Enerflex Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

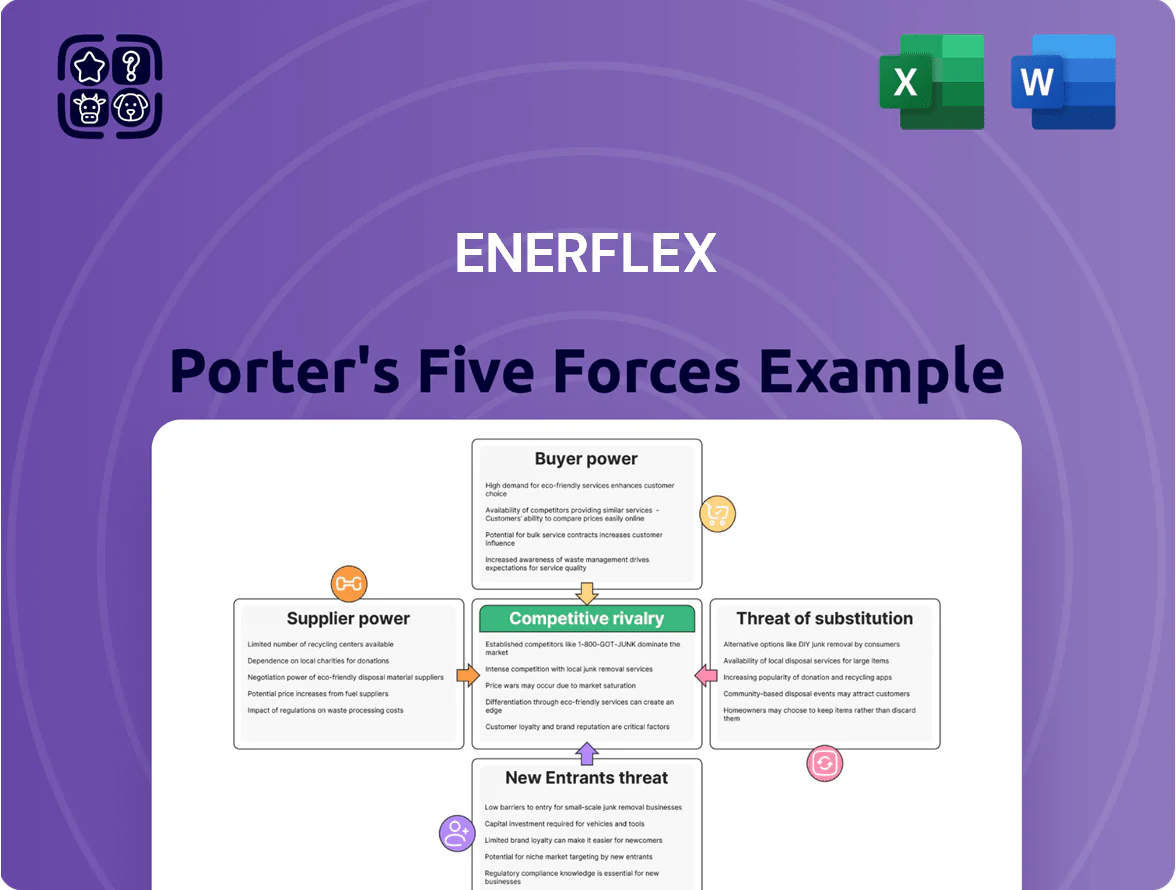

Enerflex faces moderate supplier power and fluctuating buyer demand driven by energy capex cycles, while the threat of new entrants is limited by high technical barriers and capital intensity.

Substitute threats remain low, but rivalry is elevated due to a concentrated field of global service providers competing on price and integrated solutions.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Enerflex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Critical Component Manufacturers

The market for high-performance gas engines and specialty compressors is concentrated among a few global players—Caterpillar and INNIO Waukesha supply roughly 60–70% of units for large-scale projects as of 2025—giving them strong pricing power over Enerflex’s bill of materials. Enerflex depends on these vendors for core modules of its integrated systems, so supplier lead-time shifts (often 6–18 months) directly squeeze margins and project schedules. This concentration raises switching costs: technical compatibility, recertification, and rework can add 5–12% to CAPEX and delay commissioning. Limited alternative sources mean Enerflex has weak bargaining leverage on price and delivery.

Volatility in Raw Material Costs

Enerflex faces high supplier power on steel and specialty alloys: global steel prices rose about 35% from Jan 2020 to Dec 2021 and remained volatile, with stainless steel up ~12% year-on-year in 2024, so suppliers often pass increases to manufacturers during disruptions.

Specialized Technical Labor Requirements

Enerflex’s engineering and maintenance depend on niche oilfield mechanical and digital-control skills supplied by contractors and specialist firms, giving suppliers leverage amid a chronic talent shortfall; industry data shows global energy-sector skilled labor shortages hit ~12% in 2024 and wage inflation for technical roles rose ~8–10% year-over-year, pushing project labor costs higher and compressing margins through 2025.

Limited Substitutability for High-Spec Parts

Many components in Enerflex’s custom-engineered packages are proprietary or built to tight industry specs, so generic substitutes are rarely viable; this raises supplier lock-in, especially for skid-mounted gas compression and NGL systems.

Once designs use a supplier’s tech, Enerflex stays tied to that vendor through builds and aftermarket support, strengthening suppliers’ leverage and pricing power over multi-year contracts.

In 2025 Enerflex reported supply-chain cost inflation of roughly 6–9% on key modules, a sign suppliers can transfer scarcity costs to OEMs.

- High technical specificity → low substitutability

- Design lock-in → prolonged supplier dependence

- Suppliers capture pricing power; 2025 module inflation ~6–9%

Logistical and Global Supply Chain Constraints

Suppliers of logistical services and international freight exert moderate bargaining power over Enerflex because its 2024 revenue mix included over 40% from international projects, raising reliance on cross-border heavy-lift transport.

Moving large-scale compression gear needs specialized heavy-lift carriers and permits; industry-wide port congestion in 2023–24 raised global ship turnaround times by ~12%, pushing project lead times out and costs up.

If heavy-lift shipping consolidates further—top 5 carriers handling ~60% of capacity—Enerflex faces higher freight rates and delayed deliveries for international installs.

- ~40%+ revenue from international projects

- Ship turnaround +12% (2023–24)

- Top 5 carriers ~60% capacity

- Leads to higher freight rates and longer lead times

Supplier concentration, long lead times and inflation squeeze margins

Concentrated suppliers (Caterpillar, INNIO ~60–70% of large-unit supply in 2025) and proprietary components create low substitutability, long lead times (6–18 months) and design lock‑in, enabling suppliers to pass costs (Enerflex 2025 module inflation ~6–9%) and compress margins; steel/stainless volatility (stainless +~12% YoY 2024) and skilled-labor shortages (~12% gap, wages +8–10% in 2024) add pressure.

| Metric | Value |

|---|---|

| Top suppliers share (2025) | 60–70% |

| Lead times | 6–18 months |

| Module inflation (2025) | 6–9% |

| Stainless steel YoY (2024) | +12% |

| Skilled labor gap (2024) | ~12% |

| Labor wage inflation (2024) | +8–10% |

What is included in the product

Tailored Porter's Five Forces analysis for Enerflex that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market share, with strategic commentary for investor and management use.

A concise Enerflex Porter's Five Forces snapshot—instantly highlights supplier, buyer, and competitive pressures to speed strategic decisions and simplify boardroom briefings.

Customers Bargaining Power

Concentration of Large Scale Energy Producers

Enerflex’s buyers are large E&P firms and midstream operators with deep pockets and buying clout, often consolidating orders to secure volume discounts and tighter contract terms during bids; in 2024 the top 5 customers accounted for roughly 38% of Enerflex’s revenue, so losing one major client could cut annual sales materially, often by double-digit percentages.

High Switching Costs for Integrated Systems

Once Enerflex equipment is integrated, switching costs—installation, downtime, retraining—can exceed 5–10% of a facilitys annual operating budget, creating strong customer lock-in.

Technical integration of compressors and processing modules into pipelines and control systems builds stickiness; Enerflex’s aftermarket services typically retain 70–80% of clients at contract renewal.

This dependency strengthens Enerflex’s bargaining position during renewals of long-term service and maintenance agreements, supporting recurring revenue that was 46% of 2024 sales.

Demand for Energy Transition Solutions

As of late 2025, buyers—notably oil & gas majors and utilities—demand electric-drive compression and carbon-capture-ready systems, shifting procurement toward low-emission tech; 48% of upstream capex announcements in 2024–25 cited explicit decarbonization targets. This gives customers leverage to set providers’ tech roadmaps, forcing Enerflex to boost R&D (company R&D spend rose ~22% in 2024). Customers use environmental mandates to push for higher efficiency and lower emissions at competitive pricing, increasing margin pressure.

Price Sensitivity in Cyclical Markets

Enerflex’s product demand tracks oil and gas capex, which fell ~18% globally in 2020 and rebounded unevenly through 2024; when commodity prices slide, customers sharply increase price sensitivity and defer purchases or press for lower rental rates.

This cyclicality forces Enerflex to use flexible pricing and promotional rental terms to protect rental-fleet utilization, which averaged ~72% in 2023 and dropped in past downturns.

- Demand tied to capex; capex swings drive sensitivity

- Customers defer purchases, push down rental rates

- Flexible pricing needed to sustain ~72% utilization (2023)

Focus on Lifecycle Costs and Reliability

Customers value total cost of ownership—maintenance, uptime, and lifecycle costs—over initial price; 2024 industry data shows buyers pay 25–35% more for units with 98%+ uptime guarantees.

Enerflex can command premium margins by offering high-quality aftermarket support and remote monitoring, which reduced service-related downtime by ~18% in comparable deployments.

Large customers with strong in-house maintenance teams use that capability to push down service scope and pricing, cutting third-party service spend by up to 20%.

- Customers prioritize TCO (25–35% premium for high uptime)

- Enerflex differentiation: aftermarket + remote monitoring (−18% downtime)

- In-house maintenance can trim service spend ~20%

Consolidated buyers squeeze margins despite strong aftermarket retention—decarbonization bites

Buyers (top 5 ≈38% revenue in 2024) wield strong leverage via consolidated orders, tech mandates, and price sensitivity tied to capex cycles; switching costs (5–10% of annual ops budget) and 70–80% aftermarket retention limit churn, but decarbonization demands (48% of 2024–25 capex announcements) and in-house maintenance (cut service spend ~20%) pressure margins.

| Metric | 2024/25 |

|---|---|

| Top‑5 customers | 38% rev |

| Aftermarket retention | 70–80% |

| Rental utilization | ~72% (2023) |

| Decarb capex cites | 48% |

What You See Is What You Get

Enerflex Porter's Five Forces Analysis

This preview shows the exact Enerflex Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or mockups.

You're viewing the final deliverable; once you complete your purchase you'll get instant access to this same comprehensive document for download and application.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Enerflex faces moderate supplier power and fluctuating buyer demand driven by energy capex cycles, while the threat of new entrants is limited by high technical barriers and capital intensity.

Substitute threats remain low, but rivalry is elevated due to a concentrated field of global service providers competing on price and integrated solutions.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Enerflex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Critical Component Manufacturers

The market for high-performance gas engines and specialty compressors is concentrated among a few global players—Caterpillar and INNIO Waukesha supply roughly 60–70% of units for large-scale projects as of 2025—giving them strong pricing power over Enerflex’s bill of materials. Enerflex depends on these vendors for core modules of its integrated systems, so supplier lead-time shifts (often 6–18 months) directly squeeze margins and project schedules. This concentration raises switching costs: technical compatibility, recertification, and rework can add 5–12% to CAPEX and delay commissioning. Limited alternative sources mean Enerflex has weak bargaining leverage on price and delivery.

Volatility in Raw Material Costs

Enerflex faces high supplier power on steel and specialty alloys: global steel prices rose about 35% from Jan 2020 to Dec 2021 and remained volatile, with stainless steel up ~12% year-on-year in 2024, so suppliers often pass increases to manufacturers during disruptions.

Specialized Technical Labor Requirements

Enerflex’s engineering and maintenance depend on niche oilfield mechanical and digital-control skills supplied by contractors and specialist firms, giving suppliers leverage amid a chronic talent shortfall; industry data shows global energy-sector skilled labor shortages hit ~12% in 2024 and wage inflation for technical roles rose ~8–10% year-over-year, pushing project labor costs higher and compressing margins through 2025.

Limited Substitutability for High-Spec Parts

Many components in Enerflex’s custom-engineered packages are proprietary or built to tight industry specs, so generic substitutes are rarely viable; this raises supplier lock-in, especially for skid-mounted gas compression and NGL systems.

Once designs use a supplier’s tech, Enerflex stays tied to that vendor through builds and aftermarket support, strengthening suppliers’ leverage and pricing power over multi-year contracts.

In 2025 Enerflex reported supply-chain cost inflation of roughly 6–9% on key modules, a sign suppliers can transfer scarcity costs to OEMs.

- High technical specificity → low substitutability

- Design lock-in → prolonged supplier dependence

- Suppliers capture pricing power; 2025 module inflation ~6–9%

Logistical and Global Supply Chain Constraints

Suppliers of logistical services and international freight exert moderate bargaining power over Enerflex because its 2024 revenue mix included over 40% from international projects, raising reliance on cross-border heavy-lift transport.

Moving large-scale compression gear needs specialized heavy-lift carriers and permits; industry-wide port congestion in 2023–24 raised global ship turnaround times by ~12%, pushing project lead times out and costs up.

If heavy-lift shipping consolidates further—top 5 carriers handling ~60% of capacity—Enerflex faces higher freight rates and delayed deliveries for international installs.

- ~40%+ revenue from international projects

- Ship turnaround +12% (2023–24)

- Top 5 carriers ~60% capacity

- Leads to higher freight rates and longer lead times

Supplier concentration, long lead times and inflation squeeze margins

Concentrated suppliers (Caterpillar, INNIO ~60–70% of large-unit supply in 2025) and proprietary components create low substitutability, long lead times (6–18 months) and design lock‑in, enabling suppliers to pass costs (Enerflex 2025 module inflation ~6–9%) and compress margins; steel/stainless volatility (stainless +~12% YoY 2024) and skilled-labor shortages (~12% gap, wages +8–10% in 2024) add pressure.

| Metric | Value |

|---|---|

| Top suppliers share (2025) | 60–70% |

| Lead times | 6–18 months |

| Module inflation (2025) | 6–9% |

| Stainless steel YoY (2024) | +12% |

| Skilled labor gap (2024) | ~12% |

| Labor wage inflation (2024) | +8–10% |

What is included in the product

Tailored Porter's Five Forces analysis for Enerflex that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats to its market share, with strategic commentary for investor and management use.

A concise Enerflex Porter's Five Forces snapshot—instantly highlights supplier, buyer, and competitive pressures to speed strategic decisions and simplify boardroom briefings.

Customers Bargaining Power

Concentration of Large Scale Energy Producers

Enerflex’s buyers are large E&P firms and midstream operators with deep pockets and buying clout, often consolidating orders to secure volume discounts and tighter contract terms during bids; in 2024 the top 5 customers accounted for roughly 38% of Enerflex’s revenue, so losing one major client could cut annual sales materially, often by double-digit percentages.

High Switching Costs for Integrated Systems

Once Enerflex equipment is integrated, switching costs—installation, downtime, retraining—can exceed 5–10% of a facilitys annual operating budget, creating strong customer lock-in.

Technical integration of compressors and processing modules into pipelines and control systems builds stickiness; Enerflex’s aftermarket services typically retain 70–80% of clients at contract renewal.

This dependency strengthens Enerflex’s bargaining position during renewals of long-term service and maintenance agreements, supporting recurring revenue that was 46% of 2024 sales.

Demand for Energy Transition Solutions

As of late 2025, buyers—notably oil & gas majors and utilities—demand electric-drive compression and carbon-capture-ready systems, shifting procurement toward low-emission tech; 48% of upstream capex announcements in 2024–25 cited explicit decarbonization targets. This gives customers leverage to set providers’ tech roadmaps, forcing Enerflex to boost R&D (company R&D spend rose ~22% in 2024). Customers use environmental mandates to push for higher efficiency and lower emissions at competitive pricing, increasing margin pressure.

Price Sensitivity in Cyclical Markets

Enerflex’s product demand tracks oil and gas capex, which fell ~18% globally in 2020 and rebounded unevenly through 2024; when commodity prices slide, customers sharply increase price sensitivity and defer purchases or press for lower rental rates.

This cyclicality forces Enerflex to use flexible pricing and promotional rental terms to protect rental-fleet utilization, which averaged ~72% in 2023 and dropped in past downturns.

- Demand tied to capex; capex swings drive sensitivity

- Customers defer purchases, push down rental rates

- Flexible pricing needed to sustain ~72% utilization (2023)

Focus on Lifecycle Costs and Reliability

Customers value total cost of ownership—maintenance, uptime, and lifecycle costs—over initial price; 2024 industry data shows buyers pay 25–35% more for units with 98%+ uptime guarantees.

Enerflex can command premium margins by offering high-quality aftermarket support and remote monitoring, which reduced service-related downtime by ~18% in comparable deployments.

Large customers with strong in-house maintenance teams use that capability to push down service scope and pricing, cutting third-party service spend by up to 20%.

- Customers prioritize TCO (25–35% premium for high uptime)

- Enerflex differentiation: aftermarket + remote monitoring (−18% downtime)

- In-house maintenance can trim service spend ~20%

Consolidated buyers squeeze margins despite strong aftermarket retention—decarbonization bites

Buyers (top 5 ≈38% revenue in 2024) wield strong leverage via consolidated orders, tech mandates, and price sensitivity tied to capex cycles; switching costs (5–10% of annual ops budget) and 70–80% aftermarket retention limit churn, but decarbonization demands (48% of 2024–25 capex announcements) and in-house maintenance (cut service spend ~20%) pressure margins.

| Metric | 2024/25 |

|---|---|

| Top‑5 customers | 38% rev |

| Aftermarket retention | 70–80% |

| Rental utilization | ~72% (2023) |

| Decarb capex cites | 48% |

What You See Is What You Get

Enerflex Porter's Five Forces Analysis

This preview shows the exact Enerflex Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for use with no placeholders or mockups.

You're viewing the final deliverable; once you complete your purchase you'll get instant access to this same comprehensive document for download and application.