Electrotherm PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

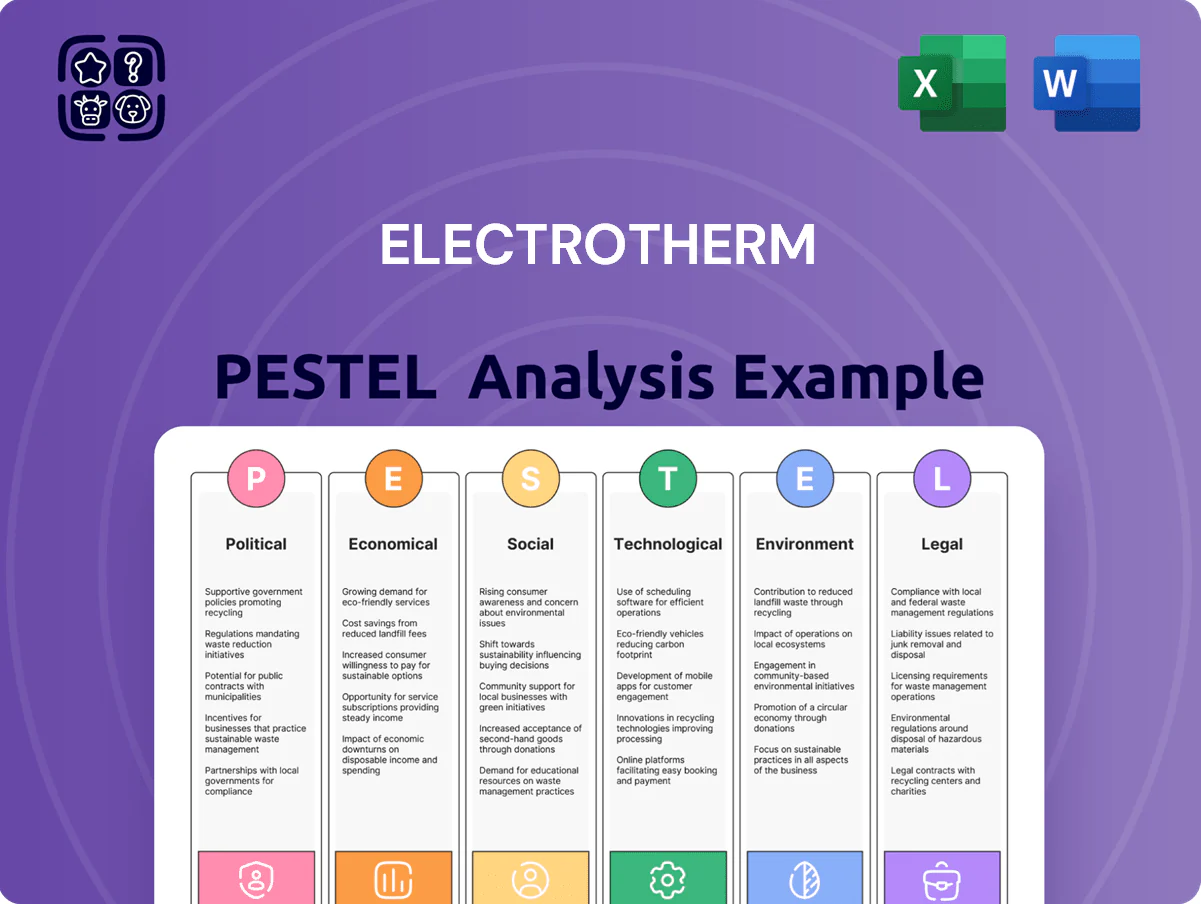

Unlock strategic clarity with our concise PESTLE Analysis of Electrotherm—spot regulatory risks, technological shifts, and market forces shaping its future; perfect for investors and strategists. Buy the full report to access the complete, editable analysis and actionable insights you can use in forecasts, pitches, or boardroom decisions.

Political factors

Infrastructure Development Initiatives

Gati Shakti National Master Plan's Rs 100 lakh crore infrastructure push through 2025 boosts demand for Electrotherm's steel and ductile iron pipes, as multimodal connectivity and logistics upgrades expand public procurement; India budgeted ~Rs 10 lakh crore for capital expenditure in 2024–25, lifting water and urban projects that purchase high-quality industrial components, ensuring a steadier domestic order pipeline for Electrotherm's manufacturing divisions.

Trade Policies and Import Duties

Imposition of anti-dumping duties on cheaper steel imports—India levied duties up to 20–25% on certain steel products in 2024—shields Electrotherm’s heavy-engineering margins by reducing unfair price competition.

Make in India incentives, linked to capital subsidies and preferential procurement, bolster Electrotherm’s domestic order book, which rose 8% YoY in FY2024 for engineered products.

Reduction in export incentives or new trade barriers in target markets could dent furnace exports; Electrotherm exported ~35% of its furnaces to Middle East & Africa in 2023–24.

Shifts in global trade agreements—e.g., regional tariff negotiations or Gulf import policy changes—require active monitoring to protect market share and pricing strategies.

Atmanirbhar Bharat Mission

The Atmanirbhar Bharat push boosts demand for indigenous heavy machinery and specialty steel, aiding Electrotherm which reported FY2024 domestic furnace orders up 28% year-on-year; government incentives and preferential procurement for local manufacturers underpin this growth.

Geopolitical Stability and Export Markets

Political stability in Southeast Asia and parts of Africa is critical for Electrotherm’s execution of export projects; ASEAN trade grew 4.6% in 2024, underpinning demand for metallurgical equipment.

Geopolitical tensions risk supply-chain delays and payment disruptions—global shipping delays increased 12% in 2024—affecting timelines for induction-furnace deliveries.

Maintaining diplomatic relationships preserves Electrotherm’s reputation as a reliable supplier; India’s bilateral trade with Africa rose 18% in FY2023–24, supporting long-term growth.

- Export-region stability: ASEAN 4.6% trade growth (2024)

- Supply-chain risk: shipping delays +12% (2024)

- Bilateral trade tailwind: India–Africa +18% (FY2023–24)

Regulatory Framework for Steel Production

- National Steel Policy: 300 MT by 2030

- Mining allocation impacts raw-material cost/margins

- Regulatory shifts affect compliance costs and operations

- Industry engagement enables policy influence

Infrastructure capex and duties fuel Electrotherm growth; exports & shipping add risk

Political support for infrastructure (Gati Shakti Rs 100 lakh crore to 2025) and India’s Rs 10 lakh crore capex (2024–25) boosts Electrotherm’s domestic orders; anti-dumping duties (up to 20–25% in 2024) protect margins, while Make in India and Atmanirbhar Bharat lifted domestic furnace orders +28% YoY in FY2024; export exposure (~35% furnaces to MEA 2023–24) and shipping delays (+12% 2024) pose geopolitical risks.

| Factor | Metric | Value |

|---|---|---|

| Infrastructure capex | Gati Shakti | Rs 100 lakh crore |

| FY24 capex | India 2024–25 | Rs 10 lakh crore |

| Domestic furnace orders | FY2024 YoY | +28% |

| Export share | Furnaces 2023–24 | ~35% |

| Anti-dumping | Steel duties 2024 | 20–25% |

| Shipping delays | Global 2024 | +12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Electrotherm across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise PESTLE summary of Electrotherm that’s visually segmented for quick interpretation, ideal for slides or meetings and easily editable to add region- or business-specific notes.

Economic factors

Raw Material Price Volatility

Volatility in iron ore, scrap and thermal coal prices—iron ore up ~35% in 2024 vs 2023 and metallurgical coal swinging 20–40% in 2024–2025—directly compresses Electrotherm’s steel and pipe margins, given their input intensity.

By late 2025, global commodity shifts require active hedging; firms reducing input-cost VaR by 15–25% on average illustrate the need for derivatives and long-term offtakes.

Energy price fluctuations, with industrial electricity up ~10% YoY in 2024 in key markets, increase running costs for induction furnaces and lower operational efficiency.

Robust supplier diversification, inventory buffers and logistics contracts are essential to limit earnings volatility and protect cash flow against sudden commodity swings.

Interest Rate Environment

As a capital-intensive manufacturer, Electrotherm’s financing costs rise with interest rates; India’s repo rate at 6.5% (RBI Aug 2024) raises borrowing costs for new plants and R&D, increasing annual interest expense and debt-servicing strain. Higher rates can delay planned capex—Electrotherm’s FY2024 capex plans of ~INR 500–700 crore face pressure—while stable or falling rates spur infrastructure and automotive demand, lifting order visibility. Financial professionals track RBI and global central bank moves to model the company’s future borrowing costs and investment capacity.

Global Economic Growth Trends

The demand for Electrotherm's engineering services and induction furnaces tracks global manufacturing; IMF projects global growth of 3.0% in 2025 after 3.1% in 2024, so slowdowns in major markets can cut industrial expansion and equipment orders.

Economic contractions in key regions reduced capital expenditure in 2024—global steel output fell 1.2% in 2024—pressuring furnace demand and project bookings.

Emerging markets (Africa, Southeast Asia) saw steel capacity additions rising ~4–6% annually, offering growth as they industrialize and modernize production.

Electrotherm must balance domestic revenues (stable service aftermarket) with targeted international expansion to mitigate cyclical volatility and protect margins.

Currency Exchange Rate Fluctuations

Electrotherm's large export share makes revenue sensitive to INR/USD and INR/EUR moves; the Rupee fell ~3.5% vs USD in 2024, which likely improved export competitiveness but raised costs for imported capital goods that comprise ~28% of production inputs (FY2024 capex/import data).

Effective FX hedging and receivables management are required to shield margins from abrupt devaluations; analysts model currency scenarios to estimate impacts on EBITDA and net margins and on global pricing power.

- Export exposure high; Rupee volatility (≈3–4% yearly swings recently) affects pricing.

- Weaker INR boosts exports but raises imported component costs (~28% of inputs).

- FX hedging and cash-management reduce margin risk.

Industrial Credit Availability

Access to working capital and long-term bank loans is vital for Electrotherm’s large-scale EPC projects; in FY2024 the company reported net debt of about INR 1,120 crore, making bank funding pivotal for tender participation.

Tightened credit since 2023 has raised borrowing costs—India’s corporate lending spread widened ~40–60 bps—limiting capacity to bid on massive infrastructure tenders and manage cash flow.

Electrotherm’s credit profile and FY2023–24 revenue volatility directly affect loan pricing; management prioritizes a healthy balance sheet to preserve investor confidence and operational liquidity.

- Net debt ~INR 1,120 crore (FY2024)

- Corporate lending spreads up ~40–60 bps since 2023

- Balance-sheet strength critical for favorable loan terms

Rising commodity, power and FX pressures squeeze margins—focus on hedging, WC and disciplined capex

Commodity-driven input cost volatility (iron ore +35% in 2024; metallurgical coal swings 20–40% in 2024–25) and ~10% industrial power inflation in 2024 compress margins; net debt ~INR 1,120 crore (FY2024) and RBI repo 6.5% (Aug 2024) raise financing costs; Rupee -3.5% vs USD (2024) aids exports but ups imported-capex costs (~28% inputs); FX hedging, working-capital access and capex discipline are critical.

| Metric | Value |

|---|---|

| Iron ore 2024 | +35% |

| Met coal 2024–25 | ±20–40% |

| Industrial electricity 2024 | +10% YoY |

| Net debt (FY2024) | ≈INR 1,120 cr |

| Repo rate (Aug 2024) | 6.5% |

| INR vs USD 2024 | -3.5% |

| Imported inputs | ~28% |

Full Version Awaits

Electrotherm PESTLE Analysis

The preview shown here is the exact Electrotherm PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without edits.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our concise PESTLE Analysis of Electrotherm—spot regulatory risks, technological shifts, and market forces shaping its future; perfect for investors and strategists. Buy the full report to access the complete, editable analysis and actionable insights you can use in forecasts, pitches, or boardroom decisions.

Political factors

Infrastructure Development Initiatives

Gati Shakti National Master Plan's Rs 100 lakh crore infrastructure push through 2025 boosts demand for Electrotherm's steel and ductile iron pipes, as multimodal connectivity and logistics upgrades expand public procurement; India budgeted ~Rs 10 lakh crore for capital expenditure in 2024–25, lifting water and urban projects that purchase high-quality industrial components, ensuring a steadier domestic order pipeline for Electrotherm's manufacturing divisions.

Trade Policies and Import Duties

Imposition of anti-dumping duties on cheaper steel imports—India levied duties up to 20–25% on certain steel products in 2024—shields Electrotherm’s heavy-engineering margins by reducing unfair price competition.

Make in India incentives, linked to capital subsidies and preferential procurement, bolster Electrotherm’s domestic order book, which rose 8% YoY in FY2024 for engineered products.

Reduction in export incentives or new trade barriers in target markets could dent furnace exports; Electrotherm exported ~35% of its furnaces to Middle East & Africa in 2023–24.

Shifts in global trade agreements—e.g., regional tariff negotiations or Gulf import policy changes—require active monitoring to protect market share and pricing strategies.

Atmanirbhar Bharat Mission

The Atmanirbhar Bharat push boosts demand for indigenous heavy machinery and specialty steel, aiding Electrotherm which reported FY2024 domestic furnace orders up 28% year-on-year; government incentives and preferential procurement for local manufacturers underpin this growth.

Geopolitical Stability and Export Markets

Political stability in Southeast Asia and parts of Africa is critical for Electrotherm’s execution of export projects; ASEAN trade grew 4.6% in 2024, underpinning demand for metallurgical equipment.

Geopolitical tensions risk supply-chain delays and payment disruptions—global shipping delays increased 12% in 2024—affecting timelines for induction-furnace deliveries.

Maintaining diplomatic relationships preserves Electrotherm’s reputation as a reliable supplier; India’s bilateral trade with Africa rose 18% in FY2023–24, supporting long-term growth.

- Export-region stability: ASEAN 4.6% trade growth (2024)

- Supply-chain risk: shipping delays +12% (2024)

- Bilateral trade tailwind: India–Africa +18% (FY2023–24)

Regulatory Framework for Steel Production

- National Steel Policy: 300 MT by 2030

- Mining allocation impacts raw-material cost/margins

- Regulatory shifts affect compliance costs and operations

- Industry engagement enables policy influence

Infrastructure capex and duties fuel Electrotherm growth; exports & shipping add risk

Political support for infrastructure (Gati Shakti Rs 100 lakh crore to 2025) and India’s Rs 10 lakh crore capex (2024–25) boosts Electrotherm’s domestic orders; anti-dumping duties (up to 20–25% in 2024) protect margins, while Make in India and Atmanirbhar Bharat lifted domestic furnace orders +28% YoY in FY2024; export exposure (~35% furnaces to MEA 2023–24) and shipping delays (+12% 2024) pose geopolitical risks.

| Factor | Metric | Value |

|---|---|---|

| Infrastructure capex | Gati Shakti | Rs 100 lakh crore |

| FY24 capex | India 2024–25 | Rs 10 lakh crore |

| Domestic furnace orders | FY2024 YoY | +28% |

| Export share | Furnaces 2023–24 | ~35% |

| Anti-dumping | Steel duties 2024 | 20–25% |

| Shipping delays | Global 2024 | +12% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Electrotherm across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise PESTLE summary of Electrotherm that’s visually segmented for quick interpretation, ideal for slides or meetings and easily editable to add region- or business-specific notes.

Economic factors

Raw Material Price Volatility

Volatility in iron ore, scrap and thermal coal prices—iron ore up ~35% in 2024 vs 2023 and metallurgical coal swinging 20–40% in 2024–2025—directly compresses Electrotherm’s steel and pipe margins, given their input intensity.

By late 2025, global commodity shifts require active hedging; firms reducing input-cost VaR by 15–25% on average illustrate the need for derivatives and long-term offtakes.

Energy price fluctuations, with industrial electricity up ~10% YoY in 2024 in key markets, increase running costs for induction furnaces and lower operational efficiency.

Robust supplier diversification, inventory buffers and logistics contracts are essential to limit earnings volatility and protect cash flow against sudden commodity swings.

Interest Rate Environment

As a capital-intensive manufacturer, Electrotherm’s financing costs rise with interest rates; India’s repo rate at 6.5% (RBI Aug 2024) raises borrowing costs for new plants and R&D, increasing annual interest expense and debt-servicing strain. Higher rates can delay planned capex—Electrotherm’s FY2024 capex plans of ~INR 500–700 crore face pressure—while stable or falling rates spur infrastructure and automotive demand, lifting order visibility. Financial professionals track RBI and global central bank moves to model the company’s future borrowing costs and investment capacity.

Global Economic Growth Trends

The demand for Electrotherm's engineering services and induction furnaces tracks global manufacturing; IMF projects global growth of 3.0% in 2025 after 3.1% in 2024, so slowdowns in major markets can cut industrial expansion and equipment orders.

Economic contractions in key regions reduced capital expenditure in 2024—global steel output fell 1.2% in 2024—pressuring furnace demand and project bookings.

Emerging markets (Africa, Southeast Asia) saw steel capacity additions rising ~4–6% annually, offering growth as they industrialize and modernize production.

Electrotherm must balance domestic revenues (stable service aftermarket) with targeted international expansion to mitigate cyclical volatility and protect margins.

Currency Exchange Rate Fluctuations

Electrotherm's large export share makes revenue sensitive to INR/USD and INR/EUR moves; the Rupee fell ~3.5% vs USD in 2024, which likely improved export competitiveness but raised costs for imported capital goods that comprise ~28% of production inputs (FY2024 capex/import data).

Effective FX hedging and receivables management are required to shield margins from abrupt devaluations; analysts model currency scenarios to estimate impacts on EBITDA and net margins and on global pricing power.

- Export exposure high; Rupee volatility (≈3–4% yearly swings recently) affects pricing.

- Weaker INR boosts exports but raises imported component costs (~28% of inputs).

- FX hedging and cash-management reduce margin risk.

Industrial Credit Availability

Access to working capital and long-term bank loans is vital for Electrotherm’s large-scale EPC projects; in FY2024 the company reported net debt of about INR 1,120 crore, making bank funding pivotal for tender participation.

Tightened credit since 2023 has raised borrowing costs—India’s corporate lending spread widened ~40–60 bps—limiting capacity to bid on massive infrastructure tenders and manage cash flow.

Electrotherm’s credit profile and FY2023–24 revenue volatility directly affect loan pricing; management prioritizes a healthy balance sheet to preserve investor confidence and operational liquidity.

- Net debt ~INR 1,120 crore (FY2024)

- Corporate lending spreads up ~40–60 bps since 2023

- Balance-sheet strength critical for favorable loan terms

Rising commodity, power and FX pressures squeeze margins—focus on hedging, WC and disciplined capex

Commodity-driven input cost volatility (iron ore +35% in 2024; metallurgical coal swings 20–40% in 2024–25) and ~10% industrial power inflation in 2024 compress margins; net debt ~INR 1,120 crore (FY2024) and RBI repo 6.5% (Aug 2024) raise financing costs; Rupee -3.5% vs USD (2024) aids exports but ups imported-capex costs (~28% inputs); FX hedging, working-capital access and capex discipline are critical.

| Metric | Value |

|---|---|

| Iron ore 2024 | +35% |

| Met coal 2024–25 | ±20–40% |

| Industrial electricity 2024 | +10% YoY |

| Net debt (FY2024) | ≈INR 1,120 cr |

| Repo rate (Aug 2024) | 6.5% |

| INR vs USD 2024 | -3.5% |

| Imported inputs | ~28% |

Full Version Awaits

Electrotherm PESTLE Analysis

The preview shown here is the exact Electrotherm PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use without edits.