Energizer Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Energizer operates in a mature, low-growth market where strong retailer relationships and brand equity mitigate supplier and buyer pressures, but commoditization and private-label players heighten rivalry and substitute threats; regulatory and input-cost volatility add strategic risk. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Energizer’s competitive dynamics, market pressures, and strategic advantages in detail.

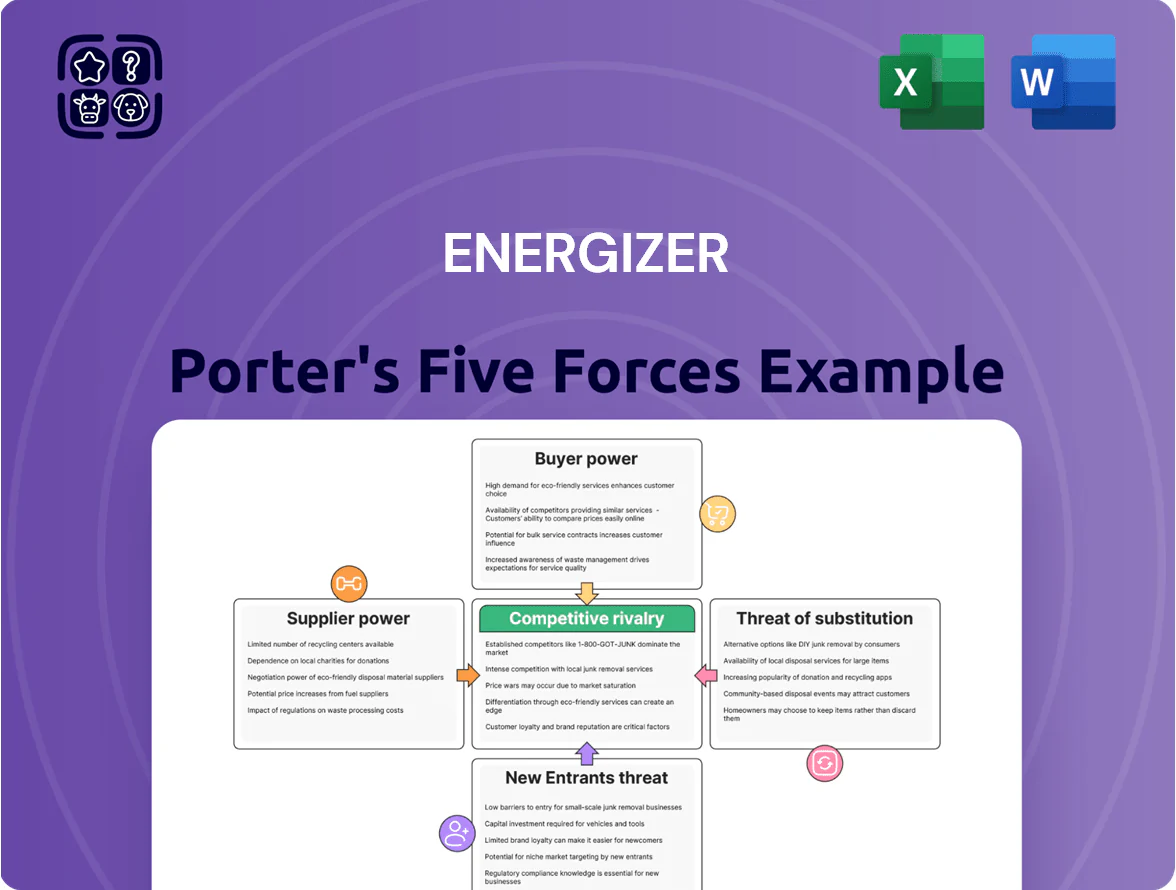

Suppliers Bargaining Power

Commodity Price Volatility

Commodity price swings for lithium, zinc, and manganese drove Energizer's input cost volatility; lithium spot prices rose ~60% in 2023 and zinc averaged $2,850/ton in 2024, pushing battery production costs up materially.

Energizer needs specific chemical grades, narrowing global suppliers to a handful; limited sources give suppliers leverage to raise prices when demand spikes.

During 2022–24 geopolitical disruptions, supplier price hikes and tight capacity increased Energizer's COGS by an estimated mid-single-digit percentage points, squeezing margins.

Specialized Chemical Components

Specialized chemical inputs for lithium-based cells—lithium, cobalt, nickel—are concentrated: the top three lithium producers (Australia, Chile, China-linked firms) supplied ~75% of refined lithium in 2024, giving suppliers strong leverage over pricing and availability.

As battery demand rose 28% in 2023–24, Energizer faces competition for high-grade feedstock; long-term offtake contracts and spot hedges are necessary to secure inputs for premium lines and protect margins.

Limited Supplier Diversity

For certain proprietary components in auto care and lighting, only a handful of qualified manufacturers exist worldwide; supplier concentration is high—estimated that top 3 suppliers control ~65% of specialized LED and sensor part capacity in 2024—raising bottleneck risk if a major vendor has outages.

Energizer balances switching costs against delay risk: in 2024 the company reported $2.1 billion revenue in lighting/auto segments and noted supply-chain contingency spending rose ~12% YoY to secure dual sourcing and buffer inventory.

Energy and Logistics Costs

- OECD industrial power +18% (2022–24)

- US industrial electricity +12% (2021–24)

- Fuel-driven transport costs hike supplier pricing power

- Energy pass-throughs limit Energizer's bargaining leverage

Impact of Trade Regulations

Trade barriers and tariffs since 2021 raised costs for imported zinc and lithium, boosting local US and EU suppliers; Energizer reported 12% higher procurement spend in 2023 vs 2020, narrowing its vendor base.

Shifts in US-China relations and 2022 US Inflation Reduction Act incentives pushed Energizer to favor domestic or preferred-nation vendors, reducing supplier competition and strengthening supplier bargaining power regionally.

- Tariff-driven procurement cost +12% (2020–2023)

- Domestic sourcing share rose—company filings show ~18% point increase

- Smaller vendor pool → higher supplier leverage

High supplier power drives +12% procurement, domestic sourcing shift and rising COGS

Supplier power is high: concentrated sources for lithium/zinc/manganese and proprietary parts, tariff-driven domestic sourcing (+18 ppt share) and higher energy/logistics costs (OECD industrial power +18% 2022–24) pushed Energizer procurement +12% (2020–23) and COGS up mid-single-digits (2022–24), forcing longer offtake contracts and dual sourcing.

| Metric | Value |

|---|---|

| Procurement spend change (2020–23) | +12% |

| Domestic sourcing shift | +18 ppt |

| OECD industrial power (2022–24) | +18% |

| COGS impact (2022–24) | Mid-single-digit ppt |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Energizer, detailing each Porter's force with industry insights, supplier/buyer power, substitutes, new entrant barriers, and disruptive threats to inform strategic decisions.

Concise Energizer Porter's Five Forces summary that highlights battery market rivalries and supplier risks—perfect for quick strategic decisions and slide-ready decks.

Customers Bargaining Power

Retailer Concentration

Major big-box retailers like Walmart and Target together accounted for roughly 22% of Energizer Holdings’ net sales in 2024, giving them strong leverage to demand lower wholesale prices and premium shelf placement.

The retailers’ ability to switch to private labels—US private-label battery penetration rose to ~18% in 2024—means Energizer faces pricing pressure and must offer trade promotions and slotting fees to retain space.

Growth of Private Labels

Retailers like Amazon (AmazonBasics) and Costco (Kirkland Signature) expanded private-label batteries to ~15–20% category share in US value channels by 2024, undercutting Energizer on price by 20–40%. This raises customer switching: Nielsen found 35% of buyers choose store brands when price gaps exceed 25%. Energizer must therefore show clear tech advantages (longer life, leak-proof cells) and invest in branding to defend its ~30% branded market share.

Low Switching Costs for Consumers

Individual consumers face almost zero switching cost at checkout, so Energizer loses little if shoppers pick Duracell or private-label batteries; NielsenIQ reported private-label share rose to 18% in AA/AAA batteries in the US in 2024. Brand loyalty yields to availability and promos, with 42% of buyers citing price or promotion as the purchase trigger in a 2023 Kantar survey. That forces Energizer to sustain high marketing and trade spend—about $120m in advertising and promotion in 2024—to stay top-of-mind.

E-commerce Price Transparency

- Global e-commerce: 5.7T USD (2022), ~4% CAGR to 2025

- Amazon/Walmart ≈60% US online share

- Algorithms favor lowest per-unit pricing

- Both consumers and small industrial buyers gain leverage

Bulk Purchasing Power

Industrial and commercial buyers who purchase batteries and auto-care products in bulk can secure double-digit volume discounts, forcing Energizer Holdings Inc. (ENR) to match lower tender prices to retain contracts.

Large tenders drive aggressive price competition among major manufacturers; losing one national account can shave several percentage points off quarterly revenue—ENR reported $1.14B revenue in Q3 2025, so a 3% contract loss equals ~$34M.

High buyer concentration raises bargaining power, compressing gross margins (ENR GAAP gross margin was ~34% in 2025) and increasing short-term cash flow volatility.

- Volume discounts: often 10%–20%

- Tenders force price matching

- Single large contract ≈ $30M–$40M impact

- Margin pressure: ~34% gross margin in 2025

Retail giants, private labels squeeze margins—price gaps shift 35% of shoppers

Buyers—especially Walmart/Target (~22% of ENR 2024 sales) and Amazon/Costco private labels (~15–20% share)—wield strong price and placement leverage, forcing trade promos and slotting fees; retail/private-label price gaps of 20–40% shift ~35% of shoppers to cheaper options. Large industrial tenders get 10%–20% discounts and can swing ~$30–40M revenue; ENR gross margin ~34% (2025), ad/trade spend ~$120M (2024).

| Metric | Value |

|---|---|

| Walmart/Target share | ~22% (2024) |

| Private-label US AA/AAA | ~18% (2024) |

| Price gap vs private-label | 20–40% |

| ENR gross margin | ~34% (2025) |

| Ad & trade spend | ~$120M (2024) |

| Large contract impact | $30–40M |

Same Document Delivered

Energizer Porter's Five Forces Analysis

This preview shows the exact Energizer Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Energizer operates in a mature, low-growth market where strong retailer relationships and brand equity mitigate supplier and buyer pressures, but commoditization and private-label players heighten rivalry and substitute threats; regulatory and input-cost volatility add strategic risk. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Energizer’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commodity Price Volatility

Commodity price swings for lithium, zinc, and manganese drove Energizer's input cost volatility; lithium spot prices rose ~60% in 2023 and zinc averaged $2,850/ton in 2024, pushing battery production costs up materially.

Energizer needs specific chemical grades, narrowing global suppliers to a handful; limited sources give suppliers leverage to raise prices when demand spikes.

During 2022–24 geopolitical disruptions, supplier price hikes and tight capacity increased Energizer's COGS by an estimated mid-single-digit percentage points, squeezing margins.

Specialized Chemical Components

Specialized chemical inputs for lithium-based cells—lithium, cobalt, nickel—are concentrated: the top three lithium producers (Australia, Chile, China-linked firms) supplied ~75% of refined lithium in 2024, giving suppliers strong leverage over pricing and availability.

As battery demand rose 28% in 2023–24, Energizer faces competition for high-grade feedstock; long-term offtake contracts and spot hedges are necessary to secure inputs for premium lines and protect margins.

Limited Supplier Diversity

For certain proprietary components in auto care and lighting, only a handful of qualified manufacturers exist worldwide; supplier concentration is high—estimated that top 3 suppliers control ~65% of specialized LED and sensor part capacity in 2024—raising bottleneck risk if a major vendor has outages.

Energizer balances switching costs against delay risk: in 2024 the company reported $2.1 billion revenue in lighting/auto segments and noted supply-chain contingency spending rose ~12% YoY to secure dual sourcing and buffer inventory.

Energy and Logistics Costs

- OECD industrial power +18% (2022–24)

- US industrial electricity +12% (2021–24)

- Fuel-driven transport costs hike supplier pricing power

- Energy pass-throughs limit Energizer's bargaining leverage

Impact of Trade Regulations

Trade barriers and tariffs since 2021 raised costs for imported zinc and lithium, boosting local US and EU suppliers; Energizer reported 12% higher procurement spend in 2023 vs 2020, narrowing its vendor base.

Shifts in US-China relations and 2022 US Inflation Reduction Act incentives pushed Energizer to favor domestic or preferred-nation vendors, reducing supplier competition and strengthening supplier bargaining power regionally.

- Tariff-driven procurement cost +12% (2020–2023)

- Domestic sourcing share rose—company filings show ~18% point increase

- Smaller vendor pool → higher supplier leverage

High supplier power drives +12% procurement, domestic sourcing shift and rising COGS

Supplier power is high: concentrated sources for lithium/zinc/manganese and proprietary parts, tariff-driven domestic sourcing (+18 ppt share) and higher energy/logistics costs (OECD industrial power +18% 2022–24) pushed Energizer procurement +12% (2020–23) and COGS up mid-single-digits (2022–24), forcing longer offtake contracts and dual sourcing.

| Metric | Value |

|---|---|

| Procurement spend change (2020–23) | +12% |

| Domestic sourcing shift | +18 ppt |

| OECD industrial power (2022–24) | +18% |

| COGS impact (2022–24) | Mid-single-digit ppt |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Energizer, detailing each Porter's force with industry insights, supplier/buyer power, substitutes, new entrant barriers, and disruptive threats to inform strategic decisions.

Concise Energizer Porter's Five Forces summary that highlights battery market rivalries and supplier risks—perfect for quick strategic decisions and slide-ready decks.

Customers Bargaining Power

Retailer Concentration

Major big-box retailers like Walmart and Target together accounted for roughly 22% of Energizer Holdings’ net sales in 2024, giving them strong leverage to demand lower wholesale prices and premium shelf placement.

The retailers’ ability to switch to private labels—US private-label battery penetration rose to ~18% in 2024—means Energizer faces pricing pressure and must offer trade promotions and slotting fees to retain space.

Growth of Private Labels

Retailers like Amazon (AmazonBasics) and Costco (Kirkland Signature) expanded private-label batteries to ~15–20% category share in US value channels by 2024, undercutting Energizer on price by 20–40%. This raises customer switching: Nielsen found 35% of buyers choose store brands when price gaps exceed 25%. Energizer must therefore show clear tech advantages (longer life, leak-proof cells) and invest in branding to defend its ~30% branded market share.

Low Switching Costs for Consumers

Individual consumers face almost zero switching cost at checkout, so Energizer loses little if shoppers pick Duracell or private-label batteries; NielsenIQ reported private-label share rose to 18% in AA/AAA batteries in the US in 2024. Brand loyalty yields to availability and promos, with 42% of buyers citing price or promotion as the purchase trigger in a 2023 Kantar survey. That forces Energizer to sustain high marketing and trade spend—about $120m in advertising and promotion in 2024—to stay top-of-mind.

E-commerce Price Transparency

- Global e-commerce: 5.7T USD (2022), ~4% CAGR to 2025

- Amazon/Walmart ≈60% US online share

- Algorithms favor lowest per-unit pricing

- Both consumers and small industrial buyers gain leverage

Bulk Purchasing Power

Industrial and commercial buyers who purchase batteries and auto-care products in bulk can secure double-digit volume discounts, forcing Energizer Holdings Inc. (ENR) to match lower tender prices to retain contracts.

Large tenders drive aggressive price competition among major manufacturers; losing one national account can shave several percentage points off quarterly revenue—ENR reported $1.14B revenue in Q3 2025, so a 3% contract loss equals ~$34M.

High buyer concentration raises bargaining power, compressing gross margins (ENR GAAP gross margin was ~34% in 2025) and increasing short-term cash flow volatility.

- Volume discounts: often 10%–20%

- Tenders force price matching

- Single large contract ≈ $30M–$40M impact

- Margin pressure: ~34% gross margin in 2025

Retail giants, private labels squeeze margins—price gaps shift 35% of shoppers

Buyers—especially Walmart/Target (~22% of ENR 2024 sales) and Amazon/Costco private labels (~15–20% share)—wield strong price and placement leverage, forcing trade promos and slotting fees; retail/private-label price gaps of 20–40% shift ~35% of shoppers to cheaper options. Large industrial tenders get 10%–20% discounts and can swing ~$30–40M revenue; ENR gross margin ~34% (2025), ad/trade spend ~$120M (2024).

| Metric | Value |

|---|---|

| Walmart/Target share | ~22% (2024) |

| Private-label US AA/AAA | ~18% (2024) |

| Price gap vs private-label | 20–40% |

| ENR gross margin | ~34% (2025) |

| Ad & trade spend | ~$120M (2024) |

| Large contract impact | $30–40M |

Same Document Delivered

Energizer Porter's Five Forces Analysis

This preview shows the exact Energizer Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.