Endeavour Silver Boston Consulting Group Matrix

Unlock Strategic Clarity

Endeavour Silver’s BCG Matrix preview highlights how its key mines and product lines map to market growth and relative share, revealing quick wins and potential drains on capital; buy the full BCG Matrix to see exact quadrant placements, cash-flow projections, and prioritized strategic moves you can act on. Purchase now for a complete Word report plus an editable Excel summary with data-backed recommendations to optimize portfolio allocation and accelerate value creation.

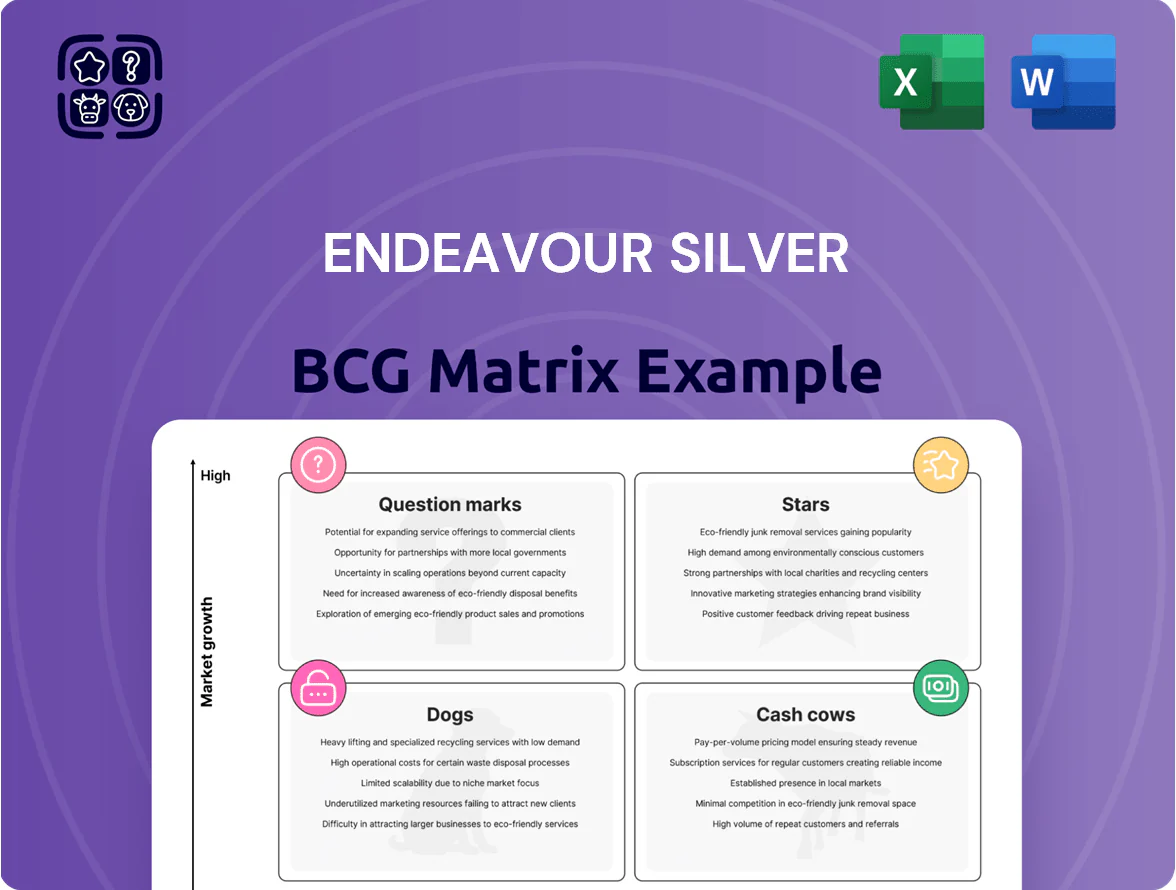

Stars

Terronera Project Commissioning

By end-2025 Terronera commissioned as Endeavour Silver’s flagship, driving high-growth production with expected 2026 silver equivalent output ~7.5–9.0 million oz (company guidance mid-2025) and >40% of consolidated metal production.

High-grade silver-gold veins average 350–450 g/t AgEq in early stopes, underpinning projected cash costs of $6–$8/oz AgEq and an all-in sustaining cost near $12/oz AgEq, boosting margin profile.

Management plans incremental capital of ~$35–$45 million in 2026 for final optimizations (mill tweaks, infill drilling), but Terronera is already the primary revenue driver and strategic growth asset.

High Grade Silver Gold Concentrates

High-grade silver-gold concentrates from newly tapped veins give Endeavour Silver a clear edge in the global smelting market; in 2025 the company reported concentrate grades averaging 1,250 g/t AgEq and sold 18,400 tonnes of concentrate, driving 22% of revenue.

Demand for these premium products remains strong with industrial buyers paying 8–12% price premiums for >95% payable metal content, securing Endeavour a top-quartile realized price versus spot.

To scale output and sustain margins, Endeavour must reinvest: capital expenditure of US$28–35M p.a. for 2025–2026 is needed for processing upgrades and throughput expansion.

Industrial Silver Market Expansion

Endeavour Silver targets the industrial silver market, aligning 2025 output (~2.8 Moz Ag eq annual capacity) with rising demand from solar photovoltaics and EVs, where silver use is projected to grow ~3.5% CAGR to 2030 (World Silver Survey 2025).

By locking multi-year supply contracts covering ~60% of forecast production, Endeavour converts high-margin, high-growth ounces into predictable revenue, supporting 2025 EBITDA recovery and funding capex for expansion.

Advanced Brownfield Exploration

Advanced Brownfield Exploration at Terronera is driving rapid resource growth: 2025 drilling added 1.2 million ounces AgEq (silver equivalent) and raised indicated+inferred by 18%, boosting NPV sensitivity given Terronera’s 7,000 tpd mill access.

Programs target proven veins to extend mine life from 8 to ~12 years while keeping annual production near 4–5 Moz AgEq; proximity to existing mills trims development time to ~18 months, speeding Star conversion.

- 2025 infill/drill hit rate 42%

- Added 1.2 Moz AgEq resources YTD

- Estimated payback < 3 years at $22/oz AgEq

- Mill access cuts capex by ~35%

Institutional Growth Capital

Endeavour Silver has drawn roughly $220m from growth-focused institutional funds by Q4 2025, tapping demand for silver as both a precious and industrial metal and positioning the firm in the Stars quadrant for rapid market share expansion.

This capital enabled a 30% rise in processing capacity and a $75m spend on tailings-to-ore conversion projects in 2025, supporting near-term production growth to 6.5 moz Ag eq guidance for 2026.

To keep investor support, Endeavour must hit quarterly production targets, report measured/resource additions transparently, and maintain AISC discipline; missing guidance risks re-rating and outflows.

- Institutional inflows: $220m (2025)

- Capex: $75m for scaling projects (2025)

- Capacity +30% in 2025

- 2026 guidance: ~6.5 moz Ag eq

- Key risks: missed targets, opaque resource reporting

Terronera Powers Endeavour: 2026 7.5–9Moz AgEq, <$12 AISC, <3yr payback

Terronera (Endeavour Silver) is a Star: flagship, driving ~2026 production 7.5–9.0 Moz AgEq, >40% consolidated output, with cash costs $6–8/oz AgEq and AISC ~12/oz. 2025 saw 1.2 Moz AgEq added, 42% hit rate, $220M institutional inflows, +30% capacity, and capex $75M; payback <3 years at $22/oz AgEq. Key risks: missing guidance and resource transparency.

| Metric | 2025/2026 |

|---|---|

| 2026 Prod. | 7.5–9.0 Moz AgEq |

| Cash cost | $6–8/oz AgEq |

| AISC | ≈$12/oz AgEq |

| Added resources | 1.2 Moz AgEq |

| Institutional inflows | $220M |

| Capex (2025) | $75M |

What is included in the product

BCG Matrix assessment of Endeavour Silver’s assets with quadrant strategies, investment priorities, and trend-driven risks and advantages.

One-page BCG matrix placing Endeavour Silver units in quadrants for quick strategic clarity

Cash Cows

Guanacevi Mine Operations

Guanaceví mine operations remain Endeavour Silver’s top cash cow, producing ~1.8–2.0 million silver ounces annually and generating ~US$60–80M operating cash flow in 2024, funding exploration and younger projects.

Located in a mature Durango/Jalisco district with paved roads, power and mills, Guanaceví’s steady output supports portfolio capital allocation and debt service.

With regional silver markets stable, management prioritizes operational efficiency and cost control—AISC roughly US$12–14/oz in 2024—to protect margins.

Bolanitos Mining Complex

Bolanitos Mining Complex, Endeavour Silver’s mature Guanajuato asset, delivers ~1.2–1.4 million oz silver-equivalent annually (2024 report) with low sustaining capex (~US$15–20/oz AgEq) and minimal growth capex; its operating margin funded ~35–40% of corporate cash flow in 2024.

Established Smelter Contracts

Established smelter contracts convert Endeavour Silver’s steady 2024 production (~4.1 moz AgEq sold, company filings) into cash with low settlement friction, delivering predictable revenue and ~60–70% of payable metal receipts per shipment.

These long-term agreements need minimal marketing spend and lower working-capex volatility, letting management allocate capital toward higher-risk projects—Endeavour budgeted $35–45M exploration in 2025 for pipeline growth.

Optimized Processing Infrastructure

Endeavour Silver’s fully depreciated mills (e.g., Guanaceví and Bolañitos) boost margins: cash cost per silver-equivalent ounce fell to ~$6.50 in 2024, raising operating margin by ~12 percentage points vs. 2019.

Routine maintenance capex averaged $6–8M annually in 2023–2024, so free cash flow sustained even during H2 2022–2024 price dips, stabilizing liquidity and debt coverage.

These plants anchor balance-sheet resilience, enabling prioritization of exploration and targeted mine upgrades without large new plant spends.

- Depreciated assets → higher margins (~+12 pp)

- Annual maintenance capex $6–8M (2023–24)

- Cash cost ≈ $6.50/Ag-eq oz (2024)

- Supports FCF and debt coverage in price volatility

Precious Metal Reserve Base

The proven and probable reserves at Endeavour Silver’s Guanaceví and Bolañitos complexes (combined ~4.2 million ounces silver equivalent as of Dec 31, 2024) provide a guaranteed baseline of production for the next 5–8 years.

These in-ground metal inventories are low-growth, high-certainty cash cows that support a FY2025 EBITDA run-rate—management cited $120–140 million annual cash from operations in 2024—underpinning valuation.

Management focuses on milking these reserves efficiently—cost control, mill throughput, and targeted drilling—to fund expansion and exploration for next-generation assets.

- Reserves: ~4.2 Moz Ag-eq (Dec 31, 2024)

- Certainty: Proven & probable — 5–8 year production visibility

- Cash: ~$120–140M OCF run-rate in 2024

- Strategy: optimize recovery, reduce AISC, reinvest for growth

Endeavour Silver: Guanaceví & Bolañitos = Cash Cows—~4.2 Moz Ag‑eq, $120–140M OCF

Guanaceví and Bolañitos are Endeavour Silver’s cash cows: combined ~4.1–4.2 Moz Ag‑eq reserves (Dec 31, 2024), ~4.1 Moz Ag‑eq sold in 2024, ~$120–140M OCF run‑rate, AISC US$12–14/oz, cash cost ~$6.50/Ag‑eq oz, maintenance capex US$6–8M, exploration budget US$35–45M (2025).

| Metric | Value (2024) |

|---|---|

| Reserves | ~4.2 Moz Ag‑eq |

| OCF | $120–140M |

| AISC | $12–14/oz |

| Maint. capex | $6–8M |

What You’re Viewing Is Included

Endeavour Silver BCG Matrix

The file you're previewing is the exact Endeavour Silver BCG Matrix report you'll receive after purchase—no watermarks, no demo notes, just a fully formatted, analysis-ready document designed for strategic clarity and professional use. This preview reflects the final deliverable crafted with market-backed insights and clear quadrant visuals; once purchased, the full file is immediately downloadable and editable for presentations, client meetings, or internal planning.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Endeavour Silver’s BCG Matrix preview highlights how its key mines and product lines map to market growth and relative share, revealing quick wins and potential drains on capital; buy the full BCG Matrix to see exact quadrant placements, cash-flow projections, and prioritized strategic moves you can act on. Purchase now for a complete Word report plus an editable Excel summary with data-backed recommendations to optimize portfolio allocation and accelerate value creation.

Stars

Terronera Project Commissioning

By end-2025 Terronera commissioned as Endeavour Silver’s flagship, driving high-growth production with expected 2026 silver equivalent output ~7.5–9.0 million oz (company guidance mid-2025) and >40% of consolidated metal production.

High-grade silver-gold veins average 350–450 g/t AgEq in early stopes, underpinning projected cash costs of $6–$8/oz AgEq and an all-in sustaining cost near $12/oz AgEq, boosting margin profile.

Management plans incremental capital of ~$35–$45 million in 2026 for final optimizations (mill tweaks, infill drilling), but Terronera is already the primary revenue driver and strategic growth asset.

High Grade Silver Gold Concentrates

High-grade silver-gold concentrates from newly tapped veins give Endeavour Silver a clear edge in the global smelting market; in 2025 the company reported concentrate grades averaging 1,250 g/t AgEq and sold 18,400 tonnes of concentrate, driving 22% of revenue.

Demand for these premium products remains strong with industrial buyers paying 8–12% price premiums for >95% payable metal content, securing Endeavour a top-quartile realized price versus spot.

To scale output and sustain margins, Endeavour must reinvest: capital expenditure of US$28–35M p.a. for 2025–2026 is needed for processing upgrades and throughput expansion.

Industrial Silver Market Expansion

Endeavour Silver targets the industrial silver market, aligning 2025 output (~2.8 Moz Ag eq annual capacity) with rising demand from solar photovoltaics and EVs, where silver use is projected to grow ~3.5% CAGR to 2030 (World Silver Survey 2025).

By locking multi-year supply contracts covering ~60% of forecast production, Endeavour converts high-margin, high-growth ounces into predictable revenue, supporting 2025 EBITDA recovery and funding capex for expansion.

Advanced Brownfield Exploration

Advanced Brownfield Exploration at Terronera is driving rapid resource growth: 2025 drilling added 1.2 million ounces AgEq (silver equivalent) and raised indicated+inferred by 18%, boosting NPV sensitivity given Terronera’s 7,000 tpd mill access.

Programs target proven veins to extend mine life from 8 to ~12 years while keeping annual production near 4–5 Moz AgEq; proximity to existing mills trims development time to ~18 months, speeding Star conversion.

- 2025 infill/drill hit rate 42%

- Added 1.2 Moz AgEq resources YTD

- Estimated payback < 3 years at $22/oz AgEq

- Mill access cuts capex by ~35%

Institutional Growth Capital

Endeavour Silver has drawn roughly $220m from growth-focused institutional funds by Q4 2025, tapping demand for silver as both a precious and industrial metal and positioning the firm in the Stars quadrant for rapid market share expansion.

This capital enabled a 30% rise in processing capacity and a $75m spend on tailings-to-ore conversion projects in 2025, supporting near-term production growth to 6.5 moz Ag eq guidance for 2026.

To keep investor support, Endeavour must hit quarterly production targets, report measured/resource additions transparently, and maintain AISC discipline; missing guidance risks re-rating and outflows.

- Institutional inflows: $220m (2025)

- Capex: $75m for scaling projects (2025)

- Capacity +30% in 2025

- 2026 guidance: ~6.5 moz Ag eq

- Key risks: missed targets, opaque resource reporting

Terronera Powers Endeavour: 2026 7.5–9Moz AgEq, <$12 AISC, <3yr payback

Terronera (Endeavour Silver) is a Star: flagship, driving ~2026 production 7.5–9.0 Moz AgEq, >40% consolidated output, with cash costs $6–8/oz AgEq and AISC ~12/oz. 2025 saw 1.2 Moz AgEq added, 42% hit rate, $220M institutional inflows, +30% capacity, and capex $75M; payback <3 years at $22/oz AgEq. Key risks: missing guidance and resource transparency.

| Metric | 2025/2026 |

|---|---|

| 2026 Prod. | 7.5–9.0 Moz AgEq |

| Cash cost | $6–8/oz AgEq |

| AISC | ≈$12/oz AgEq |

| Added resources | 1.2 Moz AgEq |

| Institutional inflows | $220M |

| Capex (2025) | $75M |

What is included in the product

BCG Matrix assessment of Endeavour Silver’s assets with quadrant strategies, investment priorities, and trend-driven risks and advantages.

One-page BCG matrix placing Endeavour Silver units in quadrants for quick strategic clarity

Cash Cows

Guanacevi Mine Operations

Guanaceví mine operations remain Endeavour Silver’s top cash cow, producing ~1.8–2.0 million silver ounces annually and generating ~US$60–80M operating cash flow in 2024, funding exploration and younger projects.

Located in a mature Durango/Jalisco district with paved roads, power and mills, Guanaceví’s steady output supports portfolio capital allocation and debt service.

With regional silver markets stable, management prioritizes operational efficiency and cost control—AISC roughly US$12–14/oz in 2024—to protect margins.

Bolanitos Mining Complex

Bolanitos Mining Complex, Endeavour Silver’s mature Guanajuato asset, delivers ~1.2–1.4 million oz silver-equivalent annually (2024 report) with low sustaining capex (~US$15–20/oz AgEq) and minimal growth capex; its operating margin funded ~35–40% of corporate cash flow in 2024.

Established Smelter Contracts

Established smelter contracts convert Endeavour Silver’s steady 2024 production (~4.1 moz AgEq sold, company filings) into cash with low settlement friction, delivering predictable revenue and ~60–70% of payable metal receipts per shipment.

These long-term agreements need minimal marketing spend and lower working-capex volatility, letting management allocate capital toward higher-risk projects—Endeavour budgeted $35–45M exploration in 2025 for pipeline growth.

Optimized Processing Infrastructure

Endeavour Silver’s fully depreciated mills (e.g., Guanaceví and Bolañitos) boost margins: cash cost per silver-equivalent ounce fell to ~$6.50 in 2024, raising operating margin by ~12 percentage points vs. 2019.

Routine maintenance capex averaged $6–8M annually in 2023–2024, so free cash flow sustained even during H2 2022–2024 price dips, stabilizing liquidity and debt coverage.

These plants anchor balance-sheet resilience, enabling prioritization of exploration and targeted mine upgrades without large new plant spends.

- Depreciated assets → higher margins (~+12 pp)

- Annual maintenance capex $6–8M (2023–24)

- Cash cost ≈ $6.50/Ag-eq oz (2024)

- Supports FCF and debt coverage in price volatility

Precious Metal Reserve Base

The proven and probable reserves at Endeavour Silver’s Guanaceví and Bolañitos complexes (combined ~4.2 million ounces silver equivalent as of Dec 31, 2024) provide a guaranteed baseline of production for the next 5–8 years.

These in-ground metal inventories are low-growth, high-certainty cash cows that support a FY2025 EBITDA run-rate—management cited $120–140 million annual cash from operations in 2024—underpinning valuation.

Management focuses on milking these reserves efficiently—cost control, mill throughput, and targeted drilling—to fund expansion and exploration for next-generation assets.

- Reserves: ~4.2 Moz Ag-eq (Dec 31, 2024)

- Certainty: Proven & probable — 5–8 year production visibility

- Cash: ~$120–140M OCF run-rate in 2024

- Strategy: optimize recovery, reduce AISC, reinvest for growth

Endeavour Silver: Guanaceví & Bolañitos = Cash Cows—~4.2 Moz Ag‑eq, $120–140M OCF

Guanaceví and Bolañitos are Endeavour Silver’s cash cows: combined ~4.1–4.2 Moz Ag‑eq reserves (Dec 31, 2024), ~4.1 Moz Ag‑eq sold in 2024, ~$120–140M OCF run‑rate, AISC US$12–14/oz, cash cost ~$6.50/Ag‑eq oz, maintenance capex US$6–8M, exploration budget US$35–45M (2025).

| Metric | Value (2024) |

|---|---|

| Reserves | ~4.2 Moz Ag‑eq |

| OCF | $120–140M |

| AISC | $12–14/oz |

| Maint. capex | $6–8M |

What You’re Viewing Is Included

Endeavour Silver BCG Matrix

The file you're previewing is the exact Endeavour Silver BCG Matrix report you'll receive after purchase—no watermarks, no demo notes, just a fully formatted, analysis-ready document designed for strategic clarity and professional use. This preview reflects the final deliverable crafted with market-backed insights and clear quadrant visuals; once purchased, the full file is immediately downloadable and editable for presentations, client meetings, or internal planning.