EDP Renovaveis Boston Consulting Group Matrix

See the Bigger Picture

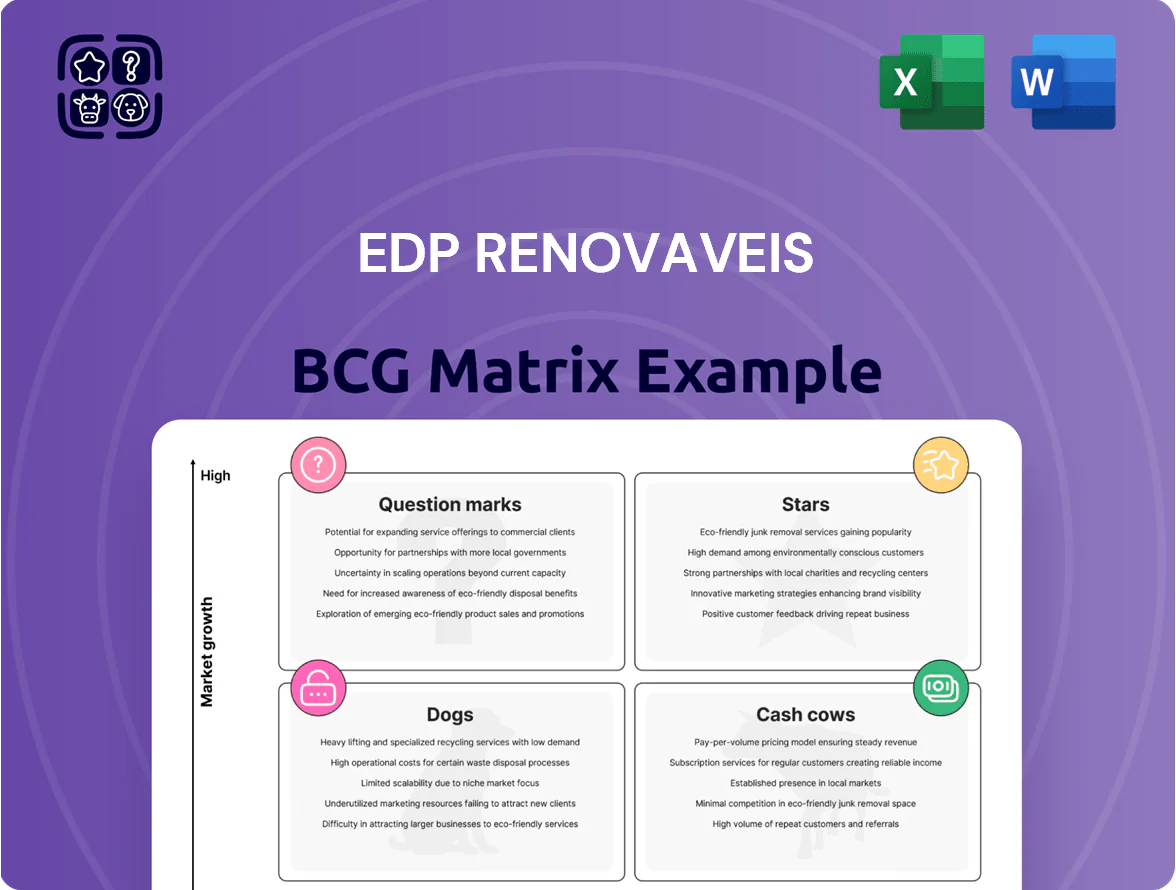

EDP Renováveis sits at the intersection of stable cash generation and growth potential as renewable demand accelerates; our preview flags which assets behave like Stars or Cash Cows and where operational or market risks could create Question Marks. The full BCG Matrix delivers quadrant-level placements, tailored strategic moves, and capital-allocation guidance to optimize the company’s portfolio. Purchase the complete report for an editable Word analysis plus an Excel summary—instant, data-driven insight to inform investment and strategic decisions.

Stars

Utility-Scale Solar PV in North America

As of end-2025, utility-scale solar PV drove EDPRs growth, with solar generation nearly doubling year-over-year to 24% of total generation and contributing to a 18% rise in group output versus 2024.

EDPR added ~1.8 GWac in the US in 2025—about 55% of recent additions—backed by 15- to 20-year PPAs with major tech firms and utilities; US portfolio now represents ~30% of global capacity.

The segment benefitted from the US Inflation Reduction Act tax credits, improving project IRRs by ~200–400 basis points, but needs sustained capital — roughly €1.2–1.5 billion annual investment — to defend market share.

Battery Energy Storage Systems (BESS)

EDP Renováveis more than doubled installed BESS to 0.6 GW by end-2025, with a 1.6 GW pipeline under construction, mostly in the US, making BESS a Star in the BCG matrix for 2026–2028.

BESS firm renewables output and meet grid flexibility; EDPR rates it a high-growth priority in its 2026–28 plan, targeting ancillary service revenues and portfolio value protection.

Though cash-intensive—CAPEX per MWh ~€350–450 in 2025—BESS enables higher dispatch value and recurring revenue streams that boost IRR on wind/solar assets.

Hybrid Renewable Energy Projects

EDP Renovaveis leads hybrid wind+solar projects in Iberia and North America, boosting effective capacity factors by 10–30% and cutting levelized cost of energy; Iberia hybrids raised fleet CF by ~15% on average in 2024, while select North American sites showed 25% gains.

Renewable Energy for Data Centers

EDPR targets the high-growth data center market in the US, with over 20% of new contracts signed with tech giants and 24/7 or shaped delivery offered to meet strict uptime and carbon-free needs.

The 2026–2028 plan ups US investment weight to 60%, focusing capital on capacity and firming solutions as data-center demand drives ~5–7 GW incremental annual corporate procurement through 2028.

- 20% of new contracts with tech giants

- 24/7 or shaped delivery for big tech

- US investment weight 60% (2026–2028)

- Market demand ~5–7 GW/yr corporate procurement

Onshore Wind Expansion in Europe

Onshore Wind Expansion in Europe: despite being mature, EDPR targets growth via repowering and new builds in Poland and Greece, blending higher yields with lower LCOE from scale.

In 2025 Europe drove 32% of EDPR capacity additions, prioritizing high-return sites and pairing projects with battery storage to boost dispatchability and merchant revenue.

The segment needs steady permitting and grid coordination support; it remains a top source of contracted cash flows, underpinning 2025 EBITDA contribution and pipeline visibility.

- 2025: Europe = 32% of additions

- Focus: Poland, Greece, repowering

- Strategy: batteries + high-return sites

- Need: permitting, grid coordination

- Outcome: stable contracted cash flows

EDPR: Solar & BESS drive 24% solar, 1.8GW US growth, €1.2–1.5bn capex, IRR +200–400bps

EDPR’s Stars: utility-scale solar (24% gen, +18% YoY 2025), US growth (≈1.8 GWac added, ~30% global capacity), BESS (0.6 GW installed, 1.6 GW pipeline), hybrids raising CF 10–30%; annual CAPEX need €1.2–1.5bn; IRR uplift 200–400 bps from IRA.

| Metric | 2025 |

|---|---|

| Solar gen share | 24% |

| US additions | 1.8 GWac |

| BESS installed | 0.6 GW |

| Capex need | €1.2–1.5bn |

What is included in the product

Comprehensive BCG Matrix for EDP Renováveis: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with invest/hold/divest actions.

One-page EDP Renováveis BCG Matrix showing each unit's position for fast strategic decisions.

Cash Cows

Onshore Wind in North America

Onshore wind in North America remains EDPR's cash cow, accounting for 76% of group generation by late 2025 and anchored by a US fleet exceeding 12 GW operational capacity.

These plants run mostly under long-term power purchase agreements (PPAs) with an average 18-year remaining tenor, delivering predictable EBITDA and roughly €1.2–1.4 billion in annual free cash flow contribution in 2024–25.

As the US market matures, EDPR is prioritizing operational efficiency, asset life extension, and availability gains to maximize yield and recycle cash into storage and offshore projects.

Operational Solar Parks in Iberia

Legacy solar parks in Spain and Portugal give EDP Renovaveis a dominant market share in Iberia, with ~1.2 GW operational as of Dec 2025 and stable generation amid a mature, predictable tariff and grid regime.

These plants show high EBITDA margins — often >60% — driven by near-zero marginal costs and largely depreciated assets, boosting free cash flow per MW versus newer builds.

Cash from Iberian parks funded ~35% of EDPR’s capex and supported a 2025 dividend yield near 3.8%, while freeing capital to reinvest in storage and green hydrogen pilots.

Asset Rotation Program

The asset rotation program is a mature process where EDP Renováveis sells minority or majority stakes in operating projects to institutions, aiming for 7.0 billion euros of proceeds through 2026; in 2025 it secured ~2.0 billion euros from deals in the US and Europe.

Hydropower Portfolio in Iberia

EDP Renovaveis' hydropower portfolio in Iberia, largely integrated with parent EDP, delivers firming and storage that smooths the group's renewable output and backed 2024 EBITDA contribution of ~€420m from hydro-generation across Portugal and Spain.

Operating in a mature Iberian market with high entry barriers, these assets generate predictable cash flows and supported EDP Group’s 2024 free cash flow, reducing financing stress and volatility.

Hydro acts as a natural hedge to wind and solar intermittency, enabling reliable offtaker delivery and optimizing ≈1.6 GW of dispatchable capacity for intraday balancing.

- ~€420m hydro EBITDA (2024)

- ≈1.6 GW dispatchable capacity

- Mature Iberian market, high barriers to entry

- Stabilizes renewable output, supports group FCF

Long-term Contracted PPAs

EDP Renováveis (EDPR) bases cash flows on long-term power purchase agreements (PPAs) covering the bulk of its generation, giving multi-decade revenue visibility and low market exposure.

By 2025 EDPR has signed over 15 GW of PPAs globally, securing predictable income with minimal marketing or placement costs and supporting stable free cash flow.

These contracted revenues underpin EDPR’s A-grade credit profile, enabling reliable debt service and steady dividend distributions to shareholders.

- 15+ GW signed PPAs (2025)

- Multi-decade revenue visibility

- Low incremental sales costs

- A-rated credit supporting dividends

EDPR: US wind & Iberian solar/hydro fuel €1.2–1.4bn FCF, €2bn asset rotation, 3.8% yield

Onshore US wind (≈12 GW) and Iberian solar/hydro are EDPR cash cows, delivering ~€1.2–1.4bn FCF (2024–25) plus ~€420m hydro EBITDA (2024); 15+ GW PPAs provide multi-decade revenue visibility and support a ~3.8% 2025 dividend yield; asset rotation raised ~€2.0bn in 2025 toward a €7.0bn 2026 target.

| Metric | Value (2024–25) |

|---|---|

| US onshore capacity | ≈12 GW |

| Signed PPAs | 15+ GW |

| FCF contribution | €1.2–1.4bn |

| Hydro EBITDA | ≈€420m |

| Asset sales 2025 | €2.0bn |

| Rotation target | €7.0bn |

Delivered as Shown

EDP Renovaveis BCG Matrix

The file you're previewing on this page is the final EDP Renováveis BCG Matrix you'll receive after purchase—no watermarks or demo content, just a fully formatted, ready-to-use strategic report designed for investor and management clarity.

This preview is the exact same BCG Matrix document delivered post-purchase, built with market-backed analysis and clear positioning of EDP Renováveis’ business units for immediate use in presentations or planning.

What you see is the actual file available upon payment; once purchased you’ll get the full editable report ready for printing, sharing, or integration into your financial models—no surprises, no revisions needed.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

EDP Renováveis sits at the intersection of stable cash generation and growth potential as renewable demand accelerates; our preview flags which assets behave like Stars or Cash Cows and where operational or market risks could create Question Marks. The full BCG Matrix delivers quadrant-level placements, tailored strategic moves, and capital-allocation guidance to optimize the company’s portfolio. Purchase the complete report for an editable Word analysis plus an Excel summary—instant, data-driven insight to inform investment and strategic decisions.

Stars

Utility-Scale Solar PV in North America

As of end-2025, utility-scale solar PV drove EDPRs growth, with solar generation nearly doubling year-over-year to 24% of total generation and contributing to a 18% rise in group output versus 2024.

EDPR added ~1.8 GWac in the US in 2025—about 55% of recent additions—backed by 15- to 20-year PPAs with major tech firms and utilities; US portfolio now represents ~30% of global capacity.

The segment benefitted from the US Inflation Reduction Act tax credits, improving project IRRs by ~200–400 basis points, but needs sustained capital — roughly €1.2–1.5 billion annual investment — to defend market share.

Battery Energy Storage Systems (BESS)

EDP Renováveis more than doubled installed BESS to 0.6 GW by end-2025, with a 1.6 GW pipeline under construction, mostly in the US, making BESS a Star in the BCG matrix for 2026–2028.

BESS firm renewables output and meet grid flexibility; EDPR rates it a high-growth priority in its 2026–28 plan, targeting ancillary service revenues and portfolio value protection.

Though cash-intensive—CAPEX per MWh ~€350–450 in 2025—BESS enables higher dispatch value and recurring revenue streams that boost IRR on wind/solar assets.

Hybrid Renewable Energy Projects

EDP Renovaveis leads hybrid wind+solar projects in Iberia and North America, boosting effective capacity factors by 10–30% and cutting levelized cost of energy; Iberia hybrids raised fleet CF by ~15% on average in 2024, while select North American sites showed 25% gains.

Renewable Energy for Data Centers

EDPR targets the high-growth data center market in the US, with over 20% of new contracts signed with tech giants and 24/7 or shaped delivery offered to meet strict uptime and carbon-free needs.

The 2026–2028 plan ups US investment weight to 60%, focusing capital on capacity and firming solutions as data-center demand drives ~5–7 GW incremental annual corporate procurement through 2028.

- 20% of new contracts with tech giants

- 24/7 or shaped delivery for big tech

- US investment weight 60% (2026–2028)

- Market demand ~5–7 GW/yr corporate procurement

Onshore Wind Expansion in Europe

Onshore Wind Expansion in Europe: despite being mature, EDPR targets growth via repowering and new builds in Poland and Greece, blending higher yields with lower LCOE from scale.

In 2025 Europe drove 32% of EDPR capacity additions, prioritizing high-return sites and pairing projects with battery storage to boost dispatchability and merchant revenue.

The segment needs steady permitting and grid coordination support; it remains a top source of contracted cash flows, underpinning 2025 EBITDA contribution and pipeline visibility.

- 2025: Europe = 32% of additions

- Focus: Poland, Greece, repowering

- Strategy: batteries + high-return sites

- Need: permitting, grid coordination

- Outcome: stable contracted cash flows

EDPR: Solar & BESS drive 24% solar, 1.8GW US growth, €1.2–1.5bn capex, IRR +200–400bps

EDPR’s Stars: utility-scale solar (24% gen, +18% YoY 2025), US growth (≈1.8 GWac added, ~30% global capacity), BESS (0.6 GW installed, 1.6 GW pipeline), hybrids raising CF 10–30%; annual CAPEX need €1.2–1.5bn; IRR uplift 200–400 bps from IRA.

| Metric | 2025 |

|---|---|

| Solar gen share | 24% |

| US additions | 1.8 GWac |

| BESS installed | 0.6 GW |

| Capex need | €1.2–1.5bn |

What is included in the product

Comprehensive BCG Matrix for EDP Renováveis: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with invest/hold/divest actions.

One-page EDP Renováveis BCG Matrix showing each unit's position for fast strategic decisions.

Cash Cows

Onshore Wind in North America

Onshore wind in North America remains EDPR's cash cow, accounting for 76% of group generation by late 2025 and anchored by a US fleet exceeding 12 GW operational capacity.

These plants run mostly under long-term power purchase agreements (PPAs) with an average 18-year remaining tenor, delivering predictable EBITDA and roughly €1.2–1.4 billion in annual free cash flow contribution in 2024–25.

As the US market matures, EDPR is prioritizing operational efficiency, asset life extension, and availability gains to maximize yield and recycle cash into storage and offshore projects.

Operational Solar Parks in Iberia

Legacy solar parks in Spain and Portugal give EDP Renovaveis a dominant market share in Iberia, with ~1.2 GW operational as of Dec 2025 and stable generation amid a mature, predictable tariff and grid regime.

These plants show high EBITDA margins — often >60% — driven by near-zero marginal costs and largely depreciated assets, boosting free cash flow per MW versus newer builds.

Cash from Iberian parks funded ~35% of EDPR’s capex and supported a 2025 dividend yield near 3.8%, while freeing capital to reinvest in storage and green hydrogen pilots.

Asset Rotation Program

The asset rotation program is a mature process where EDP Renováveis sells minority or majority stakes in operating projects to institutions, aiming for 7.0 billion euros of proceeds through 2026; in 2025 it secured ~2.0 billion euros from deals in the US and Europe.

Hydropower Portfolio in Iberia

EDP Renovaveis' hydropower portfolio in Iberia, largely integrated with parent EDP, delivers firming and storage that smooths the group's renewable output and backed 2024 EBITDA contribution of ~€420m from hydro-generation across Portugal and Spain.

Operating in a mature Iberian market with high entry barriers, these assets generate predictable cash flows and supported EDP Group’s 2024 free cash flow, reducing financing stress and volatility.

Hydro acts as a natural hedge to wind and solar intermittency, enabling reliable offtaker delivery and optimizing ≈1.6 GW of dispatchable capacity for intraday balancing.

- ~€420m hydro EBITDA (2024)

- ≈1.6 GW dispatchable capacity

- Mature Iberian market, high barriers to entry

- Stabilizes renewable output, supports group FCF

Long-term Contracted PPAs

EDP Renováveis (EDPR) bases cash flows on long-term power purchase agreements (PPAs) covering the bulk of its generation, giving multi-decade revenue visibility and low market exposure.

By 2025 EDPR has signed over 15 GW of PPAs globally, securing predictable income with minimal marketing or placement costs and supporting stable free cash flow.

These contracted revenues underpin EDPR’s A-grade credit profile, enabling reliable debt service and steady dividend distributions to shareholders.

- 15+ GW signed PPAs (2025)

- Multi-decade revenue visibility

- Low incremental sales costs

- A-rated credit supporting dividends

EDPR: US wind & Iberian solar/hydro fuel €1.2–1.4bn FCF, €2bn asset rotation, 3.8% yield

Onshore US wind (≈12 GW) and Iberian solar/hydro are EDPR cash cows, delivering ~€1.2–1.4bn FCF (2024–25) plus ~€420m hydro EBITDA (2024); 15+ GW PPAs provide multi-decade revenue visibility and support a ~3.8% 2025 dividend yield; asset rotation raised ~€2.0bn in 2025 toward a €7.0bn 2026 target.

| Metric | Value (2024–25) |

|---|---|

| US onshore capacity | ≈12 GW |

| Signed PPAs | 15+ GW |

| FCF contribution | €1.2–1.4bn |

| Hydro EBITDA | ≈€420m |

| Asset sales 2025 | €2.0bn |

| Rotation target | €7.0bn |

Delivered as Shown

EDP Renovaveis BCG Matrix

The file you're previewing on this page is the final EDP Renováveis BCG Matrix you'll receive after purchase—no watermarks or demo content, just a fully formatted, ready-to-use strategic report designed for investor and management clarity.

This preview is the exact same BCG Matrix document delivered post-purchase, built with market-backed analysis and clear positioning of EDP Renováveis’ business units for immediate use in presentations or planning.

What you see is the actual file available upon payment; once purchased you’ll get the full editable report ready for printing, sharing, or integration into your financial models—no surprises, no revisions needed.