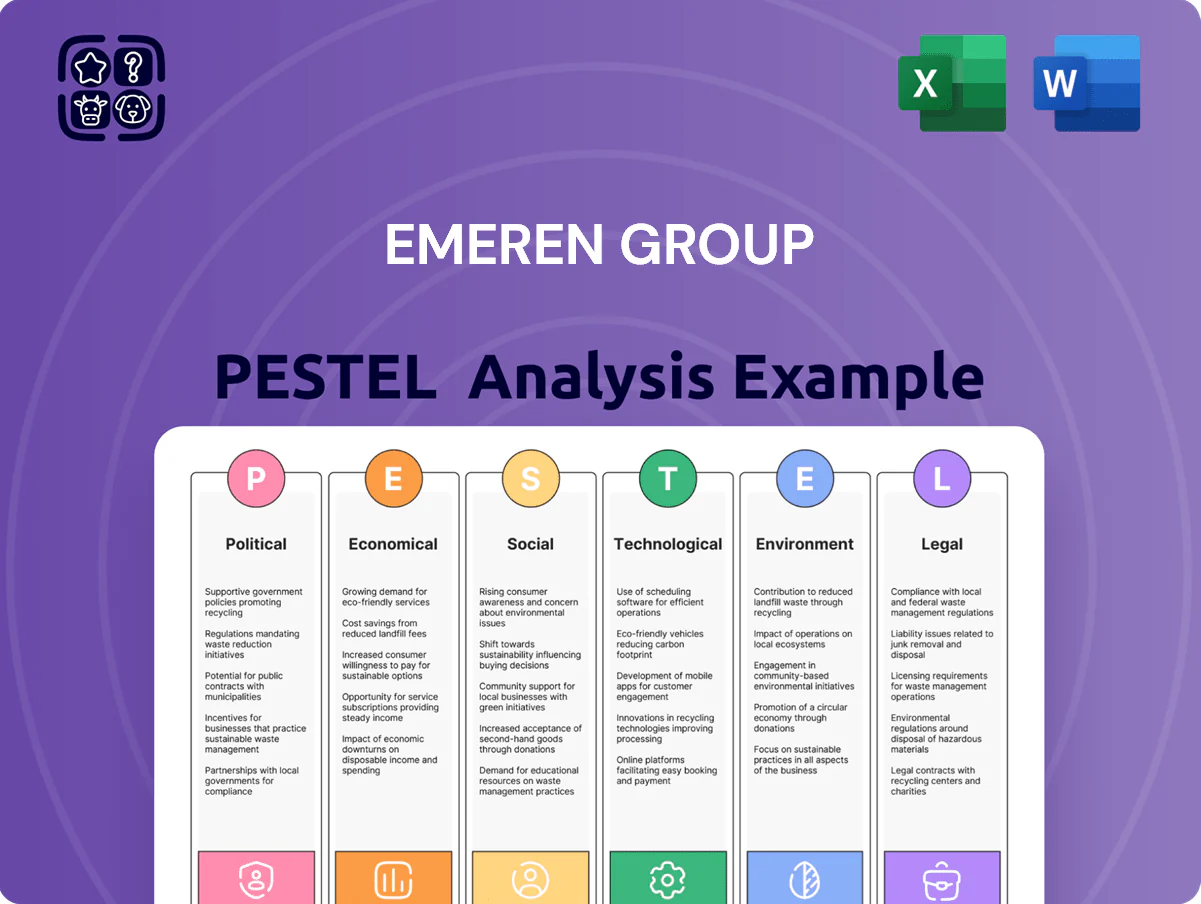

Emeren Group PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how geopolitical shifts, regulatory changes, and emerging technologies are shaping Emeren Group’s strategic outlook in our concise PESTLE snapshot—ideal for investors and strategists seeking fast, actionable context. Purchase the full PESTLE for a comprehensive, editable report with deep dives into economic risks, social trends, legal exposures, and environmental factors to inform smarter decisions.

Political factors

EU Energy Sovereignty Initiatives

EU drive for energy sovereignty boosts firms like Emeren as REPowerEU targets cutting Russian gas imports by 2030 and mobilized over €300 billion in investments; member states sped permitting, raising solar capacity additions to ~70 GW in 2023 and aiming for >100 GW/yr by 2025 under accelerated targets.

US Trade Policy and Tariffs

Trade tensions and tariffs between the US and major solar suppliers, notably China, directly impact Emeren Group's North American margins; US duties on PV cells/modules (up to 50%+ in recent Section 201/301 measures) have raised import costs by an estimated 20–40% for many developers in 2024–25.

Ongoing tariffs force Emeren to prioritize domestic manufacturing partnerships or source from approved countries like Vietnam and Malaysia, where module prices averaged $0.18–0.22/W in 2025 versus $0.14–0.16/W for Chinese imports pre-tariff.

Political uncertainty over long-term enforcement of the Inflation Reduction Act tax credits and domestic content rules affects Emeren's capital allocation and project timelines, with IRA-driven investment flows to US solar rising to $78 billion in 2024 but contingent on persistent policy clarity.

Geopolitical Tensions in Supply Chains

Persistent geopolitical instability in Eastern Europe and rising US-China trade tensions have disrupted supply chains for renewables, with European solar module imports from affected regions dropping ~22% YoY in 2024, forcing Emeren to diversify suppliers across 8+ countries to reduce concentration risk.

Trade friction in Asia increased component lead times by an average of 35% in 2024, prompting Emeren to hold strategic inventory equal to ~3 months of sales and seek alternate logistics corridors to avoid political blockades.

Growing political pressure to decouple critical infrastructure from certain foreign vendors has already led regulators in 12 EU states to recommend vendor restrictions, potentially necessitating Emeren to reorient technology partnerships and incur one-time transition costs estimated at €18–25m.

Government Subsidies and Incentives

National governments are scaling tax credits and direct subsidies to hit 2030 climate targets, with global renewables subsidies reaching an estimated 160 billion USD in 2024, boosting solar LCOE competitiveness.

Emeren depends on policy continuity to preserve project IRRs—a 5–8 percentage-point incentive-driven uplift is typical—and to secure institutional capital commitments.

Sudden political shifts can sunset incentives (eg, 2023–25 policy reversals in select markets), so Emeren must keep a flexible, geographically diversified pipeline to mitigate country risk.

- 2024 global renewables subsidies ~160B USD

- Incentives can add ~5–8pp to project IRR

- Geographic diversification reduces policy revocation risk

Cross-border Energy Cooperation

Political agreements on interconnected European grids now enable cross-border solar transmission, with EU targets pushing interconnection to 15% of installed capacity by 2030 and planned investments of €60–90 billion in grid links (EC, 2024), allowing Emeren to site projects in sun-rich Spain and sell into industrial hubs like Germany and the Netherlands.

These diplomatic frameworks let Emeren optimize load factors and revenue arbitrage—merchant power prices in 2024 averaged €120/MWh in Germany vs €45/MWh in Spain—boosting utility-scale asset profitability if interconnection capacity is secured and regulated.

- EU grid interconnection target 15% by 2030; €60–90bn planned links (2024)

- Price spread example 2024: Germany €120/MWh vs Spain €45/MWh

- Cross-border frameworks critical for Emeren’s revenue arbitrage and asset utilization

EU & US policies reshape solar: €300B mobilized, tariffs spike module costs, >100GW/yr target

EU energy sovereignty and REPowerEU mobilized €300B+ to 2030, boosting solar to ~70 GW added in 2023 and targets >100 GW/yr by 2025; US tariffs raised PV import costs ~20–40% in 2024–25, prompting Emeren to source from Vietnam/Malaysia where modules were $0.18–0.22/W in 2025 versus pre-tariff China $0.14–0.16/W; renewables subsidies ~160B USD in 2024 added ~5–8pp to project IRRs; EU grid links €60–90B planned, targeting 15% interconnection by 2030.

| Metric | 2024–25 Value |

|---|---|

| Global renewables subsidies | $160B |

| Solar additions (2023) | ~70 GW |

| Target solar additions (2025) | >100 GW/yr |

| Module price (Vietnam/Malaysia 2025) | $0.18–0.22/W |

| Pre-tariff China price | $0.14–0.16/W |

| PV import cost impact (tariffs) | +20–40% |

| Incentive IRR uplift | +5–8 pp |

| EU grid links planned | €60–90B; 15% interconnection by 2030 |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Emeren Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to reveal threats, opportunities, and strategic implications for executives, investors, and consultants.

A concise, visually segmented PESTLE summary for Emeren Group that’s easy to drop into presentations, share across teams, and customize with region- or business-specific notes to streamline external risk discussions and strategic planning.

Economic factors

Interest Rate Environment

As of late 2025, global policy rates have largely stabilized—US Fed funds around 5.25–5.50% and ECB deposit near 4.0%—giving Emeren more predictable debt costs for capital-intensive solar projects and improving NPV on long-term PPAs; with average project leverage at ~60% and blended borrowing yields falling ~150 bps vs 2023, margins widen, though management must hedge inflation risks after 2024–25 CPI averaged 3.8% which could push future borrowing costs higher.

Capital Expenditure Volatility

Fluctuations in polysilicon, silver and aluminum prices—polysilicon rose ~18% in 2024 and silver averaged $26/oz—directly raise per-MW solar installation costs, with module input costs swinging project budgets by up to 6–10% per year. Technological declines in LCOE (global utility-scale PV fell ~12% 2023–2025) temper long-term costs, but short-term volatility has caused >5% budget overruns on some 2024 development projects. Emeren’s use of fixed-price procurement and hedging, covering ~60% of 2025 material needs, is critical to stabilize margins across its global pipeline.

Global Energy Market Prices

Volatility in wholesale electricity prices—European baseload power swinging 40% in 2024 and US spot natural gas down ~25% YTD—directly affects solar’s appeal as a hedge versus fossil fuels.

High oil and gas costs, with Brent averaging $85/barrel in 2024, boost demand for Emeren’s solar solutions, while large gas price drops can erode short-term competitiveness.

Emeren balances merchant exposure with long-term PPA contracts (targeting 10–15-year fixed rates) to stabilize revenue and protect margins.

Currency Exchange Fluctuations

Operating across Europe, North America, and Asia exposes Emeren to foreign exchange risk when repatriating earnings or funding projects; in 2024, currency moves cost multinationals an estimated 0.5–1.2% of revenue annually, per industry surveys.

Appreciation of the US dollar versus the euro or yuan can reduce reported Euro-denominated margins; USD-EUR volatility averaged 8.6% in 2024.

Robust hedging and local-currency financing—Emeren could target covering 60–80% of near-term FX exposure—are essential to stabilize cash flows and protect reported results.

- Geographic FX exposure: Europe, North America, Asia

- 2024 USD-EUR volatility: ~8.6%

- Industry FX cost: ~0.5–1.2% revenue

- Suggested hedge coverage: 60–80% near-term exposure

Financing Availability for Renewables

The rise of green bonds—issuance reached about $540 billion in 2023 and global ESG fund assets surpassed $35 trillion by 2024—has expanded capital for renewables, benefiting Emeren as institutional investors seek steady, long-term returns from sustainable assets.

To access lower-cost capital versus traditional energy firms, Emeren must maintain a strong credit profile and transparent ESG reporting; green bond spreads averaged 20–50 bps tighter for high-ESG issuers in 2024.

- Green bond issuance: ~$540B (2023)

- Global ESG assets: >$35T (2024)

- Green bond spread advantage: 20–50 bps (2024)

Stable rates boost project finance; hedge 60–80% and secure 10–15y PPAs

Stable policy rates (2025: Fed 5.25–5.50%, ECB ~4.0%) improve project finance; 2024–25 CPI ~3.8% poses inflation risk. Material cost swings (polysilicon +18% in 2024; silver ~$26/oz) impact MW costs ~6–10%; LCOE fell ~12% (2023–25). FX volatility (USD-EUR ~8.6% in 2024) and merchant price swings drive need for 60–80% hedging and long-term PPAs (10–15y).

| Metric | Value |

|---|---|

| Fed/ECB (2025) | 5.25–5.50% / ~4.0% |

| CPI (2024–25) | ~3.8% |

| Polysilicon (2024) | +18% |

| USD-EUR vol (2024) | ~8.6% |

Same Document Delivered

Emeren Group PESTLE Analysis

The preview shown here is the exact Emeren Group PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Discover how geopolitical shifts, regulatory changes, and emerging technologies are shaping Emeren Group’s strategic outlook in our concise PESTLE snapshot—ideal for investors and strategists seeking fast, actionable context. Purchase the full PESTLE for a comprehensive, editable report with deep dives into economic risks, social trends, legal exposures, and environmental factors to inform smarter decisions.

Political factors

EU Energy Sovereignty Initiatives

EU drive for energy sovereignty boosts firms like Emeren as REPowerEU targets cutting Russian gas imports by 2030 and mobilized over €300 billion in investments; member states sped permitting, raising solar capacity additions to ~70 GW in 2023 and aiming for >100 GW/yr by 2025 under accelerated targets.

US Trade Policy and Tariffs

Trade tensions and tariffs between the US and major solar suppliers, notably China, directly impact Emeren Group's North American margins; US duties on PV cells/modules (up to 50%+ in recent Section 201/301 measures) have raised import costs by an estimated 20–40% for many developers in 2024–25.

Ongoing tariffs force Emeren to prioritize domestic manufacturing partnerships or source from approved countries like Vietnam and Malaysia, where module prices averaged $0.18–0.22/W in 2025 versus $0.14–0.16/W for Chinese imports pre-tariff.

Political uncertainty over long-term enforcement of the Inflation Reduction Act tax credits and domestic content rules affects Emeren's capital allocation and project timelines, with IRA-driven investment flows to US solar rising to $78 billion in 2024 but contingent on persistent policy clarity.

Geopolitical Tensions in Supply Chains

Persistent geopolitical instability in Eastern Europe and rising US-China trade tensions have disrupted supply chains for renewables, with European solar module imports from affected regions dropping ~22% YoY in 2024, forcing Emeren to diversify suppliers across 8+ countries to reduce concentration risk.

Trade friction in Asia increased component lead times by an average of 35% in 2024, prompting Emeren to hold strategic inventory equal to ~3 months of sales and seek alternate logistics corridors to avoid political blockades.

Growing political pressure to decouple critical infrastructure from certain foreign vendors has already led regulators in 12 EU states to recommend vendor restrictions, potentially necessitating Emeren to reorient technology partnerships and incur one-time transition costs estimated at €18–25m.

Government Subsidies and Incentives

National governments are scaling tax credits and direct subsidies to hit 2030 climate targets, with global renewables subsidies reaching an estimated 160 billion USD in 2024, boosting solar LCOE competitiveness.

Emeren depends on policy continuity to preserve project IRRs—a 5–8 percentage-point incentive-driven uplift is typical—and to secure institutional capital commitments.

Sudden political shifts can sunset incentives (eg, 2023–25 policy reversals in select markets), so Emeren must keep a flexible, geographically diversified pipeline to mitigate country risk.

- 2024 global renewables subsidies ~160B USD

- Incentives can add ~5–8pp to project IRR

- Geographic diversification reduces policy revocation risk

Cross-border Energy Cooperation

Political agreements on interconnected European grids now enable cross-border solar transmission, with EU targets pushing interconnection to 15% of installed capacity by 2030 and planned investments of €60–90 billion in grid links (EC, 2024), allowing Emeren to site projects in sun-rich Spain and sell into industrial hubs like Germany and the Netherlands.

These diplomatic frameworks let Emeren optimize load factors and revenue arbitrage—merchant power prices in 2024 averaged €120/MWh in Germany vs €45/MWh in Spain—boosting utility-scale asset profitability if interconnection capacity is secured and regulated.

- EU grid interconnection target 15% by 2030; €60–90bn planned links (2024)

- Price spread example 2024: Germany €120/MWh vs Spain €45/MWh

- Cross-border frameworks critical for Emeren’s revenue arbitrage and asset utilization

EU & US policies reshape solar: €300B mobilized, tariffs spike module costs, >100GW/yr target

EU energy sovereignty and REPowerEU mobilized €300B+ to 2030, boosting solar to ~70 GW added in 2023 and targets >100 GW/yr by 2025; US tariffs raised PV import costs ~20–40% in 2024–25, prompting Emeren to source from Vietnam/Malaysia where modules were $0.18–0.22/W in 2025 versus pre-tariff China $0.14–0.16/W; renewables subsidies ~160B USD in 2024 added ~5–8pp to project IRRs; EU grid links €60–90B planned, targeting 15% interconnection by 2030.

| Metric | 2024–25 Value |

|---|---|

| Global renewables subsidies | $160B |

| Solar additions (2023) | ~70 GW |

| Target solar additions (2025) | >100 GW/yr |

| Module price (Vietnam/Malaysia 2025) | $0.18–0.22/W |

| Pre-tariff China price | $0.14–0.16/W |

| PV import cost impact (tariffs) | +20–40% |

| Incentive IRR uplift | +5–8 pp |

| EU grid links planned | €60–90B; 15% interconnection by 2030 |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Emeren Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples to reveal threats, opportunities, and strategic implications for executives, investors, and consultants.

A concise, visually segmented PESTLE summary for Emeren Group that’s easy to drop into presentations, share across teams, and customize with region- or business-specific notes to streamline external risk discussions and strategic planning.

Economic factors

Interest Rate Environment

As of late 2025, global policy rates have largely stabilized—US Fed funds around 5.25–5.50% and ECB deposit near 4.0%—giving Emeren more predictable debt costs for capital-intensive solar projects and improving NPV on long-term PPAs; with average project leverage at ~60% and blended borrowing yields falling ~150 bps vs 2023, margins widen, though management must hedge inflation risks after 2024–25 CPI averaged 3.8% which could push future borrowing costs higher.

Capital Expenditure Volatility

Fluctuations in polysilicon, silver and aluminum prices—polysilicon rose ~18% in 2024 and silver averaged $26/oz—directly raise per-MW solar installation costs, with module input costs swinging project budgets by up to 6–10% per year. Technological declines in LCOE (global utility-scale PV fell ~12% 2023–2025) temper long-term costs, but short-term volatility has caused >5% budget overruns on some 2024 development projects. Emeren’s use of fixed-price procurement and hedging, covering ~60% of 2025 material needs, is critical to stabilize margins across its global pipeline.

Global Energy Market Prices

Volatility in wholesale electricity prices—European baseload power swinging 40% in 2024 and US spot natural gas down ~25% YTD—directly affects solar’s appeal as a hedge versus fossil fuels.

High oil and gas costs, with Brent averaging $85/barrel in 2024, boost demand for Emeren’s solar solutions, while large gas price drops can erode short-term competitiveness.

Emeren balances merchant exposure with long-term PPA contracts (targeting 10–15-year fixed rates) to stabilize revenue and protect margins.

Currency Exchange Fluctuations

Operating across Europe, North America, and Asia exposes Emeren to foreign exchange risk when repatriating earnings or funding projects; in 2024, currency moves cost multinationals an estimated 0.5–1.2% of revenue annually, per industry surveys.

Appreciation of the US dollar versus the euro or yuan can reduce reported Euro-denominated margins; USD-EUR volatility averaged 8.6% in 2024.

Robust hedging and local-currency financing—Emeren could target covering 60–80% of near-term FX exposure—are essential to stabilize cash flows and protect reported results.

- Geographic FX exposure: Europe, North America, Asia

- 2024 USD-EUR volatility: ~8.6%

- Industry FX cost: ~0.5–1.2% revenue

- Suggested hedge coverage: 60–80% near-term exposure

Financing Availability for Renewables

The rise of green bonds—issuance reached about $540 billion in 2023 and global ESG fund assets surpassed $35 trillion by 2024—has expanded capital for renewables, benefiting Emeren as institutional investors seek steady, long-term returns from sustainable assets.

To access lower-cost capital versus traditional energy firms, Emeren must maintain a strong credit profile and transparent ESG reporting; green bond spreads averaged 20–50 bps tighter for high-ESG issuers in 2024.

- Green bond issuance: ~$540B (2023)

- Global ESG assets: >$35T (2024)

- Green bond spread advantage: 20–50 bps (2024)

Stable rates boost project finance; hedge 60–80% and secure 10–15y PPAs

Stable policy rates (2025: Fed 5.25–5.50%, ECB ~4.0%) improve project finance; 2024–25 CPI ~3.8% poses inflation risk. Material cost swings (polysilicon +18% in 2024; silver ~$26/oz) impact MW costs ~6–10%; LCOE fell ~12% (2023–25). FX volatility (USD-EUR ~8.6% in 2024) and merchant price swings drive need for 60–80% hedging and long-term PPAs (10–15y).

| Metric | Value |

|---|---|

| Fed/ECB (2025) | 5.25–5.50% / ~4.0% |

| CPI (2024–25) | ~3.8% |

| Polysilicon (2024) | +18% |

| USD-EUR vol (2024) | ~8.6% |

Same Document Delivered

Emeren Group PESTLE Analysis

The preview shown here is the exact Emeren Group PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.