Equinix Boston Consulting Group Matrix

Actionable Strategy Starts Here

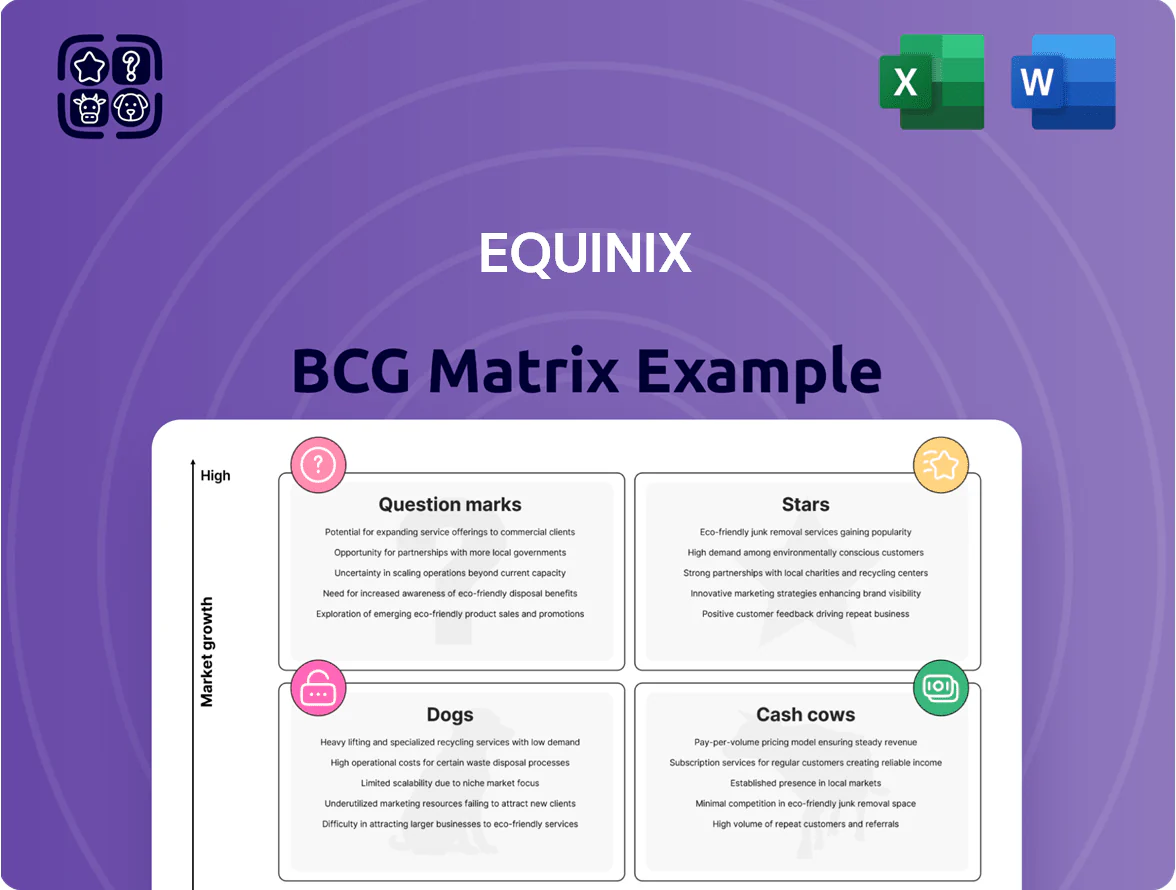

Equinix’s BCG Matrix preview highlights its role as a global data-center leader with clear Stars in high-growth interconnection services and Cash Cows in established colocation assets, while emerging edge offerings occupy Question Mark territory that could become future growth drivers. This snapshot shows where capital allocation and divestment decisions matter most to sustain market leadership and margin resilience. Purchase the full BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and downloadable Word and Excel deliverables to act on these strategic insights immediately.

Stars

AI-Ready Infrastructure (Equinix Private AI)

As of late 2025, Equinix (Equinix, Inc.) leads premium AI-ready infrastructure (Equinix Private AI) with >40% share of high-density power and cooling deployments for generative AI, supporting racks delivering 100+ kW each and 400+ MW aggregate capacity globally.

Demand surged as enterprises moved to production; Equinix reported AI-related interconnection revenue up 28% YoY in 2025 and added 60 hyperscale/private AI customers that year.

Equinix Fabric Interconnection

Equinix Fabric is a Star: it lets customers dynamically connect their infrastructure to any other customer on the platform, driving rapid uptake; Fabric grew revenue-contributing virtual connections ~28% year-over-year in 2024, with >1.2M virtual connections across 65+ metros as of Dec 31, 2024.

Hyperscale Joint Ventures (xScale)

The xScale program partners with the world’s largest cloud providers to build massive, dedicated campuses; Equinix reported xScale revenue of $1.1B in 2024, up 28% YoY, reflecting strong demand for hyperscale capacity.

Using joint ventures, Equinix shares ownership and risk, keeping equity stakes while funding needs are split—this reduced capital deployed by about $600M in 2024 versus sole-builds.

xScale is a primary growth engine as cloud providers decentralize toward edge sites; Equinix had 24 xScale campuses across 12 countries by Dec 2025, driving capacity expansion and higher long-term ARR.

Enterprise Digital Core Expansion

Enterprise Digital Core Expansion sits in the star quadrant as enterprises shift from on-prem to Equinix IBX data centers to reach cloud on-ramps; Equinix reported 2024 interconnection revenue growth of 14% and FX-neutral revenue of $7.9B, showing strong demand for proximity to AWS, Azure, and Google Cloud.

The move to decentralized IT boosts addressable market: Equinix’s Platform Equinix connects 11,000+ companies and over 3,200 cloud and network providers, keeping enterprise growth rates above company average and sustaining high-capex returns.

High demand for low-latency, multi-cloud connectivity keeps this unit a star—colocation and interconnection pricing power and 99.999% power uptime drive sticky enterprise contracts and recurring revenue.

- 2024 interconnection rev +14%

- Platform connects 11,000+ firms

- 3,200+ cloud/network providers

- FX-neutral rev $7.9B (2024)

Expansion in Emerging Markets (Africa and SE Asia)

Equinix is rapidly scaling in South Africa, Nigeria and Southeast Asia via acquisitions and new builds, targeting markets where digital GDP growth runs 6–8% annually; the company disclosed ~USD 1.2bn of capital expenditure for APAC and EMEA expansion in 2024 to capture early share.

Significant investment aims to convert high-growth sites into stable revenue: Equinix added 40+ facilities in APAC/EMEA since 2022 and cites double-digit ARR growth in select SEA and African metros.

- APAC/EMEA capex ~USD 1.2bn (2024)

- 40+ new facilities since 2022

- Digital GDP growth 6–8% in target markets

- Double-digit ARR in select metros

Equinix: Dominant AI Colocation — 400+MW, 40%+ share, double-digit growth

Equinix’s Stars: AI-ready colocation (40%+ share of high-density AI deployments, 400+ MW global capacity) and Platform Equinix (11,000+ companies, 3,200+ providers) drive strong growth; interconnection rev +14% in 2024, AI interconnection revenue +28% in 2025.

xScale fuels scale with $1.1B revenue in 2024 and 24 campuses by Dec 2025; APAC/EMEA capex ~USD 1.2B (2024) to capture double-digit ARR metros.

High uptime (99.999%) and sticky contracts sustain pricing power and recurring revenue.

| Metric | Value |

|---|---|

| AI capacity | 400+ MW |

| High-density share | 40%+ |

| Platform firms/providers | 11,000+/3,200+ |

| Interconnect rev growth (2024) | +14% |

| AI interconnect rev growth (2025) | +28% |

| xScale rev (2024) | $1.1B |

| APAC/EMEA capex (2024) | $1.2B |

| Uptime | 99.999% |

What is included in the product

Comprehensive BCG Matrix analysis of Equinix’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Equinix BCG Matrix placing each business unit in a quadrant for rapid strategic decisions and investor briefings.

Cash Cows

Retail Colocation in Tier 1 Metros

Established Equinix retail colocation in Tier 1 metros—New York, London, Tokyo—are primary cash generators, with global occupancy in these hubs often above 95% and metro-specific utilization routinely >90% as of 2025.

These mature markets give Equinix dominant scale and moats: in 2024 Equinix held roughly 30–40% market share in key metros, long-term contracts, and dense interconnection ecosystems that lower competitive pressure.

Low churn and steady rental and interconnection revenue produced ~$1.9B adjusted EBITDA from Americas core metros in FY2024, funding higher-growth builds in hyperscale and emerging markets.

Cross-Connect Physical Services

Cross-connect physical services—simple fiber links between tenants in the same Equinix International Business Exchange (IBX)—generate high-margin, low-maintenance revenue, with reported interconnection revenue contributing to Equinix’s 2024 platform growth; margins exceed 60% on port and cross-connect fees.

Equinix hosts over 10,000 customers per major metro IBX and 240+ data centers globally (2025), making local cross-connect market share nearly impenetrable and locking in recurring demand.

These services need minimal capex—mostly patch panels and port provisioning—so incremental investment per new cross-connect is under $200, while yearly recurring fees yield predictable cash flow and strong free cash flow conversion.

Financial Services Ecosystems

Equinix hosts the world’s largest electronic trading ecosystems, serving 430+ financial firms and 1,200+ market participants across 75+ financial hubs, delivering sub-microsecond latency needed by global banks and high-frequency traders.

This is a mature, stable market where Equinix holds ~40% global market share in financial colocation, generating predictable cash flows and ~15–18% EBITDA margins—classic cash cow economics.

High barriers to entry—capex for low-latency sites, regulatory certifications, and ecosystem density—plus strong network effects from existing participants lock in customers and sustain long-term profitability.

Network Service Provider Hubs

Equinix hosts over 1,800 network service providers, making its Network Service Provider Hubs a stable, mature cash cow that functions as the internet’s central nervous system and drives predictable revenue.

Carrier density reduces marketing needs since providers and customers self-reinforce connectivity demand; in 2025 interconnection revenue and recurring fees contributed materially to Equinix’s 2024 revenue of $7.1B, supporting cash flow stability.

Steady port and cross-connect fees from carriers create a reliable financial backbone with high margins and low churn, underpinning capital allocation to growth segments.

- 1,800+ carriers housed

- Low promo spend; organic customer pull

- Supports 2024 revenue $7.1B

- High-margin, recurring port/cross-connect fees

Managed Services and Support

Managed Services and Support deliver steady, high-margin revenue for Equinix—standardized support and basic managed infrastructure bundled into colocation contracts boost retention and predictability, contributing to Equinix’s 2025 recurring revenue mix where interconnection and services grew ~8% YoY and services revenue exceeded $2.1B in FY2024.

These offerings milk extra value from existing data-center footprint with minimal capex: Equinix reported 2024 free cash flow of $1.9B, enabling service expansion without major new builds.

- High margins from standardized support

- Bundled with colocation → >90% retention

- Predictable, incremental revenue (~$2.1B services 2024)

- Low incremental capex; leverages existing footprint

Equinix metros: cash cow scale—$7.1B revenue, $1.9B FCF, >60% interconnect margins

Equinix core metros and network hubs are cash cows: ~240 IBX, >10,000 customers/major metro, ~30–40% metro share, 2024 revenue $7.1B, services $2.1B, FY2024 FCF $1.9B, interconnection margins >60%, EBITDA margins ~15–18% in financial colocation.

| Metric | Value (2024/2025) |

|---|---|

| IBX count | 240+ |

| Revenue | $7.1B |

| Services rev | $2.1B |

| FCF | $1.9B |

Delivered as Shown

Equinix BCG Matrix

The file you're previewing on this page is the final Equinix BCG Matrix you'll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, analysis-ready report built for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Equinix’s BCG Matrix preview highlights its role as a global data-center leader with clear Stars in high-growth interconnection services and Cash Cows in established colocation assets, while emerging edge offerings occupy Question Mark territory that could become future growth drivers. This snapshot shows where capital allocation and divestment decisions matter most to sustain market leadership and margin resilience. Purchase the full BCG Matrix for quadrant-by-quadrant placement, data-backed recommendations, and downloadable Word and Excel deliverables to act on these strategic insights immediately.

Stars

AI-Ready Infrastructure (Equinix Private AI)

As of late 2025, Equinix (Equinix, Inc.) leads premium AI-ready infrastructure (Equinix Private AI) with >40% share of high-density power and cooling deployments for generative AI, supporting racks delivering 100+ kW each and 400+ MW aggregate capacity globally.

Demand surged as enterprises moved to production; Equinix reported AI-related interconnection revenue up 28% YoY in 2025 and added 60 hyperscale/private AI customers that year.

Equinix Fabric Interconnection

Equinix Fabric is a Star: it lets customers dynamically connect their infrastructure to any other customer on the platform, driving rapid uptake; Fabric grew revenue-contributing virtual connections ~28% year-over-year in 2024, with >1.2M virtual connections across 65+ metros as of Dec 31, 2024.

Hyperscale Joint Ventures (xScale)

The xScale program partners with the world’s largest cloud providers to build massive, dedicated campuses; Equinix reported xScale revenue of $1.1B in 2024, up 28% YoY, reflecting strong demand for hyperscale capacity.

Using joint ventures, Equinix shares ownership and risk, keeping equity stakes while funding needs are split—this reduced capital deployed by about $600M in 2024 versus sole-builds.

xScale is a primary growth engine as cloud providers decentralize toward edge sites; Equinix had 24 xScale campuses across 12 countries by Dec 2025, driving capacity expansion and higher long-term ARR.

Enterprise Digital Core Expansion

Enterprise Digital Core Expansion sits in the star quadrant as enterprises shift from on-prem to Equinix IBX data centers to reach cloud on-ramps; Equinix reported 2024 interconnection revenue growth of 14% and FX-neutral revenue of $7.9B, showing strong demand for proximity to AWS, Azure, and Google Cloud.

The move to decentralized IT boosts addressable market: Equinix’s Platform Equinix connects 11,000+ companies and over 3,200 cloud and network providers, keeping enterprise growth rates above company average and sustaining high-capex returns.

High demand for low-latency, multi-cloud connectivity keeps this unit a star—colocation and interconnection pricing power and 99.999% power uptime drive sticky enterprise contracts and recurring revenue.

- 2024 interconnection rev +14%

- Platform connects 11,000+ firms

- 3,200+ cloud/network providers

- FX-neutral rev $7.9B (2024)

Expansion in Emerging Markets (Africa and SE Asia)

Equinix is rapidly scaling in South Africa, Nigeria and Southeast Asia via acquisitions and new builds, targeting markets where digital GDP growth runs 6–8% annually; the company disclosed ~USD 1.2bn of capital expenditure for APAC and EMEA expansion in 2024 to capture early share.

Significant investment aims to convert high-growth sites into stable revenue: Equinix added 40+ facilities in APAC/EMEA since 2022 and cites double-digit ARR growth in select SEA and African metros.

- APAC/EMEA capex ~USD 1.2bn (2024)

- 40+ new facilities since 2022

- Digital GDP growth 6–8% in target markets

- Double-digit ARR in select metros

Equinix: Dominant AI Colocation — 400+MW, 40%+ share, double-digit growth

Equinix’s Stars: AI-ready colocation (40%+ share of high-density AI deployments, 400+ MW global capacity) and Platform Equinix (11,000+ companies, 3,200+ providers) drive strong growth; interconnection rev +14% in 2024, AI interconnection revenue +28% in 2025.

xScale fuels scale with $1.1B revenue in 2024 and 24 campuses by Dec 2025; APAC/EMEA capex ~USD 1.2B (2024) to capture double-digit ARR metros.

High uptime (99.999%) and sticky contracts sustain pricing power and recurring revenue.

| Metric | Value |

|---|---|

| AI capacity | 400+ MW |

| High-density share | 40%+ |

| Platform firms/providers | 11,000+/3,200+ |

| Interconnect rev growth (2024) | +14% |

| AI interconnect rev growth (2025) | +28% |

| xScale rev (2024) | $1.1B |

| APAC/EMEA capex (2024) | $1.2B |

| Uptime | 99.999% |

What is included in the product

Comprehensive BCG Matrix analysis of Equinix’s units with strategic actions for Stars, Cash Cows, Question Marks, and Dogs.

One-page Equinix BCG Matrix placing each business unit in a quadrant for rapid strategic decisions and investor briefings.

Cash Cows

Retail Colocation in Tier 1 Metros

Established Equinix retail colocation in Tier 1 metros—New York, London, Tokyo—are primary cash generators, with global occupancy in these hubs often above 95% and metro-specific utilization routinely >90% as of 2025.

These mature markets give Equinix dominant scale and moats: in 2024 Equinix held roughly 30–40% market share in key metros, long-term contracts, and dense interconnection ecosystems that lower competitive pressure.

Low churn and steady rental and interconnection revenue produced ~$1.9B adjusted EBITDA from Americas core metros in FY2024, funding higher-growth builds in hyperscale and emerging markets.

Cross-Connect Physical Services

Cross-connect physical services—simple fiber links between tenants in the same Equinix International Business Exchange (IBX)—generate high-margin, low-maintenance revenue, with reported interconnection revenue contributing to Equinix’s 2024 platform growth; margins exceed 60% on port and cross-connect fees.

Equinix hosts over 10,000 customers per major metro IBX and 240+ data centers globally (2025), making local cross-connect market share nearly impenetrable and locking in recurring demand.

These services need minimal capex—mostly patch panels and port provisioning—so incremental investment per new cross-connect is under $200, while yearly recurring fees yield predictable cash flow and strong free cash flow conversion.

Financial Services Ecosystems

Equinix hosts the world’s largest electronic trading ecosystems, serving 430+ financial firms and 1,200+ market participants across 75+ financial hubs, delivering sub-microsecond latency needed by global banks and high-frequency traders.

This is a mature, stable market where Equinix holds ~40% global market share in financial colocation, generating predictable cash flows and ~15–18% EBITDA margins—classic cash cow economics.

High barriers to entry—capex for low-latency sites, regulatory certifications, and ecosystem density—plus strong network effects from existing participants lock in customers and sustain long-term profitability.

Network Service Provider Hubs

Equinix hosts over 1,800 network service providers, making its Network Service Provider Hubs a stable, mature cash cow that functions as the internet’s central nervous system and drives predictable revenue.

Carrier density reduces marketing needs since providers and customers self-reinforce connectivity demand; in 2025 interconnection revenue and recurring fees contributed materially to Equinix’s 2024 revenue of $7.1B, supporting cash flow stability.

Steady port and cross-connect fees from carriers create a reliable financial backbone with high margins and low churn, underpinning capital allocation to growth segments.

- 1,800+ carriers housed

- Low promo spend; organic customer pull

- Supports 2024 revenue $7.1B

- High-margin, recurring port/cross-connect fees

Managed Services and Support

Managed Services and Support deliver steady, high-margin revenue for Equinix—standardized support and basic managed infrastructure bundled into colocation contracts boost retention and predictability, contributing to Equinix’s 2025 recurring revenue mix where interconnection and services grew ~8% YoY and services revenue exceeded $2.1B in FY2024.

These offerings milk extra value from existing data-center footprint with minimal capex: Equinix reported 2024 free cash flow of $1.9B, enabling service expansion without major new builds.

- High margins from standardized support

- Bundled with colocation → >90% retention

- Predictable, incremental revenue (~$2.1B services 2024)

- Low incremental capex; leverages existing footprint

Equinix metros: cash cow scale—$7.1B revenue, $1.9B FCF, >60% interconnect margins

Equinix core metros and network hubs are cash cows: ~240 IBX, >10,000 customers/major metro, ~30–40% metro share, 2024 revenue $7.1B, services $2.1B, FY2024 FCF $1.9B, interconnection margins >60%, EBITDA margins ~15–18% in financial colocation.

| Metric | Value (2024/2025) |

|---|---|

| IBX count | 240+ |

| Revenue | $7.1B |

| Services rev | $2.1B |

| FCF | $1.9B |

Delivered as Shown

Equinix BCG Matrix

The file you're previewing on this page is the final Equinix BCG Matrix you'll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, analysis-ready report built for strategic clarity and professional use.