Epic Systems PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, healthcare funding, and rapid tech innovation are reshaping Epic Systems' strategic landscape in our concise PESTLE snapshot; buy the full analysis to access detailed regulatory, economic, and environmental insights tailored for investors and strategists.

Political factors

Federal Interoperability Mandates

The US is enforcing TEFCA to expand nationwide health data sharing; OCR reported a 2024 TEFCA participation goal covering over 300 million patients, pressuring Epic to maintain compliance to enable interoperability across health systems.

Epic must update modules and interfaces to align with evolving TEFCA technical and contractual requirements or face enforcement actions and potential fines under HIPAA and the 21st Century Cures Act.

Noncompliance risks revenue loss and market share decline as agile competitors and FHIR-based startups—venture funding into digital health reached $15.3 billion in 2024—increase adoption among health systems seeking open data exchange.

Government Healthcare Spending

International Regulatory Expansion

As Epic expands in Europe and Asia it faces fragmented political landscapes and national health systems—EU digital health regulations and country-level procurement often favor local suppliers, creating entry barriers; for example, 47% of EU tenders in 2023 favored domestic firms.

Cybersecurity as National Security

The federal government treats healthcare infrastructure as a national security priority, increasing oversight of EHR vendors; in 2024 HHS announced enhanced cybersecurity requirements after healthcare breaches rose 45% since 2019.

Epic faces pressure to defend against state-sponsored attacks—health sector cyber incidents cost an average $10.1M per breach in 2023—forcing continuous investment in security.

Pending federal legislation seeks mandated protocols for EHRs, so Epic must outpace regulation to retain trust and large contracts with government health systems.

- Federal oversight rising; HHS 2024 mandates

- Healthcare breaches +45% since 2019; $10.1M average cost per breach (2023)

- Legislation pushing mandatory EHR security protocols

- Epic must invest continually to secure government partnerships

Public Health Data Integration

Political pushes after COVID-19 and CDC initiatives (eg 2024 Data Modernization Initiative funding of $1.1B) demand tighter EHR-public health integration; Epic, with ~33% US acute EHR market share and >250M patient records, is a focal point for these reforms.

Lawmakers expect Epic to adopt standardized reporting (FHIR/US Core) and face scrutiny—Congressional hearings and state-level legislation in 2024 increased oversight and transparency mandates tied to federal grants.

- Epic holds ~33% US hospital EHR market share and >250M patient records

- $1.1B CDC Data Modernization Initiative (2024) pushes integration

- Increased legislative oversight and transparency mandates in 2024

Epic faces TEFCA/FHIR, funding & cyber pressure across 33% US acute market

Federal TEFCA/HHS mandates (2024) force Epic to maintain TEFCA/FHIR compliance across ~33% US acute market and >250M records; Medicare/Medicaid budgets (~$900B/$700B in 2024) and $1.1B CDC Data Modernization funding raise integration demands; cyber threats (+45% breaches since 2019; $10.1M avg cost 2023) and EU/local procurement (47% domestic wins 2023) increase regulatory and market pressure.

| Metric | 2023–2024 |

|---|---|

| US acute market share | ~33% |

| Patient records | >250M |

| Medicare/Medicaid spend | $900B / $700B |

| CDC DMI funding | $1.1B |

| Digital health VC | $15.3B (2024) |

| Healthcare breaches rise | +45% since 2019; $10.1M avg |

| EU domestic tender bias | 47% (2023) |

What is included in the product

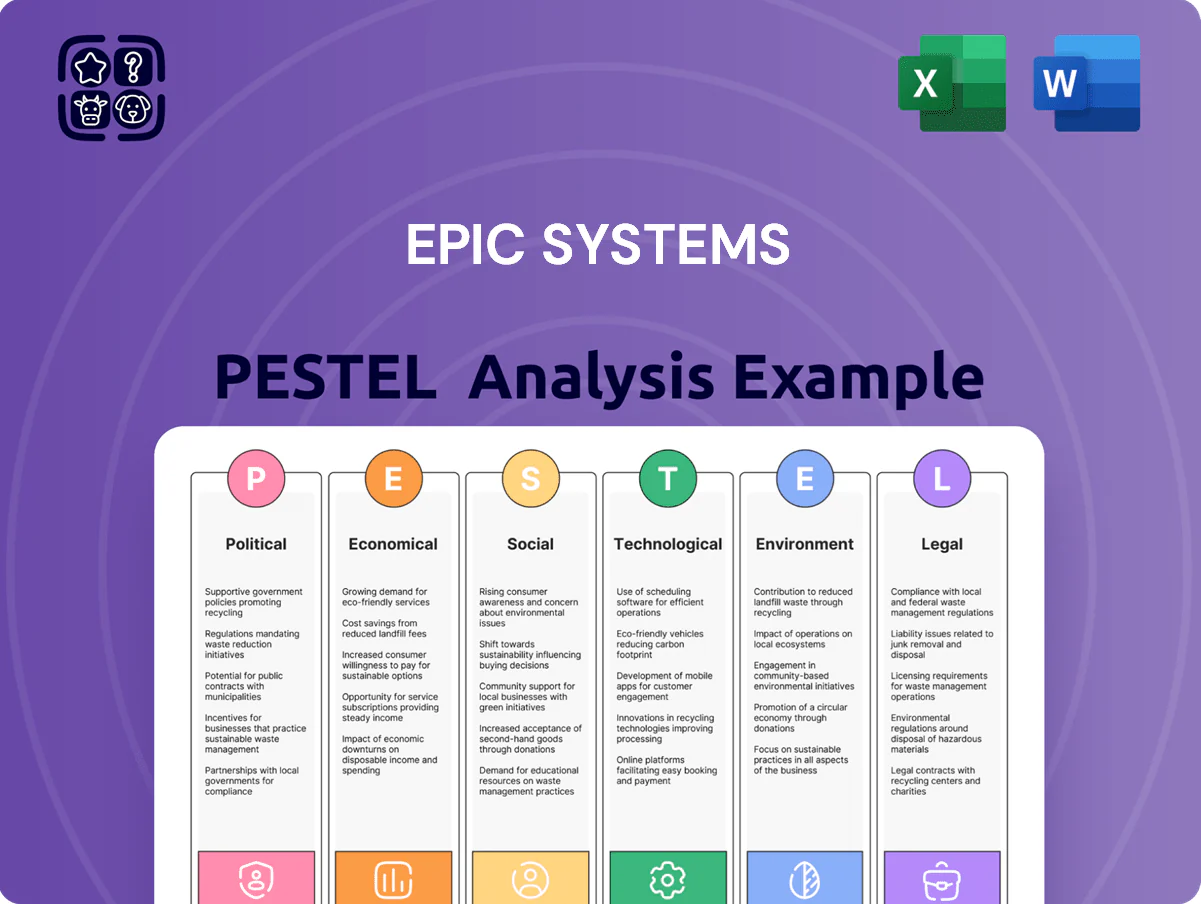

Explores how external macro-environmental factors uniquely affect Epic Systems across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

Provides a concise, visually segmented PESTLE snapshot of Epic Systems that can be dropped into presentations or shared across teams to streamline strategic discussions and risk assessment.

Economic factors

Healthcare Provider Consolidation

Consolidation of US hospitals—M&A volume reached roughly 725 transactions in 2024 and 2025 saw continued large-system deals—favors Epic as health systems standardize on one EHR; acquisitions of clinics by Epic-using systems typically trigger migrations, boosting Epic’s bookings and services revenue. Fewer independent buyers reduce addressable customers but increase contract size, reinforcing Epic’s enterprise market share (estimated >30% inpatient EHR market in 2024) and organic growth.

High Cost of Implementation

The significant capital expenditure to implement and maintain Epic systems—often $1–10 million for mid-sized hospitals per 2024 estimates—remains a major barrier for smaller or rural providers; total cost of ownership can exceed $20 million over a decade. Elevated U.S. base rates peaking near 5.5% in 2024–2025 increased financing costs, raising annual carrying costs by tens to hundreds of thousands per project. Epic must innovate pricing and offer modular, cloud or subscription options to broaden affordability across the healthcare economic spectrum.

Labor Shortages in IT

A persistent shortage of Epic-certified analysts and IT pros raises operational costs for Epic and its clients; US IT job openings hit 8.7M in 2024, and healthcare IT wages grew ~6–8% year-over-year, fueling wage inflation and hiring competition. Epic and partners face higher implementation TCO and must invest in training programs and automation—Epic reportedly expanded its training capacity by 20% in 2024—to lower long-term labor needs.

Global Inflationary Pressures

Global inflation raises data center energy and hardware costs—U.S. core PCE rose 3.5% YoY in 2024—pressuring Epic Systems’ operating expenses for servers, networking, and maintenance.

Epic’s recurring maintenance/support revenue cushions volatility, but higher input costs risk squeezing adjusted operating margins if price increases lag inflation.

Epic must calibrate pricing to cover rising costs while avoiding rate shocks for hospital clients facing constrained 2024–25 health budgets.

- 2024 U.S. core PCE +3.5% YoY

- Recurring maintenance stabilizes revenue

- Rising capex/opex from hardware and energy

- Pricing balance critical to retain budget-constrained clients

Subscription and Cloud Revenue Stability

The shift to cloud hosting and SaaS has given Epic more predictable recurring revenue versus legacy perpetual licenses, with cloud/subscription bookings rising to an estimated 65% of new contract value by end-2025 and recurring revenue representing roughly 70% of total revenue in 2024–25.

Investors value this stability: SaaS-like gross retention rates above 95% and multi-year contracts have improved free cash flow predictability and supported R&D investment, with Epic reportedly increasing R&D spend to around 12–14% of revenue by 2025.

- Recurring revenue dominance: ~70% of revenue (2024–25)

- New bookings: ~65% cloud/subscription by end-2025

- Gross retention: >95%

- R&D spend: ~12–14% of revenue (2025)

Epic dominates inpatient EHRs as cloud, costs, and labor squeeze smaller buyers

Consolidation and cloud shifts increased Epic’s enterprise share (>30% inpatient EHR 2024) and recurring revenue (~70% 2024–25), while high capex ($1–10M midsize, $20M TCO/decade) and 2024–25 rate-driven financing costs (US rates ~5.5%) pressure smaller buyers; labor scarcity (IT openings 8.7M 2024, wages +6–8%) and inflation (core PCE +3.5% 2024) raise opex, forcing pricing and modular SaaS offers to preserve margins.

| Metric | 2024–25 |

|---|---|

| Inpatient EHR share | >30% |

| Recurring rev | ~70% |

| Cloud bookings | ~65% new CV by end‑2025 |

| Mid HS capex | $1–10M |

| TCO/decade | ~$20M |

| US core PCE | +3.5% YoY (2024) |

| US rates | ~5.5% (2024–25) |

| IT openings | 8.7M (2024) |

Full Version Awaits

Epic Systems PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Epic Systems PESTLE Analysis provides concise legal, economic, social, technological, environmental, and political insights tailored to healthcare IT decision-makers. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders or surprises—just the final, professional file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, healthcare funding, and rapid tech innovation are reshaping Epic Systems' strategic landscape in our concise PESTLE snapshot; buy the full analysis to access detailed regulatory, economic, and environmental insights tailored for investors and strategists.

Political factors

Federal Interoperability Mandates

The US is enforcing TEFCA to expand nationwide health data sharing; OCR reported a 2024 TEFCA participation goal covering over 300 million patients, pressuring Epic to maintain compliance to enable interoperability across health systems.

Epic must update modules and interfaces to align with evolving TEFCA technical and contractual requirements or face enforcement actions and potential fines under HIPAA and the 21st Century Cures Act.

Noncompliance risks revenue loss and market share decline as agile competitors and FHIR-based startups—venture funding into digital health reached $15.3 billion in 2024—increase adoption among health systems seeking open data exchange.

Government Healthcare Spending

International Regulatory Expansion

As Epic expands in Europe and Asia it faces fragmented political landscapes and national health systems—EU digital health regulations and country-level procurement often favor local suppliers, creating entry barriers; for example, 47% of EU tenders in 2023 favored domestic firms.

Cybersecurity as National Security

The federal government treats healthcare infrastructure as a national security priority, increasing oversight of EHR vendors; in 2024 HHS announced enhanced cybersecurity requirements after healthcare breaches rose 45% since 2019.

Epic faces pressure to defend against state-sponsored attacks—health sector cyber incidents cost an average $10.1M per breach in 2023—forcing continuous investment in security.

Pending federal legislation seeks mandated protocols for EHRs, so Epic must outpace regulation to retain trust and large contracts with government health systems.

- Federal oversight rising; HHS 2024 mandates

- Healthcare breaches +45% since 2019; $10.1M average cost per breach (2023)

- Legislation pushing mandatory EHR security protocols

- Epic must invest continually to secure government partnerships

Public Health Data Integration

Political pushes after COVID-19 and CDC initiatives (eg 2024 Data Modernization Initiative funding of $1.1B) demand tighter EHR-public health integration; Epic, with ~33% US acute EHR market share and >250M patient records, is a focal point for these reforms.

Lawmakers expect Epic to adopt standardized reporting (FHIR/US Core) and face scrutiny—Congressional hearings and state-level legislation in 2024 increased oversight and transparency mandates tied to federal grants.

- Epic holds ~33% US hospital EHR market share and >250M patient records

- $1.1B CDC Data Modernization Initiative (2024) pushes integration

- Increased legislative oversight and transparency mandates in 2024

Epic faces TEFCA/FHIR, funding & cyber pressure across 33% US acute market

Federal TEFCA/HHS mandates (2024) force Epic to maintain TEFCA/FHIR compliance across ~33% US acute market and >250M records; Medicare/Medicaid budgets (~$900B/$700B in 2024) and $1.1B CDC Data Modernization funding raise integration demands; cyber threats (+45% breaches since 2019; $10.1M avg cost 2023) and EU/local procurement (47% domestic wins 2023) increase regulatory and market pressure.

| Metric | 2023–2024 |

|---|---|

| US acute market share | ~33% |

| Patient records | >250M |

| Medicare/Medicaid spend | $900B / $700B |

| CDC DMI funding | $1.1B |

| Digital health VC | $15.3B (2024) |

| Healthcare breaches rise | +45% since 2019; $10.1M avg |

| EU domestic tender bias | 47% (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Epic Systems across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform strategy, risk management, and investor communications.

Provides a concise, visually segmented PESTLE snapshot of Epic Systems that can be dropped into presentations or shared across teams to streamline strategic discussions and risk assessment.

Economic factors

Healthcare Provider Consolidation

Consolidation of US hospitals—M&A volume reached roughly 725 transactions in 2024 and 2025 saw continued large-system deals—favors Epic as health systems standardize on one EHR; acquisitions of clinics by Epic-using systems typically trigger migrations, boosting Epic’s bookings and services revenue. Fewer independent buyers reduce addressable customers but increase contract size, reinforcing Epic’s enterprise market share (estimated >30% inpatient EHR market in 2024) and organic growth.

High Cost of Implementation

The significant capital expenditure to implement and maintain Epic systems—often $1–10 million for mid-sized hospitals per 2024 estimates—remains a major barrier for smaller or rural providers; total cost of ownership can exceed $20 million over a decade. Elevated U.S. base rates peaking near 5.5% in 2024–2025 increased financing costs, raising annual carrying costs by tens to hundreds of thousands per project. Epic must innovate pricing and offer modular, cloud or subscription options to broaden affordability across the healthcare economic spectrum.

Labor Shortages in IT

A persistent shortage of Epic-certified analysts and IT pros raises operational costs for Epic and its clients; US IT job openings hit 8.7M in 2024, and healthcare IT wages grew ~6–8% year-over-year, fueling wage inflation and hiring competition. Epic and partners face higher implementation TCO and must invest in training programs and automation—Epic reportedly expanded its training capacity by 20% in 2024—to lower long-term labor needs.

Global Inflationary Pressures

Global inflation raises data center energy and hardware costs—U.S. core PCE rose 3.5% YoY in 2024—pressuring Epic Systems’ operating expenses for servers, networking, and maintenance.

Epic’s recurring maintenance/support revenue cushions volatility, but higher input costs risk squeezing adjusted operating margins if price increases lag inflation.

Epic must calibrate pricing to cover rising costs while avoiding rate shocks for hospital clients facing constrained 2024–25 health budgets.

- 2024 U.S. core PCE +3.5% YoY

- Recurring maintenance stabilizes revenue

- Rising capex/opex from hardware and energy

- Pricing balance critical to retain budget-constrained clients

Subscription and Cloud Revenue Stability

The shift to cloud hosting and SaaS has given Epic more predictable recurring revenue versus legacy perpetual licenses, with cloud/subscription bookings rising to an estimated 65% of new contract value by end-2025 and recurring revenue representing roughly 70% of total revenue in 2024–25.

Investors value this stability: SaaS-like gross retention rates above 95% and multi-year contracts have improved free cash flow predictability and supported R&D investment, with Epic reportedly increasing R&D spend to around 12–14% of revenue by 2025.

- Recurring revenue dominance: ~70% of revenue (2024–25)

- New bookings: ~65% cloud/subscription by end-2025

- Gross retention: >95%

- R&D spend: ~12–14% of revenue (2025)

Epic dominates inpatient EHRs as cloud, costs, and labor squeeze smaller buyers

Consolidation and cloud shifts increased Epic’s enterprise share (>30% inpatient EHR 2024) and recurring revenue (~70% 2024–25), while high capex ($1–10M midsize, $20M TCO/decade) and 2024–25 rate-driven financing costs (US rates ~5.5%) pressure smaller buyers; labor scarcity (IT openings 8.7M 2024, wages +6–8%) and inflation (core PCE +3.5% 2024) raise opex, forcing pricing and modular SaaS offers to preserve margins.

| Metric | 2024–25 |

|---|---|

| Inpatient EHR share | >30% |

| Recurring rev | ~70% |

| Cloud bookings | ~65% new CV by end‑2025 |

| Mid HS capex | $1–10M |

| TCO/decade | ~$20M |

| US core PCE | +3.5% YoY (2024) |

| US rates | ~5.5% (2024–25) |

| IT openings | 8.7M (2024) |

Full Version Awaits

Epic Systems PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Epic Systems PESTLE Analysis provides concise legal, economic, social, technological, environmental, and political insights tailored to healthcare IT decision-makers. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying. No placeholders or surprises—just the final, professional file.