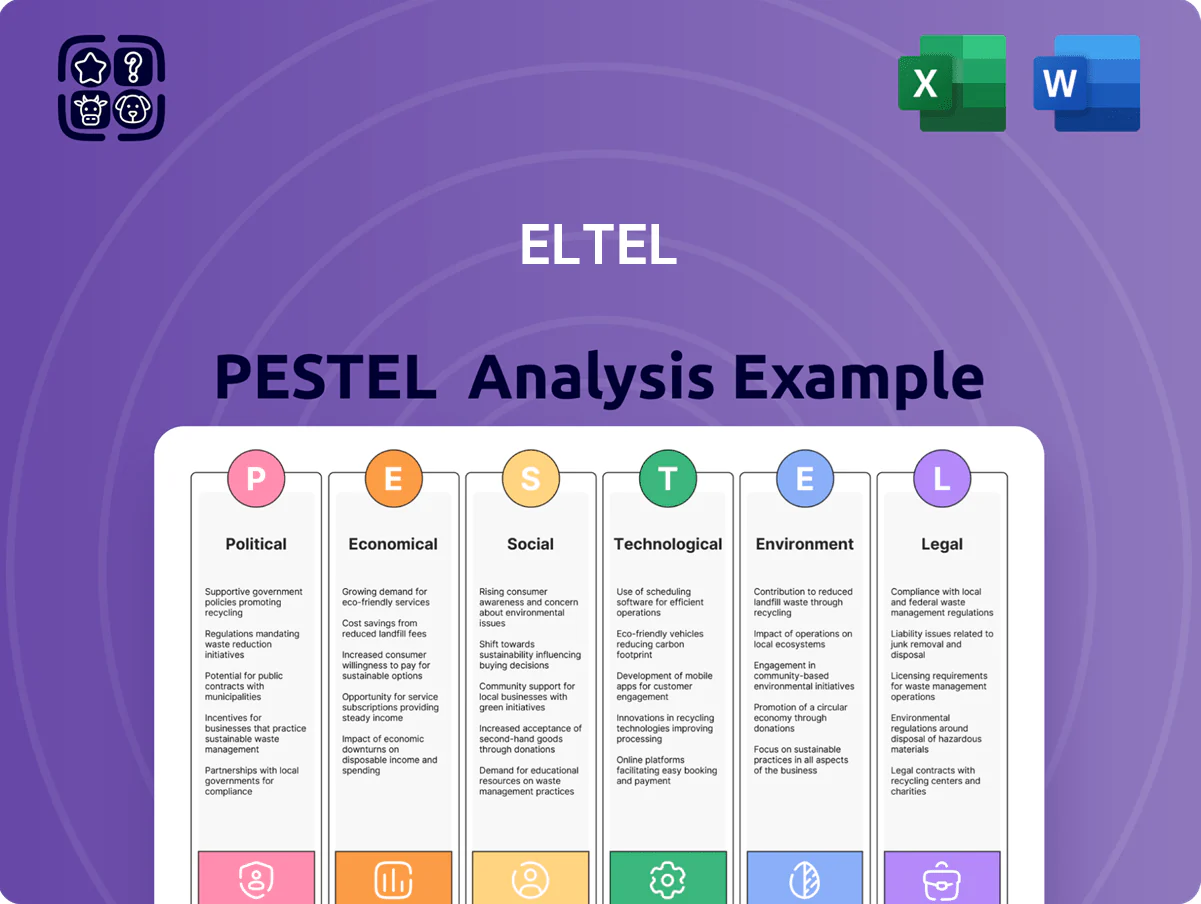

Eltel PESTLE Analysis

Your Competitive Advantage Starts with This Report

Get a clear view of how political shifts, regulatory pressures, economic cycles, and technological change are shaping Eltel’s prospects—our compact PESTLE highlights the most critical external risks and opportunities to inform your strategy. Ideal for investors and advisors, the full analysis delivers detailed, actionable insights and editable charts to accelerate decision-making. Purchase the complete PESTLE now for instant, board-ready intelligence.

Political factors

Nordic Energy Security and Sovereignty

Governments across Northern Europe are prioritizing energy independence, with EU and Nordic green recovery funds directing over €120bn to grid and resilience projects in 2024–25, reducing reliance on external suppliers amid geopolitical risks.

This shift drives massive investment into domestic power grids and decentralized renewables, creating demand for Eltel’s technical services—Nordic transmission & distribution capex rose ~18% y/y in 2024.

National security policies now classify energy and communications as critical infrastructure, unlocking multi-year, government-backed contracts and sustaining a steady pipeline of projects for Eltel.

EU Infrastructure Funding and Green Deal

EU allocates large funds—Connecting Europe Facility budget rose to 42.3 billion EUR for 2021–2027 and the EU Green Deal mobilises an estimated 1 trillion EUR of sustainable investment by 2030—targeting cross-border grids and broadband in underserved regions, directly increasing demand for grid upgrades and fibre rollout.

Geopolitical Resilience and Defense Strategy

Increased regional tensions have pushed Nordic and Baltic states to harden critical infrastructure; governments allocated about EUR 4.5bn in 2024–2025 for security upgrades and cyber resilience across energy and telecom sectors.

Political mandates now require utility and telecom providers to boost physical security and network redundancy, raising CAPEX and service contracts for integrators by an estimated 12–18% in 2025.

Eltel, with ~8,000 employees in the region and 2024 revenue near EUR 1.2bn, is positioned as a trusted local partner to implement high-security upgrades for state-owned and private operators.

National Decarbonization Mandates

National net-zero commitments (over 130 countries covering >80% of global emissions as of 2025) are driving laws for rapid electrification of heat and transport, raising EU and UK targets for EVs and heat pumps that could triple electricity demand by 2050, requiring significant network upgrades.

Aggressive fossil-fuel phase-out timelines (e.g., EU 2035 combustion-engine sales ban) force immediate reinforcement of distribution grids; Eltel’s grid-strengthening services are critical to deliver legally binding climate targets and capture portions of the ~€500bn European smart-grid investment pipeline to 2030.

- 130+ countries net-zero by mid-century

- Electricity demand could triple by 2050

- EU combustion-engine sales ban from 2035

- €500bn European smart-grid investment to 2030

Public Procurement and Tendering Policies

Nordic procurement increasingly favors suppliers with strong social responsibility and local economic impact; tenders now weight non-financial criteria up to 30% in some countries—Finland and Sweden introduced guidelines in 2023–24 emphasizing job creation and domestic supply chain resilience.

Eltel’s 40+ year Northern European presence and 2024 revenue of ~EUR 1.3bn and 9,000 employees position it to win tenders prioritizing local content and employment impact.

- Non-financial criteria weight up to 30% in recent Nordic tenders

- Eltel revenue ~EUR 1.3bn (2024), ~9,000 employees

- Strong local footprint boosts competitiveness in public contracts

Eltel poised to grab slice of €500bn smart‑grid boom as Europe pours €120–150bn into grids

Political support for energy independence and security is driving €120–€150bn in 2024–25 grid/ resilience spend across Northern Europe, plus ~€4.5bn for security upgrades; EU funds (Connecting Europe Facility €42.3bn) and net-zero rules boost demand for Eltel’s services—2024 revenue ~€1.3bn, ~9,000 employees, positioning it to capture parts of a ~€500bn smart-grid pipeline to 2030.

| Metric | Value |

|---|---|

| 2024 revenue | €1.3bn |

| Employees | 9,000 |

| 2024–25 regional capex | €120–€150bn |

| Security upgrades 2024–25 | €4.5bn |

| EU CEF (2021–27) | €42.3bn |

| Smart-grid pipeline to 2030 | €500bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Eltel across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights tied to the company’s Nordic/European infrastructure-services context.

A concise, visually segmented PESTLE summary for Eltel that can be dropped into presentations or planning sessions to quickly align teams on external risks, market positioning, and regulatory impacts.

Economic factors

Interest Rate Environment and Capital Costs

Persistent mid-2020s rate volatility raised Eltel’s average borrowing cost; Nordic corporate bond yields rose to ~3.5–4.5% in 2024–25, pushing weighted average debt costs higher and increasing capex financing expenses for its capital-intensive projects.

Eltel must balance refinancing maturing debt (net debt ~EUR 300–400m range in 2024 reported) with clients’ shifting investment appetite, as utilities delay discretionary spend when rates are elevated.

Despite slower private investment during high-rate periods, demand for grid maintenance and critical infrastructure kept revenue resilience, with recurring service contracts cushioning margin pressure.

Labor Market Pressures and Wage Inflation

The Nordic region faces a structural shortage of skilled technicians and engineers, with OECD data showing vacancy rates in technical occupations near 3.5% in 2024 and average technician wages rising 6–8% year-on-year; this drives recruitment costs for Eltel. Eltel’s profitability depends on controlling labor expenses while retaining quality staff—wage inflation pushed gross margin pressure in 2024, where sector peers reported EBITDA margin compressions of 100–250 bps. Economic competition for technical talent—from utilities, telecoms and renewables—remains a primary challenge to Eltel’s operational margins, with industry hiring costs up roughly 20% since 2021.

Utility Sector Capital Expenditure Trends

The economic health of major utility providers and telecom operators determines contract flow for Eltel; for example, European utilities increased grid capex to about €90–€110 billion in 2024 while EU broadband investment topped €30 billion, redirecting spend toward grid modernization and fiber expansion. Eltel’s revenue is therefore highly sensitive to these multi-year investment cycles—company order intake fell 12% in 2023 when several large customers delayed projects.

Currency Fluctuations in Nordic Markets

Operating across Sweden, Norway, Denmark and Finland exposes Eltel to FX risk; NOK/SEK moved ~8% vs EUR in 2024, pressuring reported EBITDA when translated to euros.

Currency swings also raise imported materials costs—steel and equipment prices invoiced in euros/dollars rose ~6% in 2024, compressing margins.

Effective hedging and local-currency contracts are essential; using forwards/options and invoicing 60–80% of contracts in local currency can stabilize cash flows.

- Multi-currency exposure: SEK, NOK, DKK, EUR, EUR volatility ~6–8% in 2024

- Material price impact: imported equipment +6% in 2024

- Hedge practice: forwards/options; local invoicing target 60–80%

Supply Chain Stabilization and Material Costs

Global supply chains have largely stabilized since 2022, but copper and aluminum prices stayed volatile—copper averaged about 9,000 USD/t in 2024 and rose ~15% YTD into 2025—pressuring input costs for Eltel.

Eltel must actively hedge and renegotiate cost pass-throughs in long-term service contracts to prevent margin erosion; materials swings can shift project margins by several percentage points.

Commodity market shifts directly affect bid pricing and profitability on large infrastructure projects, where material costs can represent 10–30% of total project value.

- 2024 copper avg ~9,000 USD/t; up ~15% YTD in 2025

- Materials often 10–30% of project costs

- Hedging and contract pass-throughs essential to protect margins

Refinancing, wage and material inflation squeeze margins amid FX and capex swings

Higher borrowing costs (Nordic bond yields ~3.5–4.5% in 2024) and net debt ~EUR 300–400m in 2024 raise refinancing pressure; wage inflation (technician pay +6–8% in 2024) and material inflation (imported equipment +6% in 2024; copper ~9,000 USD/t in 2024, +15% YTD 2025) compress margins; FX swings (~8% NOK/SEK vs EUR in 2024) and utility capex cycles (grid capex €90–110bn in 2024) drive revenue sensitivity.

| Metric | 2024/2025 |

|---|---|

| Nordic bond yields | 3.5–4.5% |

| Net debt | EUR 300–400m |

| Technician wage growth | +6–8% |

| Imported equipment | +6% |

| Copper | ~9,000 USD/t (+15% YTD 2025) |

| FX moves (NOK/SEK vs EUR) | ~8% |

| Grid capex EU | €90–110bn |

Same Document Delivered

Eltel PESTLE Analysis

The preview shown here is the exact Eltel PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Get a clear view of how political shifts, regulatory pressures, economic cycles, and technological change are shaping Eltel’s prospects—our compact PESTLE highlights the most critical external risks and opportunities to inform your strategy. Ideal for investors and advisors, the full analysis delivers detailed, actionable insights and editable charts to accelerate decision-making. Purchase the complete PESTLE now for instant, board-ready intelligence.

Political factors

Nordic Energy Security and Sovereignty

Governments across Northern Europe are prioritizing energy independence, with EU and Nordic green recovery funds directing over €120bn to grid and resilience projects in 2024–25, reducing reliance on external suppliers amid geopolitical risks.

This shift drives massive investment into domestic power grids and decentralized renewables, creating demand for Eltel’s technical services—Nordic transmission & distribution capex rose ~18% y/y in 2024.

National security policies now classify energy and communications as critical infrastructure, unlocking multi-year, government-backed contracts and sustaining a steady pipeline of projects for Eltel.

EU Infrastructure Funding and Green Deal

EU allocates large funds—Connecting Europe Facility budget rose to 42.3 billion EUR for 2021–2027 and the EU Green Deal mobilises an estimated 1 trillion EUR of sustainable investment by 2030—targeting cross-border grids and broadband in underserved regions, directly increasing demand for grid upgrades and fibre rollout.

Geopolitical Resilience and Defense Strategy

Increased regional tensions have pushed Nordic and Baltic states to harden critical infrastructure; governments allocated about EUR 4.5bn in 2024–2025 for security upgrades and cyber resilience across energy and telecom sectors.

Political mandates now require utility and telecom providers to boost physical security and network redundancy, raising CAPEX and service contracts for integrators by an estimated 12–18% in 2025.

Eltel, with ~8,000 employees in the region and 2024 revenue near EUR 1.2bn, is positioned as a trusted local partner to implement high-security upgrades for state-owned and private operators.

National Decarbonization Mandates

National net-zero commitments (over 130 countries covering >80% of global emissions as of 2025) are driving laws for rapid electrification of heat and transport, raising EU and UK targets for EVs and heat pumps that could triple electricity demand by 2050, requiring significant network upgrades.

Aggressive fossil-fuel phase-out timelines (e.g., EU 2035 combustion-engine sales ban) force immediate reinforcement of distribution grids; Eltel’s grid-strengthening services are critical to deliver legally binding climate targets and capture portions of the ~€500bn European smart-grid investment pipeline to 2030.

- 130+ countries net-zero by mid-century

- Electricity demand could triple by 2050

- EU combustion-engine sales ban from 2035

- €500bn European smart-grid investment to 2030

Public Procurement and Tendering Policies

Nordic procurement increasingly favors suppliers with strong social responsibility and local economic impact; tenders now weight non-financial criteria up to 30% in some countries—Finland and Sweden introduced guidelines in 2023–24 emphasizing job creation and domestic supply chain resilience.

Eltel’s 40+ year Northern European presence and 2024 revenue of ~EUR 1.3bn and 9,000 employees position it to win tenders prioritizing local content and employment impact.

- Non-financial criteria weight up to 30% in recent Nordic tenders

- Eltel revenue ~EUR 1.3bn (2024), ~9,000 employees

- Strong local footprint boosts competitiveness in public contracts

Eltel poised to grab slice of €500bn smart‑grid boom as Europe pours €120–150bn into grids

Political support for energy independence and security is driving €120–€150bn in 2024–25 grid/ resilience spend across Northern Europe, plus ~€4.5bn for security upgrades; EU funds (Connecting Europe Facility €42.3bn) and net-zero rules boost demand for Eltel’s services—2024 revenue ~€1.3bn, ~9,000 employees, positioning it to capture parts of a ~€500bn smart-grid pipeline to 2030.

| Metric | Value |

|---|---|

| 2024 revenue | €1.3bn |

| Employees | 9,000 |

| 2024–25 regional capex | €120–€150bn |

| Security upgrades 2024–25 | €4.5bn |

| EU CEF (2021–27) | €42.3bn |

| Smart-grid pipeline to 2030 | €500bn |

What is included in the product

Explores how external macro-environmental factors uniquely affect Eltel across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights tied to the company’s Nordic/European infrastructure-services context.

A concise, visually segmented PESTLE summary for Eltel that can be dropped into presentations or planning sessions to quickly align teams on external risks, market positioning, and regulatory impacts.

Economic factors

Interest Rate Environment and Capital Costs

Persistent mid-2020s rate volatility raised Eltel’s average borrowing cost; Nordic corporate bond yields rose to ~3.5–4.5% in 2024–25, pushing weighted average debt costs higher and increasing capex financing expenses for its capital-intensive projects.

Eltel must balance refinancing maturing debt (net debt ~EUR 300–400m range in 2024 reported) with clients’ shifting investment appetite, as utilities delay discretionary spend when rates are elevated.

Despite slower private investment during high-rate periods, demand for grid maintenance and critical infrastructure kept revenue resilience, with recurring service contracts cushioning margin pressure.

Labor Market Pressures and Wage Inflation

The Nordic region faces a structural shortage of skilled technicians and engineers, with OECD data showing vacancy rates in technical occupations near 3.5% in 2024 and average technician wages rising 6–8% year-on-year; this drives recruitment costs for Eltel. Eltel’s profitability depends on controlling labor expenses while retaining quality staff—wage inflation pushed gross margin pressure in 2024, where sector peers reported EBITDA margin compressions of 100–250 bps. Economic competition for technical talent—from utilities, telecoms and renewables—remains a primary challenge to Eltel’s operational margins, with industry hiring costs up roughly 20% since 2021.

Utility Sector Capital Expenditure Trends

The economic health of major utility providers and telecom operators determines contract flow for Eltel; for example, European utilities increased grid capex to about €90–€110 billion in 2024 while EU broadband investment topped €30 billion, redirecting spend toward grid modernization and fiber expansion. Eltel’s revenue is therefore highly sensitive to these multi-year investment cycles—company order intake fell 12% in 2023 when several large customers delayed projects.

Currency Fluctuations in Nordic Markets

Operating across Sweden, Norway, Denmark and Finland exposes Eltel to FX risk; NOK/SEK moved ~8% vs EUR in 2024, pressuring reported EBITDA when translated to euros.

Currency swings also raise imported materials costs—steel and equipment prices invoiced in euros/dollars rose ~6% in 2024, compressing margins.

Effective hedging and local-currency contracts are essential; using forwards/options and invoicing 60–80% of contracts in local currency can stabilize cash flows.

- Multi-currency exposure: SEK, NOK, DKK, EUR, EUR volatility ~6–8% in 2024

- Material price impact: imported equipment +6% in 2024

- Hedge practice: forwards/options; local invoicing target 60–80%

Supply Chain Stabilization and Material Costs

Global supply chains have largely stabilized since 2022, but copper and aluminum prices stayed volatile—copper averaged about 9,000 USD/t in 2024 and rose ~15% YTD into 2025—pressuring input costs for Eltel.

Eltel must actively hedge and renegotiate cost pass-throughs in long-term service contracts to prevent margin erosion; materials swings can shift project margins by several percentage points.

Commodity market shifts directly affect bid pricing and profitability on large infrastructure projects, where material costs can represent 10–30% of total project value.

- 2024 copper avg ~9,000 USD/t; up ~15% YTD in 2025

- Materials often 10–30% of project costs

- Hedging and contract pass-throughs essential to protect margins

Refinancing, wage and material inflation squeeze margins amid FX and capex swings

Higher borrowing costs (Nordic bond yields ~3.5–4.5% in 2024) and net debt ~EUR 300–400m in 2024 raise refinancing pressure; wage inflation (technician pay +6–8% in 2024) and material inflation (imported equipment +6% in 2024; copper ~9,000 USD/t in 2024, +15% YTD 2025) compress margins; FX swings (~8% NOK/SEK vs EUR in 2024) and utility capex cycles (grid capex €90–110bn in 2024) drive revenue sensitivity.

| Metric | 2024/2025 |

|---|---|

| Nordic bond yields | 3.5–4.5% |

| Net debt | EUR 300–400m |

| Technician wage growth | +6–8% |

| Imported equipment | +6% |

| Copper | ~9,000 USD/t (+15% YTD 2025) |

| FX moves (NOK/SEK vs EUR) | ~8% |

| Grid capex EU | €90–110bn |

Same Document Delivered

Eltel PESTLE Analysis

The preview shown here is the exact Eltel PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.