Eolus Vind Porter's Five Forces Analysis

Don't Miss the Bigger Picture

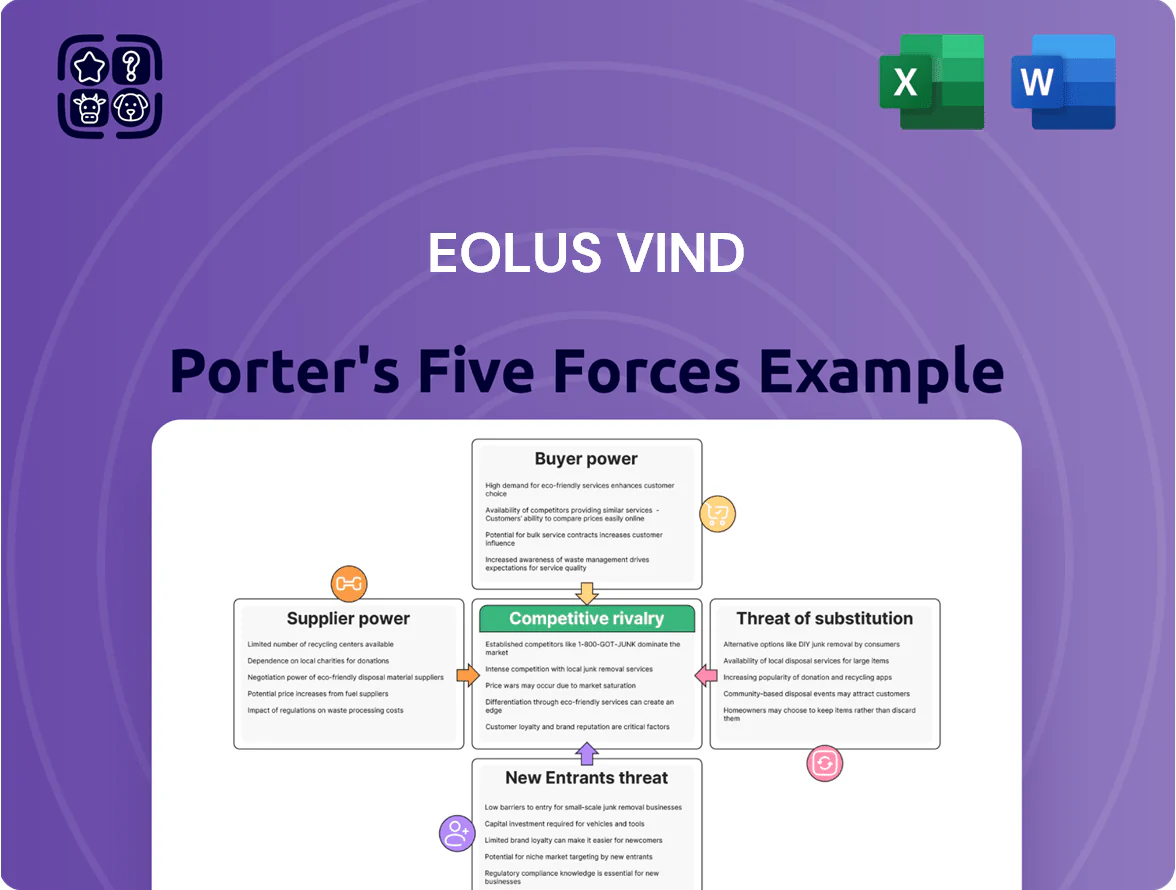

Eolus Vind faces moderate supplier power, intense rivalry among renewables developers, and growing buyer sophistication as green energy markets mature; barriers to entry are rising but technological change and policy shifts keep substitute threats meaningful. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Eolus Vind’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Wind Turbine Manufacturers

The high-capacity turbine market is concentrated: Vestas, Siemens Gamesa and GE held about 70–80% global market share in 2024–25 for >3 MW units, giving them strong bargaining power over Eolus Vind.

Eolus depends on supplier-specific blades, drivetrains and 15–25 year service contracts, so OEMs can dictate delivery schedules and spare-part pricing.

By late 2025 few suppliers can supply next-gen offshore 10+ MW and onshore 5+ MW units, keeping manufacturers’ pricing power high and capex uncertainty elevated for Eolus.

Raw Material Cost Volatility

Suppliers of steel, copper and rare earths now dictate Eolus Vind’s project margins: steel rose 28% and copper 35% in 2024, while neodymium prices jumped ~40% through 2024–2025, forcing index-linked procurement. Developers accepted pass-through clauses in 60–80% of 2024 supplier contracts, cutting Eolus’s ability to lock lower input costs. This means inflationary swings are directly transmitted to project budgets and EBITDA volatility.

Scarcity of Specialized Construction Services

The global shortage of specialized vessels and heavy‑lift rigs pushes suppliers’ power up: demand for offshore wind vessels rose 28% from 2020–2024 while available turbine‑installation vessels stayed flat, so Eolus competes with developers for scarce contractor slots and logistics capacity. Suppliers use that leverage to charge premiums—dayrates for jack‑up vessels climbed to €120k–€250k in 2024—and enforce tighter contract terms as EU renewables targets accelerate toward 2030.

Grid Connection Equipment Lead Times

Suppliers of high-voltage transformers and substation gear hit record backlogs into 2025—global grid upgrades pushed lead times to 18–36 months, according to industry reports.

Eolus Vind depends on a handful of specialized electrical firms to meet commissioning dates, creating supplier leverage over project timing and costs.

Long lead times and surge demand let suppliers prioritize large utilities over smaller independent developers, raising delivery risk and potential price pressure for Eolus.

- Typical lead times: 18–36 months by 2025

- Few specialized suppliers; high concentration

- Large utilities get priority; independents delayed

- Higher scheduling and price risk for Eolus

Landowner Leverage in Site Acquisition

Securing land rights is essential for Eolus Vind; private and municipal landowners thus hold significant leverage over site acquisition and timelines.

In Sweden prime wind sites fell by ~25% from 2015–2024, pushing average annual lease rates up about 18% to ~SEK 6–9k/ha in 2024, so owners demand higher rent or profit shares.

That local supplier power forces Eolus to offer enhanced lease terms or revenue-sharing to lock long-term exclusivity and avoid project delays.

- Prime-site scarcity: –25% (2015–2024)

- 2024 avg lease: ~SEK 6–9k/ha/yr

- Lease inflation: +18% vs 2015

- Response: higher profit-share or longer leases

Supply squeeze: OEM dominance & raw‑material spikes drive wind project costs up

Suppliers hold strong power: top OEMs (Vestas, Siemens Gamesa, GE) had ~70–80% share for >3 MW in 2024–25, steel +28% and copper +35% in 2024, neodymium +~40% through 2024–25, jack‑up dayrates €120k–€250k in 2024, HV lead times 18–36 months by 2025, Swedish leases ~SEK 6–9k/ha in 2024 (+18% vs 2015).

| Metric | Value |

|---|---|

| OEM share | 70–80% (2024–25) |

| Steel price | +28% (2024) |

| Copper price | +35% (2024) |

| Neodymium | +~40% (2024–25) |

| Jack‑up dayrates | €120k–€250k (2024) |

| HV lead times | 18–36 months (2025) |

| Sweden lease | SEK 6–9k/ha (2024) |

What is included in the product

Tailored exclusively for Eolus Vind, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape the company’s pricing power and long-term profitability.

A concise Porter's Five Forces one-sheet for Eolus Vind—quickly assess supplier, buyer, entrant, substitute, and rivalry pressures to streamline strategic decisions.

Customers Bargaining Power

Institutional Investor Requirements

Pension funds and insurers—core buyers for Eolus Vind—seek stable, long-term ESG assets; in 2025 Nordic pension funds target 5–7% portfolio allocation to renewables, raising expectations for predictability.

These sophisticated investors run deep due diligence and require transparent LCoE, P50/P90 yield models, and O&M risk metrics; missing items can cut valuations by 10–20% in buy-side models.

Because global allocators can redeploy capital quickly, Eolus faces strong buyer bargaining power: a 1% gap in IRR vs peers can shift multi‑year offtake demand to competitors.

Corporate Power Purchase Agreements

Utility-Scale Acquisition Strategies

Traditional utilities buy ready-to-build projects from developers like Eolus to meet 2030 RES targets; in Europe utilities acquired ~6.5 GW of wind/solar projects in 2024, tightening demand.

Utilities’ deep engineering and cost models let them estimate development costs to ±10% accuracy, capping Eolus’s premium negotiation room.

European utility consolidation—top 10 players control ~45% of generation—reduces buyer count and raises collective bargaining power over sellers.

Electricity Market Price Sensitivity

Customers push back when Eolus Vind’s Levelized Cost of Energy (LCOE) exceeds competing sources; 2024 EU onshore wind LCOE fell to about 30–50 EUR/MWh, so auction-winning bids cluster at the low end.

If market prices drop from oversupply or cheaper gas, buyers demand lower PPA rates; Nord Pool day-ahead averages fell to ~40 EUR/MWh in 2024, pressuring margins.

Eolus must cut capex/O&M and boost capacity factors; buyers favor the lowest-cost renewables in auctions where winning bids were often below 35 EUR/MWh in several 2024 EU tenders.

- 2024 EU onshore wind LCOE: ~30–50 EUR/MWh

- Nord Pool 2024 average: ~40 EUR/MWh

- Auction clearing bids often <35 EUR/MWh in 2024 tenders

Government and Regulatory Tender Processes

In many markets Eolus faces government-set renewable auctions where the state acts as proxy customer, and 2024 auction averages saw winning bids hit as low as 20–25 EUR/MWh in parts of Europe, capping project revenue.

These tenders are designed to drive prices down, so Eolus must chase thin margins—industry reports show wind developers' EBIT margins falling to mid-single digits in low-bid regimes.

That buyer power forces trade-offs: accept tight returns to secure volume or skip tenders and pursue merchant risk, which raises financing costs and time-to-market.

- Auctions cap price: 20–25 EUR/MWh observed (2024)

- Developer EBIT: mid-single digits in low-bid markets

- Choice: accept thin margins or assume merchant price risk

Buyers' leverage squeezes Eolus: cut costs, accept thin EBIT, or take merchant risk

Buyers hold strong leverage: pension funds, corporates, and utilities demand low, predictable LCoE and tailored PPAs; 2024–25 benchmarks (EU onshore LCOE 30–50 EUR/MWh; Nord Pool avg ~40 EUR/MWh; auction wins 20–35 EUR/MWh) force Eolus to cut capex/O&M or accept thin EBIT (mid-single digits) or take merchant risk.

| Buyer | Key 2024–25 metrics | Impact on Eolus |

|---|---|---|

| Pension/Insurers | 5–7% renewables target (Nordic 2025) | Demand predictability, strict due diligence |

| Corporates | 60%+ procurement via long PPAs (2025); discounts 5–15% | Price pressure, tailored terms needed |

| Auctions/State | Winning bids 20–25 EUR/MWh (2024) | Caps revenue, forces thin margins |

What You See Is What You Get

Eolus Vind Porter's Five Forces Analysis

This preview is the exact Eolus Vind Porter's Five Forces analysis you'll receive upon purchase—no samples or placeholders, fully formatted and ready to download for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Eolus Vind faces moderate supplier power, intense rivalry among renewables developers, and growing buyer sophistication as green energy markets mature; barriers to entry are rising but technological change and policy shifts keep substitute threats meaningful. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Eolus Vind’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Wind Turbine Manufacturers

The high-capacity turbine market is concentrated: Vestas, Siemens Gamesa and GE held about 70–80% global market share in 2024–25 for >3 MW units, giving them strong bargaining power over Eolus Vind.

Eolus depends on supplier-specific blades, drivetrains and 15–25 year service contracts, so OEMs can dictate delivery schedules and spare-part pricing.

By late 2025 few suppliers can supply next-gen offshore 10+ MW and onshore 5+ MW units, keeping manufacturers’ pricing power high and capex uncertainty elevated for Eolus.

Raw Material Cost Volatility

Suppliers of steel, copper and rare earths now dictate Eolus Vind’s project margins: steel rose 28% and copper 35% in 2024, while neodymium prices jumped ~40% through 2024–2025, forcing index-linked procurement. Developers accepted pass-through clauses in 60–80% of 2024 supplier contracts, cutting Eolus’s ability to lock lower input costs. This means inflationary swings are directly transmitted to project budgets and EBITDA volatility.

Scarcity of Specialized Construction Services

The global shortage of specialized vessels and heavy‑lift rigs pushes suppliers’ power up: demand for offshore wind vessels rose 28% from 2020–2024 while available turbine‑installation vessels stayed flat, so Eolus competes with developers for scarce contractor slots and logistics capacity. Suppliers use that leverage to charge premiums—dayrates for jack‑up vessels climbed to €120k–€250k in 2024—and enforce tighter contract terms as EU renewables targets accelerate toward 2030.

Grid Connection Equipment Lead Times

Suppliers of high-voltage transformers and substation gear hit record backlogs into 2025—global grid upgrades pushed lead times to 18–36 months, according to industry reports.

Eolus Vind depends on a handful of specialized electrical firms to meet commissioning dates, creating supplier leverage over project timing and costs.

Long lead times and surge demand let suppliers prioritize large utilities over smaller independent developers, raising delivery risk and potential price pressure for Eolus.

- Typical lead times: 18–36 months by 2025

- Few specialized suppliers; high concentration

- Large utilities get priority; independents delayed

- Higher scheduling and price risk for Eolus

Landowner Leverage in Site Acquisition

Securing land rights is essential for Eolus Vind; private and municipal landowners thus hold significant leverage over site acquisition and timelines.

In Sweden prime wind sites fell by ~25% from 2015–2024, pushing average annual lease rates up about 18% to ~SEK 6–9k/ha in 2024, so owners demand higher rent or profit shares.

That local supplier power forces Eolus to offer enhanced lease terms or revenue-sharing to lock long-term exclusivity and avoid project delays.

- Prime-site scarcity: –25% (2015–2024)

- 2024 avg lease: ~SEK 6–9k/ha/yr

- Lease inflation: +18% vs 2015

- Response: higher profit-share or longer leases

Supply squeeze: OEM dominance & raw‑material spikes drive wind project costs up

Suppliers hold strong power: top OEMs (Vestas, Siemens Gamesa, GE) had ~70–80% share for >3 MW in 2024–25, steel +28% and copper +35% in 2024, neodymium +~40% through 2024–25, jack‑up dayrates €120k–€250k in 2024, HV lead times 18–36 months by 2025, Swedish leases ~SEK 6–9k/ha in 2024 (+18% vs 2015).

| Metric | Value |

|---|---|

| OEM share | 70–80% (2024–25) |

| Steel price | +28% (2024) |

| Copper price | +35% (2024) |

| Neodymium | +~40% (2024–25) |

| Jack‑up dayrates | €120k–€250k (2024) |

| HV lead times | 18–36 months (2025) |

| Sweden lease | SEK 6–9k/ha (2024) |

What is included in the product

Tailored exclusively for Eolus Vind, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape the company’s pricing power and long-term profitability.

A concise Porter's Five Forces one-sheet for Eolus Vind—quickly assess supplier, buyer, entrant, substitute, and rivalry pressures to streamline strategic decisions.

Customers Bargaining Power

Institutional Investor Requirements

Pension funds and insurers—core buyers for Eolus Vind—seek stable, long-term ESG assets; in 2025 Nordic pension funds target 5–7% portfolio allocation to renewables, raising expectations for predictability.

These sophisticated investors run deep due diligence and require transparent LCoE, P50/P90 yield models, and O&M risk metrics; missing items can cut valuations by 10–20% in buy-side models.

Because global allocators can redeploy capital quickly, Eolus faces strong buyer bargaining power: a 1% gap in IRR vs peers can shift multi‑year offtake demand to competitors.

Corporate Power Purchase Agreements

Utility-Scale Acquisition Strategies

Traditional utilities buy ready-to-build projects from developers like Eolus to meet 2030 RES targets; in Europe utilities acquired ~6.5 GW of wind/solar projects in 2024, tightening demand.

Utilities’ deep engineering and cost models let them estimate development costs to ±10% accuracy, capping Eolus’s premium negotiation room.

European utility consolidation—top 10 players control ~45% of generation—reduces buyer count and raises collective bargaining power over sellers.

Electricity Market Price Sensitivity

Customers push back when Eolus Vind’s Levelized Cost of Energy (LCOE) exceeds competing sources; 2024 EU onshore wind LCOE fell to about 30–50 EUR/MWh, so auction-winning bids cluster at the low end.

If market prices drop from oversupply or cheaper gas, buyers demand lower PPA rates; Nord Pool day-ahead averages fell to ~40 EUR/MWh in 2024, pressuring margins.

Eolus must cut capex/O&M and boost capacity factors; buyers favor the lowest-cost renewables in auctions where winning bids were often below 35 EUR/MWh in several 2024 EU tenders.

- 2024 EU onshore wind LCOE: ~30–50 EUR/MWh

- Nord Pool 2024 average: ~40 EUR/MWh

- Auction clearing bids often <35 EUR/MWh in 2024 tenders

Government and Regulatory Tender Processes

In many markets Eolus faces government-set renewable auctions where the state acts as proxy customer, and 2024 auction averages saw winning bids hit as low as 20–25 EUR/MWh in parts of Europe, capping project revenue.

These tenders are designed to drive prices down, so Eolus must chase thin margins—industry reports show wind developers' EBIT margins falling to mid-single digits in low-bid regimes.

That buyer power forces trade-offs: accept tight returns to secure volume or skip tenders and pursue merchant risk, which raises financing costs and time-to-market.

- Auctions cap price: 20–25 EUR/MWh observed (2024)

- Developer EBIT: mid-single digits in low-bid markets

- Choice: accept thin margins or assume merchant price risk

Buyers' leverage squeezes Eolus: cut costs, accept thin EBIT, or take merchant risk

Buyers hold strong leverage: pension funds, corporates, and utilities demand low, predictable LCoE and tailored PPAs; 2024–25 benchmarks (EU onshore LCOE 30–50 EUR/MWh; Nord Pool avg ~40 EUR/MWh; auction wins 20–35 EUR/MWh) force Eolus to cut capex/O&M or accept thin EBIT (mid-single digits) or take merchant risk.

| Buyer | Key 2024–25 metrics | Impact on Eolus |

|---|---|---|

| Pension/Insurers | 5–7% renewables target (Nordic 2025) | Demand predictability, strict due diligence |

| Corporates | 60%+ procurement via long PPAs (2025); discounts 5–15% | Price pressure, tailored terms needed |

| Auctions/State | Winning bids 20–25 EUR/MWh (2024) | Caps revenue, forces thin margins |

What You See Is What You Get

Eolus Vind Porter's Five Forces Analysis

This preview is the exact Eolus Vind Porter's Five Forces analysis you'll receive upon purchase—no samples or placeholders, fully formatted and ready to download for immediate use.