Ennostar Porter's Five Forces Analysis

From Overview to Strategy Blueprint

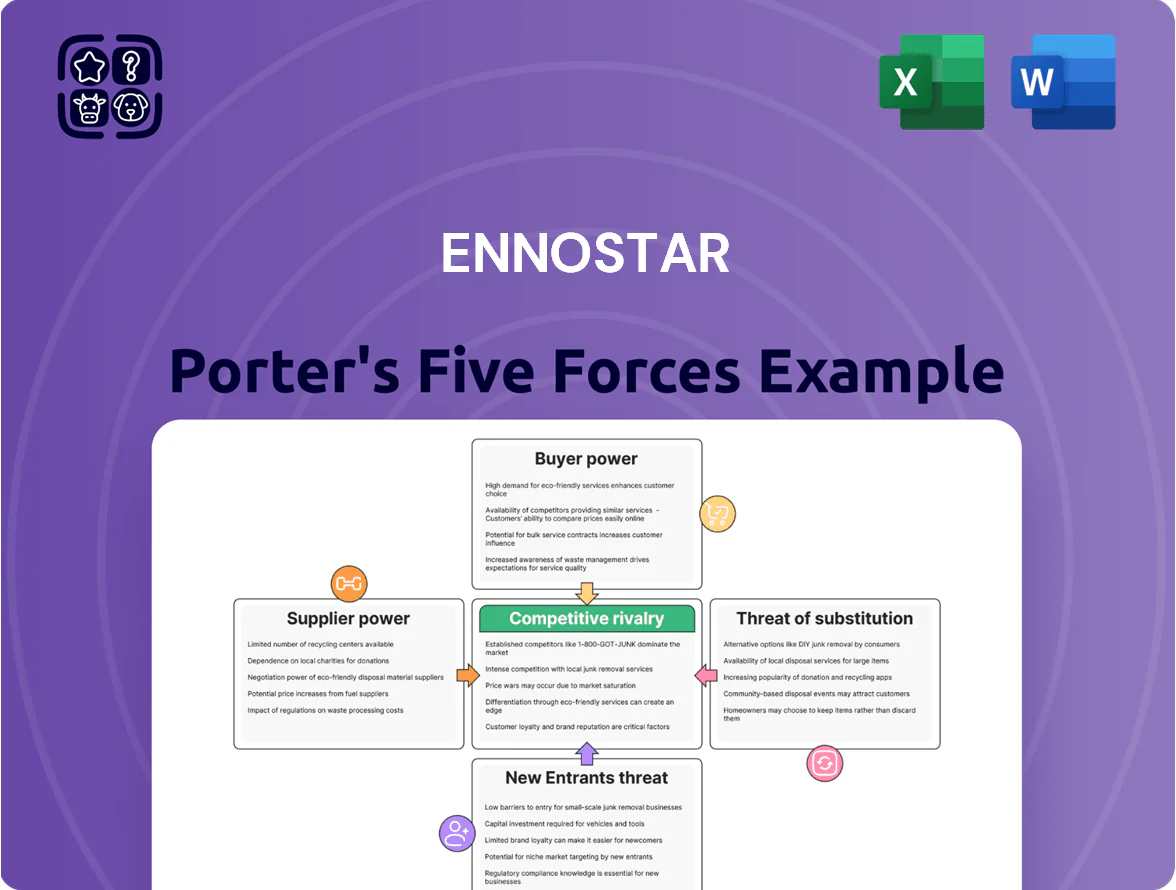

Ennostar faces moderate supplier power and intensified rivalry as niche tech incumbents vie for scale, while buyer sophistication and potential substitutes pressure margins—regulatory shifts and capital requirements add asymmetric threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ennostar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of MOCVD equipment providers

The market for MOCVD (metal-organic chemical vapor deposition) tools is highly concentrated: Aixtron and Veeco held about 70% of global market share for LED/MicroLED MOCVD systems in 2024, giving them pricing and delivery power over Ennostar.

These machines cost $5–30 million each and lead times often exceed 12–18 months, so supplier schedules directly cap Ennostar’s output and timing for next‑gen displays.

Volatility in specialty chemical and gas pricing

Manufacturing compound semiconductors needs high-purity gases and specialty chemicals—ammonia and metal-organic precursors—that saw spot-price spikes of 20–45% in 2023–2024 after supply disruptions and 2024 China export controls on key precursors.

Global supply-chain volatility and geopolitical tensions drove lead times up 30% and raised input-cost volatility, contributing 6–12% margin pressure for comparable fabs in 2024.

Ennostar cannot quickly switch suppliers because ultra-high purity specs lower vendor options to a few qualified global firms, so sudden cost increases translate rapidly into higher production costs and yield risk.

Dependence on sapphire and silicon substrate vendors

Substrates (sapphire and silicon wafers) are the foundation of Ennostar’s LED chips, and wafer quality directly affects MicroLED yield and brightness; high-spec wafers for MicroLED cut the qualified supplier pool to roughly 5–7 global players as of 2025, tightening supplier power. A single-week supply disruption can raise per-unit costs by an estimated 3–6% due to halted fabs and overtime; long lead times (12–20 weeks) further amplify leverage for suppliers.

Energy intensity and utility costs

Ennostar's LED and fab processes consume large power; fabs can use 100–200 MW each, so electricity makes up 10–20% of COGS for advanced nodes.

In operating regions where single utility providers prevail, Ennostar has near-zero leverage on rates, exposing margins to tariff hikes and outages.

Higher energy prices and carbon taxes (example: EU ETS €80/ton in 2025) raise per-unit costs materially for high-intensity manufacturing.

- Fabs: 100–200 MW demand

- Electricity = ~10–20% of COGS

- Monopoly utilities → no bargaining power

- EU ETS €80/ton (2025) increases costs

Intellectual property licensing for materials

Ennostar faces supplier power from chemical firms holding patents on advanced LED and power-management materials, forcing licensing fees or tied purchasing; industry reports show specialty precursor royalties can reach 2–5% of bill-of-materials, raising COGS and R&D allocations.

This dependence increases long-term R&D cost volatility—if license renewals rise 10–20% over five years, product margins could compress materially and slow new-node development.

- Patented precursors: common

- Licensing fees: ~2–5% BOM

- Renewal risk: +10–20% over 5 yrs

- Impact: higher COGS, constrained R&D

Supply bottlenecks: MOCVD dominance, soaring inputs & wafer/electricity cost risks

Suppliers exert strong power: Aixtron+Veeco ≈70% MOCVD share (2024), machines $5–30M, lead times 12–18+ months; specialty gases/precursors spiked 20–45% (2023–24); wafers limited to 5–7 qualified suppliers (2025), 12–20 week lead times; electricity 10–20% COGS (fabs 100–200 MW); patent/licensing fees ~2–5% BOM, renewal risk +10–20% over 5 yrs.

| Item | Metric |

|---|---|

| MOCVD share | 70% (2024) |

| Machine cost | $5–30M |

| Gas price spikes | 20–45% (2023–24) |

| Wafer suppliers | 5–7 (2025) |

| Electricity | 10–20% COGS |

| Licensing fees | 2–5% BOM |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, and substitution risks specific to Ennostar, highlighting disruptive threats, pricing pressure, and strategic defenses to protect market share.

Ennostar Porter's Five Forces distilled into a one-sheet—quickly gauge competitive pressures and prioritize strategic moves to relieve decision-making friction.

Customers Bargaining Power

Concentration of consumer electronics giants

Ennostar derives over 70% of revenue from a handful of tier-one clients in smartphones, tablets and TVs, giving these brands strong bargaining leverage through massive order volumes and frequent requests for double-digit price cuts; in 2024 top-3 customers accounted for 58% of sales. The scale of orders lets buyers push margins down and demand tighter payment terms. Losing one tier-one client could cut factory utilization by 20–35% and erase a similar share of operating profit.

Standardization and price sensitivity in commodity LEDs

In traditional lighting and backlighting, LEDs are commoditized: unit price for standard SMD LEDs fell ~18% YoY in 2024, pushing gross margins below 12% for commodity SKUs. Buyers switch suppliers for a few cents per piece, so Ennostar faces tight pricing and must prioritize volume and cost cuts. This gives customers high bargaining power, as they favor lowest-cost bids over brand features, squeezing Ennostar’s negotiating leverage.

High switching costs for automotive and industrial clients

High switching costs in automotive and industrial sensing mean long qualification cycles—often 12–36 months—so once Ennostar components are designed into lighting or ADAS (advanced driver-assistance systems), customers rarely switch; industry data shows design win retention rates above 80% for Tier‑1 suppliers, letting Ennostar secure multi-year supply contracts and sustain pricing, supporting revenue visibility (Ennostar-like peers report 60–70% of revenue from long-term automotive programs).

Vertical integration trends among tech leaders

- Customers building chips in-house: Apple, Samsung, Google

- Apple MicroLED R&D ~$1.5B (2024)

- Samsung foundry cap +12% (2025)

- Revenue at risk if 10–20% insourcing

Demand for rapid technological evolution

- R&D spend: ~8–12% revenue (2024)

- OEM spec push: 5–10% yearly efficiency gains

- HDR/luminance target: 1,000+ nits

- Cost risk: capex and yield ramp exposure

Concentrated buyers, plunging SMD margins, and 10–20% insourcing revenue risk

Buyers hold strong leverage: top‑3 customers = 58% sales (2024) and >70% revenue from tier‑one clients, enabling double‑digit price cuts and tighter terms; commodity SMD LED prices fell ~18% YoY (2024) pushing commodity gross margins <12%; automotive/industrial design wins lock 60–80% revenue but take 12–36 months to qualify; Apple MicroLED R&D ~$1.5B (2024) and Samsung foundry +12% cap (2025) raise insourcing risk (10–20% revenue at risk).

| Metric | Value |

|---|---|

| Top‑3 customers (2024) | 58% sales |

| Tier‑one client revenue | >70% |

| SMD LED price change (2024) | −18% YoY |

| Commodity gross margin | <12% |

| Design win retention | 60–80% |

| Qualif. cycle | 12–36 months |

| Apple MicroLED R&D (2024) | $1.5B |

| Samsung foundry cap (2025) | +12% |

| Revenue at risk (insourcing) | 10–20% |

Preview Before You Purchase

Ennostar Porter's Five Forces Analysis

This preview shows the exact Ennostar Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the fully formatted, final version of the analysis, ready for instant download and use the moment you buy.

You're viewing the actual deliverable: a complete, professionally written Porter’s Five Forces report on Ennostar, identical to the file you’ll get after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Ennostar faces moderate supplier power and intensified rivalry as niche tech incumbents vie for scale, while buyer sophistication and potential substitutes pressure margins—regulatory shifts and capital requirements add asymmetric threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ennostar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of MOCVD equipment providers

The market for MOCVD (metal-organic chemical vapor deposition) tools is highly concentrated: Aixtron and Veeco held about 70% of global market share for LED/MicroLED MOCVD systems in 2024, giving them pricing and delivery power over Ennostar.

These machines cost $5–30 million each and lead times often exceed 12–18 months, so supplier schedules directly cap Ennostar’s output and timing for next‑gen displays.

Volatility in specialty chemical and gas pricing

Manufacturing compound semiconductors needs high-purity gases and specialty chemicals—ammonia and metal-organic precursors—that saw spot-price spikes of 20–45% in 2023–2024 after supply disruptions and 2024 China export controls on key precursors.

Global supply-chain volatility and geopolitical tensions drove lead times up 30% and raised input-cost volatility, contributing 6–12% margin pressure for comparable fabs in 2024.

Ennostar cannot quickly switch suppliers because ultra-high purity specs lower vendor options to a few qualified global firms, so sudden cost increases translate rapidly into higher production costs and yield risk.

Dependence on sapphire and silicon substrate vendors

Substrates (sapphire and silicon wafers) are the foundation of Ennostar’s LED chips, and wafer quality directly affects MicroLED yield and brightness; high-spec wafers for MicroLED cut the qualified supplier pool to roughly 5–7 global players as of 2025, tightening supplier power. A single-week supply disruption can raise per-unit costs by an estimated 3–6% due to halted fabs and overtime; long lead times (12–20 weeks) further amplify leverage for suppliers.

Energy intensity and utility costs

Ennostar's LED and fab processes consume large power; fabs can use 100–200 MW each, so electricity makes up 10–20% of COGS for advanced nodes.

In operating regions where single utility providers prevail, Ennostar has near-zero leverage on rates, exposing margins to tariff hikes and outages.

Higher energy prices and carbon taxes (example: EU ETS €80/ton in 2025) raise per-unit costs materially for high-intensity manufacturing.

- Fabs: 100–200 MW demand

- Electricity = ~10–20% of COGS

- Monopoly utilities → no bargaining power

- EU ETS €80/ton (2025) increases costs

Intellectual property licensing for materials

Ennostar faces supplier power from chemical firms holding patents on advanced LED and power-management materials, forcing licensing fees or tied purchasing; industry reports show specialty precursor royalties can reach 2–5% of bill-of-materials, raising COGS and R&D allocations.

This dependence increases long-term R&D cost volatility—if license renewals rise 10–20% over five years, product margins could compress materially and slow new-node development.

- Patented precursors: common

- Licensing fees: ~2–5% BOM

- Renewal risk: +10–20% over 5 yrs

- Impact: higher COGS, constrained R&D

Supply bottlenecks: MOCVD dominance, soaring inputs & wafer/electricity cost risks

Suppliers exert strong power: Aixtron+Veeco ≈70% MOCVD share (2024), machines $5–30M, lead times 12–18+ months; specialty gases/precursors spiked 20–45% (2023–24); wafers limited to 5–7 qualified suppliers (2025), 12–20 week lead times; electricity 10–20% COGS (fabs 100–200 MW); patent/licensing fees ~2–5% BOM, renewal risk +10–20% over 5 yrs.

| Item | Metric |

|---|---|

| MOCVD share | 70% (2024) |

| Machine cost | $5–30M |

| Gas price spikes | 20–45% (2023–24) |

| Wafer suppliers | 5–7 (2025) |

| Electricity | 10–20% COGS |

| Licensing fees | 2–5% BOM |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry barriers, and substitution risks specific to Ennostar, highlighting disruptive threats, pricing pressure, and strategic defenses to protect market share.

Ennostar Porter's Five Forces distilled into a one-sheet—quickly gauge competitive pressures and prioritize strategic moves to relieve decision-making friction.

Customers Bargaining Power

Concentration of consumer electronics giants

Ennostar derives over 70% of revenue from a handful of tier-one clients in smartphones, tablets and TVs, giving these brands strong bargaining leverage through massive order volumes and frequent requests for double-digit price cuts; in 2024 top-3 customers accounted for 58% of sales. The scale of orders lets buyers push margins down and demand tighter payment terms. Losing one tier-one client could cut factory utilization by 20–35% and erase a similar share of operating profit.

Standardization and price sensitivity in commodity LEDs

In traditional lighting and backlighting, LEDs are commoditized: unit price for standard SMD LEDs fell ~18% YoY in 2024, pushing gross margins below 12% for commodity SKUs. Buyers switch suppliers for a few cents per piece, so Ennostar faces tight pricing and must prioritize volume and cost cuts. This gives customers high bargaining power, as they favor lowest-cost bids over brand features, squeezing Ennostar’s negotiating leverage.

High switching costs for automotive and industrial clients

High switching costs in automotive and industrial sensing mean long qualification cycles—often 12–36 months—so once Ennostar components are designed into lighting or ADAS (advanced driver-assistance systems), customers rarely switch; industry data shows design win retention rates above 80% for Tier‑1 suppliers, letting Ennostar secure multi-year supply contracts and sustain pricing, supporting revenue visibility (Ennostar-like peers report 60–70% of revenue from long-term automotive programs).

Vertical integration trends among tech leaders

- Customers building chips in-house: Apple, Samsung, Google

- Apple MicroLED R&D ~$1.5B (2024)

- Samsung foundry cap +12% (2025)

- Revenue at risk if 10–20% insourcing

Demand for rapid technological evolution

- R&D spend: ~8–12% revenue (2024)

- OEM spec push: 5–10% yearly efficiency gains

- HDR/luminance target: 1,000+ nits

- Cost risk: capex and yield ramp exposure

Concentrated buyers, plunging SMD margins, and 10–20% insourcing revenue risk

Buyers hold strong leverage: top‑3 customers = 58% sales (2024) and >70% revenue from tier‑one clients, enabling double‑digit price cuts and tighter terms; commodity SMD LED prices fell ~18% YoY (2024) pushing commodity gross margins <12%; automotive/industrial design wins lock 60–80% revenue but take 12–36 months to qualify; Apple MicroLED R&D ~$1.5B (2024) and Samsung foundry +12% cap (2025) raise insourcing risk (10–20% revenue at risk).

| Metric | Value |

|---|---|

| Top‑3 customers (2024) | 58% sales |

| Tier‑one client revenue | >70% |

| SMD LED price change (2024) | −18% YoY |

| Commodity gross margin | <12% |

| Design win retention | 60–80% |

| Qualif. cycle | 12–36 months |

| Apple MicroLED R&D (2024) | $1.5B |

| Samsung foundry cap (2025) | +12% |

| Revenue at risk (insourcing) | 10–20% |

Preview Before You Purchase

Ennostar Porter's Five Forces Analysis

This preview shows the exact Ennostar Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the fully formatted, final version of the analysis, ready for instant download and use the moment you buy.

You're viewing the actual deliverable: a complete, professionally written Porter’s Five Forces report on Ennostar, identical to the file you’ll get after payment.