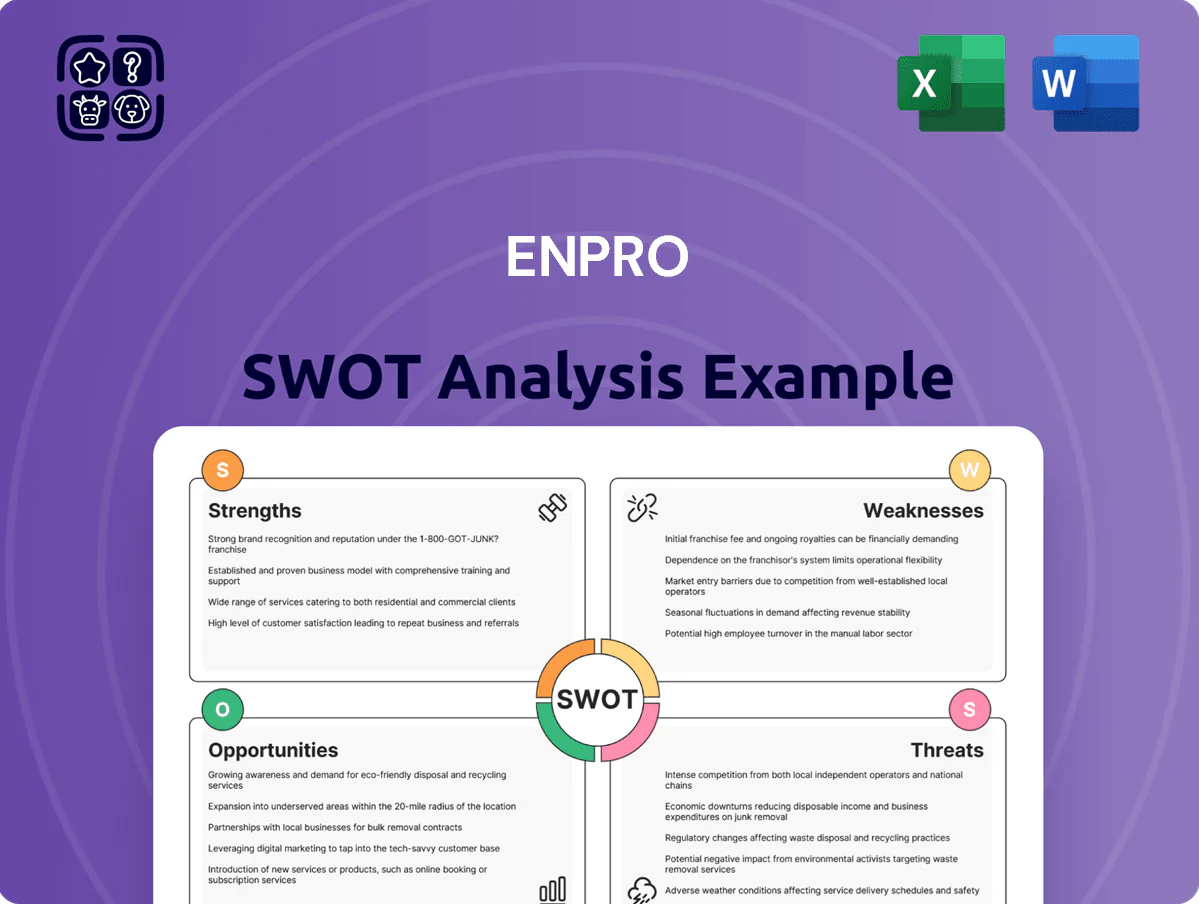

EnPro SWOT Analysis

Your Strategic Toolkit Starts Here

Uncover EnPro’s competitive edge, operational risks, and strategic growth levers with our concise SWOT preview—then purchase the full analysis for a research-backed, investor-ready report that includes editable Word and Excel deliverables to support planning, pitches, and investment decisions.

Strengths

Leadership in High-Margin Sealing Technologies

EnPro Holdings leads high-margin sealing tech for failure-intolerant markets—about 45% of 2024 sales came from engineered products serving aerospace, nuclear, and pharma, where uptime is critical.

These end-markets drive >60% repeat purchase rates and long product lifecycles, supporting aftermarket margins near 30% and recurring revenue that bolstered 2024 gross margin to ~34%.

Advanced Surface Technologies for Semiconductors

EnPro’s Advanced Surface Technologies has shifted revenue mix toward semiconductors, fueling 2025 segment growth—reported as roughly 18% CAGR since 2021 and contributing about $220m revenue in FY2024—by supplying critical wafer-clean and surface-treatment services for next-gen chips.

By supporting logic and AI accelerator fabs, the segment ties EnPro to long-term electronics and AI secular demand; global semiconductor capital spending was $118bn in 2024, so EnPro gains durable end-market exposure.

The business creates a high-technology moat: complex process know-how and capital-intensive tools mean competitors need multi-year investment and specialized talent to replicate EnPro’s position, lowering direct substitution risk.

Strong Free Cash Flow Generation

EnPro Industries generated $198 million of free cash flow in FY2024 (year ended Sept 30, 2024), funding $45 million in share repurchases and $30 million in dividends while cutting net debt by $60 million; this cash conversion underpins disciplined capital allocation to R&D and M&A. Maintaining a net debt/EBITDA near 1.0 keeps the balance sheet resilient during industrial cyclicality, supporting buybacks without sacrificing investment.

Portfolio Optimization and Strategic Focus

EnPro has sold multiple lower-margin, cyclical units since 2018, boosting trailing-12-month adjusted EBITDA margin to about 18% as of Q3 2025 and narrowing capital expenditures to roughly 3% of sales, sharpening its industrial-technology focus and investor value prop.

The pivot reduced legacy liabilities exposure and improved quality of earnings: operating cash flow rose 22% year-over-year in 2024, while net debt/EBITDA fell from ~3.2x in 2019 to ~1.6x in Q3 2025.

- Adjusted EBITDA margin ~18% (TTM Q3 2025)

- CapEx ≈3% of revenue (2024)

- Op. cash flow +22% YoY (2024)

- Net debt/EBITDA ≈1.6x (Q3 2025)

Deep Engineering Expertise and Innovation

EnPro leverages a large material-science repository to solve complex sealing and surface-treatment problems for a global customer base, enabling joint product development and early-stage tech embedding; Roper-like margins return—EnPro reported 2024 R&D spend of $51.6m (about 4.2% of revenue) and patent filings up 9% YoY through 2024.

- Co-develops designs with customers, shortening development by months

- R&D $51.6m in 2024, 4.2% of revenue

- Patents filed +9% YoY (2024)

- Focus on sealing & surface tech keeps win-rate high in industrial accounts

EnPro: High-margin surface tech drives $220M unit, $198M FCF, debt down to ~1.6x

EnPro’s high-margin sealing and surface-tech serving aerospace, nuclear, pharma, and semiconductors drove recurring revenue and ~34% gross margin in 2024, with Advanced Surface Technologies at ~$220m revenue (FY2024) and ~18% CAGR since 2021; FCF was $198m (FY2024) funding $45m buybacks and $30m dividends while net debt/EBITDA fell to ~1.6x (Q3 2025).

| Metric | Value |

|---|---|

| Gross margin (2024) | ~34% |

| Advanced Surface Rev (FY2024) | $220m |

| FCF (FY2024) | $198m |

| Net debt/EBITDA (Q3 2025) | ~1.6x |

What is included in the product

Provides a concise SWOT assessment of EnPro, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a clear, one-page EnPro SWOT that accelerates strategic alignment and supports fast decision-making for executives and teams.

Weaknesses

Sensitivity to Semiconductor Industry Cyclicality

EnPro’s reliance on semiconductor cleaning and coating ties revenue to a cyclical market where global wafer fab equipment spending fell about 28% in 2023 to $95bn and rebounded unevenly in 2024, causing quarterly revenue swings; major fab capex cuts by TSMC or Samsung can trim near-term orders and produce earnings volatility, a risk that may deter conservative investors focused on stable cash flows.

Concentration in Specialized Industrial Niches

EnPro's focus on specialized industrial niches limits TAM for many products; several segments address markets under $1bn annually, constraining upside versus broad-market peers.

That niche focus creates a durable moat but capped organic growth—EnPro's 2024 revenue grew 3.8% to $1.09bn, below broader industrial peers averaging ~7–10%.

To sustain mid-single-digit growth, EnPro must enter new niches or bolt on acquisitions; management spent $120m on M&A in 2023–24 to offset organic limits.

Complexity in Integrating High-Tech Acquisitions

The shift to an industrial-technology model depends on integrating high-tech buys; EnPro’s 2024 acquisitions added $180M in revenue but only 8% margin, below the company average, signaling integration lag.

Failing to capture synergies or retain key engineers risks eroding deal returns—EnPro reported 14% voluntary turnover at recent tech units vs 6% companywide in 2024.

Bridging cultural and operational gaps between legacy manufacturing and software-heavy services remains hard and could delay projected $40M cost saves through 2026.

Dependence on Key Large Customers

In Advanced Surface Technologies, roughly 30-40% of EnPro's segment revenue in 2024 came from a handful of large semiconductor equipment manufacturers, creating concentration risk; losing one major contract could cut segment revenue by double-digit percent and hurt margins.

Maintaining close technical roadmaps and account teams is essential, since shifts in procurement or vertical integration by those customers would materially affect cash flow and R&D prioritization.

- 30–40% segment revenue from few customers (2024)

- Loss of one contract → potential double-digit % revenue hit

- Requires continuous relationship and tech alignment

Vulnerability to Raw Material Price Fluctuations

- High-performance polymers, metals volatile (~±25% 2022–24)

- Surcharge lag reduced gross margin to 22.1% in Q4 2024

- Supply disruptions caused 2023 production cuts, higher freight/overtime

EnPro: cyclical WFE swings, high customer concentration and thin margins

EnPro’s revenue is cyclical and concentrated: wafer fab equipment spending dropped ~28% to $95bn in 2023 and rebounded unevenly in 2024, causing quarterly swings; 30–40% of Advanced Surface revenue came from a few customers in 2024, so losing one contract could cut segment revenue by double digits. Organic growth lags peers (2024 revenue +3.8% to $1.09bn vs peers ~7–10%); 2023–24 M&A $120m, added $180m revenue but 8% margin. Q4 2024 gross margin 22.1%; input cost volatility ~±25% (2022–24).

| Metric | Value |

|---|---|

| 2024 revenue | $1.09bn |

| Revenue growth 2024 | +3.8% |

| Q4 2024 gross margin | 22.1% |

| WFE spend 2023 | $95bn (−28%) |

| Customer concentration | 30–40% segment rev |

| Input price volatility | ~±25% (2022–24) |

| M&A 2023–24 | $120m spent, +$180m rev (8% margin) |

Full Version Awaits

EnPro SWOT Analysis

This is the actual EnPro SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality and structured insights across strengths, weaknesses, opportunities, and threats.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Strategic Toolkit Starts Here

Uncover EnPro’s competitive edge, operational risks, and strategic growth levers with our concise SWOT preview—then purchase the full analysis for a research-backed, investor-ready report that includes editable Word and Excel deliverables to support planning, pitches, and investment decisions.

Strengths

Leadership in High-Margin Sealing Technologies

EnPro Holdings leads high-margin sealing tech for failure-intolerant markets—about 45% of 2024 sales came from engineered products serving aerospace, nuclear, and pharma, where uptime is critical.

These end-markets drive >60% repeat purchase rates and long product lifecycles, supporting aftermarket margins near 30% and recurring revenue that bolstered 2024 gross margin to ~34%.

Advanced Surface Technologies for Semiconductors

EnPro’s Advanced Surface Technologies has shifted revenue mix toward semiconductors, fueling 2025 segment growth—reported as roughly 18% CAGR since 2021 and contributing about $220m revenue in FY2024—by supplying critical wafer-clean and surface-treatment services for next-gen chips.

By supporting logic and AI accelerator fabs, the segment ties EnPro to long-term electronics and AI secular demand; global semiconductor capital spending was $118bn in 2024, so EnPro gains durable end-market exposure.

The business creates a high-technology moat: complex process know-how and capital-intensive tools mean competitors need multi-year investment and specialized talent to replicate EnPro’s position, lowering direct substitution risk.

Strong Free Cash Flow Generation

EnPro Industries generated $198 million of free cash flow in FY2024 (year ended Sept 30, 2024), funding $45 million in share repurchases and $30 million in dividends while cutting net debt by $60 million; this cash conversion underpins disciplined capital allocation to R&D and M&A. Maintaining a net debt/EBITDA near 1.0 keeps the balance sheet resilient during industrial cyclicality, supporting buybacks without sacrificing investment.

Portfolio Optimization and Strategic Focus

EnPro has sold multiple lower-margin, cyclical units since 2018, boosting trailing-12-month adjusted EBITDA margin to about 18% as of Q3 2025 and narrowing capital expenditures to roughly 3% of sales, sharpening its industrial-technology focus and investor value prop.

The pivot reduced legacy liabilities exposure and improved quality of earnings: operating cash flow rose 22% year-over-year in 2024, while net debt/EBITDA fell from ~3.2x in 2019 to ~1.6x in Q3 2025.

- Adjusted EBITDA margin ~18% (TTM Q3 2025)

- CapEx ≈3% of revenue (2024)

- Op. cash flow +22% YoY (2024)

- Net debt/EBITDA ≈1.6x (Q3 2025)

Deep Engineering Expertise and Innovation

EnPro leverages a large material-science repository to solve complex sealing and surface-treatment problems for a global customer base, enabling joint product development and early-stage tech embedding; Roper-like margins return—EnPro reported 2024 R&D spend of $51.6m (about 4.2% of revenue) and patent filings up 9% YoY through 2024.

- Co-develops designs with customers, shortening development by months

- R&D $51.6m in 2024, 4.2% of revenue

- Patents filed +9% YoY (2024)

- Focus on sealing & surface tech keeps win-rate high in industrial accounts

EnPro: High-margin surface tech drives $220M unit, $198M FCF, debt down to ~1.6x

EnPro’s high-margin sealing and surface-tech serving aerospace, nuclear, pharma, and semiconductors drove recurring revenue and ~34% gross margin in 2024, with Advanced Surface Technologies at ~$220m revenue (FY2024) and ~18% CAGR since 2021; FCF was $198m (FY2024) funding $45m buybacks and $30m dividends while net debt/EBITDA fell to ~1.6x (Q3 2025).

| Metric | Value |

|---|---|

| Gross margin (2024) | ~34% |

| Advanced Surface Rev (FY2024) | $220m |

| FCF (FY2024) | $198m |

| Net debt/EBITDA (Q3 2025) | ~1.6x |

What is included in the product

Provides a concise SWOT assessment of EnPro, highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a clear, one-page EnPro SWOT that accelerates strategic alignment and supports fast decision-making for executives and teams.

Weaknesses

Sensitivity to Semiconductor Industry Cyclicality

EnPro’s reliance on semiconductor cleaning and coating ties revenue to a cyclical market where global wafer fab equipment spending fell about 28% in 2023 to $95bn and rebounded unevenly in 2024, causing quarterly revenue swings; major fab capex cuts by TSMC or Samsung can trim near-term orders and produce earnings volatility, a risk that may deter conservative investors focused on stable cash flows.

Concentration in Specialized Industrial Niches

EnPro's focus on specialized industrial niches limits TAM for many products; several segments address markets under $1bn annually, constraining upside versus broad-market peers.

That niche focus creates a durable moat but capped organic growth—EnPro's 2024 revenue grew 3.8% to $1.09bn, below broader industrial peers averaging ~7–10%.

To sustain mid-single-digit growth, EnPro must enter new niches or bolt on acquisitions; management spent $120m on M&A in 2023–24 to offset organic limits.

Complexity in Integrating High-Tech Acquisitions

The shift to an industrial-technology model depends on integrating high-tech buys; EnPro’s 2024 acquisitions added $180M in revenue but only 8% margin, below the company average, signaling integration lag.

Failing to capture synergies or retain key engineers risks eroding deal returns—EnPro reported 14% voluntary turnover at recent tech units vs 6% companywide in 2024.

Bridging cultural and operational gaps between legacy manufacturing and software-heavy services remains hard and could delay projected $40M cost saves through 2026.

Dependence on Key Large Customers

In Advanced Surface Technologies, roughly 30-40% of EnPro's segment revenue in 2024 came from a handful of large semiconductor equipment manufacturers, creating concentration risk; losing one major contract could cut segment revenue by double-digit percent and hurt margins.

Maintaining close technical roadmaps and account teams is essential, since shifts in procurement or vertical integration by those customers would materially affect cash flow and R&D prioritization.

- 30–40% segment revenue from few customers (2024)

- Loss of one contract → potential double-digit % revenue hit

- Requires continuous relationship and tech alignment

Vulnerability to Raw Material Price Fluctuations

- High-performance polymers, metals volatile (~±25% 2022–24)

- Surcharge lag reduced gross margin to 22.1% in Q4 2024

- Supply disruptions caused 2023 production cuts, higher freight/overtime

EnPro: cyclical WFE swings, high customer concentration and thin margins

EnPro’s revenue is cyclical and concentrated: wafer fab equipment spending dropped ~28% to $95bn in 2023 and rebounded unevenly in 2024, causing quarterly swings; 30–40% of Advanced Surface revenue came from a few customers in 2024, so losing one contract could cut segment revenue by double digits. Organic growth lags peers (2024 revenue +3.8% to $1.09bn vs peers ~7–10%); 2023–24 M&A $120m, added $180m revenue but 8% margin. Q4 2024 gross margin 22.1%; input cost volatility ~±25% (2022–24).

| Metric | Value |

|---|---|

| 2024 revenue | $1.09bn |

| Revenue growth 2024 | +3.8% |

| Q4 2024 gross margin | 22.1% |

| WFE spend 2023 | $95bn (−28%) |

| Customer concentration | 30–40% segment rev |

| Input price volatility | ~±25% (2022–24) |

| M&A 2023–24 | $120m spent, +$180m rev (8% margin) |

Full Version Awaits

EnPro SWOT Analysis

This is the actual EnPro SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality and structured insights across strengths, weaknesses, opportunities, and threats.