ePlus Porter's Five Forces Analysis

Don't Miss the Bigger Picture

ePlus operates in a dynamic IT solutions market where supplier leverage, buyer expectations, and competitive rivalry shape margins and growth prospects—this snapshot highlights key pressures and strategic levers.

This brief preview only scratches the surface; unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentration of Major Technology Vendors

Supplier power is high: ePlus sources over 60% of hardware from a few OEMs—Cisco, Dell, Hewlett Packard Enterprise—giving those vendors control over pricing, availability, and product roadmaps.

If a primary vendor shifts channel strategy or cuts partner margins (Cisco cut some reseller incentives 2024–25), ePlus would see margin compression and inventory gaps that can lower FY2025 gross margin by an estimated 100–200 bps.

Criticality of Partner Certification Tiers

Suppliers wield power via strict certification tiers that determine discounts and support levels, with top-tier partners often receiving 20–40% better margin terms; ePlus must fund extensive technical and sales certifications—estimated $3.5–5k per employee—to keep status. This ongoing spend creates dependency, since vendors can revoke privileges and cut ePlus’s access to lead programs, pricing, and co-marketing, directly affecting revenue and competitiveness.

Influence of Proprietary Technology Ecosystems

The shift to proprietary cloud and software ecosystems gives suppliers control of product lifecycles—maintenance, updates, and security—forcing ePlus to keep deep ties with vendors like Microsoft, AWS, and Oracle; in 2024 ePlus reported 62% of revenue tied to major vendor platforms.

Customer lock-in to vendor architectures raises churn risk if ePlus drops support, so switching suppliers could disrupt services and client SLAs, limiting ePlus’s bargaining flexibility and pushing margin pressure.

Supplier Driven Incentive and Rebate Programs

Supplier-driven rebates and incentives account for roughly 15–25% of gross margin for US technology resellers; ePlus relies heavily on these backend payments to hit margins and fund operations, giving manufacturers leverage to shape product mix and pricing.

Manufacturers tie bonuses to volume, attach rates, and certification levels, so suppliers can push preferred lines and quarterly targets, constraining ePlus strategic choices and negotiation power.

- 15–25% of gross margin from rebates (industry range, 2024)

- Quarterly bonus thresholds shift product focus

- Supplier control limits ePlus pricing flexibility

- Performance incentives influence channel strategy

Market Consolidation Among Sub-component Providers

ePlus buys through major OEMs, but by late 2025 consolidation among semiconductor and specialized-hardware makers raised component lead times to 20–30 weeks and pushed spot premiums ~15–25%, so OEMs pass higher costs to ePlus.

That trickle-down keeps supplier pricing power elevated because these components are essential and scarce, amplifying margin pressure and purchase volatility for ePlus.

- Lead times: 20–30 weeks (late 2025)

- Spot premiums: ~15–25% (hardware/semi)

- Supplier concentration: top 5 firms control >60% capacity

- Impact: higher OEM pass-through, margin squeeze

Supplier concentration (>60%) and rebate shifts can swing ePlus margins 100–200 bps

High supplier power: top OEMs (Cisco, Dell, HPE, Microsoft, AWS) supply >60% of hardware/software; rebates drive 15–25% of gross margin, certification costs ~$3.5–5k/employee, and vendor actions (2024–25 incentive cuts) can swing ePlus gross margin by ~100–200 bps.

| Metric | Value (2024–25) |

|---|---|

| Supplier concentration | >60% |

| Rebates share | 15–25% |

| Cert cost/employee | $3.5–5k |

| Margin sensitivity | 100–200 bps |

What is included in the product

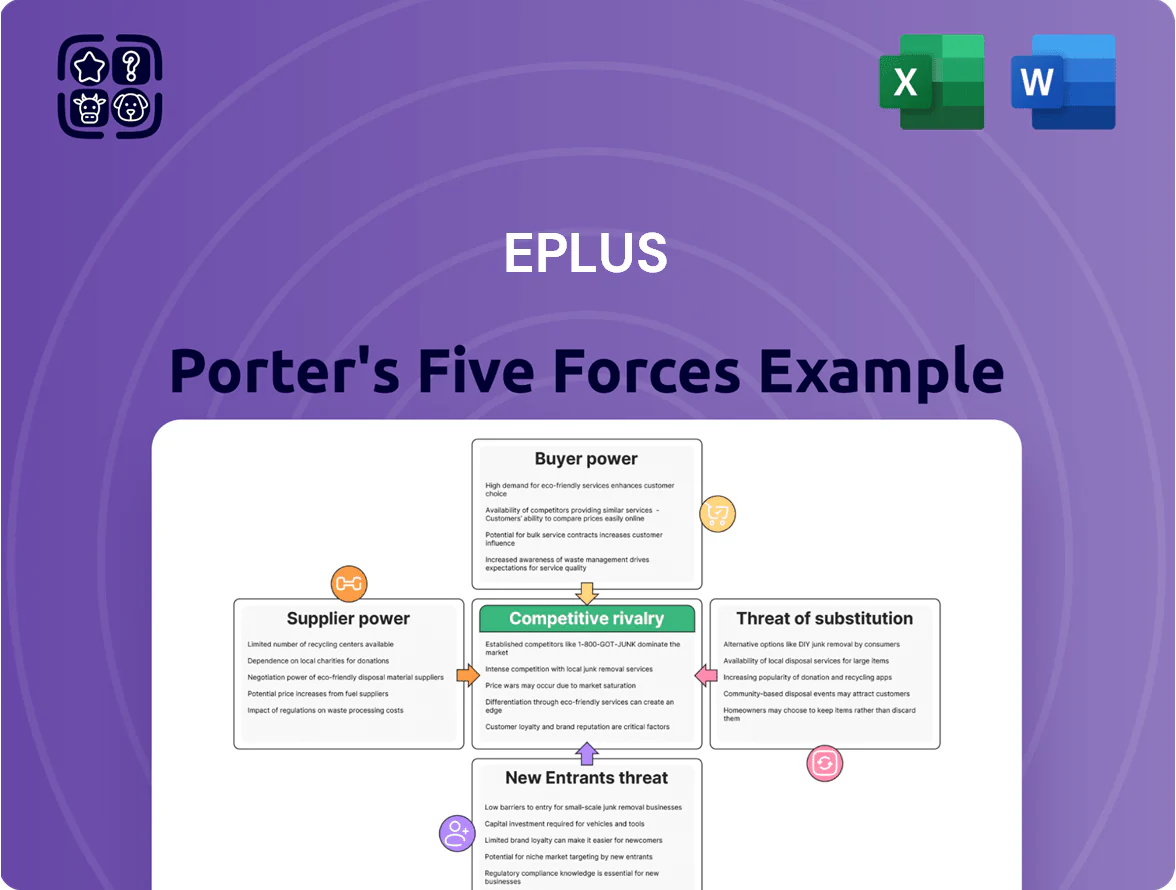

Tailored exclusively for ePlus, this Porter's Five Forces overview uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats shaping its market position and profitability.

A one-sheet Porter's Five Forces summary that visualizes competitive pressure with a radar chart and editable fields—perfect for fast strategic decisions and seamless inclusion in decks or Excel dashboards.

Customers Bargaining Power

High Price Sensitivity in Enterprise Procurement

Customers treat hardware and basic networking as commodities, driving price-led buying; IDC reported in 2024 that 62% of enterprise IT spend on standard infrastructure is procurement-driven. Large enterprises use RFPs and competitive bidding—Gartner found 74% of deals over $1M invited three or more vendors—forcing ePlus to trim margins to win contracts. Price sensitivity peaks for non-differentiated equipment where reseller differentiation is minimal and bids converge on cost.

Low Switching Costs for Standard Product Fulfillment

Low switching costs for standard hardware fulfillment mean clients can move from ePlus to other large VARs with little friction; Gartner estimates 60% of enterprise hardware spend is re-competed annually, and IDC found 45% of buyers prioritize price over vendor loyalty. Competitors match logistics and procurement, so even 1–3% price differences trigger migrations, forcing ePlus to defend revenue with superior service, faster lead times, and deeper technical expertise.

Demand for Integrated and Tailored Solutions

Modern buyers now demand end-to-end, tailored IT roadmaps over point products, boosting their bargaining power in SLAs; 2024 surveys show 62% of enterprise buyers prefer vendors offering integrated strategy and delivery (Gartner, 2024).

Clients expect ePlus to act as a strategic consultant, stitching cloud, security, and networking into a unified stack, enabling tougher negotiations on pricing and scope.

As a result, customers push for elevated post-sale support and managed services upfront; managed services made up 34% of ePlus’s 2023 services revenue, strengthening customer leverage.

Influence of Large Scale Corporate Buyers

Large corporate and government buyers account for roughly 60–70% of enterprise IT spend in North America, letting them demand volume discounts and service-level concessions from providers like ePlus.

These buyers can insource services—US federal IT staffing rose 4% in 2024—creating a credible vertical-integration threat that pressures margins.

So ePlus must provide measurable value-adds—case studies, 20–30% time-to-deploy improvements, or guaranteed uptime—to justify premium professional and managed services.

- 60–70% enterprise IT spend concentration

- 4% rise in US federal IT staffing (2024)

- 20–30% deployment time savings as a defensible differentiator

Increased Information Transparency and Market Awareness

By 2025, real-time market data and peer reviews let buyers compare ePlus pricing and service quality instantly, reducing information asymmetry and raising price sensitivity.

Customers benchmark ePlus at renewals and RFPs, using sites and benchmarks that show 10–20% price variance among competitors, pressuring ePlus on standard services.

This informed base caps ePlus’s margins on commoditized services; services seen as unique keep premium pricing only when tied to measurable outcomes.

- Real-time data and reviews up by ~40% usage since 2021

- Buyers cite 10–20% competitor price variance

- Commoditized service margins under pressure

Large buyers force price-led RFPs—managed services and faster deployment hold the premium

Customers wield strong bargaining power: 60–70% of NA enterprise IT spend is concentrated in large buyers who re-compete 60% of purchases annually, driving price-led RFPs (74% of >$1M deals invite 3+ vendors) and 10–20% observable price variance; managed services (34% of ePlus 2023 services revenue) and 20–30% deployment time savings are required to retain premiums.

| Metric | Value |

|---|---|

| Concentration of spend | 60–70% |

| Re-compete rate | 60% |

| Large-deal multi-vendor RFPs | 74% |

| Price variance seen | 10–20% |

| Managed services share (ePlus 2023) | 34% |

| Defensible deployment savings | 20–30% |

Same Document Delivered

ePlus Porter's Five Forces Analysis

This preview shows the exact ePlus Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready to use for decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

ePlus operates in a dynamic IT solutions market where supplier leverage, buyer expectations, and competitive rivalry shape margins and growth prospects—this snapshot highlights key pressures and strategic levers.

This brief preview only scratches the surface; unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentration of Major Technology Vendors

Supplier power is high: ePlus sources over 60% of hardware from a few OEMs—Cisco, Dell, Hewlett Packard Enterprise—giving those vendors control over pricing, availability, and product roadmaps.

If a primary vendor shifts channel strategy or cuts partner margins (Cisco cut some reseller incentives 2024–25), ePlus would see margin compression and inventory gaps that can lower FY2025 gross margin by an estimated 100–200 bps.

Criticality of Partner Certification Tiers

Suppliers wield power via strict certification tiers that determine discounts and support levels, with top-tier partners often receiving 20–40% better margin terms; ePlus must fund extensive technical and sales certifications—estimated $3.5–5k per employee—to keep status. This ongoing spend creates dependency, since vendors can revoke privileges and cut ePlus’s access to lead programs, pricing, and co-marketing, directly affecting revenue and competitiveness.

Influence of Proprietary Technology Ecosystems

The shift to proprietary cloud and software ecosystems gives suppliers control of product lifecycles—maintenance, updates, and security—forcing ePlus to keep deep ties with vendors like Microsoft, AWS, and Oracle; in 2024 ePlus reported 62% of revenue tied to major vendor platforms.

Customer lock-in to vendor architectures raises churn risk if ePlus drops support, so switching suppliers could disrupt services and client SLAs, limiting ePlus’s bargaining flexibility and pushing margin pressure.

Supplier Driven Incentive and Rebate Programs

Supplier-driven rebates and incentives account for roughly 15–25% of gross margin for US technology resellers; ePlus relies heavily on these backend payments to hit margins and fund operations, giving manufacturers leverage to shape product mix and pricing.

Manufacturers tie bonuses to volume, attach rates, and certification levels, so suppliers can push preferred lines and quarterly targets, constraining ePlus strategic choices and negotiation power.

- 15–25% of gross margin from rebates (industry range, 2024)

- Quarterly bonus thresholds shift product focus

- Supplier control limits ePlus pricing flexibility

- Performance incentives influence channel strategy

Market Consolidation Among Sub-component Providers

ePlus buys through major OEMs, but by late 2025 consolidation among semiconductor and specialized-hardware makers raised component lead times to 20–30 weeks and pushed spot premiums ~15–25%, so OEMs pass higher costs to ePlus.

That trickle-down keeps supplier pricing power elevated because these components are essential and scarce, amplifying margin pressure and purchase volatility for ePlus.

- Lead times: 20–30 weeks (late 2025)

- Spot premiums: ~15–25% (hardware/semi)

- Supplier concentration: top 5 firms control >60% capacity

- Impact: higher OEM pass-through, margin squeeze

Supplier concentration (>60%) and rebate shifts can swing ePlus margins 100–200 bps

High supplier power: top OEMs (Cisco, Dell, HPE, Microsoft, AWS) supply >60% of hardware/software; rebates drive 15–25% of gross margin, certification costs ~$3.5–5k/employee, and vendor actions (2024–25 incentive cuts) can swing ePlus gross margin by ~100–200 bps.

| Metric | Value (2024–25) |

|---|---|

| Supplier concentration | >60% |

| Rebates share | 15–25% |

| Cert cost/employee | $3.5–5k |

| Margin sensitivity | 100–200 bps |

What is included in the product

Tailored exclusively for ePlus, this Porter's Five Forces overview uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and disruptive threats shaping its market position and profitability.

A one-sheet Porter's Five Forces summary that visualizes competitive pressure with a radar chart and editable fields—perfect for fast strategic decisions and seamless inclusion in decks or Excel dashboards.

Customers Bargaining Power

High Price Sensitivity in Enterprise Procurement

Customers treat hardware and basic networking as commodities, driving price-led buying; IDC reported in 2024 that 62% of enterprise IT spend on standard infrastructure is procurement-driven. Large enterprises use RFPs and competitive bidding—Gartner found 74% of deals over $1M invited three or more vendors—forcing ePlus to trim margins to win contracts. Price sensitivity peaks for non-differentiated equipment where reseller differentiation is minimal and bids converge on cost.

Low Switching Costs for Standard Product Fulfillment

Low switching costs for standard hardware fulfillment mean clients can move from ePlus to other large VARs with little friction; Gartner estimates 60% of enterprise hardware spend is re-competed annually, and IDC found 45% of buyers prioritize price over vendor loyalty. Competitors match logistics and procurement, so even 1–3% price differences trigger migrations, forcing ePlus to defend revenue with superior service, faster lead times, and deeper technical expertise.

Demand for Integrated and Tailored Solutions

Modern buyers now demand end-to-end, tailored IT roadmaps over point products, boosting their bargaining power in SLAs; 2024 surveys show 62% of enterprise buyers prefer vendors offering integrated strategy and delivery (Gartner, 2024).

Clients expect ePlus to act as a strategic consultant, stitching cloud, security, and networking into a unified stack, enabling tougher negotiations on pricing and scope.

As a result, customers push for elevated post-sale support and managed services upfront; managed services made up 34% of ePlus’s 2023 services revenue, strengthening customer leverage.

Influence of Large Scale Corporate Buyers

Large corporate and government buyers account for roughly 60–70% of enterprise IT spend in North America, letting them demand volume discounts and service-level concessions from providers like ePlus.

These buyers can insource services—US federal IT staffing rose 4% in 2024—creating a credible vertical-integration threat that pressures margins.

So ePlus must provide measurable value-adds—case studies, 20–30% time-to-deploy improvements, or guaranteed uptime—to justify premium professional and managed services.

- 60–70% enterprise IT spend concentration

- 4% rise in US federal IT staffing (2024)

- 20–30% deployment time savings as a defensible differentiator

Increased Information Transparency and Market Awareness

By 2025, real-time market data and peer reviews let buyers compare ePlus pricing and service quality instantly, reducing information asymmetry and raising price sensitivity.

Customers benchmark ePlus at renewals and RFPs, using sites and benchmarks that show 10–20% price variance among competitors, pressuring ePlus on standard services.

This informed base caps ePlus’s margins on commoditized services; services seen as unique keep premium pricing only when tied to measurable outcomes.

- Real-time data and reviews up by ~40% usage since 2021

- Buyers cite 10–20% competitor price variance

- Commoditized service margins under pressure

Large buyers force price-led RFPs—managed services and faster deployment hold the premium

Customers wield strong bargaining power: 60–70% of NA enterprise IT spend is concentrated in large buyers who re-compete 60% of purchases annually, driving price-led RFPs (74% of >$1M deals invite 3+ vendors) and 10–20% observable price variance; managed services (34% of ePlus 2023 services revenue) and 20–30% deployment time savings are required to retain premiums.

| Metric | Value |

|---|---|

| Concentration of spend | 60–70% |

| Re-compete rate | 60% |

| Large-deal multi-vendor RFPs | 74% |

| Price variance seen | 10–20% |

| Managed services share (ePlus 2023) | 34% |

| Defensible deployment savings | 20–30% |

Same Document Delivered

ePlus Porter's Five Forces Analysis

This preview shows the exact ePlus Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups, fully formatted and ready to use for decision-making.