Emaar Properties Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

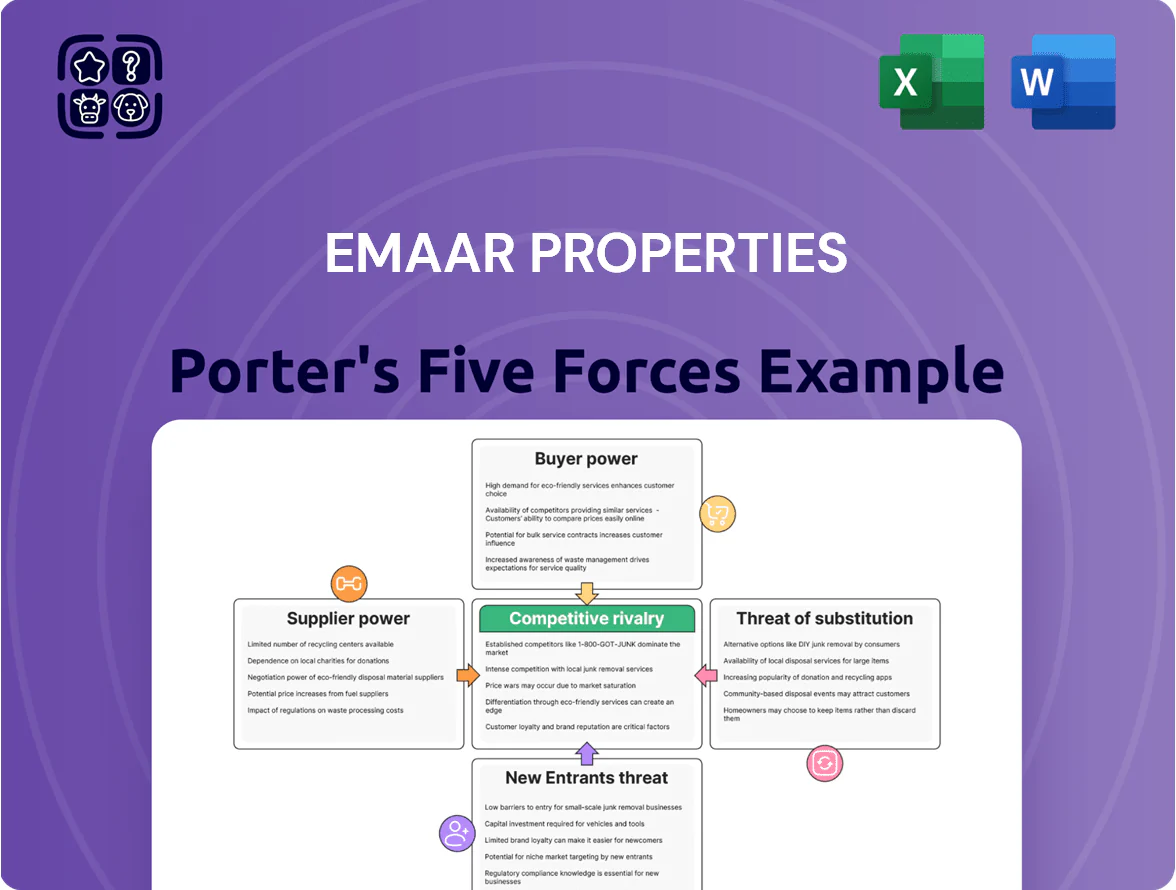

Emaar Properties navigates intense industry rivalry, moderate supplier leverage, and rising buyer expectations amid high capital barriers and evolving substitute offerings in real estate and hospitality.

Suppliers Bargaining Power

Concentration of construction and engineering firms

The pool of Tier-1 contractors able to execute Emaar Properties’ large-scale projects is small, giving suppliers negotiation leverage; about 8–12 regional/global firms win most Dubai mega-project contracts.

Emaar offsets this by long-term strategic partnerships and a steady pipeline—revenues of AED 9.5bn in 2024 helped secure repeat work and preferred pricing.

By end-2025 Emaar’s scale lets it dictate many commercial terms, yet smart-building integration suppliers remain supplier-heavy, with niche specialists commanding 15–30% premium.

Governmental control over land banks

In Dubai, the government is the primary supplier of land, the key input for developers, and holds large stakes in Emaar Properties (the government and related entities held ~29% as of Dec 2024), which skews supplier power in Emaar’s favor.

This privileged tie gives Emaar priority access to flagship plots such as Dubai Creek Harbour, lowering land acquisition costs and reducing typical supplier pressure seen in private markets.

Volatility in global raw material costs

Suppliers of steel, cement, and glass face international commodity swings, and Emaar’s 2024–2025 development margins were squeezed when steel spiked ~28% YoY and cement rose ~12% in 2024.

Emaar uses bulk contracts—$1.2bn procurement in 2024—to lock prices, but essential materials let suppliers pass through inflation during supply shocks.

By late 2025 Emaar shifted toward vertical procurement, adding on-site batching and preferred JV suppliers, cutting material cost volatility exposure by an estimated 6–9%.

Availability of specialized architectural and design talent

Emaar depends on a few top global firms for flagship projects like Burj Khalifa and Dubai Mall, giving these firms high bargaining power because of brand equity and technical complexity; flagship design fees can command premiums of 10–25% on project budgets, per 2024 industry reports. Emaar lowers risk by expanding its roster of design partners and scaling in-house design teams, which handled ~18% of design work in 2024, up from 10% in 2020.

- Few elite firms → higher supplier power

- Design premiums ~10–25% on flagship budgets (2024)

- In-house design rose to ~18% of work in 2024

- Diversified partner roster reduces single-vendor risk

Reliance on specialized technology and proptech providers

As buildings adopt AI and IoT, suppliers of cloud, sensors and platforms gain leverage over developers; global tech vendors now command higher margins and long lead times.

Emaar’s 2025 push—committing about $500m to smart-city projects—raises dependence on a few firms for software/hardware integration.

To reduce supplier power, Emaar formed tech investment arms in 2023–24 to co-develop proprietary systems and keep platform control.

- 2025 smart-city capex ~$500m

- Dependency on 3–4 global vendors

- In-house tech arms launched 2023–24

Emaar’s scale and gov’t ties shift supplier power back to the developer

Few Tier‑1 contractors and niche tech/design suppliers give suppliers moderate-to-high bargaining power, but Emaar’s scale, AED 9.5bn 2024 revenues, ~29% government-related stake (Dec 2024), $1.2bn 2024 procurement, $500m 2025 smart-city capex, and rising in‑house work (design 18% in 2024) tilt power back to Emaar.

| Item | 2024–2025 metric |

|---|---|

| Revenue | AED 9.5bn (2024) |

| Govt stake | ~29% (Dec 2024) |

| Procurement | $1.2bn (2024) |

| Smart-city capex | $500m (2025) |

| In-house design | 18% (2024) |

What is included in the product

Tailored exclusively for Emaar Properties, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats that shape its pricing, profitability, and market defense.

A concise Porter's Five Forces snapshot for Emaar Properties—quickly gauge competitive intensity and strategic risk to inform investment or corporate decisions.

Customers Bargaining Power

High availability of luxury residential alternatives

Buyers in Dubai can choose among high-end projects from Nakheel, Damac, and Sobha, raising their bargaining power as luxury inventory hit ~48,000 units in 2024, up 12% year-on-year.

This choice forces Emaar to push amenities, community lifestyle and signature architecture to protect premium ASPs—Emaar reported AED 55,000/sqm in prime Downtown by 2024.

By end-2025 the market is buyer-centric: customization and post-handover services drive sales, with 60% of high-net-worth buyers stating these factors influenced purchase decisions in 2025 surveys.

Price sensitivity of institutional and retail investors

A large share of Emaar Properties buyers are global institutional and retail investors chasing yields and capital gains; in 2024 non-UAE buyers accounted for about 60% of Dubai real-estate transactions, raising price sensitivity.

These investors are capital-mobile and can redirect funds to competing emerging markets if Emaar’s pricing or IRR projections lag peers, so even 100–200 bps yield gaps matter.

Emaar must offer competitive payment plans and publish transparent sales, delivery, and rental yield data—investors demand quarterly KPIs and clear cash-flow schedules to meet their analytical thresholds.

Influence of large-scale commercial and retail tenants

Major global brands and anchor tenants in Emaar’s retail and office portfolios can demand favorable lease terms and fit-out contributions; for example, anchor leases at The Dubai Mall account for roughly 25% of annual footfall, so losing one can cut traffic and EBITDA at the mall level significantly.

Emaar offsets tenant bargaining by using high-traffic assets—The Dubai Mall saw 66 million visitors in 2023—and a steady waiting list of international brands, keeping vacancy below 6% across Emaar Malls in 2024 and rebalancing negotiating leverage.

Impact of digital transparency and market data

By 2025, real estate tech gave buyers clear access to historical prices, service charges, and developer track records, cutting information asymmetry and enabling tougher negotiation on listings up to 8–12% below asking in Dubai resale markets.

Emaar counters by upgrading its digital sales portals with live market data, detailed pricing histories, and verified reviews to speed decisions and raise conversion; digital leads rose 22% year-over-year in 2024.

These tools shift bargaining power toward informed customers but also let Emaar protect margins via brand trust and faster, data-driven sales cycles.

- 2025: platforms publish historical prices, service charges, track records

- Buyer leverage: 8–12% negotiation on resale listings (Dubai)

- Emaar action: new data-rich portals; digital leads +22% in 2024

Low switching costs in the secondary market

Low switching costs in Dubai’s secondary market let buyers choose pre-owned Emaar or rival units for immediate occupancy or yield; in 2024 Dubai resale transactions rose ~18% YoY to ~30,000 units, raising competitive pressure on off-plan sales.

Secondary liquidity means Emaar competes with its past stock and peers, so it emphasizes premium property management and community upkeep to keep resale premiums; Emaar reported 6–10% higher resale prices in flagship communities in 2024.

- Resale volume ~30,000 units 2024

- Resale +18% YoY

- Emaar resale premium 6–10% 2024

Buyers Gain Leverage as Dubai Luxury Supply Rises; Emaar Leans on Brand & Leads

Buyers hold strong leverage: 2024 luxury inventory ~48,000 units (+12% YoY) and resale volume ~30,000 (+18% YoY) let purchasers negotiate 8–12% off asking; non-UAE buyers were ~60% of transactions in 2024, increasing price sensitivity. Emaar defends premiums via amenities, brand, 66m mall visits (2023) and digital leads +22% (2024), while offering clearer KPIs and payment plans.

| Metric | 2023–2025 |

|---|---|

| Luxury inventory | 48,000 (2024) |

| Resale volume | 30,000 (2024) |

| Non-UAE buyer share | ~60% (2024) |

| Negotiation range | 8–12% (resale) |

| Dubai Mall visits | 66m (2023) |

| Digital leads | +22% (2024) |

Preview the Actual Deliverable

Emaar Properties Porter's Five Forces Analysis

This preview shows the exact Emaar Properties Porter’s Five Forces analysis you'll receive—no placeholders or samples; the full, professionally formatted document is available for immediate download after purchase.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Emaar Properties navigates intense industry rivalry, moderate supplier leverage, and rising buyer expectations amid high capital barriers and evolving substitute offerings in real estate and hospitality.

Suppliers Bargaining Power

Concentration of construction and engineering firms

The pool of Tier-1 contractors able to execute Emaar Properties’ large-scale projects is small, giving suppliers negotiation leverage; about 8–12 regional/global firms win most Dubai mega-project contracts.

Emaar offsets this by long-term strategic partnerships and a steady pipeline—revenues of AED 9.5bn in 2024 helped secure repeat work and preferred pricing.

By end-2025 Emaar’s scale lets it dictate many commercial terms, yet smart-building integration suppliers remain supplier-heavy, with niche specialists commanding 15–30% premium.

Governmental control over land banks

In Dubai, the government is the primary supplier of land, the key input for developers, and holds large stakes in Emaar Properties (the government and related entities held ~29% as of Dec 2024), which skews supplier power in Emaar’s favor.

This privileged tie gives Emaar priority access to flagship plots such as Dubai Creek Harbour, lowering land acquisition costs and reducing typical supplier pressure seen in private markets.

Volatility in global raw material costs

Suppliers of steel, cement, and glass face international commodity swings, and Emaar’s 2024–2025 development margins were squeezed when steel spiked ~28% YoY and cement rose ~12% in 2024.

Emaar uses bulk contracts—$1.2bn procurement in 2024—to lock prices, but essential materials let suppliers pass through inflation during supply shocks.

By late 2025 Emaar shifted toward vertical procurement, adding on-site batching and preferred JV suppliers, cutting material cost volatility exposure by an estimated 6–9%.

Availability of specialized architectural and design talent

Emaar depends on a few top global firms for flagship projects like Burj Khalifa and Dubai Mall, giving these firms high bargaining power because of brand equity and technical complexity; flagship design fees can command premiums of 10–25% on project budgets, per 2024 industry reports. Emaar lowers risk by expanding its roster of design partners and scaling in-house design teams, which handled ~18% of design work in 2024, up from 10% in 2020.

- Few elite firms → higher supplier power

- Design premiums ~10–25% on flagship budgets (2024)

- In-house design rose to ~18% of work in 2024

- Diversified partner roster reduces single-vendor risk

Reliance on specialized technology and proptech providers

As buildings adopt AI and IoT, suppliers of cloud, sensors and platforms gain leverage over developers; global tech vendors now command higher margins and long lead times.

Emaar’s 2025 push—committing about $500m to smart-city projects—raises dependence on a few firms for software/hardware integration.

To reduce supplier power, Emaar formed tech investment arms in 2023–24 to co-develop proprietary systems and keep platform control.

- 2025 smart-city capex ~$500m

- Dependency on 3–4 global vendors

- In-house tech arms launched 2023–24

Emaar’s scale and gov’t ties shift supplier power back to the developer

Few Tier‑1 contractors and niche tech/design suppliers give suppliers moderate-to-high bargaining power, but Emaar’s scale, AED 9.5bn 2024 revenues, ~29% government-related stake (Dec 2024), $1.2bn 2024 procurement, $500m 2025 smart-city capex, and rising in‑house work (design 18% in 2024) tilt power back to Emaar.

| Item | 2024–2025 metric |

|---|---|

| Revenue | AED 9.5bn (2024) |

| Govt stake | ~29% (Dec 2024) |

| Procurement | $1.2bn (2024) |

| Smart-city capex | $500m (2025) |

| In-house design | 18% (2024) |

What is included in the product

Tailored exclusively for Emaar Properties, this Porter's Five Forces overview uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats that shape its pricing, profitability, and market defense.

A concise Porter's Five Forces snapshot for Emaar Properties—quickly gauge competitive intensity and strategic risk to inform investment or corporate decisions.

Customers Bargaining Power

High availability of luxury residential alternatives

Buyers in Dubai can choose among high-end projects from Nakheel, Damac, and Sobha, raising their bargaining power as luxury inventory hit ~48,000 units in 2024, up 12% year-on-year.

This choice forces Emaar to push amenities, community lifestyle and signature architecture to protect premium ASPs—Emaar reported AED 55,000/sqm in prime Downtown by 2024.

By end-2025 the market is buyer-centric: customization and post-handover services drive sales, with 60% of high-net-worth buyers stating these factors influenced purchase decisions in 2025 surveys.

Price sensitivity of institutional and retail investors

A large share of Emaar Properties buyers are global institutional and retail investors chasing yields and capital gains; in 2024 non-UAE buyers accounted for about 60% of Dubai real-estate transactions, raising price sensitivity.

These investors are capital-mobile and can redirect funds to competing emerging markets if Emaar’s pricing or IRR projections lag peers, so even 100–200 bps yield gaps matter.

Emaar must offer competitive payment plans and publish transparent sales, delivery, and rental yield data—investors demand quarterly KPIs and clear cash-flow schedules to meet their analytical thresholds.

Influence of large-scale commercial and retail tenants

Major global brands and anchor tenants in Emaar’s retail and office portfolios can demand favorable lease terms and fit-out contributions; for example, anchor leases at The Dubai Mall account for roughly 25% of annual footfall, so losing one can cut traffic and EBITDA at the mall level significantly.

Emaar offsets tenant bargaining by using high-traffic assets—The Dubai Mall saw 66 million visitors in 2023—and a steady waiting list of international brands, keeping vacancy below 6% across Emaar Malls in 2024 and rebalancing negotiating leverage.

Impact of digital transparency and market data

By 2025, real estate tech gave buyers clear access to historical prices, service charges, and developer track records, cutting information asymmetry and enabling tougher negotiation on listings up to 8–12% below asking in Dubai resale markets.

Emaar counters by upgrading its digital sales portals with live market data, detailed pricing histories, and verified reviews to speed decisions and raise conversion; digital leads rose 22% year-over-year in 2024.

These tools shift bargaining power toward informed customers but also let Emaar protect margins via brand trust and faster, data-driven sales cycles.

- 2025: platforms publish historical prices, service charges, track records

- Buyer leverage: 8–12% negotiation on resale listings (Dubai)

- Emaar action: new data-rich portals; digital leads +22% in 2024

Low switching costs in the secondary market

Low switching costs in Dubai’s secondary market let buyers choose pre-owned Emaar or rival units for immediate occupancy or yield; in 2024 Dubai resale transactions rose ~18% YoY to ~30,000 units, raising competitive pressure on off-plan sales.

Secondary liquidity means Emaar competes with its past stock and peers, so it emphasizes premium property management and community upkeep to keep resale premiums; Emaar reported 6–10% higher resale prices in flagship communities in 2024.

- Resale volume ~30,000 units 2024

- Resale +18% YoY

- Emaar resale premium 6–10% 2024

Buyers Gain Leverage as Dubai Luxury Supply Rises; Emaar Leans on Brand & Leads

Buyers hold strong leverage: 2024 luxury inventory ~48,000 units (+12% YoY) and resale volume ~30,000 (+18% YoY) let purchasers negotiate 8–12% off asking; non-UAE buyers were ~60% of transactions in 2024, increasing price sensitivity. Emaar defends premiums via amenities, brand, 66m mall visits (2023) and digital leads +22% (2024), while offering clearer KPIs and payment plans.

| Metric | 2023–2025 |

|---|---|

| Luxury inventory | 48,000 (2024) |

| Resale volume | 30,000 (2024) |

| Non-UAE buyer share | ~60% (2024) |

| Negotiation range | 8–12% (resale) |

| Dubai Mall visits | 66m (2023) |

| Digital leads | +22% (2024) |

Preview the Actual Deliverable

Emaar Properties Porter's Five Forces Analysis

This preview shows the exact Emaar Properties Porter’s Five Forces analysis you'll receive—no placeholders or samples; the full, professionally formatted document is available for immediate download after purchase.