Entegris Porter's Five Forces Analysis

Don't Miss the Bigger Picture

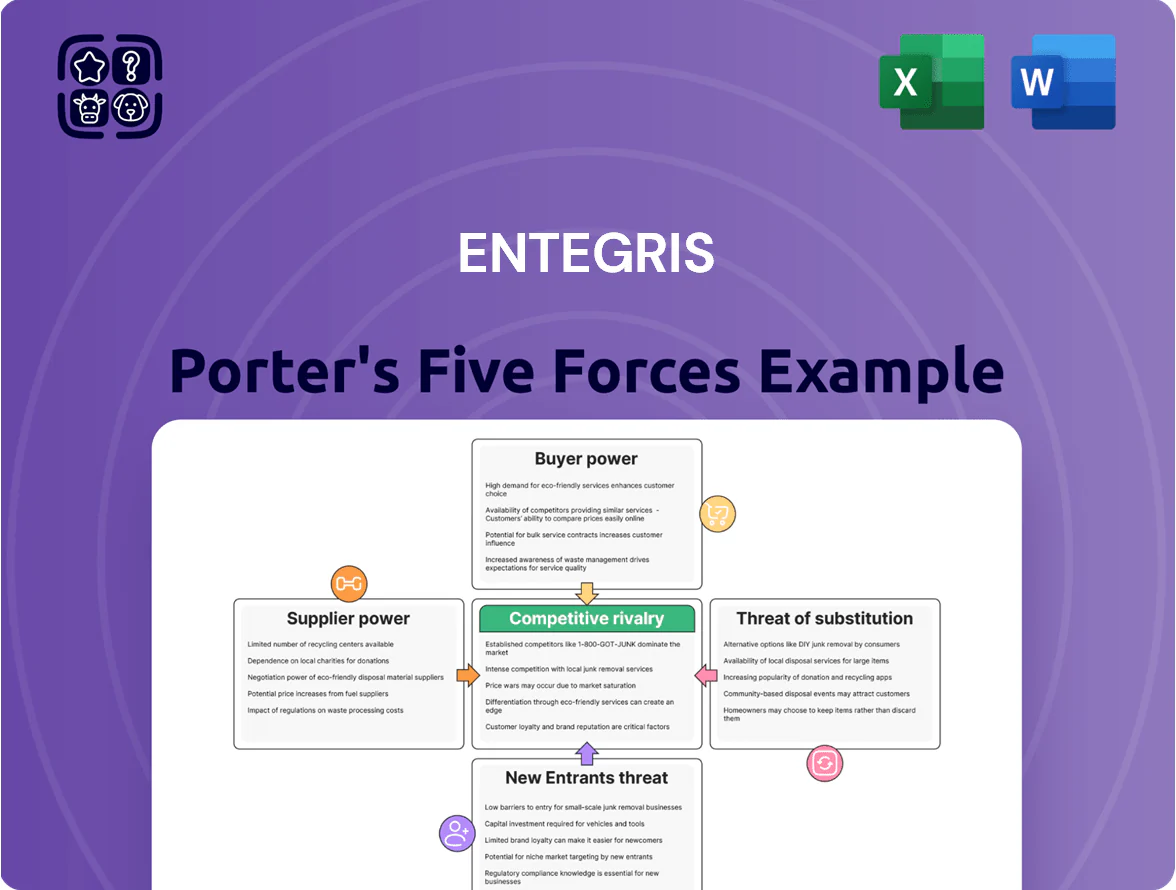

Entegris faces moderate supplier power, high buyer demands for purity and reliability, and significant rivalry from specialized semiconductor materials players—while barriers to entry remain substantial due to tech intensity and capital needs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Entegris’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Requirements

The production of high-purity chemicals and advanced polymers needs raw materials meeting sub-ppb (parts-per-billion) cleanliness; only about 10–15 global vendors can meet these specs, giving suppliers strong leverage over Entegris (as of 2025 Entegris sourced ~40% of specialty inputs from top 5 suppliers). This dependency is acute for rare earths and noble gases—neon and helium supply shocks in 2022–24 pushed spot prices up 120–300%, raising input-cost volatility and supplier bargaining power.

Validation and Regulatory Constraints

Suppliers face strict qualification: fabs require particle levels <1 ppb for key chemicals and Entegris reports supplier audits account for ~12% of procurement spend timing, so qualification takes months. Once a supplier is specced into an Entegris product line, re-qualification and customer notification drive high switching costs and downtime risk, locking customers in. That lock-in boosts supplier pricing power at renewals, evident in 2024 when specialty-material price increases contributed to ~2–3% margin pressure.

Energy and Utility Cost Pass-throughs

The manufacturing of specialty materials at Entegris is energy-intensive, so 2024 electricity and natural gas price volatility (US industrial electricity up ~8% YoY; natural gas spot prices +20% in 2023–24) directly raises COGS and gross-margin pressure.

Utilities suppliers sit in regulated or oligopolistic markets, giving Entegris limited rate-negotiation power and forcing either cost absorption or customer surcharges.

Entegris disclosed energy-related pass-throughs in pricing actions during 2023–25, but margin recovery depends on customer contract terms and cyclical chip demand.

Supplier Consolidation Trends

The chemical and materials sector saw 18% fewer independent suppliers from 2018–2024, concentrating spend among top 5 vendors and raising supplier leverage over Entegris (market data, 2024).

Larger suppliers used M&A to push stricter payment terms—average payable days extended from 45 to 62 days in specialty chemicals between 2019–2024—pressuring Entegris cash flow.

To reduce disruption risk from dominant vendors, Entegris holds strategic buffer stocks equal to roughly 8–10 weeks of critical components, adding inventory carrying costs of about 1.2% of revenue (2024 estimate).

- Supplier count down 18% (2018–2024)

- Top 5 vendors control majority spend (2024)

- Payables rose 45→62 days (2019–2024)

- Buffer stock = 8–10 weeks, ~1.2% revenue cost (2024 est.)

Geopolitical Influence on Key Inputs

- ~60% supply concentration in China/DRC (rare-earths/cobalt)

- FY2024: raw-materials pressured gross margin by 2.1 ppt

- Diversification limited by specialized precursor specs

- High supplier power increases input-cost volatility

Supplier power, gas shocks and energy costs shave 2.1ppt gross margin

Suppliers hold high bargaining power: ~10–15 qualified global vendors; Entegris sourced ~40% specialty inputs from top‑5 (2025). Rare gas shocks (neon/helium +120–300% in 2022–24) and energy cost rises (US industrial electricity +8% YoY, natural gas +20% 2023–24) raised COGS; FY2024 raw‑materials cut gross margin ~2.1 ppt; buffer stocks = 8–10 weeks (~1.2% revenue cost).

| Metric | Value |

|---|---|

| Qualified vendors | 10–15 |

| Top‑5 spend | ~40% |

| Neon/He price spike | +120–300% |

| Energy cost moves | +8% elec / +20% gas |

| Gross margin impact FY2024 | -2.1 ppt |

| Buffer stock | 8–10 weeks (~1.2% rev) |

What is included in the product

Tailored for Entegris, this Porter's Five Forces analysis uncovers competitive dynamics, supplier and buyer power, threats from substitutes and new entrants, and strategic levers protecting market position to inform investor and management decisions.

A concise Porter's Five Forces one-sheet for Entegris—quickly assess supplier, buyer, and competitive pressures to speed strategic decisions.

Customers Bargaining Power

Concentration of Major Semiconductor Fabs

A small group of fabs—TSMC, Samsung, Intel—accounts for roughly 40–50% of Entegris’s wafer-chemical and filtration demand, giving them outsized leverage over pricing and terms.

Because these customers place massive, repeat orders (TSMC alone grew capex to ~$40B in 2024), they can push for price cuts, longer payment terms, or bespoke supplies, squeezing Entegris’s gross margins.

Their gatekeeper role also raises switching-cost risk: losing one large fab could cut Entegris revenue by double digits in a year, so Entegris must balance margin protection with strategic account retention.

High Switching Costs for Qualified Materials

Entegris gains strong customer bargaining power protection because its filtration systems and chemical precursors are often embedded in customers’ process recipes; once qualified, switching risks yield loss and downtime. For example, fabs typically require 6–18 months requalification and may face yield declines up to 5% during vendor changeovers, so price alone rarely drives vendor swaps. This technical lock-in keeps customer switching leverage low and supports Entegris’ pricing resilience.

Yield-Critical Nature of Products

For semiconductor fabs, Entegris materials often account for well under 1% of wafer production cost while a single contamination event can destroy wafers worth $5–10 million, so customers favor proven reliability over price cuts.

This yield-critical dynamic gives Entegris measurable pricing power: customers accept price premia to avoid yield loss, supporting Entegris’s 2024 gross margin of ~46% and 5–7% ASP (average selling price) premiums on qualifying high-purity products.

Collaborative R and D Cycles

Entegris partners with chipmakers years ahead to co-develop materials and filtration for future nodes like 2nm, embedding its products in customers’ roadmaps and raising switching costs.

This deep collaboration creates dependency: customers risk delays and yield loss if they replace Entegris, reducing their leverage in price or contract negotiations.

In 2025 Entegris reported R&D spend of $232 million and >1,000 customer-engaged projects, reinforcing its innovation lock-in.

- Long lead co‑development: years

- R&D spend 2025: $232M

- Customer projects: >1,000

- High switching cost, low bargaining power

Demand for Localized Support

Global chipmakers now expect Entegris to hold local inventory and staff near fabs in Arizona, Taiwan, and Korea; in 2024 Entegris reported 52% of revenue tied to Asia-Pacific, underscoring regional reliance.

Maintaining warehouses, single-digit lead times, and on-site support raises switching costs for customers, so demand for localized service strengthens Entegris’s bargaining position.

- 52% revenue APAC (2024)

- Local inventory near major fabs

- High service levels = higher switching cost

- Complex logistics deter provider changes

Entegris: High fab concentration boosts leverage amid costly switching, strong margins

Major fabs (TSMC, Samsung, Intel) drive 40–50% of demand, giving them leverage, but high switching costs—6–18 months requalification, potential 5% yield loss—plus Entegris’s 2024 gross margin ~46% and 2025 R&D $232M, >1,000 projects, and 52% APAC revenue, limit customer bargaining power.

| Metric | Value |

|---|---|

| Top-fab share | 40–50% |

| Requalification time | 6–18 months |

| Potential yield loss | up to 5% |

| Gross margin (2024) | ~46% |

| R&D (2025) | $232M |

| Customer projects | >1,000 |

| APAC revenue (2024) | 52% |

Full Version Awaits

Entegris Porter's Five Forces Analysis

This preview shows the exact Entegris Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Entegris faces moderate supplier power, high buyer demands for purity and reliability, and significant rivalry from specialized semiconductor materials players—while barriers to entry remain substantial due to tech intensity and capital needs.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Entegris’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Requirements

The production of high-purity chemicals and advanced polymers needs raw materials meeting sub-ppb (parts-per-billion) cleanliness; only about 10–15 global vendors can meet these specs, giving suppliers strong leverage over Entegris (as of 2025 Entegris sourced ~40% of specialty inputs from top 5 suppliers). This dependency is acute for rare earths and noble gases—neon and helium supply shocks in 2022–24 pushed spot prices up 120–300%, raising input-cost volatility and supplier bargaining power.

Validation and Regulatory Constraints

Suppliers face strict qualification: fabs require particle levels <1 ppb for key chemicals and Entegris reports supplier audits account for ~12% of procurement spend timing, so qualification takes months. Once a supplier is specced into an Entegris product line, re-qualification and customer notification drive high switching costs and downtime risk, locking customers in. That lock-in boosts supplier pricing power at renewals, evident in 2024 when specialty-material price increases contributed to ~2–3% margin pressure.

Energy and Utility Cost Pass-throughs

The manufacturing of specialty materials at Entegris is energy-intensive, so 2024 electricity and natural gas price volatility (US industrial electricity up ~8% YoY; natural gas spot prices +20% in 2023–24) directly raises COGS and gross-margin pressure.

Utilities suppliers sit in regulated or oligopolistic markets, giving Entegris limited rate-negotiation power and forcing either cost absorption or customer surcharges.

Entegris disclosed energy-related pass-throughs in pricing actions during 2023–25, but margin recovery depends on customer contract terms and cyclical chip demand.

Supplier Consolidation Trends

The chemical and materials sector saw 18% fewer independent suppliers from 2018–2024, concentrating spend among top 5 vendors and raising supplier leverage over Entegris (market data, 2024).

Larger suppliers used M&A to push stricter payment terms—average payable days extended from 45 to 62 days in specialty chemicals between 2019–2024—pressuring Entegris cash flow.

To reduce disruption risk from dominant vendors, Entegris holds strategic buffer stocks equal to roughly 8–10 weeks of critical components, adding inventory carrying costs of about 1.2% of revenue (2024 estimate).

- Supplier count down 18% (2018–2024)

- Top 5 vendors control majority spend (2024)

- Payables rose 45→62 days (2019–2024)

- Buffer stock = 8–10 weeks, ~1.2% revenue cost (2024 est.)

Geopolitical Influence on Key Inputs

- ~60% supply concentration in China/DRC (rare-earths/cobalt)

- FY2024: raw-materials pressured gross margin by 2.1 ppt

- Diversification limited by specialized precursor specs

- High supplier power increases input-cost volatility

Supplier power, gas shocks and energy costs shave 2.1ppt gross margin

Suppliers hold high bargaining power: ~10–15 qualified global vendors; Entegris sourced ~40% specialty inputs from top‑5 (2025). Rare gas shocks (neon/helium +120–300% in 2022–24) and energy cost rises (US industrial electricity +8% YoY, natural gas +20% 2023–24) raised COGS; FY2024 raw‑materials cut gross margin ~2.1 ppt; buffer stocks = 8–10 weeks (~1.2% revenue cost).

| Metric | Value |

|---|---|

| Qualified vendors | 10–15 |

| Top‑5 spend | ~40% |

| Neon/He price spike | +120–300% |

| Energy cost moves | +8% elec / +20% gas |

| Gross margin impact FY2024 | -2.1 ppt |

| Buffer stock | 8–10 weeks (~1.2% rev) |

What is included in the product

Tailored for Entegris, this Porter's Five Forces analysis uncovers competitive dynamics, supplier and buyer power, threats from substitutes and new entrants, and strategic levers protecting market position to inform investor and management decisions.

A concise Porter's Five Forces one-sheet for Entegris—quickly assess supplier, buyer, and competitive pressures to speed strategic decisions.

Customers Bargaining Power

Concentration of Major Semiconductor Fabs

A small group of fabs—TSMC, Samsung, Intel—accounts for roughly 40–50% of Entegris’s wafer-chemical and filtration demand, giving them outsized leverage over pricing and terms.

Because these customers place massive, repeat orders (TSMC alone grew capex to ~$40B in 2024), they can push for price cuts, longer payment terms, or bespoke supplies, squeezing Entegris’s gross margins.

Their gatekeeper role also raises switching-cost risk: losing one large fab could cut Entegris revenue by double digits in a year, so Entegris must balance margin protection with strategic account retention.

High Switching Costs for Qualified Materials

Entegris gains strong customer bargaining power protection because its filtration systems and chemical precursors are often embedded in customers’ process recipes; once qualified, switching risks yield loss and downtime. For example, fabs typically require 6–18 months requalification and may face yield declines up to 5% during vendor changeovers, so price alone rarely drives vendor swaps. This technical lock-in keeps customer switching leverage low and supports Entegris’ pricing resilience.

Yield-Critical Nature of Products

For semiconductor fabs, Entegris materials often account for well under 1% of wafer production cost while a single contamination event can destroy wafers worth $5–10 million, so customers favor proven reliability over price cuts.

This yield-critical dynamic gives Entegris measurable pricing power: customers accept price premia to avoid yield loss, supporting Entegris’s 2024 gross margin of ~46% and 5–7% ASP (average selling price) premiums on qualifying high-purity products.

Collaborative R and D Cycles

Entegris partners with chipmakers years ahead to co-develop materials and filtration for future nodes like 2nm, embedding its products in customers’ roadmaps and raising switching costs.

This deep collaboration creates dependency: customers risk delays and yield loss if they replace Entegris, reducing their leverage in price or contract negotiations.

In 2025 Entegris reported R&D spend of $232 million and >1,000 customer-engaged projects, reinforcing its innovation lock-in.

- Long lead co‑development: years

- R&D spend 2025: $232M

- Customer projects: >1,000

- High switching cost, low bargaining power

Demand for Localized Support

Global chipmakers now expect Entegris to hold local inventory and staff near fabs in Arizona, Taiwan, and Korea; in 2024 Entegris reported 52% of revenue tied to Asia-Pacific, underscoring regional reliance.

Maintaining warehouses, single-digit lead times, and on-site support raises switching costs for customers, so demand for localized service strengthens Entegris’s bargaining position.

- 52% revenue APAC (2024)

- Local inventory near major fabs

- High service levels = higher switching cost

- Complex logistics deter provider changes

Entegris: High fab concentration boosts leverage amid costly switching, strong margins

Major fabs (TSMC, Samsung, Intel) drive 40–50% of demand, giving them leverage, but high switching costs—6–18 months requalification, potential 5% yield loss—plus Entegris’s 2024 gross margin ~46% and 2025 R&D $232M, >1,000 projects, and 52% APAC revenue, limit customer bargaining power.

| Metric | Value |

|---|---|

| Top-fab share | 40–50% |

| Requalification time | 6–18 months |

| Potential yield loss | up to 5% |

| Gross margin (2024) | ~46% |

| R&D (2025) | $232M |

| Customer projects | >1,000 |

| APAC revenue (2024) | 52% |

Full Version Awaits

Entegris Porter's Five Forces Analysis

This preview shows the exact Entegris Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or samples, fully formatted and ready for use.