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a downloadable Word and Excel package to turn insights into actionable investment and operational decisions.

Stars

Grid Modernization and Electrification

Edison International has invested over $15 billion into grid modernization through 2025 to support California’s decarbonization and electrification targets, positioning this segment as a high-growth leader with dominant regional share in utility-scale distribution and smart-grid services.

As California advances toward full electrification of buildings and transport, demand for grid capacity is rising ~6–8% annually, driving rate-base growth potential despite heavy upfront spending.

High capital expenditure and multi-year projects raise short-term leverage, but these investments are central to long-term stable returns and regulated revenue expansion.

Electric Vehicle Charging Infrastructure

Southern California Edison (SCE) runs one of the largest U.S. utility-led EV charging programs, with SCE proposing $1.6 billion for charging and grid upgrades through 2026 and targeting ~2.4 million EVs in its service area by 2030 per CPUC-aligned forecasts.

Utility Scale Battery Energy Storage

Edison International is rapidly scaling utility-scale battery energy storage, adding ~1.2 GW/2.4 GWh from 2023–2025 to smooth solar/wind intermittency and meet California's 2045 carbon-free mandate; storage now represents a core Stars segment in the BCG matrix with >30% annual capacity growth.

Wildfire Mitigation Technology

Edison International’s wildfire mitigation tech—covered conductors and advanced weather monitoring—sits in a high-growth BCG quadrant: rising demand from worsening climate trends and strict California regulations. In 2024 the company spent about $1.2 billion on wildfire safety programs, cutting ignition incidents and limiting potential liability exposures tied to past fires.

- High growth: wildfire losses up 30% since 2010

- Capex: $1.2B in 2024 for mitigation

- Benefit: lowers long-term liability and preserves market position

- Drawback: high upfront cost, slow ROI

Clean Energy Transmission Projects

Edison International rates Clean Energy Transmission Projects as Stars: high-growth segment driven by CAISO 2030 targets and 2035 SB100 ambitions; statewide transmission investment needs hit $22–28 billion through 2030 per CAISO, and Edison holds ~45% share of planned regional tie-line projects in its service territory as of Dec 2025.

These HV transmission assets are core to Edison’s growth plan, representing roughly $1.2–1.6 billion of capital spend in 2026–2028 guidance and expected to lift regulated rate base growth by ~3–4% annually through 2030.

They enable large-scale renewable integration from remote zones to Los Angeles and San Diego, cut curtailment, and lower system LCOE (levelized cost of energy) by estimated 8–12% for connected projects based on recent CAISO modeling.

- High growth: CAISO $22–28B need to 2030

- Dominant share: ~45% regional tie-lines (Dec 2025)

- CAPEX: $1.2–1.6B (2026–2028)

- Rate base lift: ~3–4% CAGR to 2030

- LCOE cut: 8–12% for connected renewables

Edison International: $15B Grid Capex, Storage & EV Push, Rate-Base Growth to 2030

Edison International’s Stars: grid modernization, storage, wildfire mitigation, EV charging, and clean transmission—high-growth, regulated rate-base drivers with $15B capex to 2025, $1.2B wildfire spend (2024), ~1.2GW storage added (2023–25), SCE $1.6B EV plan to 2026, CAISO $22–28B transmission need to 2030; rate-base CAGR ~3–4% to 2030.

| Segment | Key 2024–26 |

|---|---|

| Grid | $15B capex to 2025 |

| Storage | ~1.2GW/2.4GWh (’23–25) |

| Wildfire | $1.2B 2024 |

| EV | $1.6B to 2026 |

| Transmission | $1.2–1.6B (’26–28) |

What is included in the product

BCG Matrix analysis of Edison International’s units with quadrant-specific strategies, investment recommendations, and trend-driven risks/opportunities.

One-page overview placing each Edison International business unit in a BCG quadrant for fast strategic clarity.

Cash Cows

Core Residential Power Distribution

The regulated residential utility at Edison International (Southern California Edison, market cap ~55B USD as of Dec 31, 2025) delivers steady revenue—~63% of 2024 consolidated revenues—driven by a captive ~5M customer base and allowed ROE near 10.4%, so growth tracks population and demand (low, ~1–2% CAGR). It generates strong free cash flow (~$1.6B in 2024) funding dividends and reinvesting into higher-growth grid modernization stars.

Transmission Asset Portfolio

Edison International’s Transmission Asset Portfolio delivers steady cash flow: California high-voltage lines generated ~ $1.1B EBITDA in 2024, driven by regulated returns and established rate bases, yielding margins near 60% vs company avg ~25%.

These lines need mainly maintenance capex—EIX spent ~$220M on transmission maintenance in 2024—not large development outlays, preserving free cash flow and dividend capacity.

Regulated Rate Base Assets

The regulated rate base assets of Edison International, totaling about $22.5 billion in electric plant in service as of Dec 31, 2024, form the earnings foundation under California Public Utilities Commission oversight.

This mature, monopoly-like footprint in Southern California delivers predictable cash flows and low incremental growth, making it a classic cash cow in the BCG matrix.

Cash from these assets funds interest and principal on corporate debt—EIX had $7.9 billion long-term debt at end-2024—and supports the holding company’s financial stability.

Commercial and Industrial Power Delivery

Commercial and Industrial Power Delivery in Southern California provides Edison International steady, low-growth cash flows—SCE sold ~86 million MWh in 2024 to C&I customers, generating roughly $9.2 billion in revenue (about 45% of total utility revenue), reflecting market maturity and stable demand.

High-volume sales to large users ensure predictable cash inflows and EBITDA margins near utility sector norms (~33% in 2024), with minimal marketing since customers are tied to existing distribution infrastructure.

Risk is low but capped upside: load growth ~0.8% CAGR (2020–2024) limits expansion without new electrification or rate actions.

- Stable revenue: ~$9.2B from C&I (2024)

- High volume: ~86M MWh sold to C&I (2024)

- Margins: ~33% utility EBITDA (2024)

- Growth: ~0.8% load CAGR (2020–2024)

Legacy Hydropower Operations

Legacy Hydropower Operations: Edison International’s century-old hydro plants deliver stable, low-cost baseload generation—operating with >90% availability and marginal O&M below $10/MWh—so they subsidize margins across the portfolio.

Installed capacity ~1,200 MW, annual output ~4.5 TWh (2025 forecast), negligible capital spend needed, and cash returns support utility earnings and fund renewables growth.

- High availability >90%

- O&M < $10/MWh

- Capacity ~1,200 MW

- Annual output ~4.5 TWh (2025)

- Minimal capex; strong free cash flow

Edison International: Stable cash cows — $1.6B FCF, $22.5B assets, 1.2GW hydro

Edison International cash cows (SCE utility, transmission, C&I sales, hydro) generated ~63% of 2024 revenue, ~$1.6B FCF (2024), ~$9.2B C&I revenue (86M MWh, 2024), transmission EBITDA ~$1.1B (2024), electric plant in service ~$22.5B (12/31/24), long-term debt $7.9B (12/31/24), hydro ~1,200 MW ~4.5 TWh (2025 forecast).

| Metric | Value |

|---|---|

| % Rev (2024) | ~63% |

| FCF (2024) | $1.6B |

| C&I Rev (2024) | $9.2B |

| Transmission EBITDA (2024) | $1.1B |

| Plant in service (12/31/24) | $22.5B |

| Long-term debt (12/31/24) | $7.9B |

| Hydro capacity/output | ~1,200 MW / ~4.5 TWh (2025) |

What You See Is What You Get

Edison International BCG Matrix

The file you're previewing is the exact Edison International BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, ready-to-use strategic analysis designed for clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Edison International’s BCG Matrix preview highlights where its business lines—regulated electric utilities, grid modernization projects, and emerging clean-energy initiatives—likely sit across Stars, Cash Cows, Dogs, and Question Marks, revealing growth potential versus cash generation and resource drains; this snapshot helps prioritize capital allocation and strategic focus. Purchase the full BCG Matrix for quadrant-by-quadrant placements, data-backed recommendations, and a downloadable Word and Excel package to turn insights into actionable investment and operational decisions.

Stars

Grid Modernization and Electrification

Edison International has invested over $15 billion into grid modernization through 2025 to support California’s decarbonization and electrification targets, positioning this segment as a high-growth leader with dominant regional share in utility-scale distribution and smart-grid services.

As California advances toward full electrification of buildings and transport, demand for grid capacity is rising ~6–8% annually, driving rate-base growth potential despite heavy upfront spending.

High capital expenditure and multi-year projects raise short-term leverage, but these investments are central to long-term stable returns and regulated revenue expansion.

Electric Vehicle Charging Infrastructure

Southern California Edison (SCE) runs one of the largest U.S. utility-led EV charging programs, with SCE proposing $1.6 billion for charging and grid upgrades through 2026 and targeting ~2.4 million EVs in its service area by 2030 per CPUC-aligned forecasts.

Utility Scale Battery Energy Storage

Edison International is rapidly scaling utility-scale battery energy storage, adding ~1.2 GW/2.4 GWh from 2023–2025 to smooth solar/wind intermittency and meet California's 2045 carbon-free mandate; storage now represents a core Stars segment in the BCG matrix with >30% annual capacity growth.

Wildfire Mitigation Technology

Edison International’s wildfire mitigation tech—covered conductors and advanced weather monitoring—sits in a high-growth BCG quadrant: rising demand from worsening climate trends and strict California regulations. In 2024 the company spent about $1.2 billion on wildfire safety programs, cutting ignition incidents and limiting potential liability exposures tied to past fires.

- High growth: wildfire losses up 30% since 2010

- Capex: $1.2B in 2024 for mitigation

- Benefit: lowers long-term liability and preserves market position

- Drawback: high upfront cost, slow ROI

Clean Energy Transmission Projects

Edison International rates Clean Energy Transmission Projects as Stars: high-growth segment driven by CAISO 2030 targets and 2035 SB100 ambitions; statewide transmission investment needs hit $22–28 billion through 2030 per CAISO, and Edison holds ~45% share of planned regional tie-line projects in its service territory as of Dec 2025.

These HV transmission assets are core to Edison’s growth plan, representing roughly $1.2–1.6 billion of capital spend in 2026–2028 guidance and expected to lift regulated rate base growth by ~3–4% annually through 2030.

They enable large-scale renewable integration from remote zones to Los Angeles and San Diego, cut curtailment, and lower system LCOE (levelized cost of energy) by estimated 8–12% for connected projects based on recent CAISO modeling.

- High growth: CAISO $22–28B need to 2030

- Dominant share: ~45% regional tie-lines (Dec 2025)

- CAPEX: $1.2–1.6B (2026–2028)

- Rate base lift: ~3–4% CAGR to 2030

- LCOE cut: 8–12% for connected renewables

Edison International: $15B Grid Capex, Storage & EV Push, Rate-Base Growth to 2030

Edison International’s Stars: grid modernization, storage, wildfire mitigation, EV charging, and clean transmission—high-growth, regulated rate-base drivers with $15B capex to 2025, $1.2B wildfire spend (2024), ~1.2GW storage added (2023–25), SCE $1.6B EV plan to 2026, CAISO $22–28B transmission need to 2030; rate-base CAGR ~3–4% to 2030.

| Segment | Key 2024–26 |

|---|---|

| Grid | $15B capex to 2025 |

| Storage | ~1.2GW/2.4GWh (’23–25) |

| Wildfire | $1.2B 2024 |

| EV | $1.6B to 2026 |

| Transmission | $1.2–1.6B (’26–28) |

What is included in the product

BCG Matrix analysis of Edison International’s units with quadrant-specific strategies, investment recommendations, and trend-driven risks/opportunities.

One-page overview placing each Edison International business unit in a BCG quadrant for fast strategic clarity.

Cash Cows

Core Residential Power Distribution

The regulated residential utility at Edison International (Southern California Edison, market cap ~55B USD as of Dec 31, 2025) delivers steady revenue—~63% of 2024 consolidated revenues—driven by a captive ~5M customer base and allowed ROE near 10.4%, so growth tracks population and demand (low, ~1–2% CAGR). It generates strong free cash flow (~$1.6B in 2024) funding dividends and reinvesting into higher-growth grid modernization stars.

Transmission Asset Portfolio

Edison International’s Transmission Asset Portfolio delivers steady cash flow: California high-voltage lines generated ~ $1.1B EBITDA in 2024, driven by regulated returns and established rate bases, yielding margins near 60% vs company avg ~25%.

These lines need mainly maintenance capex—EIX spent ~$220M on transmission maintenance in 2024—not large development outlays, preserving free cash flow and dividend capacity.

Regulated Rate Base Assets

The regulated rate base assets of Edison International, totaling about $22.5 billion in electric plant in service as of Dec 31, 2024, form the earnings foundation under California Public Utilities Commission oversight.

This mature, monopoly-like footprint in Southern California delivers predictable cash flows and low incremental growth, making it a classic cash cow in the BCG matrix.

Cash from these assets funds interest and principal on corporate debt—EIX had $7.9 billion long-term debt at end-2024—and supports the holding company’s financial stability.

Commercial and Industrial Power Delivery

Commercial and Industrial Power Delivery in Southern California provides Edison International steady, low-growth cash flows—SCE sold ~86 million MWh in 2024 to C&I customers, generating roughly $9.2 billion in revenue (about 45% of total utility revenue), reflecting market maturity and stable demand.

High-volume sales to large users ensure predictable cash inflows and EBITDA margins near utility sector norms (~33% in 2024), with minimal marketing since customers are tied to existing distribution infrastructure.

Risk is low but capped upside: load growth ~0.8% CAGR (2020–2024) limits expansion without new electrification or rate actions.

- Stable revenue: ~$9.2B from C&I (2024)

- High volume: ~86M MWh sold to C&I (2024)

- Margins: ~33% utility EBITDA (2024)

- Growth: ~0.8% load CAGR (2020–2024)

Legacy Hydropower Operations

Legacy Hydropower Operations: Edison International’s century-old hydro plants deliver stable, low-cost baseload generation—operating with >90% availability and marginal O&M below $10/MWh—so they subsidize margins across the portfolio.

Installed capacity ~1,200 MW, annual output ~4.5 TWh (2025 forecast), negligible capital spend needed, and cash returns support utility earnings and fund renewables growth.

- High availability >90%

- O&M < $10/MWh

- Capacity ~1,200 MW

- Annual output ~4.5 TWh (2025)

- Minimal capex; strong free cash flow

Edison International: Stable cash cows — $1.6B FCF, $22.5B assets, 1.2GW hydro

Edison International cash cows (SCE utility, transmission, C&I sales, hydro) generated ~63% of 2024 revenue, ~$1.6B FCF (2024), ~$9.2B C&I revenue (86M MWh, 2024), transmission EBITDA ~$1.1B (2024), electric plant in service ~$22.5B (12/31/24), long-term debt $7.9B (12/31/24), hydro ~1,200 MW ~4.5 TWh (2025 forecast).

| Metric | Value |

|---|---|

| % Rev (2024) | ~63% |

| FCF (2024) | $1.6B |

| C&I Rev (2024) | $9.2B |

| Transmission EBITDA (2024) | $1.1B |

| Plant in service (12/31/24) | $22.5B |

| Long-term debt (12/31/24) | $7.9B |

| Hydro capacity/output | ~1,200 MW / ~4.5 TWh (2025) |

What You See Is What You Get

Edison International BCG Matrix

The file you're previewing is the exact Edison International BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, ready-to-use strategic analysis designed for clarity and professional presentation.