EirGenix Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

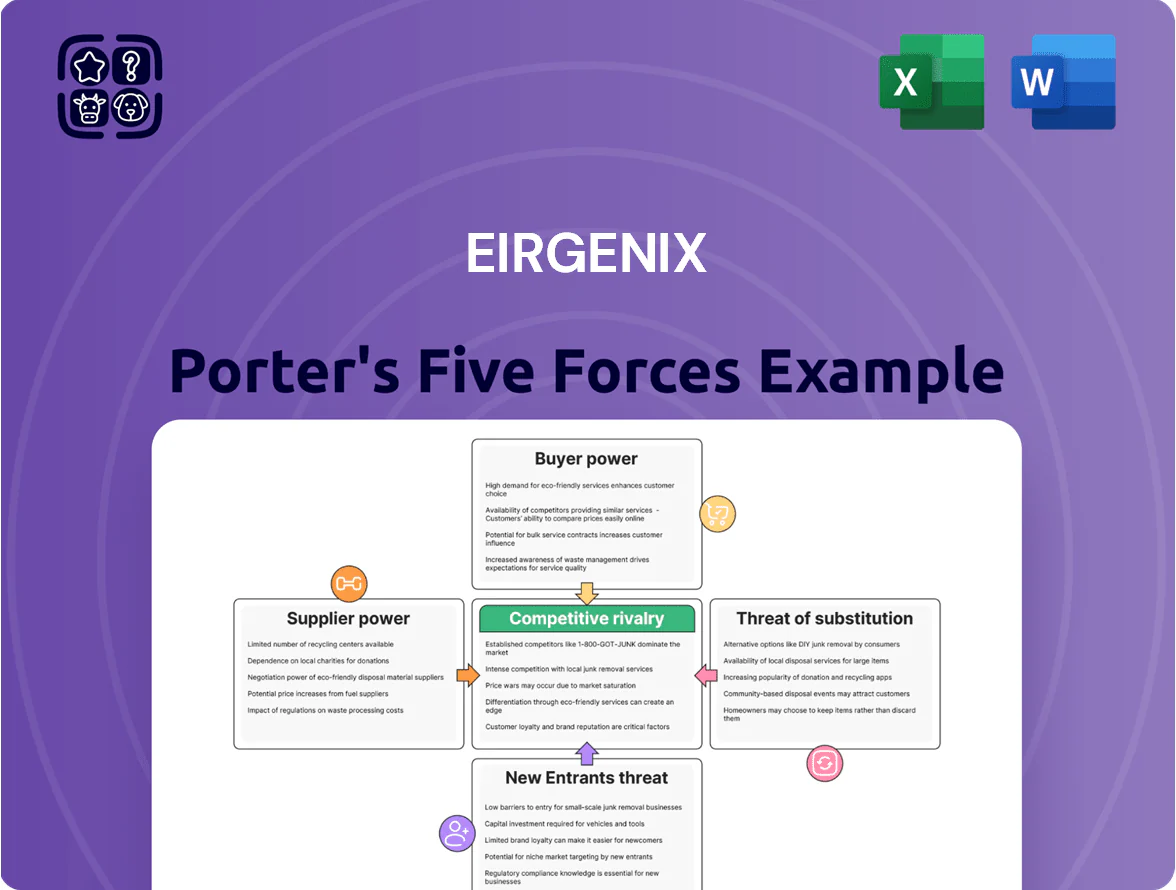

EirGenix faces moderate supplier power and high innovation-driven rivalry, while regulatory hurdles and niche patient demand moderate new entrants and substitutes; pricing pressure from larger pharma and reimbursement dynamics are key risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore EirGenix’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Bioprocessing Inputs

The production of biologics needs niche inputs—culture media, affinity resins, single-use bioreactor bags—sourced from few suppliers; Thermo Fisher Scientific and Merck KGaA together held roughly 40–50% global market share in bioprocess consumables in 2024, giving them pricing power.

This supplier concentration lets vendors push 5–15% annual price increases; EirGenix must secure multi-year contracts and dual-source plans to avoid supply shocks that could delay batches and cost millions.

High Switching Costs for Validated Materials

Once a process is validated by regulators like the FDA or EMA, switching suppliers often forces re-validation with typical costs of $0.5–2.0M and 6–18 months of delay, creating technical lock-in for EirGenix. This lock-in raises supplier bargaining power because swapping critical reagents risks regulatory non-compliance and market access delays. As of 2025, specialty reagent suppliers commonly secure 5–15% annual price premiums and multi-year contracts versus CDMO peers. That long-term pricing power pressures EirGenix’s margins and procurement flexibility.

Scarcity of Specialized Biopharma Equipment

Long lead times for high-end cGMP equipment and automation—often 9–18 months from a handful of engineering firms—leave EirGenix exposed as it scales to meet projected 2025 demand of ~25% capacity growth; vendors command premium pricing tiers, with OEM markups of 15–40% during peak ordering, and global biotech capacity expansions in 2023–25 drove backlog increases of ~30%, raising delivery and cost risk for EirGenix.

Reliance on Specialized Technical Talent

The global pool of skilled biologics scientists is scarce; a 2024 Nature Biotechnology survey found 62% of firms report talent shortages, raising hiring costs by ~18% year-over-year.

As a Taiwan-based firm, EirGenix competes with local peers and multinationals like Roche and Pfizer for this labor, increasing turnover and recruitment spend.

Top-tier candidates in 2024 commanded median total compensation 25–40% above industry averages, giving them strong bargaining power.

- 62% of firms report talent shortages (Nature Biotech 2024)

- Hiring costs +18% YoY (2024 industry data)

- Top talent pay +25–40% vs industry averages (2024)

Energy and Utility Requirements for Sterile Facilities

Maintaining cGMP sterile facilities demands continuous HVAC and WFI (water-for-injection) systems that can consume 20–40 MW for large plants and drive utility bills to 5–10% of manufacturing OPEX; that creates lock-in to local high-reliability suppliers.

Energy is a commodity, but bespoke uptime, redundancy, and quality specs force dependency on regional utility firms and on-site backup investments, raising capex by 8–12%.

In APAC, 2024 wholesale electricity price swings (±15–25%) directly shift margins for large-scale biologics sites; a 20% price jump can cut EBITDA by ~3–6 percentage points.

- 20–40 MW typical load for large sterile plants

- Utilities ≈5–10% of OPEX; on-site systems add 8–12% capex

- APAC price volatility ±15–25% (2024); 20% rise → EBITDA −3–6 pp

Supplier dominance, rising costs and shortages squeeze EirGenix margins

Supplier power is high: a few vendors (Thermo Fisher, Merck) held ~40–50% of bioprocess consumables in 2024, allowing 5–15% annual price increases and multi-year contract leverage; switching suppliers post-validation costs $0.5–2.0M and 6–18 months. Long equipment lead times (9–18 months) and OEM markups (15–40%) plus talent shortages (62% firms report, hiring +18% YoY; top pay +25–40%) and utility volatility (±15–25%) squeeze EirGenix margins.

| Metric | 2024–25 Value |

|---|---|

| Consumables market share | 40–50% |

| Supplier price rise | 5–15% YoY |

| Switching cost/time | $0.5–2.0M; 6–18m |

| Equipment lead time | 9–18m; OEM +15–40% |

| Talent shortage | 62% firms; hiring +18% YoY; pay +25–40% |

| Utility volatility | ±15–25%; 20% ↑ → EBITDA −3–6pp |

What is included in the product

Tailored Porter’s Five Forces analysis of EirGenix that uncovers competitive drivers, buyer and supplier power, substitute threats, and entry barriers to assess pricing leverage and strategic vulnerabilities within its biotech/pharma niche.

A concise, one-sheet Porter's Five Forces summary for EirGenix—ideal for fast strategic decisions and slide-ready use.

Customers Bargaining Power

Consolidation of Major Pharmaceutical Clients

Major pharma buyers often concentrate spending: top 5 pharma firms accounted for ~35% of global CDMO spend in 2024, so they push volume to a few partners for scale. These high-volume clients use that scale to demand price cuts and softer liability terms, cutting per-unit prices by 10–25% on big contracts. EirGenix must diversify so no single client exceeds ~15% of revenue to limit bargaining leverage.

High Technical Switching Costs for Biologics

Transferring biologics manufacturing from EirGenix to another CDMO can take 12–24+ months and cost $5–20M per product, plus regulatory bridging studies, so once commercialized customers face high switching costs and reduced immediate bargaining power.

Still, during bidding and clinical-stage transitions clients wield strong leverage: ~60–75% of contract value and design terms are negotiated then, and customers can drive price concessions before tech transfer locks them in.

Demand for Integrated End-to-End Services

Modern biotech clients now prefer end-to-end partners handling cell line development through fill-and-finish; 68% of biopharma outsourcing deals in 2024 favored vertically integrated CDMOs, so buyers can and do insist on full-service packages before signing multi-year contracts. EirGenix must keep investing—R&D and capacity capex rising ~12% annually industry-wide—to maintain service breadth and win these high-value, long-term agreements.

Price Sensitivity in the Biosimilar Market

EirGenix faces strong customer price sensitivity in biosimilars: global biosimilar sales reached $15.6B in 2024, with price discounts versus reference biologics often 30–70%, forcing developers to cut costs.

Clients demand low COGS, so EirGenix must boost process yields and cut downstream expenses; contract margins compress as average biosimilar development costs near $100–200M per asset.

- Global biosimilar market $15.6B (2024)

- Typical price discounts 30–70%

- Development cost per biosimilar $100–200M

- Pressure: lower COGS, higher yields

Availability of Alternative Global CDMOs

The global CDMO market exceeded $180 billion in 2024, with major hubs in Europe, North America, and Asia, so customers face many viable suppliers.

EirGenix has regional strengths, but buyers can credibly threaten switching to large rivals such as Samsung Biologics (2024 revenue $7.6B) or WuXi Biologics (2024 revenue $2.8B) to extract better pricing or terms.

High transparency, public capacity announcements, and well-funded pharma clients keep customer bargaining power elevated, especially for large-volume contracts.

- Global CDMO market ~$180B (2024)

- Samsung Biologics rev $7.6B (2024)

- WuXi Biologics rev $2.8B (2024)

- Multiple hubs = high buyer leverage

Buyers Rule: Top Clients, Biosimilars & Giants Crush CDMO Margins

Customers hold high bargaining power: top buyers drove ~35% of CDMO spend (2024), switching costs are $5–20M and 12–24+ months, bidding captures ~60–75% of commercial terms, biosimilar price pressure (30–70% discounts) and a $180B CDMO market with rivals (Samsung Biologics rev $7.6B, WuXi $2.8B) compress margins.

| Metric | 2024 value |

|---|---|

| Top5 share of CDMO spend | ~35% |

| Switch cost per product | $5–20M; 12–24+ months |

| Bid negotiation share | 60–75% |

| Global CDMO market | $180B |

| Biosimilar discounts | 30–70% |

| Samsung Biologics rev | $7.6B |

| WuXi Biologics rev | $2.8B |

Preview Before You Purchase

EirGenix Porter's Five Forces Analysis

This preview shows the exact EirGenix Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

EirGenix faces moderate supplier power and high innovation-driven rivalry, while regulatory hurdles and niche patient demand moderate new entrants and substitutes; pricing pressure from larger pharma and reimbursement dynamics are key risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore EirGenix’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Bioprocessing Inputs

The production of biologics needs niche inputs—culture media, affinity resins, single-use bioreactor bags—sourced from few suppliers; Thermo Fisher Scientific and Merck KGaA together held roughly 40–50% global market share in bioprocess consumables in 2024, giving them pricing power.

This supplier concentration lets vendors push 5–15% annual price increases; EirGenix must secure multi-year contracts and dual-source plans to avoid supply shocks that could delay batches and cost millions.

High Switching Costs for Validated Materials

Once a process is validated by regulators like the FDA or EMA, switching suppliers often forces re-validation with typical costs of $0.5–2.0M and 6–18 months of delay, creating technical lock-in for EirGenix. This lock-in raises supplier bargaining power because swapping critical reagents risks regulatory non-compliance and market access delays. As of 2025, specialty reagent suppliers commonly secure 5–15% annual price premiums and multi-year contracts versus CDMO peers. That long-term pricing power pressures EirGenix’s margins and procurement flexibility.

Scarcity of Specialized Biopharma Equipment

Long lead times for high-end cGMP equipment and automation—often 9–18 months from a handful of engineering firms—leave EirGenix exposed as it scales to meet projected 2025 demand of ~25% capacity growth; vendors command premium pricing tiers, with OEM markups of 15–40% during peak ordering, and global biotech capacity expansions in 2023–25 drove backlog increases of ~30%, raising delivery and cost risk for EirGenix.

Reliance on Specialized Technical Talent

The global pool of skilled biologics scientists is scarce; a 2024 Nature Biotechnology survey found 62% of firms report talent shortages, raising hiring costs by ~18% year-over-year.

As a Taiwan-based firm, EirGenix competes with local peers and multinationals like Roche and Pfizer for this labor, increasing turnover and recruitment spend.

Top-tier candidates in 2024 commanded median total compensation 25–40% above industry averages, giving them strong bargaining power.

- 62% of firms report talent shortages (Nature Biotech 2024)

- Hiring costs +18% YoY (2024 industry data)

- Top talent pay +25–40% vs industry averages (2024)

Energy and Utility Requirements for Sterile Facilities

Maintaining cGMP sterile facilities demands continuous HVAC and WFI (water-for-injection) systems that can consume 20–40 MW for large plants and drive utility bills to 5–10% of manufacturing OPEX; that creates lock-in to local high-reliability suppliers.

Energy is a commodity, but bespoke uptime, redundancy, and quality specs force dependency on regional utility firms and on-site backup investments, raising capex by 8–12%.

In APAC, 2024 wholesale electricity price swings (±15–25%) directly shift margins for large-scale biologics sites; a 20% price jump can cut EBITDA by ~3–6 percentage points.

- 20–40 MW typical load for large sterile plants

- Utilities ≈5–10% of OPEX; on-site systems add 8–12% capex

- APAC price volatility ±15–25% (2024); 20% rise → EBITDA −3–6 pp

Supplier dominance, rising costs and shortages squeeze EirGenix margins

Supplier power is high: a few vendors (Thermo Fisher, Merck) held ~40–50% of bioprocess consumables in 2024, allowing 5–15% annual price increases and multi-year contract leverage; switching suppliers post-validation costs $0.5–2.0M and 6–18 months. Long equipment lead times (9–18 months) and OEM markups (15–40%) plus talent shortages (62% firms report, hiring +18% YoY; top pay +25–40%) and utility volatility (±15–25%) squeeze EirGenix margins.

| Metric | 2024–25 Value |

|---|---|

| Consumables market share | 40–50% |

| Supplier price rise | 5–15% YoY |

| Switching cost/time | $0.5–2.0M; 6–18m |

| Equipment lead time | 9–18m; OEM +15–40% |

| Talent shortage | 62% firms; hiring +18% YoY; pay +25–40% |

| Utility volatility | ±15–25%; 20% ↑ → EBITDA −3–6pp |

What is included in the product

Tailored Porter’s Five Forces analysis of EirGenix that uncovers competitive drivers, buyer and supplier power, substitute threats, and entry barriers to assess pricing leverage and strategic vulnerabilities within its biotech/pharma niche.

A concise, one-sheet Porter's Five Forces summary for EirGenix—ideal for fast strategic decisions and slide-ready use.

Customers Bargaining Power

Consolidation of Major Pharmaceutical Clients

Major pharma buyers often concentrate spending: top 5 pharma firms accounted for ~35% of global CDMO spend in 2024, so they push volume to a few partners for scale. These high-volume clients use that scale to demand price cuts and softer liability terms, cutting per-unit prices by 10–25% on big contracts. EirGenix must diversify so no single client exceeds ~15% of revenue to limit bargaining leverage.

High Technical Switching Costs for Biologics

Transferring biologics manufacturing from EirGenix to another CDMO can take 12–24+ months and cost $5–20M per product, plus regulatory bridging studies, so once commercialized customers face high switching costs and reduced immediate bargaining power.

Still, during bidding and clinical-stage transitions clients wield strong leverage: ~60–75% of contract value and design terms are negotiated then, and customers can drive price concessions before tech transfer locks them in.

Demand for Integrated End-to-End Services

Modern biotech clients now prefer end-to-end partners handling cell line development through fill-and-finish; 68% of biopharma outsourcing deals in 2024 favored vertically integrated CDMOs, so buyers can and do insist on full-service packages before signing multi-year contracts. EirGenix must keep investing—R&D and capacity capex rising ~12% annually industry-wide—to maintain service breadth and win these high-value, long-term agreements.

Price Sensitivity in the Biosimilar Market

EirGenix faces strong customer price sensitivity in biosimilars: global biosimilar sales reached $15.6B in 2024, with price discounts versus reference biologics often 30–70%, forcing developers to cut costs.

Clients demand low COGS, so EirGenix must boost process yields and cut downstream expenses; contract margins compress as average biosimilar development costs near $100–200M per asset.

- Global biosimilar market $15.6B (2024)

- Typical price discounts 30–70%

- Development cost per biosimilar $100–200M

- Pressure: lower COGS, higher yields

Availability of Alternative Global CDMOs

The global CDMO market exceeded $180 billion in 2024, with major hubs in Europe, North America, and Asia, so customers face many viable suppliers.

EirGenix has regional strengths, but buyers can credibly threaten switching to large rivals such as Samsung Biologics (2024 revenue $7.6B) or WuXi Biologics (2024 revenue $2.8B) to extract better pricing or terms.

High transparency, public capacity announcements, and well-funded pharma clients keep customer bargaining power elevated, especially for large-volume contracts.

- Global CDMO market ~$180B (2024)

- Samsung Biologics rev $7.6B (2024)

- WuXi Biologics rev $2.8B (2024)

- Multiple hubs = high buyer leverage

Buyers Rule: Top Clients, Biosimilars & Giants Crush CDMO Margins

Customers hold high bargaining power: top buyers drove ~35% of CDMO spend (2024), switching costs are $5–20M and 12–24+ months, bidding captures ~60–75% of commercial terms, biosimilar price pressure (30–70% discounts) and a $180B CDMO market with rivals (Samsung Biologics rev $7.6B, WuXi $2.8B) compress margins.

| Metric | 2024 value |

|---|---|

| Top5 share of CDMO spend | ~35% |

| Switch cost per product | $5–20M; 12–24+ months |

| Bid negotiation share | 60–75% |

| Global CDMO market | $180B |

| Biosimilar discounts | 30–70% |

| Samsung Biologics rev | $7.6B |

| WuXi Biologics rev | $2.8B |

Preview Before You Purchase

EirGenix Porter's Five Forces Analysis

This preview shows the exact EirGenix Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready for download.