Eolus Vind SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Eolus Vind faces strong sector tailwinds from accelerating renewable demand and a solid project pipeline, yet it must navigate supply-chain pressures and regulatory variability; our full SWOT unpacks these dynamics with financial context, competitive mapping, and actionable strategy. Purchase the complete analysis to receive a professionally formatted Word report and editable Excel tools for investment, planning, or pitching.

Strengths

Proven Full Lifecycle Expertise

Eolus Vind runs full lifecycle development—from site ID and permitting to construction and divestment—cutting reliance on contractors and keeping quality control; in 2024 Eolus delivered 1,150 MW in projects and reported EUR 132.4m revenue, capturing development-to-sale margins and recurring earnings; owning the value chain lets Eolus realize higher IRRs (company-stated target >10%) and reduce schedule risk versus pure-play EPC firms.

Geographic Diversification across Northern Europe and US

Eolus Vind has broadened operations from Sweden into Norway, Finland, the Baltics and the US, giving a project pipeline of about 5.2 GW under development as of Dec 31, 2025 and backing a 2025 revenue of ~SEK 1.6bn;

This spread cuts exposure to single-market regulation or local low-wind years, smoothing generation and cashflow volatility across climates and grids;

Access to diverse markets also raises project conversion odds and supports target growth of 600–800 MW annual installations through 2027.

Asset-Light Business Model

Eolus Vind develops and builds wind farms to sell to long-term investors while keeping management contracts, letting it recycle capital fast—Eolus sold projects totaling ~1.1 GW in 2024 and reported SEK 1.6bn in divestment proceeds that year. This asset-light approach avoids heavy operating debt, keeps net debt/EBITDA lower (0.9x at end-2024), and gives a flexible balance sheet that can adapt to changing power prices and permitting delays.

Strong Track Record in Asset Management

Eolus manages operations and administration for roughly 1.6 GW of developed capacity, earning recurring service fees that smooth revenues versus sporadic project sales; in 2024 service income accounted for about 18% of group revenues, reducing volatility from divestment timing.

These services deepen ties with institutional investors and infrastructure funds, supporting repeat deals and long-term O&M contracts that boost lifetime asset returns and lower investor financing costs.

- 1.6 GW under management (approx, 2024)

- Service revenue ≈18% of 2024 group revenues

- Recurring fees reduce divestment volatility

- Strengthens relations with institutional investors

Deep Regulatory and Permitting Knowledge

- 7.4 GW pipeline (2025)

- Decades in Nordic permitting

- Faster FID, higher project IRR

Eolus Vind: 1.15GW delivered, €132m revenue, 5.2–7.4GW pipeline, asset-light growth

Eolus Vind runs full lifecycle development and O&M, delivered 1,150 MW in 2024 with EUR 132.4m revenue, and targets >10% IRR; diversified across Sweden, Norway, Finland, Baltics and US with ~5.2 GW pipeline (Dec 31, 2025) and 7.4 GW broader pipeline (2025); asset-light model drove SEK 1.6bn divestments and net debt/EBITDA 0.9x (end-2024), while 1.6 GW under management generated ~18% of 2024 revenue.

| Metric | Value |

|---|---|

| 2024 delivered | 1,150 MW |

| 2024 revenue | EUR 132.4m |

| Pipeline (Dec 31, 2025) | 5.2 GW |

| Broader pipeline (2025) | 7.4 GW |

| Divestments 2024 | SEK 1.6bn |

| Net debt/EBITDA | 0.9x (end-2024) |

| Under management | 1.6 GW |

| Service revenue | ~18% (2024) |

What is included in the product

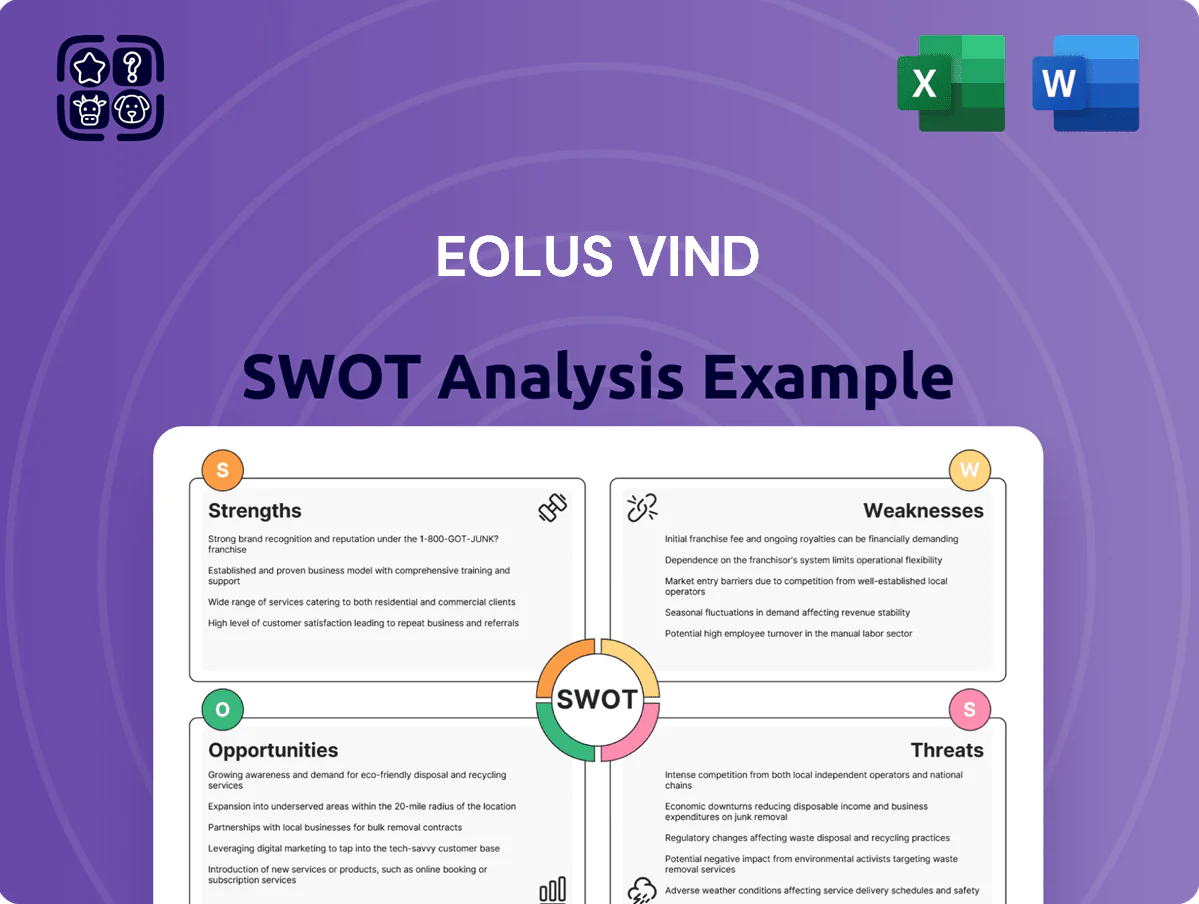

Provides a concise SWOT overview of Eolus Vind, highlighting its operational strengths, internal weaknesses, external growth opportunities in renewables, and market and regulatory threats shaping its strategic position.

Provides a concise SWOT matrix for Eolus Vind to quickly align wind-power strategy and prioritize investments.

Weaknesses

High Dependency on Project Timelines

The company’s earnings swing with project handovers: Eolus Vind recognized SEK 1.2bn revenue in 2024 largely tied to three completed projects, causing quarterly EBITDA to vary by ±35% year-over-year; permitting or construction delays routinely shift revenue into later periods. Delays beyond company control—e.g., Sweden grid wait times averaging 9–14 months in 2023–24—make near-term guidance volatile and complicate cash-flow planning for investors.

Exposure to Interest Rate Fluctuations

Eolus Vind, as a developer of capital-intensive wind projects, is highly sensitive to cost of capital: a 100‑bp rise in Nordic corporate borrowing costs (about 2024‑25 trend) can cut project IRRs by ~1 percentage point, making assets less attractive to buyers.

Higher global rates have already delayed some FID (final investment decisions); institutional partners often pause allocations when yields rise, compressing Eolus’s developer margins and sale timing.

Although asset-light, Eolus relies on customers whose buying power links to global credit spreads; widening bank lending spreads (e.g., EUR corporate OAS +40–60bp in 2024) lowers deal flow and bid prices.

Limited Control Over Grid Connection Delays

Eolus depends on national and regional grid operators for timely connections, and in 2024 grid congestion in key markets like Sweden and Poland delayed ~18% of planned commissions, per industry grid reports. These delays can push back revenue recognition for ready-to-build or finished assets, deferring expected cash flows—Eolus reported a SEK 220m carryover in 2024 tied to connection timing. The lack of control over grid upgrades raises execution risk and can increase financing costs if projects sit idle past contracted dates.

Concentration in Wind Power Technology

Eolus Vind's revenue and project pipeline remain dominated by onshore wind—about 78% of its 2024 project portfolio capacity (≈1.2 GW) and roughly 70% of 2024 revenues, despite pilot solar and battery projects launched in 2023–24.

This concentration raises exposure to wind-specific regulatory changes and local opposition; a 2023 Swedish municipal permit rejection halted a 120 MW project, highlighting vulnerability.

Scaling a balanced tech mix is nascent: solar/battery projects represent <15% of pipeline capacity and need multi-year ramp-up to materially diversify risk.

- 78% pipeline: onshore wind (~1.2 GW)

- ~70% 2024 revenue from wind

- Solar/battery <15% pipeline

- Permit denial: 120 MW project (2023)

Sensitivity to Power Price Volatility

Project valuations at Eolus often rely on long-term power purchase agreements or projected wholesale prices; a 30% drop in Nordic baseload prices in 2023 cut projected IRRs for some onshore deals below target thresholds, squeezing sale prices.

That sensitivity makes divestment timing critical and creates market risk that developers can’t fully hedge during permitting and construction, raising holding-cost exposure.

- Valuation tied to PPA/price forecasts

- Wholesale price swings (eg −30% in 2023) hit IRRs

- Hard to fully hedge in development

- Higher holding costs and sale-timing risk

Eolus at risk: project delays, grid carryover, wind concentration & price sensitivity

Eolus faces revenue volatility from project handovers and grid delays (SEK 1.2bn 2024 revenue tied to three projects; SEK 220m carryover), high sensitivity to cost of capital (100bp → ~1pp IRR hit), concentration in onshore wind (78% pipeline, ~70% 2024 revenue), limited solar/battery scale (<15% pipeline), and market-price exposure (Nordic baseload −30% in 2023).

| Metric | 2023–24 |

|---|---|

| Revenue tied to project handovers | SEK 1.2bn (2024) |

| Carryover due to grid | SEK 220m (2024) |

| Pipeline: onshore wind | 78% (~1.2 GW) |

| Revenue from wind | ~70% (2024) |

| Solar/battery pipeline | <15% |

| Nordic baseload move | −30% (2023) |

Full Version Awaits

Eolus Vind SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You’re viewing a live preview of the real file—professional, structured, and ready to use immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Eolus Vind faces strong sector tailwinds from accelerating renewable demand and a solid project pipeline, yet it must navigate supply-chain pressures and regulatory variability; our full SWOT unpacks these dynamics with financial context, competitive mapping, and actionable strategy. Purchase the complete analysis to receive a professionally formatted Word report and editable Excel tools for investment, planning, or pitching.

Strengths

Proven Full Lifecycle Expertise

Eolus Vind runs full lifecycle development—from site ID and permitting to construction and divestment—cutting reliance on contractors and keeping quality control; in 2024 Eolus delivered 1,150 MW in projects and reported EUR 132.4m revenue, capturing development-to-sale margins and recurring earnings; owning the value chain lets Eolus realize higher IRRs (company-stated target >10%) and reduce schedule risk versus pure-play EPC firms.

Geographic Diversification across Northern Europe and US

Eolus Vind has broadened operations from Sweden into Norway, Finland, the Baltics and the US, giving a project pipeline of about 5.2 GW under development as of Dec 31, 2025 and backing a 2025 revenue of ~SEK 1.6bn;

This spread cuts exposure to single-market regulation or local low-wind years, smoothing generation and cashflow volatility across climates and grids;

Access to diverse markets also raises project conversion odds and supports target growth of 600–800 MW annual installations through 2027.

Asset-Light Business Model

Eolus Vind develops and builds wind farms to sell to long-term investors while keeping management contracts, letting it recycle capital fast—Eolus sold projects totaling ~1.1 GW in 2024 and reported SEK 1.6bn in divestment proceeds that year. This asset-light approach avoids heavy operating debt, keeps net debt/EBITDA lower (0.9x at end-2024), and gives a flexible balance sheet that can adapt to changing power prices and permitting delays.

Strong Track Record in Asset Management

Eolus manages operations and administration for roughly 1.6 GW of developed capacity, earning recurring service fees that smooth revenues versus sporadic project sales; in 2024 service income accounted for about 18% of group revenues, reducing volatility from divestment timing.

These services deepen ties with institutional investors and infrastructure funds, supporting repeat deals and long-term O&M contracts that boost lifetime asset returns and lower investor financing costs.

- 1.6 GW under management (approx, 2024)

- Service revenue ≈18% of 2024 group revenues

- Recurring fees reduce divestment volatility

- Strengthens relations with institutional investors

Deep Regulatory and Permitting Knowledge

- 7.4 GW pipeline (2025)

- Decades in Nordic permitting

- Faster FID, higher project IRR

Eolus Vind: 1.15GW delivered, €132m revenue, 5.2–7.4GW pipeline, asset-light growth

Eolus Vind runs full lifecycle development and O&M, delivered 1,150 MW in 2024 with EUR 132.4m revenue, and targets >10% IRR; diversified across Sweden, Norway, Finland, Baltics and US with ~5.2 GW pipeline (Dec 31, 2025) and 7.4 GW broader pipeline (2025); asset-light model drove SEK 1.6bn divestments and net debt/EBITDA 0.9x (end-2024), while 1.6 GW under management generated ~18% of 2024 revenue.

| Metric | Value |

|---|---|

| 2024 delivered | 1,150 MW |

| 2024 revenue | EUR 132.4m |

| Pipeline (Dec 31, 2025) | 5.2 GW |

| Broader pipeline (2025) | 7.4 GW |

| Divestments 2024 | SEK 1.6bn |

| Net debt/EBITDA | 0.9x (end-2024) |

| Under management | 1.6 GW |

| Service revenue | ~18% (2024) |

What is included in the product

Provides a concise SWOT overview of Eolus Vind, highlighting its operational strengths, internal weaknesses, external growth opportunities in renewables, and market and regulatory threats shaping its strategic position.

Provides a concise SWOT matrix for Eolus Vind to quickly align wind-power strategy and prioritize investments.

Weaknesses

High Dependency on Project Timelines

The company’s earnings swing with project handovers: Eolus Vind recognized SEK 1.2bn revenue in 2024 largely tied to three completed projects, causing quarterly EBITDA to vary by ±35% year-over-year; permitting or construction delays routinely shift revenue into later periods. Delays beyond company control—e.g., Sweden grid wait times averaging 9–14 months in 2023–24—make near-term guidance volatile and complicate cash-flow planning for investors.

Exposure to Interest Rate Fluctuations

Eolus Vind, as a developer of capital-intensive wind projects, is highly sensitive to cost of capital: a 100‑bp rise in Nordic corporate borrowing costs (about 2024‑25 trend) can cut project IRRs by ~1 percentage point, making assets less attractive to buyers.

Higher global rates have already delayed some FID (final investment decisions); institutional partners often pause allocations when yields rise, compressing Eolus’s developer margins and sale timing.

Although asset-light, Eolus relies on customers whose buying power links to global credit spreads; widening bank lending spreads (e.g., EUR corporate OAS +40–60bp in 2024) lowers deal flow and bid prices.

Limited Control Over Grid Connection Delays

Eolus depends on national and regional grid operators for timely connections, and in 2024 grid congestion in key markets like Sweden and Poland delayed ~18% of planned commissions, per industry grid reports. These delays can push back revenue recognition for ready-to-build or finished assets, deferring expected cash flows—Eolus reported a SEK 220m carryover in 2024 tied to connection timing. The lack of control over grid upgrades raises execution risk and can increase financing costs if projects sit idle past contracted dates.

Concentration in Wind Power Technology

Eolus Vind's revenue and project pipeline remain dominated by onshore wind—about 78% of its 2024 project portfolio capacity (≈1.2 GW) and roughly 70% of 2024 revenues, despite pilot solar and battery projects launched in 2023–24.

This concentration raises exposure to wind-specific regulatory changes and local opposition; a 2023 Swedish municipal permit rejection halted a 120 MW project, highlighting vulnerability.

Scaling a balanced tech mix is nascent: solar/battery projects represent <15% of pipeline capacity and need multi-year ramp-up to materially diversify risk.

- 78% pipeline: onshore wind (~1.2 GW)

- ~70% 2024 revenue from wind

- Solar/battery <15% pipeline

- Permit denial: 120 MW project (2023)

Sensitivity to Power Price Volatility

Project valuations at Eolus often rely on long-term power purchase agreements or projected wholesale prices; a 30% drop in Nordic baseload prices in 2023 cut projected IRRs for some onshore deals below target thresholds, squeezing sale prices.

That sensitivity makes divestment timing critical and creates market risk that developers can’t fully hedge during permitting and construction, raising holding-cost exposure.

- Valuation tied to PPA/price forecasts

- Wholesale price swings (eg −30% in 2023) hit IRRs

- Hard to fully hedge in development

- Higher holding costs and sale-timing risk

Eolus at risk: project delays, grid carryover, wind concentration & price sensitivity

Eolus faces revenue volatility from project handovers and grid delays (SEK 1.2bn 2024 revenue tied to three projects; SEK 220m carryover), high sensitivity to cost of capital (100bp → ~1pp IRR hit), concentration in onshore wind (78% pipeline, ~70% 2024 revenue), limited solar/battery scale (<15% pipeline), and market-price exposure (Nordic baseload −30% in 2023).

| Metric | 2023–24 |

|---|---|

| Revenue tied to project handovers | SEK 1.2bn (2024) |

| Carryover due to grid | SEK 220m (2024) |

| Pipeline: onshore wind | 78% (~1.2 GW) |

| Revenue from wind | ~70% (2024) |

| Solar/battery pipeline | <15% |

| Nordic baseload move | −30% (2023) |

Full Version Awaits

Eolus Vind SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You’re viewing a live preview of the real file—professional, structured, and ready to use immediately after checkout.