Eolus Vind PESTLE Analysis

Skip the Research. Get the Strategy.

Understand how regulatory shifts, market dynamics, and technological advances are shaping Eolus Vind’s growth prospects and risk profile—our concise PESTLE snapshot highlights the most critical external drivers. Purchase the full analysis to access detailed, actionable insights, sector benchmarks, and scenario-driven recommendations tailored for investors and strategists.

Political factors

European Green Deal and REPowerEU alignment

Eolus Vind benefits from the EU Green Deal and REPowerEU targets to cut fossil fuel use 55% by 2030 and accelerate renewables, securing stable long-term offtake and grid integration across Nordic-Baltic markets where wind & solar share rose to ~40% of generation in 2024; Eolus uses these mandates to obtain priority permitting and inclusion in national energy plans, supporting its pipeline valued at SEK ~6.5bn (2024 estimate) for onshore wind and solar projects.

Geopolitical energy security priorities

Following the 2021–22 energy crisis, Northern European governments treat renewables as national security: by 2025 EU wind capacity targets rose 28% vs 2020 and Sweden aimed for 100% fossil-free electricity by 2040, accelerating permitting and subsidies for projects that cut gas imports.

States fast-track capacity additions—Nordic permitting times shortened by ~20% in 2023–24—and direct financing grew: EU renewable OPEX/CAPEX support exceeded €45bn in 2024, lowering deployment barriers.

Eolus Vind, with ~2.2 GW project pipeline in Scandinavia and market cap ~SEK 6.5bn (2025), is positioned as a domestic developer supporting regional energy autonomy and reduced exposure to volatile global gas prices.

Permitting process reforms and streamlining

Political pressure to meet 2030 EU climate targets has driven reforms cutting permitting times for wind projects by up to 40% in some regions; Sweden and Poland report average permitting reductions from ~4.5 years to ~2.7 years 2021–2024. Many jurisdictions where Eolus operates now use one-stop-shop procedures, reducing approval touchpoints by 30–50% and lowering development risk and average capex delay costs—improving IRR visibility and shortening lead times to commissioning.

Nationalistic industrial policies and subsidies

European states increased renewable subsidies to record levels in 2024: EU member state aid approvals for green projects rose 22% YoY, with local content clauses in 9 major schemes (Germany, France, Spain, Poland, Italy, Sweden, Netherlands, Norway, Portugal) affecting turbine and panel sourcing.

For Eolus Vind, subsidy-driven margins improved—average project IRR uplifts of 150–300 bps—but procurement complexity and tariff risk rose as 60–75% of suppliers face localization expectations in key markets.

Eolus must adapt contracts and supply-chain hedges to preserve profitability and comply with shifting rules; failure to localize can delay projects and forfeit subsidies, impacting cash flows.

- 2024 EU green aid approvals +22% YoY

- 9 countries with local content rules

- IRR uplift +150–300 bps from subsidies

- 60–75% suppliers subject to localization

Cross-border energy infrastructure cooperation

Political agreements among Baltic Sea nations, including the 2024 Baltic Energy Market Interconnection Plan updates, are accelerating interconnected offshore/onshore grids that support Eolus Vind projects by enabling cross-border flows of up to 10–15 GW of additional capacity regionally.

These partnerships increase market liquidity—Nord Pool reported 2024 intraday volume growth of ~12%—improving price discovery for Eolus-generated power and potentially lifting realized merchant revenues.

Stable political frameworks are critical: multi-year transmission contracts and EU joint funding (EU grants €1.5bn+ for Baltic grid projects in 2024–25) reduce export risk and underpin long-term project bankability.

- Cross-border capacity: 10–15 GW potential

- Market liquidity: Nord Pool intraday +12% (2024)

- EU funding: €1.5bn+ for Baltic grids (2024–25)

Eolus set to accelerate: SEK 6.5bn pipeline, faster permits, Baltic grid boosts liquidity

Eolus benefits from EU Green Deal/REPowerEU, faster permitting (‑40% in some regions to ~2.7y) and record aid (+22% YoY 2024), boosting a SEK ~6.5bn pipeline (~2.2 GW); local content rules in 9 countries and supplier localization (60–75%) raise procurement risk; Baltic grid funding €1.5bn+ (2024–25) and 10–15 GW cross‑border capacity increase market liquidity (Nord Pool intraday +12% 2024).

| Metric | Value |

|---|---|

| Pipeline value (2024) | SEK ~6.5bn |

| Pipeline capacity | ~2.2 GW |

| Permitting reduction | up to 40% (to ~2.7y) |

| EU green aid 2024 | +22% YoY |

| Local content countries | 9 |

| Baltic grid funding | €1.5bn+ |

| Cross‑border capacity | 10–15 GW |

| Nord Pool intraday growth | +12% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Eolus Vind—backed by current data and regional market/regulatory dynamics—to identify risks, opportunities, and forward-looking scenarios for executives, investors, and strategists, delivered in clean, actionable format ready for business plans, pitch decks, and funding discussions.

Concise PESTLE summary tailored for Eolus Vind that highlights regulatory, market, and technological risks and opportunities for quick inclusion in presentations or strategy sessions.

Economic factors

Interest rate environment and capital costs

As a capital-intensive wind developer, Eolus Vind is highly sensitive to debt costs and investor discount rates; Sweden's 2024 long-term mortgage rate rose to about 3.5% and ECB rates held at 4.0% in 2025, which can compress project margins and reduce resale valuations by several percentage points. Eolus mitigates this via diversified financing—bank debt, green bonds and tax equity—and a flexible pipeline allowing project timing adjustments to counter rising capital costs.

Inflationary pressure on supply chain costs

Rising prices for steel (up ~25% year-on-year in 2024) and copper (up ~18% in 2024) have pushed wind/solar capex for developers like Eolus Vind by an estimated 10–15%, while specialized components face lead-time premiums; Eolus must balance fixed-price supplier contracts against variable logistics and labor inflation (global labor costs up ~6% in 2024) to protect IRRs; proactive procurement and hedging kept recent project margins within targeted ranges despite inflationary headwinds.

Electricity price volatility and PPA markets

The shift toward merchant exposure raises Eolus Vind’s sensitivity to wholesale price swings—Nord Pool day-ahead prices ranged €50–€120/MWh in 2024—so Eolus secures long-term PPAs (often 10–15 years) with corporates to lock revenues; these contracts boost project IRR predictability and were cited as key to achieving >80% debt financing coverage in recent institutional asset sales, enhancing bankability amid market volatility.

Currency exchange rate fluctuations

Operating across Europe and the US exposes Eolus to SEK/EUR/USD FX risk; in 2024 around 35% of project costs were invoiced in EUR/USD, amplifying exposure when SEK weakened ~6% vs EUR (2023–24).

FX moves affect imported turbine and inverter costs and consolidated earnings; a 5% SEK decline can raise capex by several percent per project.

The company uses forwards and swaps to hedge development-phase exposures, covering a substantial portion of forecasted cash flows to stabilize the balance sheet.

- ~35% project costs in EUR/USD (2024)

- SEK weakened ~6% vs EUR (2023–24)

- Hedging via forwards/swaps covering major development cash flows

Asset divestment and secondary market liquidity

Eolus Vind sells completed or ready-to-build wind projects to institutional buyers; in 2024 global green bond issuance hit about USD 600bn, supporting demand from pension funds and insurers.

However, secondary market liquidity is tied to financial conditions—2024 credit spreads widened at times, reducing transaction volumes and slowing exits.

A liquid secondary market lets Eolus recycle capital; in 2023 Eolus reported divestment-driven cash inflows enabling new project launches.

- Institutional demand strong: ~USD 600bn green issuance (2024)

- Liquidity sensitive to credit spreads and market stress

- Divestments fund new developments and growth

Eolus weathers rising rates, commodity inflation and FX with hedges, PPAs and green-bond demand

Eolus is sensitive to rising capital costs, commodity inflation and FX; 2024–25: Sweden mortgage ~3.5%, ECB ~4.0%, steel +25%, copper +18%, labor +6%, Nord Pool €50–€120/MWh, ~35% costs in EUR/USD, SEK -6% vs EUR. Hedging, diversified financing, PPAs and robust secondary demand (global green bonds ≈USD600bn in 2024) support resilience.

| Metric | 2024–25 |

|---|---|

| Sweden mortgage | ≈3.5% |

| ECB rate | ≈4.0% |

| Steel/copper | +25% / +18% |

| Nord Pool | €50–€120/MWh |

| EUR/USD invoicing | ≈35% |

| Green bonds | ≈USD600bn |

Preview Before You Purchase

Eolus Vind PESTLE Analysis

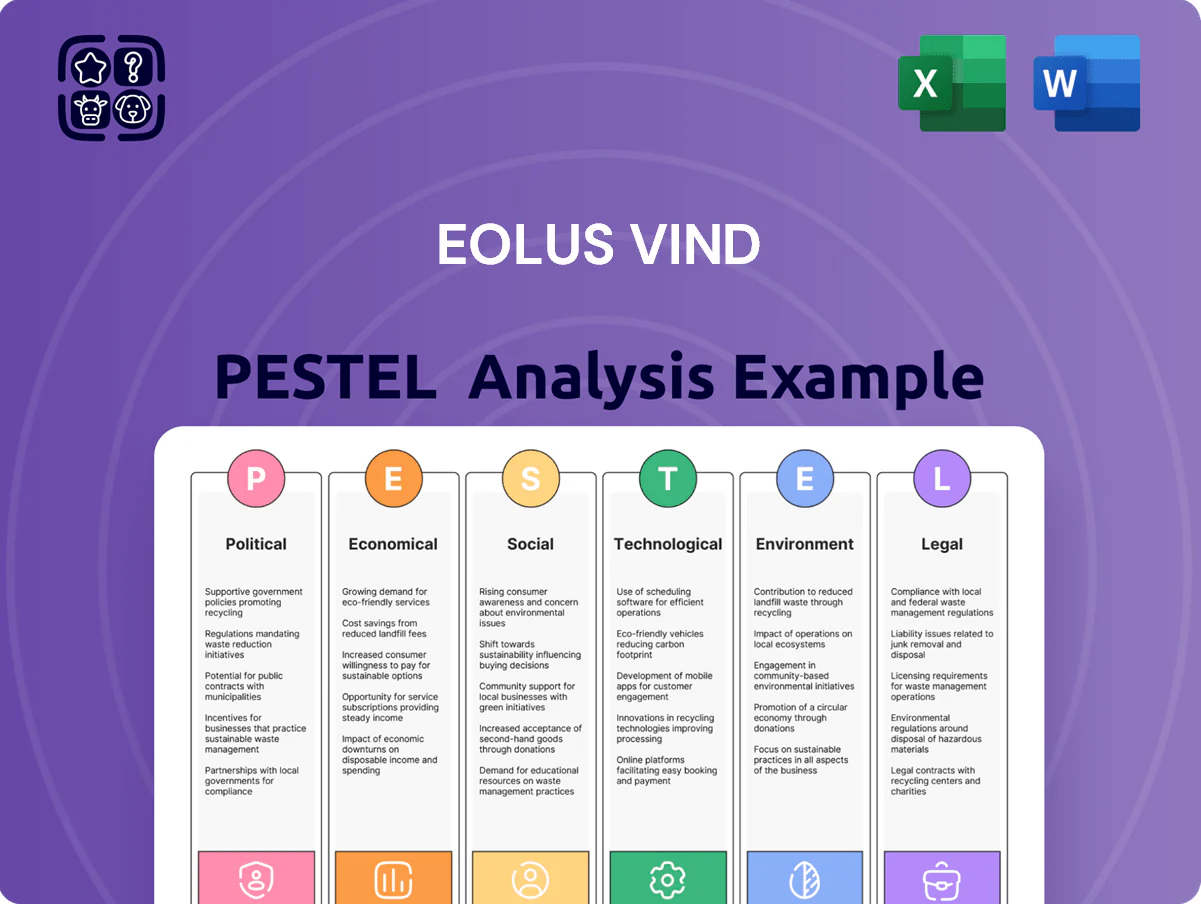

The preview shown here is the exact Eolus Vind PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This screenshot reflects the real file with complete content and no placeholders. After payment you’ll instantly download the same document as displayed, with identical layout, insights, and analysis. What you see is what you’ll own.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Understand how regulatory shifts, market dynamics, and technological advances are shaping Eolus Vind’s growth prospects and risk profile—our concise PESTLE snapshot highlights the most critical external drivers. Purchase the full analysis to access detailed, actionable insights, sector benchmarks, and scenario-driven recommendations tailored for investors and strategists.

Political factors

European Green Deal and REPowerEU alignment

Eolus Vind benefits from the EU Green Deal and REPowerEU targets to cut fossil fuel use 55% by 2030 and accelerate renewables, securing stable long-term offtake and grid integration across Nordic-Baltic markets where wind & solar share rose to ~40% of generation in 2024; Eolus uses these mandates to obtain priority permitting and inclusion in national energy plans, supporting its pipeline valued at SEK ~6.5bn (2024 estimate) for onshore wind and solar projects.

Geopolitical energy security priorities

Following the 2021–22 energy crisis, Northern European governments treat renewables as national security: by 2025 EU wind capacity targets rose 28% vs 2020 and Sweden aimed for 100% fossil-free electricity by 2040, accelerating permitting and subsidies for projects that cut gas imports.

States fast-track capacity additions—Nordic permitting times shortened by ~20% in 2023–24—and direct financing grew: EU renewable OPEX/CAPEX support exceeded €45bn in 2024, lowering deployment barriers.

Eolus Vind, with ~2.2 GW project pipeline in Scandinavia and market cap ~SEK 6.5bn (2025), is positioned as a domestic developer supporting regional energy autonomy and reduced exposure to volatile global gas prices.

Permitting process reforms and streamlining

Political pressure to meet 2030 EU climate targets has driven reforms cutting permitting times for wind projects by up to 40% in some regions; Sweden and Poland report average permitting reductions from ~4.5 years to ~2.7 years 2021–2024. Many jurisdictions where Eolus operates now use one-stop-shop procedures, reducing approval touchpoints by 30–50% and lowering development risk and average capex delay costs—improving IRR visibility and shortening lead times to commissioning.

Nationalistic industrial policies and subsidies

European states increased renewable subsidies to record levels in 2024: EU member state aid approvals for green projects rose 22% YoY, with local content clauses in 9 major schemes (Germany, France, Spain, Poland, Italy, Sweden, Netherlands, Norway, Portugal) affecting turbine and panel sourcing.

For Eolus Vind, subsidy-driven margins improved—average project IRR uplifts of 150–300 bps—but procurement complexity and tariff risk rose as 60–75% of suppliers face localization expectations in key markets.

Eolus must adapt contracts and supply-chain hedges to preserve profitability and comply with shifting rules; failure to localize can delay projects and forfeit subsidies, impacting cash flows.

- 2024 EU green aid approvals +22% YoY

- 9 countries with local content rules

- IRR uplift +150–300 bps from subsidies

- 60–75% suppliers subject to localization

Cross-border energy infrastructure cooperation

Political agreements among Baltic Sea nations, including the 2024 Baltic Energy Market Interconnection Plan updates, are accelerating interconnected offshore/onshore grids that support Eolus Vind projects by enabling cross-border flows of up to 10–15 GW of additional capacity regionally.

These partnerships increase market liquidity—Nord Pool reported 2024 intraday volume growth of ~12%—improving price discovery for Eolus-generated power and potentially lifting realized merchant revenues.

Stable political frameworks are critical: multi-year transmission contracts and EU joint funding (EU grants €1.5bn+ for Baltic grid projects in 2024–25) reduce export risk and underpin long-term project bankability.

- Cross-border capacity: 10–15 GW potential

- Market liquidity: Nord Pool intraday +12% (2024)

- EU funding: €1.5bn+ for Baltic grids (2024–25)

Eolus set to accelerate: SEK 6.5bn pipeline, faster permits, Baltic grid boosts liquidity

Eolus benefits from EU Green Deal/REPowerEU, faster permitting (‑40% in some regions to ~2.7y) and record aid (+22% YoY 2024), boosting a SEK ~6.5bn pipeline (~2.2 GW); local content rules in 9 countries and supplier localization (60–75%) raise procurement risk; Baltic grid funding €1.5bn+ (2024–25) and 10–15 GW cross‑border capacity increase market liquidity (Nord Pool intraday +12% 2024).

| Metric | Value |

|---|---|

| Pipeline value (2024) | SEK ~6.5bn |

| Pipeline capacity | ~2.2 GW |

| Permitting reduction | up to 40% (to ~2.7y) |

| EU green aid 2024 | +22% YoY |

| Local content countries | 9 |

| Baltic grid funding | €1.5bn+ |

| Cross‑border capacity | 10–15 GW |

| Nord Pool intraday growth | +12% (2024) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Eolus Vind—backed by current data and regional market/regulatory dynamics—to identify risks, opportunities, and forward-looking scenarios for executives, investors, and strategists, delivered in clean, actionable format ready for business plans, pitch decks, and funding discussions.

Concise PESTLE summary tailored for Eolus Vind that highlights regulatory, market, and technological risks and opportunities for quick inclusion in presentations or strategy sessions.

Economic factors

Interest rate environment and capital costs

As a capital-intensive wind developer, Eolus Vind is highly sensitive to debt costs and investor discount rates; Sweden's 2024 long-term mortgage rate rose to about 3.5% and ECB rates held at 4.0% in 2025, which can compress project margins and reduce resale valuations by several percentage points. Eolus mitigates this via diversified financing—bank debt, green bonds and tax equity—and a flexible pipeline allowing project timing adjustments to counter rising capital costs.

Inflationary pressure on supply chain costs

Rising prices for steel (up ~25% year-on-year in 2024) and copper (up ~18% in 2024) have pushed wind/solar capex for developers like Eolus Vind by an estimated 10–15%, while specialized components face lead-time premiums; Eolus must balance fixed-price supplier contracts against variable logistics and labor inflation (global labor costs up ~6% in 2024) to protect IRRs; proactive procurement and hedging kept recent project margins within targeted ranges despite inflationary headwinds.

Electricity price volatility and PPA markets

The shift toward merchant exposure raises Eolus Vind’s sensitivity to wholesale price swings—Nord Pool day-ahead prices ranged €50–€120/MWh in 2024—so Eolus secures long-term PPAs (often 10–15 years) with corporates to lock revenues; these contracts boost project IRR predictability and were cited as key to achieving >80% debt financing coverage in recent institutional asset sales, enhancing bankability amid market volatility.

Currency exchange rate fluctuations

Operating across Europe and the US exposes Eolus to SEK/EUR/USD FX risk; in 2024 around 35% of project costs were invoiced in EUR/USD, amplifying exposure when SEK weakened ~6% vs EUR (2023–24).

FX moves affect imported turbine and inverter costs and consolidated earnings; a 5% SEK decline can raise capex by several percent per project.

The company uses forwards and swaps to hedge development-phase exposures, covering a substantial portion of forecasted cash flows to stabilize the balance sheet.

- ~35% project costs in EUR/USD (2024)

- SEK weakened ~6% vs EUR (2023–24)

- Hedging via forwards/swaps covering major development cash flows

Asset divestment and secondary market liquidity

Eolus Vind sells completed or ready-to-build wind projects to institutional buyers; in 2024 global green bond issuance hit about USD 600bn, supporting demand from pension funds and insurers.

However, secondary market liquidity is tied to financial conditions—2024 credit spreads widened at times, reducing transaction volumes and slowing exits.

A liquid secondary market lets Eolus recycle capital; in 2023 Eolus reported divestment-driven cash inflows enabling new project launches.

- Institutional demand strong: ~USD 600bn green issuance (2024)

- Liquidity sensitive to credit spreads and market stress

- Divestments fund new developments and growth

Eolus weathers rising rates, commodity inflation and FX with hedges, PPAs and green-bond demand

Eolus is sensitive to rising capital costs, commodity inflation and FX; 2024–25: Sweden mortgage ~3.5%, ECB ~4.0%, steel +25%, copper +18%, labor +6%, Nord Pool €50–€120/MWh, ~35% costs in EUR/USD, SEK -6% vs EUR. Hedging, diversified financing, PPAs and robust secondary demand (global green bonds ≈USD600bn in 2024) support resilience.

| Metric | 2024–25 |

|---|---|

| Sweden mortgage | ≈3.5% |

| ECB rate | ≈4.0% |

| Steel/copper | +25% / +18% |

| Nord Pool | €50–€120/MWh |

| EUR/USD invoicing | ≈35% |

| Green bonds | ≈USD600bn |

Preview Before You Purchase

Eolus Vind PESTLE Analysis

The preview shown here is the exact Eolus Vind PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This screenshot reflects the real file with complete content and no placeholders. After payment you’ll instantly download the same document as displayed, with identical layout, insights, and analysis. What you see is what you’ll own.