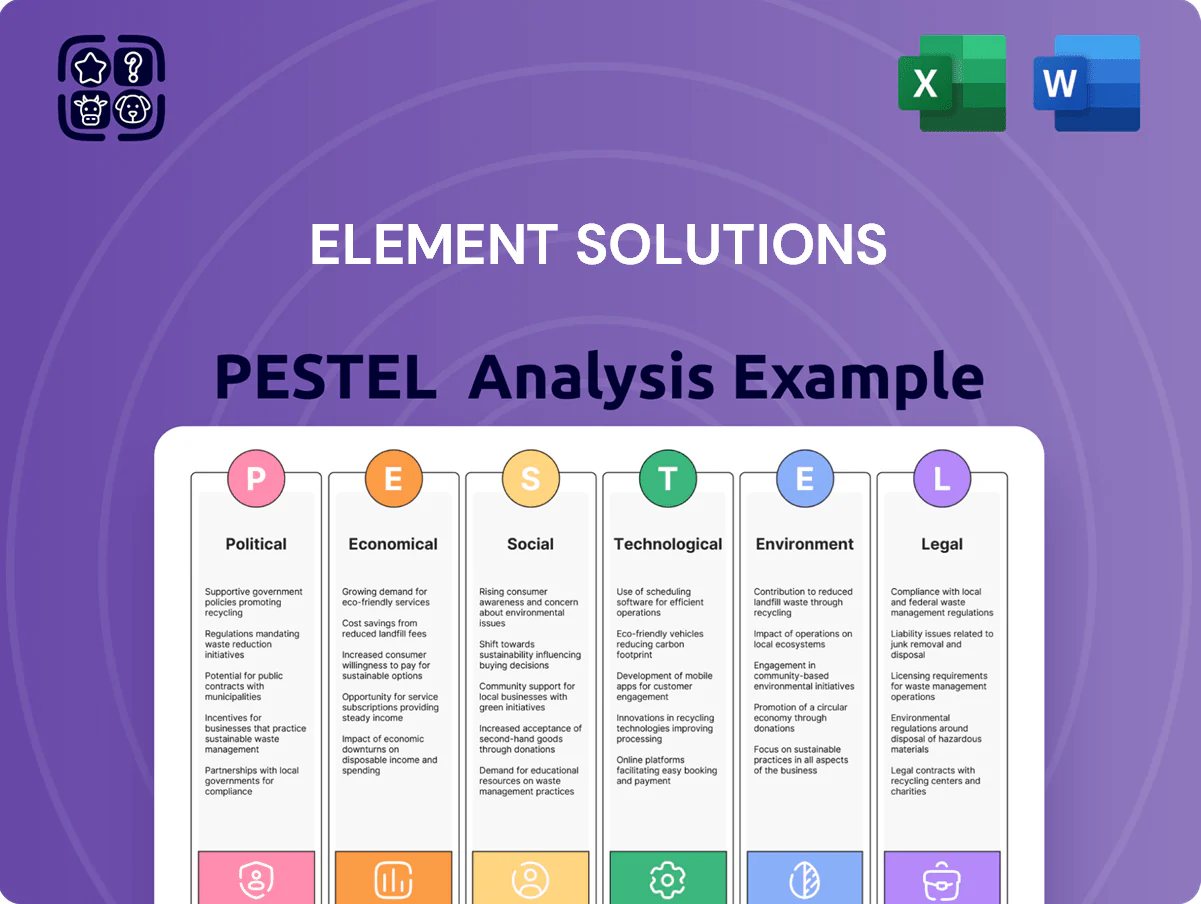

Element Solutions PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological innovation are shaping Element Solutions’ strategic outlook with our concise PESTLE Analysis—designed for investors and strategists who need ready-to-use external intelligence. Buy the full version for a detailed breakdown, editable charts, and actionable recommendations to inform investments, risk mitigation, and growth planning.

Political factors

Geopolitical trade tensions and export controls

Ongoing US-China trade friction reshapes supply chains for specialty chemicals and semiconductor materials, with 2025 bilateral tariffs and tariffs on 18% of targeted tech components increasing logistics costs by an estimated 6-9% for suppliers in the sector.

By late 2025, tighter US export controls on advanced semiconductor inputs expanded to over 120 controlled items, forcing Element Solutions to comply with complex licensing regimes across 30+ jurisdictions.

Element Solutions must strategically manage a global manufacturing footprint—including shifts toward Southeast Asia where 42% of regional capacity growth occurred in 2024—to mitigate sudden tariff hikes and trade barriers in key Asian markets.

Government incentives for domestic semiconductor production

The CHIPS Act (US) and EU's IPCEI programs have mobilized over $200 billion in public and private investment globally through 2025, creating a multiyear build-out of fabs that boosts demand for specialty chemistries.

Political subsidies and tax credits favor regionalized semiconductor manufacturing, increasing near-term procurement of high-performance materials that Element Solutions supplies.

By co-locating capacity near U.S. and European subsidized hubs, Element Solutions can pursue multi-year supply contracts with leading fabs, supporting revenue visibility and margin expansion.

Regional stability in Southeast Asian manufacturing hubs

Political stability in Taiwan, Vietnam and Malaysia underpins PCB and electronic assembly flows; Taiwan accounted for about 63% of global semiconductor packaging and testing capacity in 2023, while Vietnam’s electronics exports rose 18.4% to $110.4B in 2024, highlighting concentration risks.

Localized unrest or South China Sea tensions could halt logistics, with container delays already adding ~7–12% to lead times in 2024 for ASEAN routes.

Element Solutions tracks these geopolitical risks, maintaining supplier diversification and contingency plans to limit regional exposure and protect revenue streams tied to major customers.

Corporate tax policy shifts

Changes in corporate tax rates and updates to international tax treaties at end-2025 could raise Element Solutions effective tax rate from recent ~15% GAAP rates toward global averages near 21%, pressuring net profitability for its multinational operations.

Governments funding infrastructure/social programs may increase jurisdictional tax burdens, making strategic tax planning and cross-border transaction optimization critical to preserve shareholder value amid political flux.

- End-2025 tax shifts may push ESI effective tax toward ~20–22%

National security reviews of chemical manufacturing

National security reviews now target specialty chemicals used in defense and aerospace, affecting Element Solutions which supplies such compounds to customers including defense primes; US CFIUS and export controls have increased vetting since 2020 with a 35% rise in reviewed transactions in 2023.

To retain trusted-supplier status, Element Solutions must pass rigorous security protocols and compliance audits, with potential contract impact on >$100m in defense-related revenue streams.

Political scrutiny forces greater transparency and investment in cybersecurity—industry reports show chemical firms increased cyber budgets by ~18% in 2024—to protect proprietary formulations and client data.

- 35% rise in national-security reviews (2023)

- >$100m exposure in defense-related contracts

- ~18% increase in cyber spending (2024)

Geopolitics Force Element Solutions to Nearshore, Diversify Supply Chains, Boost Security

Political risks—US-China trade frictions, tightened export controls (120+ items by 2025), and regional subsidies (CHIPS/IPCEI ~$200B through 2025)—reshape Element Solutions’ supply chain, tax exposure (effective rate risk rising toward ~20–22%), and defense contract scrutiny (>35% rise in reviews; >$100m exposure), prompting diversification, nearshoring, and increased cybersecurity spend (~18% in 2024).

| Metric | Value |

|---|---|

| Export-controlled items (2025) | 120+ |

| Public/private chips investment | $200B+ |

| Tax rate risk | ~20–22% |

| Security review increase (2023) | 35% |

| Cyber spend increase (2024) | ~18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Element Solutions across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

Condenses Element Solutions' PESTLE into a concise, meeting-ready summary that highlights external risks and opportunities for quick strategic decision-making.

Economic factors

Cyclical nature of the global electronics market

Demand for Element Solutions products closely follows cyclical consumer electronics and automotive markets; electronics assembly sales benefited from smartphone and PC stabilization in 2025, with global smartphone shipments roughly flat YoY at ~1.2 billion units and PC shipments down only 1–2% after prior declines, supporting steady revenue streams estimated to lift segment growth toward low single digits in 2025.

Volatility in raw material and energy costs

The specialty chemicals sector is highly sensitive to raw material prices—precious metals and petroleum feedstock swings drove Element Solutions' cost of goods volatility, with oil prices rising ~28% in 2024 and silver up ~15% year-on-year, pressuring margins.

Global energy cost increases raised manufacturing and logistics expenses; Element reported a 2024 freight and energy-related cost increase of roughly 4–6% impacting SG&A.

Element offsets exposure via pricing surcharges and strategic sourcing: in 2024 the company implemented pass-through surcharges and long-term supply contracts that helped sustain adjusted gross margin near 34%.

Interest rate environment and capital allocation

As interest rates stabilize in late 2025—U.S. benchmark rates projected near 5.25%—costs for financing large capital projects and acquisitions become more predictable for Element Solutions, whose net debt was about $1.1 billion at FY2024 year-end. The company must balance debt management with maintaining R&D spend (FY2024 R&D ~2.8% of revenue) to defend technological edge. A favorable rate backdrop improves capacity for inorganic growth, easing funding for strategic M&A.

Currency exchange rate fluctuations

With roughly 60% of Element Solutions revenue earned outside the US, foreign currency translation poses material risk to reported results; a 5% appreciation of the US dollar vs. the euro, yen or renminbi could swing reported EPS by several cents based on 2024 geographic sales mix.

The company reported using forward contracts and option overlays covering a large portion of forecasted cash flows in FY2024 to hedge transaction and translation exposure.

Hedging reduced reported FX volatility in 2024, with net currency translation losses narrowing to under 1% of revenue versus prior-year swings of ~2%.

- ~60% revenue ex-US

- 5% USD move materially impacts EPS

- FY2024 forward/option hedges in place

- FX losses <1% of revenue in 2024

Emerging market industrialization

Continued industrial growth in emerging economies—notably India (GDP 6.3% in 2024) and Southeast Asia (regional manufacturing output +4.5% YoY in 2024)—boosts demand for Element Solutions’ industrial finishes and surface treatments, especially in automotive and infrastructure projects.

Expansion into these markets offers volume growth beyond Western markets but requires localized sales teams and distribution networks; Element Solutions’ 2024 international revenue mix showed ~28% from APAC/EMEA combined, highlighting opportunity.

- EM industrial output +4–6% (2024)

- India automotive production ~5.2M units (2024)

- 2024 INT revenue ~28% of total

Element Solutions: Stabilizing electronics demand offsets cost, FX and debt remain key risks

Element Solutions faces mixed economic drivers: end-market stabilization lifted electronics demand (global smartphone ~1.2B units in 2025), raw material/energy cost inflation (oil +28% in 2024; silver +15%) pressured margins, net debt ~$1.1B (FY2024) with interest rates ~5.25% impacting financing, and ~60% revenue ex‑US creating material FX sensitivity (5% USD move affects EPS); hedges kept FX losses <1% of revenue in 2024.

| Metric | Value |

|---|---|

| Smartphone shipments (2025) | ~1.2B |

| Oil price change (2024) | +28% |

| Silver change (2024) | +15% |

| Net debt (FY2024) | $1.1B |

| Revenue ex‑US | ~60% |

| FX losses (2024) | <1% rev |

Preview Before You Purchase

Element Solutions PESTLE Analysis

The preview shown here is the exact Element Solutions PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and technological innovation are shaping Element Solutions’ strategic outlook with our concise PESTLE Analysis—designed for investors and strategists who need ready-to-use external intelligence. Buy the full version for a detailed breakdown, editable charts, and actionable recommendations to inform investments, risk mitigation, and growth planning.

Political factors

Geopolitical trade tensions and export controls

Ongoing US-China trade friction reshapes supply chains for specialty chemicals and semiconductor materials, with 2025 bilateral tariffs and tariffs on 18% of targeted tech components increasing logistics costs by an estimated 6-9% for suppliers in the sector.

By late 2025, tighter US export controls on advanced semiconductor inputs expanded to over 120 controlled items, forcing Element Solutions to comply with complex licensing regimes across 30+ jurisdictions.

Element Solutions must strategically manage a global manufacturing footprint—including shifts toward Southeast Asia where 42% of regional capacity growth occurred in 2024—to mitigate sudden tariff hikes and trade barriers in key Asian markets.

Government incentives for domestic semiconductor production

The CHIPS Act (US) and EU's IPCEI programs have mobilized over $200 billion in public and private investment globally through 2025, creating a multiyear build-out of fabs that boosts demand for specialty chemistries.

Political subsidies and tax credits favor regionalized semiconductor manufacturing, increasing near-term procurement of high-performance materials that Element Solutions supplies.

By co-locating capacity near U.S. and European subsidized hubs, Element Solutions can pursue multi-year supply contracts with leading fabs, supporting revenue visibility and margin expansion.

Regional stability in Southeast Asian manufacturing hubs

Political stability in Taiwan, Vietnam and Malaysia underpins PCB and electronic assembly flows; Taiwan accounted for about 63% of global semiconductor packaging and testing capacity in 2023, while Vietnam’s electronics exports rose 18.4% to $110.4B in 2024, highlighting concentration risks.

Localized unrest or South China Sea tensions could halt logistics, with container delays already adding ~7–12% to lead times in 2024 for ASEAN routes.

Element Solutions tracks these geopolitical risks, maintaining supplier diversification and contingency plans to limit regional exposure and protect revenue streams tied to major customers.

Corporate tax policy shifts

Changes in corporate tax rates and updates to international tax treaties at end-2025 could raise Element Solutions effective tax rate from recent ~15% GAAP rates toward global averages near 21%, pressuring net profitability for its multinational operations.

Governments funding infrastructure/social programs may increase jurisdictional tax burdens, making strategic tax planning and cross-border transaction optimization critical to preserve shareholder value amid political flux.

- End-2025 tax shifts may push ESI effective tax toward ~20–22%

National security reviews of chemical manufacturing

National security reviews now target specialty chemicals used in defense and aerospace, affecting Element Solutions which supplies such compounds to customers including defense primes; US CFIUS and export controls have increased vetting since 2020 with a 35% rise in reviewed transactions in 2023.

To retain trusted-supplier status, Element Solutions must pass rigorous security protocols and compliance audits, with potential contract impact on >$100m in defense-related revenue streams.

Political scrutiny forces greater transparency and investment in cybersecurity—industry reports show chemical firms increased cyber budgets by ~18% in 2024—to protect proprietary formulations and client data.

- 35% rise in national-security reviews (2023)

- >$100m exposure in defense-related contracts

- ~18% increase in cyber spending (2024)

Geopolitics Force Element Solutions to Nearshore, Diversify Supply Chains, Boost Security

Political risks—US-China trade frictions, tightened export controls (120+ items by 2025), and regional subsidies (CHIPS/IPCEI ~$200B through 2025)—reshape Element Solutions’ supply chain, tax exposure (effective rate risk rising toward ~20–22%), and defense contract scrutiny (>35% rise in reviews; >$100m exposure), prompting diversification, nearshoring, and increased cybersecurity spend (~18% in 2024).

| Metric | Value |

|---|---|

| Export-controlled items (2025) | 120+ |

| Public/private chips investment | $200B+ |

| Tax rate risk | ~20–22% |

| Security review increase (2023) | 35% |

| Cyber spend increase (2024) | ~18% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Element Solutions across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities for executives, investors, and strategists.

Condenses Element Solutions' PESTLE into a concise, meeting-ready summary that highlights external risks and opportunities for quick strategic decision-making.

Economic factors

Cyclical nature of the global electronics market

Demand for Element Solutions products closely follows cyclical consumer electronics and automotive markets; electronics assembly sales benefited from smartphone and PC stabilization in 2025, with global smartphone shipments roughly flat YoY at ~1.2 billion units and PC shipments down only 1–2% after prior declines, supporting steady revenue streams estimated to lift segment growth toward low single digits in 2025.

Volatility in raw material and energy costs

The specialty chemicals sector is highly sensitive to raw material prices—precious metals and petroleum feedstock swings drove Element Solutions' cost of goods volatility, with oil prices rising ~28% in 2024 and silver up ~15% year-on-year, pressuring margins.

Global energy cost increases raised manufacturing and logistics expenses; Element reported a 2024 freight and energy-related cost increase of roughly 4–6% impacting SG&A.

Element offsets exposure via pricing surcharges and strategic sourcing: in 2024 the company implemented pass-through surcharges and long-term supply contracts that helped sustain adjusted gross margin near 34%.

Interest rate environment and capital allocation

As interest rates stabilize in late 2025—U.S. benchmark rates projected near 5.25%—costs for financing large capital projects and acquisitions become more predictable for Element Solutions, whose net debt was about $1.1 billion at FY2024 year-end. The company must balance debt management with maintaining R&D spend (FY2024 R&D ~2.8% of revenue) to defend technological edge. A favorable rate backdrop improves capacity for inorganic growth, easing funding for strategic M&A.

Currency exchange rate fluctuations

With roughly 60% of Element Solutions revenue earned outside the US, foreign currency translation poses material risk to reported results; a 5% appreciation of the US dollar vs. the euro, yen or renminbi could swing reported EPS by several cents based on 2024 geographic sales mix.

The company reported using forward contracts and option overlays covering a large portion of forecasted cash flows in FY2024 to hedge transaction and translation exposure.

Hedging reduced reported FX volatility in 2024, with net currency translation losses narrowing to under 1% of revenue versus prior-year swings of ~2%.

- ~60% revenue ex-US

- 5% USD move materially impacts EPS

- FY2024 forward/option hedges in place

- FX losses <1% of revenue in 2024

Emerging market industrialization

Continued industrial growth in emerging economies—notably India (GDP 6.3% in 2024) and Southeast Asia (regional manufacturing output +4.5% YoY in 2024)—boosts demand for Element Solutions’ industrial finishes and surface treatments, especially in automotive and infrastructure projects.

Expansion into these markets offers volume growth beyond Western markets but requires localized sales teams and distribution networks; Element Solutions’ 2024 international revenue mix showed ~28% from APAC/EMEA combined, highlighting opportunity.

- EM industrial output +4–6% (2024)

- India automotive production ~5.2M units (2024)

- 2024 INT revenue ~28% of total

Element Solutions: Stabilizing electronics demand offsets cost, FX and debt remain key risks

Element Solutions faces mixed economic drivers: end-market stabilization lifted electronics demand (global smartphone ~1.2B units in 2025), raw material/energy cost inflation (oil +28% in 2024; silver +15%) pressured margins, net debt ~$1.1B (FY2024) with interest rates ~5.25% impacting financing, and ~60% revenue ex‑US creating material FX sensitivity (5% USD move affects EPS); hedges kept FX losses <1% of revenue in 2024.

| Metric | Value |

|---|---|

| Smartphone shipments (2025) | ~1.2B |

| Oil price change (2024) | +28% |

| Silver change (2024) | +15% |

| Net debt (FY2024) | $1.1B |

| Revenue ex‑US | ~60% |

| FX losses (2024) | <1% rev |

Preview Before You Purchase

Element Solutions PESTLE Analysis

The preview shown here is the exact Element Solutions PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.