Envista Boston Consulting Group Matrix

Unlock Strategic Clarity

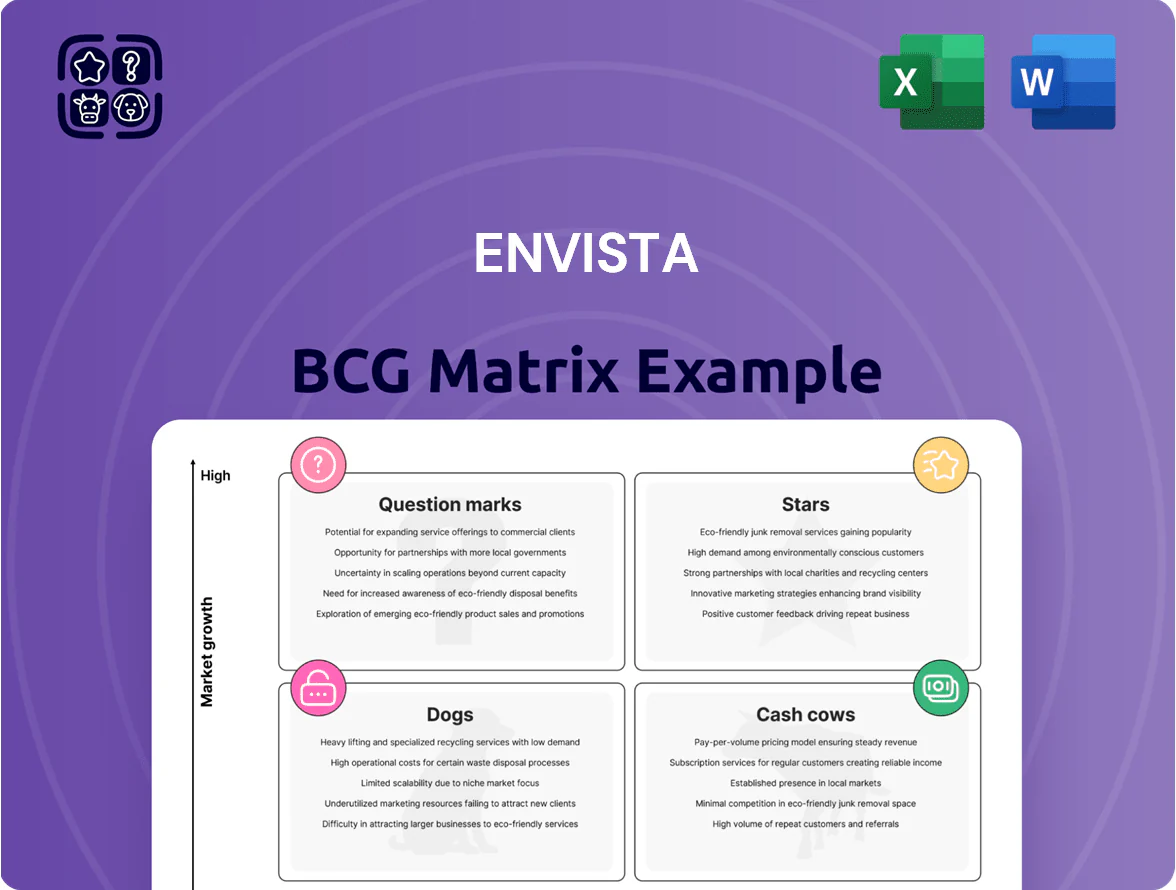

Envista’s BCG Matrix preview highlights how its product lines balance market share and growth—spotting potential Stars in imaging and any Cash Cows in consumables, while flagging Question Marks and Dogs that need strategic review. This snapshot guides resource allocation and portfolio prioritization at a glance. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel files that speed your investment and product decisions.

Stars

Spark Clear Aligners

As of late 2025, Spark Clear Aligners is a Star in Envista’s BCG matrix: high market growth and strong share—Spark grew unit shipments ~38% YoY in 2024–25 and took ~14% global aligner share by Q3 2025, driven by advanced polymer materials and a doctor-centric digital workflow.

It needs heavy marketing and clinician education—Envista planned $120–150M capex/marketing spend for Spark in 2025—but rapid orthodontist adoption (clinic installs up ~30% YoY) makes it a primary growth engine amid a global shift to aesthetic, digitally planned treatments.

Nobel Biocare N1 System

Nobel Biocare N1 System sits in Stars: rapid growth in the premium implant market, driven by biological design and simplified protocols; global implant market grew 7.8% in 2024 to $5.6B, premium segment ~18% (2024).

Envista has poured R&D and sales support—R&D spend rose 12% to $145M in FY2024—aiming to capture next-gen implantologists seeking efficiency and better outcomes.

N1 holds a leadership spot in the high-growth biological dental niche, but consumes capital for expansion: 2024 capex tied to platform rollout ~ $60M and rising.

DEXIS Digital Imaging Ecosystem

DEXIS Digital Imaging Ecosystem sits in Envista’s high-growth BCG quadrant as a market leader in digital diagnostics, with dental imaging market expected to grow at ~8.2% CAGR through 2028 and DEXIS holding a top share in intraoral sensors (Envista reported imaging segment revenue of $1.2B in 2024).

By combining AI-driven diagnostics and cloud software, DEXIS captures rising demand for data-driven dentistry—AI reads reduce diagnostic time by ~30% in published pilot studies and cloud adoption in practices rose to 46% in 2024.

Continued capex for software updates and tighter hardware integration is essential; Envista’s 2024 R&D spend totaled $160M, and maintaining a 3–5% incremental market share requires sustained investment against competitors.

DTX Studio Suite

DTX Studio Suite sits in Envista’s BCG Matrix Stars: it’s an open-software connector driving cross-brand adoption as digital dental workflows grow ~18% CAGR through 2025, tying together imaging and device data crucial for modern high-tech practices.

It earns revenue—Envista reported ~12% software/recurrent sales growth in 2024—but high R&D and integration costs keep it in the star phase, requiring heavy reinvestment to scale and capture market share.

- High growth: ~18% CAGR to 2025

- Revenue lift: ~12% software growth in 2024

- Strategic role: unifies multi-vendor clinical data

- Needs reinvestment: elevated R&D and integration spend

Premium Biological Solutions

Envista’s Premium Biological Solutions—high-end bone grafts and membranes—are in a high-growth segment as complex implant procedures rose ~8% CAGR 2019–2024; these products command a top-tier share in the premium oral surgery market and drive durable clinical outcomes.

The firm spent ~$45m on clinical trials and specialist training in 2024 to keep these solutions the gold standard for oral surgeons and protect premium margins.

- High growth: ~8% CAGR 2019–2024

- 2024 R&D/training: ~$45m

- Top-tier market share in premium segment

- Key for long-term clinical success

High-growth dental stars: Spark, Nobel N1, DEXIS, DTX & Premium Bio dominate market gains

Stars: Spark, Nobel N1, DEXIS, DTX, Premium Biologicals—high growth, strong share; 2024–25 highlights: Spark shipments +38% YoY, ~14% global share (Q3 2025); Nobel N1 in premium implants (market $5.6B, premium ~18% 2024); DEXIS imaging revenue $1.2B (2024), AI cuts reads ~30%; DTX software rev +12% (2024); Premium bio spend ~$45M (2024).

| Product | Growth | 2024–25 datapoints |

|---|---|---|

| Spark | High | +38% shipments; 14% share; $120–150M spend (2025) |

| N1 | High | Premium implant market $5.6B; 18% premium |

| DEXIS | High | $1.2B imaging rev; AI −30% read time |

| DTX | High | +12% software rev (2024) |

| Premium Bio | High | $45M trials/training (2024) |

What is included in the product

Comprehensive BCG Matrix review of Envista’s portfolio with quadrant strategies, investment recommendations, and trend-driven risks/opportunities.

One-page Envista BCG Matrix placing each business unit in a quadrant for instant portfolio clarity

Cash Cows

Kerr Restorative Consumables

Kerr Restorative Consumables anchors Envista’s cash cows with roughly 25% share of the global restorative composites and cements market, delivering steady revenue of about $650 million in 2024 and predictable operating margins near 28%.

Stable demand for composites and cements keeps promotional spend low—Envista’s SG&A for Kerr lines ran ~8% of sales in 2024 versus 14% for new digital products—so cash generation is reliable.

High margins on everyday essentials funded Envista’s R&D spend of $120 million in 2024, underwriting riskier digital dentistry initiatives without tapping external capital.

Ormco Traditional Brackets

Ormco Traditional Brackets retain a high, stable share of the global orthodontics market—about 45% of device revenue in 2024—while clear aligners grow; they’re a mature, low-growth cash cow within Envista’s BCG matrix.

Manufacturing scale and 12–15% gross margins on metal/ceramic brackets cut costs, and a loyal clinical base means minimal marketing spend and predictable recurring orders.

Cash from Ormco’s portfolio funded roughly $120 million of Envista’s 2024 debt service and helped allocate $75–100 million into Spark aligner R&D and go-to-market expansion in 2024–2025.

Nobel Biocare Legacy Implants

Nobel Biocare legacy implants, including TiUnite surface lines, dominate a mature global implant market and generated steady revenue for Envista’s Specialty Products & Technologies—Nobel Biocare contributed about $520M of segment sales in FY2024, reflecting high brand recall among veteran clinicians.

These products enjoy material economies of scale and low incremental costs, delivering margin stability (gross margins ~65% on implant ranges in 2024) and acting as a cash cow funding R&D and growth initiatives.

Metrex Infection Prevention

Metrex Infection Prevention supplies high-share surface disinfectants and sterilization chemicals in healthcare and dental markets, generating roughly $120–150M annual revenue within Envista’s consumables segment as of 2025 and acting as a stable cash cow.

Demand is non-cyclical—hospital and dental hygiene use keeps volumes steady; Envista reported ~5–7% annual organic growth in infection-prevention consumables in 2024.

Low capex for mature chemical lines means high free cash flow conversion; Metrex margins exceed corporate average, freeing capital for M&A and R&D.

- High market share in stable healthcare/dental sectors

- Estimated $120–150M revenue (2025 range)

- Non-cyclical demand; ~5–7% organic growth (2024)

- Low capex, above-average margins, strong free cash flow

General Dental Instruments

Envista’s handpieces and basic surgical instruments sit squarely in Cash Cows: a mature, defensive market where Envista held roughly 22% global market share in dental instruments in 2024 and saw low single-digit volume decline but stable revenues of about $420 million in 2024.

These tools are essential to every dental practice, driving high replacement rates—estimated 12–18% annual replacement—and consistent sales volume with gross margins near 58% and minimal need for aggressive marketing.

Established distribution and brand trust (over 40,000 active distributor accounts globally in 2024) keep operating costs low and free cash flow steady, funding R&D and higher-growth segments without heavy reinvestment.

- Mature market, ~22% share (2024)

- Revenue ≈ $420M (2024)

- Replacement rate 12–18% p.a.

- Gross margin ≈ 58%

- 40,000+ distributor accounts (2024)

Envista’s cash cows power strong margins and steady cash: Kerr, Nobel, Handpieces lead

Envista cash cows (Kerr, Ormco brackets, Nobel Biocare implants, Metrex, handpieces) delivered steady 2024–25 cash: Kerr ~$650M revenue/28% op margin; Ormco ~45% device share funding $120M debt service; Nobel Biocare ~$520M sales/65% gross margin; Metrex $120–150M (2025)/5–7% organic growth; handpieces ~$420M/58% gross margin.

| Product | 2024–25 Revenue | Margin | Notes |

|---|---|---|---|

| Kerr | $650M | 28% op | 25% market share |

| Ormco | — | 12–15% gross | 45% device share |

| Nobel Biocare | $520M | 65% gross | legacy implants |

| Metrex | $120–150M | above avg | 5–7% growth |

| Handpieces | $420M | 58% gross | 22% market share |

What You’re Viewing Is Included

Envista BCG Matrix

The file you're previewing is the exact Envista BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

Envista’s BCG Matrix preview highlights how its product lines balance market share and growth—spotting potential Stars in imaging and any Cash Cows in consumables, while flagging Question Marks and Dogs that need strategic review. This snapshot guides resource allocation and portfolio prioritization at a glance. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-driven recommendations, and ready-to-use Word and Excel files that speed your investment and product decisions.

Stars

Spark Clear Aligners

As of late 2025, Spark Clear Aligners is a Star in Envista’s BCG matrix: high market growth and strong share—Spark grew unit shipments ~38% YoY in 2024–25 and took ~14% global aligner share by Q3 2025, driven by advanced polymer materials and a doctor-centric digital workflow.

It needs heavy marketing and clinician education—Envista planned $120–150M capex/marketing spend for Spark in 2025—but rapid orthodontist adoption (clinic installs up ~30% YoY) makes it a primary growth engine amid a global shift to aesthetic, digitally planned treatments.

Nobel Biocare N1 System

Nobel Biocare N1 System sits in Stars: rapid growth in the premium implant market, driven by biological design and simplified protocols; global implant market grew 7.8% in 2024 to $5.6B, premium segment ~18% (2024).

Envista has poured R&D and sales support—R&D spend rose 12% to $145M in FY2024—aiming to capture next-gen implantologists seeking efficiency and better outcomes.

N1 holds a leadership spot in the high-growth biological dental niche, but consumes capital for expansion: 2024 capex tied to platform rollout ~ $60M and rising.

DEXIS Digital Imaging Ecosystem

DEXIS Digital Imaging Ecosystem sits in Envista’s high-growth BCG quadrant as a market leader in digital diagnostics, with dental imaging market expected to grow at ~8.2% CAGR through 2028 and DEXIS holding a top share in intraoral sensors (Envista reported imaging segment revenue of $1.2B in 2024).

By combining AI-driven diagnostics and cloud software, DEXIS captures rising demand for data-driven dentistry—AI reads reduce diagnostic time by ~30% in published pilot studies and cloud adoption in practices rose to 46% in 2024.

Continued capex for software updates and tighter hardware integration is essential; Envista’s 2024 R&D spend totaled $160M, and maintaining a 3–5% incremental market share requires sustained investment against competitors.

DTX Studio Suite

DTX Studio Suite sits in Envista’s BCG Matrix Stars: it’s an open-software connector driving cross-brand adoption as digital dental workflows grow ~18% CAGR through 2025, tying together imaging and device data crucial for modern high-tech practices.

It earns revenue—Envista reported ~12% software/recurrent sales growth in 2024—but high R&D and integration costs keep it in the star phase, requiring heavy reinvestment to scale and capture market share.

- High growth: ~18% CAGR to 2025

- Revenue lift: ~12% software growth in 2024

- Strategic role: unifies multi-vendor clinical data

- Needs reinvestment: elevated R&D and integration spend

Premium Biological Solutions

Envista’s Premium Biological Solutions—high-end bone grafts and membranes—are in a high-growth segment as complex implant procedures rose ~8% CAGR 2019–2024; these products command a top-tier share in the premium oral surgery market and drive durable clinical outcomes.

The firm spent ~$45m on clinical trials and specialist training in 2024 to keep these solutions the gold standard for oral surgeons and protect premium margins.

- High growth: ~8% CAGR 2019–2024

- 2024 R&D/training: ~$45m

- Top-tier market share in premium segment

- Key for long-term clinical success

High-growth dental stars: Spark, Nobel N1, DEXIS, DTX & Premium Bio dominate market gains

Stars: Spark, Nobel N1, DEXIS, DTX, Premium Biologicals—high growth, strong share; 2024–25 highlights: Spark shipments +38% YoY, ~14% global share (Q3 2025); Nobel N1 in premium implants (market $5.6B, premium ~18% 2024); DEXIS imaging revenue $1.2B (2024), AI cuts reads ~30%; DTX software rev +12% (2024); Premium bio spend ~$45M (2024).

| Product | Growth | 2024–25 datapoints |

|---|---|---|

| Spark | High | +38% shipments; 14% share; $120–150M spend (2025) |

| N1 | High | Premium implant market $5.6B; 18% premium |

| DEXIS | High | $1.2B imaging rev; AI −30% read time |

| DTX | High | +12% software rev (2024) |

| Premium Bio | High | $45M trials/training (2024) |

What is included in the product

Comprehensive BCG Matrix review of Envista’s portfolio with quadrant strategies, investment recommendations, and trend-driven risks/opportunities.

One-page Envista BCG Matrix placing each business unit in a quadrant for instant portfolio clarity

Cash Cows

Kerr Restorative Consumables

Kerr Restorative Consumables anchors Envista’s cash cows with roughly 25% share of the global restorative composites and cements market, delivering steady revenue of about $650 million in 2024 and predictable operating margins near 28%.

Stable demand for composites and cements keeps promotional spend low—Envista’s SG&A for Kerr lines ran ~8% of sales in 2024 versus 14% for new digital products—so cash generation is reliable.

High margins on everyday essentials funded Envista’s R&D spend of $120 million in 2024, underwriting riskier digital dentistry initiatives without tapping external capital.

Ormco Traditional Brackets

Ormco Traditional Brackets retain a high, stable share of the global orthodontics market—about 45% of device revenue in 2024—while clear aligners grow; they’re a mature, low-growth cash cow within Envista’s BCG matrix.

Manufacturing scale and 12–15% gross margins on metal/ceramic brackets cut costs, and a loyal clinical base means minimal marketing spend and predictable recurring orders.

Cash from Ormco’s portfolio funded roughly $120 million of Envista’s 2024 debt service and helped allocate $75–100 million into Spark aligner R&D and go-to-market expansion in 2024–2025.

Nobel Biocare Legacy Implants

Nobel Biocare legacy implants, including TiUnite surface lines, dominate a mature global implant market and generated steady revenue for Envista’s Specialty Products & Technologies—Nobel Biocare contributed about $520M of segment sales in FY2024, reflecting high brand recall among veteran clinicians.

These products enjoy material economies of scale and low incremental costs, delivering margin stability (gross margins ~65% on implant ranges in 2024) and acting as a cash cow funding R&D and growth initiatives.

Metrex Infection Prevention

Metrex Infection Prevention supplies high-share surface disinfectants and sterilization chemicals in healthcare and dental markets, generating roughly $120–150M annual revenue within Envista’s consumables segment as of 2025 and acting as a stable cash cow.

Demand is non-cyclical—hospital and dental hygiene use keeps volumes steady; Envista reported ~5–7% annual organic growth in infection-prevention consumables in 2024.

Low capex for mature chemical lines means high free cash flow conversion; Metrex margins exceed corporate average, freeing capital for M&A and R&D.

- High market share in stable healthcare/dental sectors

- Estimated $120–150M revenue (2025 range)

- Non-cyclical demand; ~5–7% organic growth (2024)

- Low capex, above-average margins, strong free cash flow

General Dental Instruments

Envista’s handpieces and basic surgical instruments sit squarely in Cash Cows: a mature, defensive market where Envista held roughly 22% global market share in dental instruments in 2024 and saw low single-digit volume decline but stable revenues of about $420 million in 2024.

These tools are essential to every dental practice, driving high replacement rates—estimated 12–18% annual replacement—and consistent sales volume with gross margins near 58% and minimal need for aggressive marketing.

Established distribution and brand trust (over 40,000 active distributor accounts globally in 2024) keep operating costs low and free cash flow steady, funding R&D and higher-growth segments without heavy reinvestment.

- Mature market, ~22% share (2024)

- Revenue ≈ $420M (2024)

- Replacement rate 12–18% p.a.

- Gross margin ≈ 58%

- 40,000+ distributor accounts (2024)

Envista’s cash cows power strong margins and steady cash: Kerr, Nobel, Handpieces lead

Envista cash cows (Kerr, Ormco brackets, Nobel Biocare implants, Metrex, handpieces) delivered steady 2024–25 cash: Kerr ~$650M revenue/28% op margin; Ormco ~45% device share funding $120M debt service; Nobel Biocare ~$520M sales/65% gross margin; Metrex $120–150M (2025)/5–7% organic growth; handpieces ~$420M/58% gross margin.

| Product | 2024–25 Revenue | Margin | Notes |

|---|---|---|---|

| Kerr | $650M | 28% op | 25% market share |

| Ormco | — | 12–15% gross | 45% device share |

| Nobel Biocare | $520M | 65% gross | legacy implants |

| Metrex | $120–150M | above avg | 5–7% growth |

| Handpieces | $420M | 58% gross | 22% market share |

What You’re Viewing Is Included

Envista BCG Matrix

The file you're previewing is the exact Envista BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.