Electrotherm Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

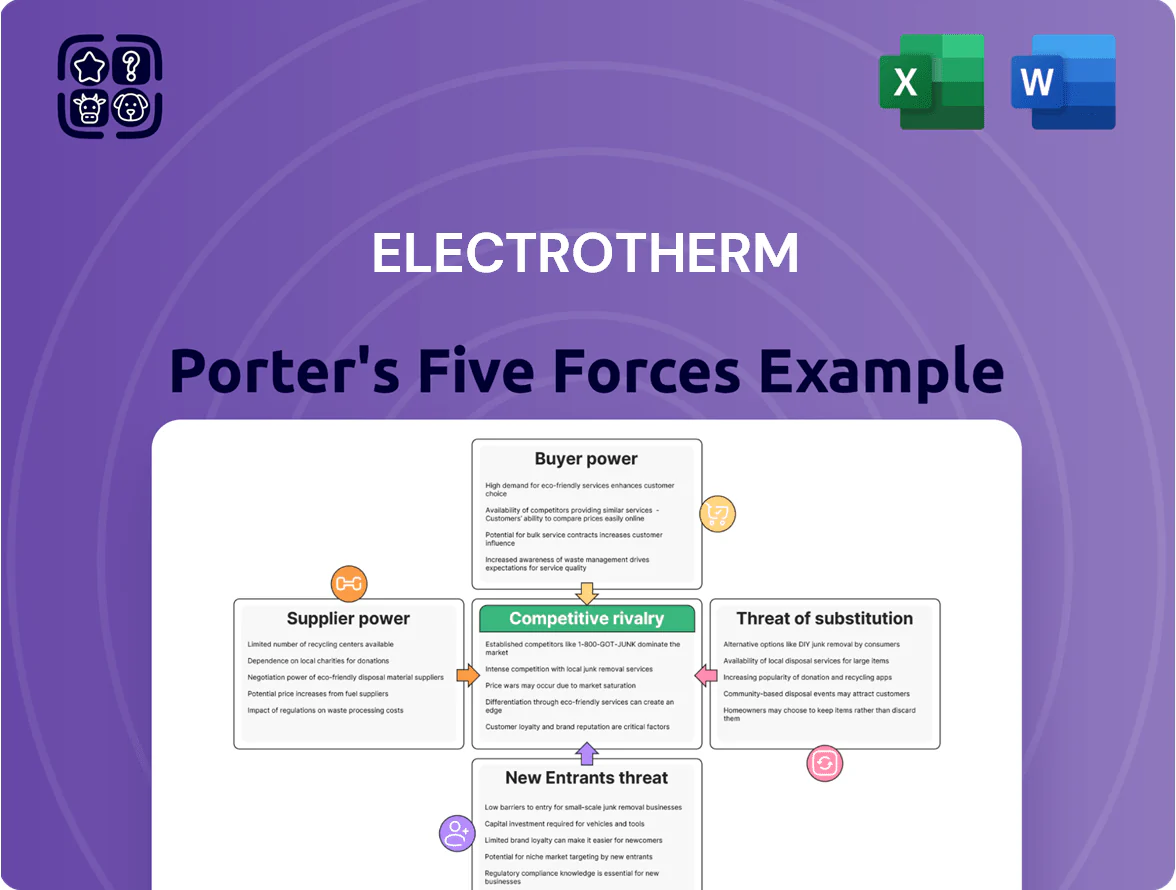

Electrotherm faces moderate supplier and buyer power, with capital-intensive barriers limiting new entrants but rising substitute and competitive pressures from global OEMs; growth hinges on technology upgrades and downstream integration. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Electrotherm’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of raw material inputs

Electrotherm depends on iron ore, coal and scrap for steel and pipes; by late 2025 iron ore spot rose ~18% year-on-year and thermal coal prices were ~25% higher, keeping pricing power with large miners and exporters like Vale and Glencore.

Mining-related environmental curbs and shipping bottlenecks tightened supply, forcing Electrotherm to absorb input cost swings and operate with thin EBITDA margins (steel sector median ~6% in 2024–25), limiting its leverage over base commodity prices.

Specialized electronic components for furnaces

Manufacturing induction melting furnaces depends on high-end power electronics and specialized copper parts from a small set of global vendors, giving suppliers strong leverage; industry surveys show >60% of critical components are single- or dual-sourced as of 2024. These proprietary technologies directly affect Electrotherm’s product performance and margins, with supplier-driven price moves potentially raising component costs by 8–15% per year. Any supply disruption can halt lines—Electrotherm’s engineering division could face weeks-long delays and cost overruns that eat into FY2025 EBITDA, where components represent ~12% of COGS.

Energy costs and utility dependency

Electrotherm’s steel and heavy-machinery plants are energy-heavy, so they rely on state utilities and large private suppliers; in India industrial power rates rose ~7% in 2024 and average industrial tariffs hit ~INR 9–11/kWh in 2025, reducing pricing flexibility.

Accelerating energy-transition rules through 2025 raised carbon costs; India’s traded carbon-equivalent compliance estimates add ~INR 0.5–1.0/kg CO2e, making electricity and credits mandatory, externally set inputs.

Because suppliers set tariffs and credit prices, Electrotherm has weak supplier bargaining power, which increases its integrated-solution cost base and compresses margins unless it secures captive renewables or long-term power purchase agreements.

Supplier concentration in the DI pipe segment

Supplier concentration in the DI pipe segment raises bargaining power: high‑purity magnesium and alloy additives are essential to meet ISO 2531 and EN 545 standards, and only a handful of global producers supply >70% of specialty magnesium refined for foundry use as of 2025, letting suppliers set prices and tight delivery windows during infrastructure booms.

That scarcity pushed premium for specialty alloys up ~18% in 2024 vs 2023, increasing Electrotherm’s input cost volatility and forcing longer contractual lead times.

- Few suppliers: >70% supply from top producers (2025)

- Price pressure: specialty alloy premiums +18% in 2024

- Standards impact: ISO 2531 / EN 545 require high purity

- Risk: delivery schedule leverage during infrastructure demand spikes

Logistics and transportation providers

Supply-side consolidation in freight cut global heavy-lift carriers to a handful by 2025, boosting transporters’ pricing power for heavy engineering and bulk steel moves needed by Electrotherm.

International routes saw average heavy-cargo freight rates rise ~22% YoY in 2024–25 on reduced capacity and higher fuel/insurance costs, letting carriers push through surcharges that pressure Electrotherm’s margins.

Long-term contracts and multimodal routing lower exposure, but single-vendor ports or specialist lift providers still create choke points for exports to Europe and Africa.

- Carrier consolidation: few specialist heavy-lift firms by 2025

- Freight rate change: ~+22% YoY (2024–25)

- Key risk: port/lift provider choke points on export lanes

- Mitigation: long-term contracts, multimodal routing

Supplier squeeze: concentrated inputs, surging commodities and energy dent Electrotherm margins

Suppliers hold strong power: key commodities (iron ore, coal, specialty alloys) and critical electronics are concentrated—top producers supply >70% (2025), alloy premiums rose ~18% in 2024, iron ore +18% YoY (late 2025) and coal ~+25% (2025), freight +22% YoY (2024–25); energy tariffs ~INR 9–11/kWh (2025) and components ≈12% of COGS shrink Electrotherm’s margin unless long-term contracts or captive power are secured.

| Item | 2024–25 change | 2025 level |

|---|---|---|

| Alloy premium | +18% YoY | - |

| Iron ore | +18% YoY | - |

| Thermal coal | +25% YoY | - |

| Freight (heavy) | +22% YoY | - |

| Industrial power tariff | +7% (2024) | INR 9–11/kWh |

| Supplier concentration | - | Top suppliers >70% |

What is included in the product

Tailored exclusively for Electrotherm, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats impacting its pricing, profitability, and strategic positioning.

Compact Porter's Five Forces snapshot for Electrotherm—instantly highlights competitive pressures and strategic levers for rapid decision-making.

Customers Bargaining Power

Concentration of large scale infrastructure buyers

A significant share of Electrotherm's ductile iron pipe and EPC revenues—estimated at ~45% in FY2024—comes from state governments and large municipal corporations, which use tender-based procurement that drives prices down; for example, average bid discounts vs. list prices reached 12–18% in 2023 municipal tenders. These buyers can pick among multiple certified suppliers, giving them strong leverage to demand lower prices and tougher payment terms, pressuring margins.

Low switching costs in the steel segment

In TMT bars and basic steel, products are commoditized so buyers switch brands easily; switching costs are near zero for construction and automotive firms. Large buyers compare prices and often choose the lowest bidder—India’s rebar spot market saw a 12% price dispersion in 2024, boosting price sensitivity. This limits Electrotherm’s pricing power and makes sustained price hikes unrealistic without volume loss.

Technical expertise of furnace clients

Electrotherm’s furnace buyers—mainly steelmakers and foundries—have deep process expertise and in 2024 drove >60% of procurement decisions by technical spec and life-cycle cost; they run strict cost-benefit models and push for custom designs and multi-year service contracts, forcing Electrotherm to offer tailored engineering, extended warranties, and performance SLAs, which compresses margins and raises negotiation leverage.

Availability of global alternatives

Industrial buyers for metal-melting solutions can choose domestic firms and global suppliers from Europe and China; global imports accounted for roughly 18% of India’s foundry-equipment market in 2024, widening choice and lowering reliance on any single local maker.

That forces Electrotherm to keep prices tight and invest in tech—R&D spend of 2.1% of revenue would be a benchmark to defend share.

- Global alternatives up — 18% import share (2024)

- Pressure on pricing

- Need for >2% R&D spend

Impact of economic cycles on buyer demand

Buyers in automotive and infrastructure are very rate-sensitive; by Q4 2025 rising borrowing costs cut fixed-asset investment—Indian auto capex fell 12% YoY in H1 2025—so customers defer furnaces and construction, forcing Electrotherm to offer price concessions.

This cyclicality gives buyers timing power: they wait for lower rates or fiscal stimulus before large orders, increasing order volatility and squeezing margins for Electrotherm.

- Auto capex down 12% YoY H1 2025

- Infrastructure project delays up 18% in 2025

- Electrotherm faces higher discounting during slow cycles

Buyers’ leverage squeezes margins—tenders, imports, and auto capex cut drive deep discounts

Buyers wield strong leverage: government tenders (~45% FY2024 revenue) force 12–18% bid discounts; commoditized TMT/rebar showed 12% price dispersion in 2024; furnace customers drove >60% technical procurement in 2024; imports were 18% of foundry-equipment market (2024); auto capex fell 12% YoY H1 2025, raising discounting and order volatility.

| Metric | Value |

|---|---|

| Govt tender share (FY2024) | ~45% |

| Bid discounts (2023) | 12–18% |

| Rebar price dispersion (2024) | 12% |

| Furnace buyer technical influence (2024) | >60% |

| Foundry-equipment imports (2024) | 18% |

| Auto capex change (H1 2025) | -12% YoY |

Preview Before You Purchase

Electrotherm Porter's Five Forces Analysis

This preview shows the exact Electrotherm Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

No mockups or samples: this is the final, ready-to-use deliverable covering competitive rivalry, supplier power, buyer power, threats of entry and substitutes.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Electrotherm faces moderate supplier and buyer power, with capital-intensive barriers limiting new entrants but rising substitute and competitive pressures from global OEMs; growth hinges on technology upgrades and downstream integration. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Electrotherm’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility of raw material inputs

Electrotherm depends on iron ore, coal and scrap for steel and pipes; by late 2025 iron ore spot rose ~18% year-on-year and thermal coal prices were ~25% higher, keeping pricing power with large miners and exporters like Vale and Glencore.

Mining-related environmental curbs and shipping bottlenecks tightened supply, forcing Electrotherm to absorb input cost swings and operate with thin EBITDA margins (steel sector median ~6% in 2024–25), limiting its leverage over base commodity prices.

Specialized electronic components for furnaces

Manufacturing induction melting furnaces depends on high-end power electronics and specialized copper parts from a small set of global vendors, giving suppliers strong leverage; industry surveys show >60% of critical components are single- or dual-sourced as of 2024. These proprietary technologies directly affect Electrotherm’s product performance and margins, with supplier-driven price moves potentially raising component costs by 8–15% per year. Any supply disruption can halt lines—Electrotherm’s engineering division could face weeks-long delays and cost overruns that eat into FY2025 EBITDA, where components represent ~12% of COGS.

Energy costs and utility dependency

Electrotherm’s steel and heavy-machinery plants are energy-heavy, so they rely on state utilities and large private suppliers; in India industrial power rates rose ~7% in 2024 and average industrial tariffs hit ~INR 9–11/kWh in 2025, reducing pricing flexibility.

Accelerating energy-transition rules through 2025 raised carbon costs; India’s traded carbon-equivalent compliance estimates add ~INR 0.5–1.0/kg CO2e, making electricity and credits mandatory, externally set inputs.

Because suppliers set tariffs and credit prices, Electrotherm has weak supplier bargaining power, which increases its integrated-solution cost base and compresses margins unless it secures captive renewables or long-term power purchase agreements.

Supplier concentration in the DI pipe segment

Supplier concentration in the DI pipe segment raises bargaining power: high‑purity magnesium and alloy additives are essential to meet ISO 2531 and EN 545 standards, and only a handful of global producers supply >70% of specialty magnesium refined for foundry use as of 2025, letting suppliers set prices and tight delivery windows during infrastructure booms.

That scarcity pushed premium for specialty alloys up ~18% in 2024 vs 2023, increasing Electrotherm’s input cost volatility and forcing longer contractual lead times.

- Few suppliers: >70% supply from top producers (2025)

- Price pressure: specialty alloy premiums +18% in 2024

- Standards impact: ISO 2531 / EN 545 require high purity

- Risk: delivery schedule leverage during infrastructure demand spikes

Logistics and transportation providers

Supply-side consolidation in freight cut global heavy-lift carriers to a handful by 2025, boosting transporters’ pricing power for heavy engineering and bulk steel moves needed by Electrotherm.

International routes saw average heavy-cargo freight rates rise ~22% YoY in 2024–25 on reduced capacity and higher fuel/insurance costs, letting carriers push through surcharges that pressure Electrotherm’s margins.

Long-term contracts and multimodal routing lower exposure, but single-vendor ports or specialist lift providers still create choke points for exports to Europe and Africa.

- Carrier consolidation: few specialist heavy-lift firms by 2025

- Freight rate change: ~+22% YoY (2024–25)

- Key risk: port/lift provider choke points on export lanes

- Mitigation: long-term contracts, multimodal routing

Supplier squeeze: concentrated inputs, surging commodities and energy dent Electrotherm margins

Suppliers hold strong power: key commodities (iron ore, coal, specialty alloys) and critical electronics are concentrated—top producers supply >70% (2025), alloy premiums rose ~18% in 2024, iron ore +18% YoY (late 2025) and coal ~+25% (2025), freight +22% YoY (2024–25); energy tariffs ~INR 9–11/kWh (2025) and components ≈12% of COGS shrink Electrotherm’s margin unless long-term contracts or captive power are secured.

| Item | 2024–25 change | 2025 level |

|---|---|---|

| Alloy premium | +18% YoY | - |

| Iron ore | +18% YoY | - |

| Thermal coal | +25% YoY | - |

| Freight (heavy) | +22% YoY | - |

| Industrial power tariff | +7% (2024) | INR 9–11/kWh |

| Supplier concentration | - | Top suppliers >70% |

What is included in the product

Tailored exclusively for Electrotherm, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats impacting its pricing, profitability, and strategic positioning.

Compact Porter's Five Forces snapshot for Electrotherm—instantly highlights competitive pressures and strategic levers for rapid decision-making.

Customers Bargaining Power

Concentration of large scale infrastructure buyers

A significant share of Electrotherm's ductile iron pipe and EPC revenues—estimated at ~45% in FY2024—comes from state governments and large municipal corporations, which use tender-based procurement that drives prices down; for example, average bid discounts vs. list prices reached 12–18% in 2023 municipal tenders. These buyers can pick among multiple certified suppliers, giving them strong leverage to demand lower prices and tougher payment terms, pressuring margins.

Low switching costs in the steel segment

In TMT bars and basic steel, products are commoditized so buyers switch brands easily; switching costs are near zero for construction and automotive firms. Large buyers compare prices and often choose the lowest bidder—India’s rebar spot market saw a 12% price dispersion in 2024, boosting price sensitivity. This limits Electrotherm’s pricing power and makes sustained price hikes unrealistic without volume loss.

Technical expertise of furnace clients

Electrotherm’s furnace buyers—mainly steelmakers and foundries—have deep process expertise and in 2024 drove >60% of procurement decisions by technical spec and life-cycle cost; they run strict cost-benefit models and push for custom designs and multi-year service contracts, forcing Electrotherm to offer tailored engineering, extended warranties, and performance SLAs, which compresses margins and raises negotiation leverage.

Availability of global alternatives

Industrial buyers for metal-melting solutions can choose domestic firms and global suppliers from Europe and China; global imports accounted for roughly 18% of India’s foundry-equipment market in 2024, widening choice and lowering reliance on any single local maker.

That forces Electrotherm to keep prices tight and invest in tech—R&D spend of 2.1% of revenue would be a benchmark to defend share.

- Global alternatives up — 18% import share (2024)

- Pressure on pricing

- Need for >2% R&D spend

Impact of economic cycles on buyer demand

Buyers in automotive and infrastructure are very rate-sensitive; by Q4 2025 rising borrowing costs cut fixed-asset investment—Indian auto capex fell 12% YoY in H1 2025—so customers defer furnaces and construction, forcing Electrotherm to offer price concessions.

This cyclicality gives buyers timing power: they wait for lower rates or fiscal stimulus before large orders, increasing order volatility and squeezing margins for Electrotherm.

- Auto capex down 12% YoY H1 2025

- Infrastructure project delays up 18% in 2025

- Electrotherm faces higher discounting during slow cycles

Buyers’ leverage squeezes margins—tenders, imports, and auto capex cut drive deep discounts

Buyers wield strong leverage: government tenders (~45% FY2024 revenue) force 12–18% bid discounts; commoditized TMT/rebar showed 12% price dispersion in 2024; furnace customers drove >60% technical procurement in 2024; imports were 18% of foundry-equipment market (2024); auto capex fell 12% YoY H1 2025, raising discounting and order volatility.

| Metric | Value |

|---|---|

| Govt tender share (FY2024) | ~45% |

| Bid discounts (2023) | 12–18% |

| Rebar price dispersion (2024) | 12% |

| Furnace buyer technical influence (2024) | >60% |

| Foundry-equipment imports (2024) | 18% |

| Auto capex change (H1 2025) | -12% YoY |

Preview Before You Purchase

Electrotherm Porter's Five Forces Analysis

This preview shows the exact Electrotherm Porter’s Five Forces analysis you’ll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

No mockups or samples: this is the final, ready-to-use deliverable covering competitive rivalry, supplier power, buyer power, threats of entry and substitutes.