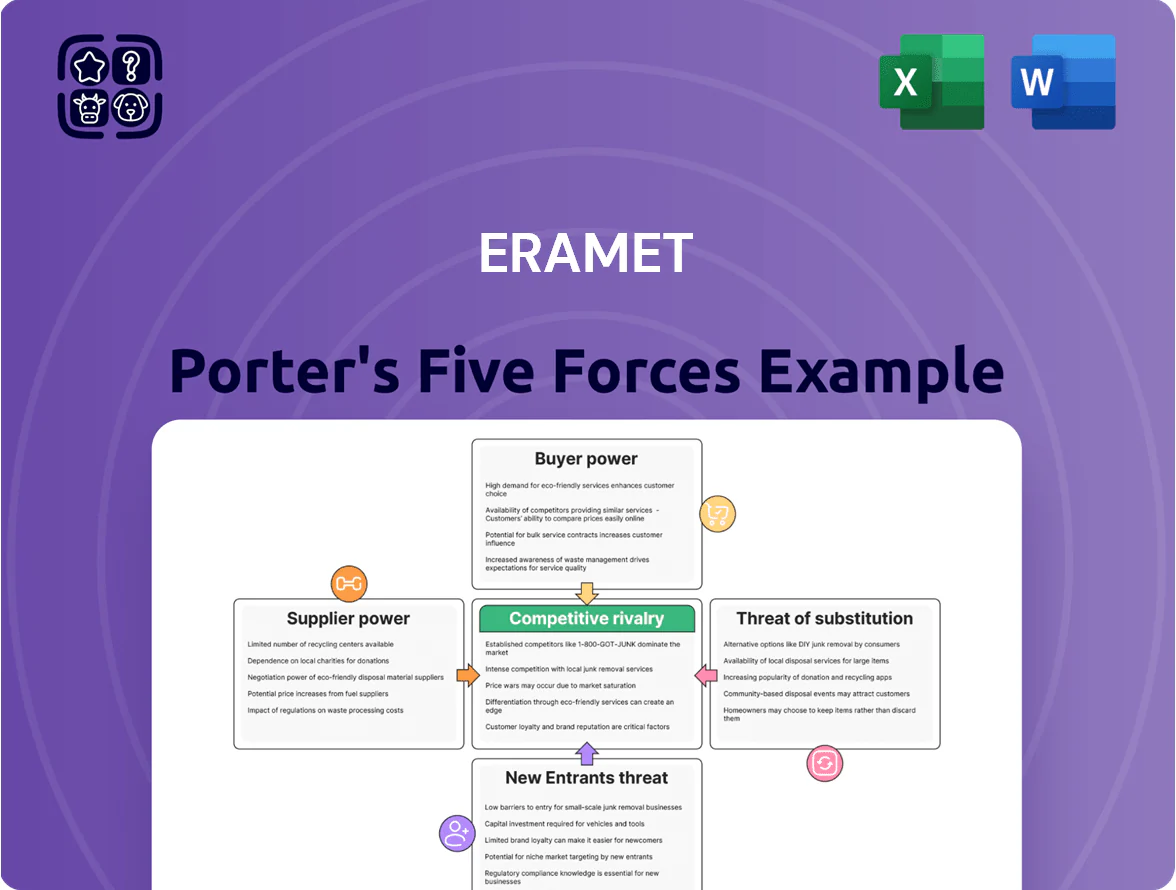

Eramet Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Eramet faces moderate supplier power, cyclical commodity pricing, and concentrated buyers that pressure margins, while high capital requirements and complex metallurgy limit new entrants.

Competitive rivalry is intense among diversified miners and alloy producers, and substitution risks emerge from recycling and material innovation—strategic positioning and cost control are critical.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Eramet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy provider pricing leverage

Eramet depends on stable, low-cost electricity for manganese and nickel smelting; energy costs made up about 9–11% of COGS in 2024 and materially affect margins.

By late 2025, Gabon and Norway suppliers wield pricing leverage—few high-capacity grids and pipeline options concentrate supply; spot prices spiked 28% in 2022–24 in some regions.

Price swings force Eramet into self-generation and long-term PPA contracts; reported c.€250m capex 2023–25 for power projects and multi‑year PPAs hedge volatility.

Specialized mining equipment vendors

Eramet depends on a small global set of suppliers—Caterpillar, Komatsu— for specialized heavy gear; in 2024 capital spares and OEM services accounted for ~12% of group procurement spend, concentrating supplier leverage.

Suppliers hold power via proprietary tech and critical maintenance for deep-pit mining and ore processing; OEM contracts often include high-margin service packages, raising switching costs.

Eramet reduces risk with diverse vendor relationships and multi-year service contracts covering ~40–60% of fleet maintenance, locking costs and availability.

Strategic procurement is key as Eramet shifts to automated and electric fleets to meet 2030 carbon targets; EV/automation capex is forecasted at €120–180m through 2027, altering supplier dynamics.

Geopolitical and land access rights

Host governments in Gabon, New Caledonia and Argentina supply legal extraction rights and wield strong bargaining power by controlling permits, royalties and environmental terms; Eg: New Caledonia raised mining royalties to 3–5% in 2023 and Gabon tightened permit renewals in 2024. Eramet must prove social value and local hiring—New Caledonia and Gabon now mandate >40% local content in some contracts—so political risk directly affects project IRR and reserve access. By 2025 regulators press profit-sharing and community benefits, increasing fixed and variable costs and raising capital-return thresholds for new developments.

Logistics and infrastructure constraints

Eramet faces high supplier power from state-controlled rail and port links; Gabon’s Trans-Gabon Railway carries ~90% of manganese exports, so tariff hikes or outages quickly hit volumes and costs.

Since 2020 Eramet has spent ~€120m on rail and port upgrades and long-term logistics contracts, a move that reduces exposure to external tariff swings and delays.

- Trans‑Gabon: ~90% manganese flow

- Eramet infrastructure spend: ~€120m (2020–2025)

- Effect: lowers tariff risk, improves shipment reliability

Specialized technical labor unions

The extraction and metallurgical processing of high-performance alloys require highly skilled, often unionized labor; in France and New Caledonia unions can disrupt Eramet’s operations via strikes or wage demands—France saw 7.1% mining sector strike-days/year (2023) and New Caledonia had three major mine stoppages 2019–2023.

Eramet mitigates risk with proactive social dialogue, workforce training programs (€25m spent 2022–2024) and retention incentives; global mining engineering shortfall—ICMM estimates 140,000 skilled roles gap by 2025—keeps specialized workers’ bargaining power high.

- Union influence: high in France/New Caledonia

- Operational risk: historical stoppages 2019–2023

- Mitigation: €25m training investment (2022–2024)

- Talent shortage: ~140,000 global gap by 2025

Eramet faces strong supplier leverage; heavy capex and PPAs mitigate energy & logistics risks

Suppliers exert high bargaining power over Eramet via concentrated energy, OEMs, state logistics and host governments; energy was ~10% of COGS (2024), OEM spares ~12% procurement (2024), and Trans‑Gabon carries ~90% manganese exports. Eramet spent c.€250m power capex (2023–25) and ~€120m on rail/port (2020–25) and uses multi‑year PPAs and 40–60% covered service contracts to hedge risk.

| Metric | Value |

|---|---|

| Energy share of COGS (2024) | ~10% |

| OEM spares share (2024) | ~12% |

| Trans‑Gabon export share | ~90% |

| Power & PPA capex (2023–25) | ~€250m |

| Rail/port spend (2020–25) | ~€120m |

What is included in the product

Tailored exclusively for Eramet, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats that shape its pricing, profitability, and market positioning.

A concise, one-sheet Porter's Five Forces for Eramet—clarifies competitive pressures fast so leaders can prioritize strategic moves.

Customers Bargaining Power

Consolidated steel industry demand

Electric vehicle battery manufacturers

With EV sales hitting 10.5 million units in 2025 globally, lithium-ion battery makers are core customers for Eramet’s nickel and lithium, giving buyers strong leverage over specs and price sensitivity.

These high-tech buyers require ESG traceability and battery-grade purities (99.8%+ NiSO4 equivalents), so they can force supply-chain transparency and contract terms.

Eramet uses its ICMM-aligned certifications and a 2024 pilot of 15,000 tpa sustainable nickel to win multi-year offtake deals and long-term pricing, often via partnerships with automakers like Renault and Stellantis, which dampen short-term volatility.

Aerospace and defense specifications

Eramet’s high-performance alloys supply critical aerospace programs at Airbus and Boeing, where material qualification can take 18–36 months and costs exceed $5m per part program, making switching prohibitively expensive.

Large OEM buyers wield bargaining power on price, but Eramet’s metallurgy know-how and certified supply chains (≈20% alloy margin premium in 2024) create a lock-in that limits customer churn.

Commodity market price transparency

Commodity prices for nickel and base metals are set largely on exchanges like the London Metal Exchange, so Eramet cannot set independent prices and sees customers benchmark bids to LME levels.

Transparent exchange pricing and digital trading platforms (trade latency down ~40% by 2025) let buyers quickly lock spot-linked contracts, capping Eramet’s premium on standard products.

Eramet shifts to value-added alloys and specialty chemicals—segments that fetched 15–25% higher margins in 2024—to reduce sensitivity to spot volatility.

- Benchmarks: LME-driven pricing limits Eramet’s price-setting

- Buyer leverage: transparent data + faster platforms tighten negotiations

- Strategy: focus on specialty, value-added products (15–25% margin uplift)

- By 2025: faster price discovery increases contract anchoring to spot

Strategic offtake and joint ventures

Many of Eramet’s biggest customers are also strategic partners or JV participants, locking in demand but using pre-set pricing that caps upside during price spikes; for example, Eramet’s 2024 manganese and lithium JV contracts often linked prices to 3–6 month averages, trimming windfall gains.

These JV/offtake deals are common in lithium brine projects to share upfront capex—industry data shows third-party financing covers 40–60% of initial capex for new brine operations—so customers supplying funds gain leverage over terms and offtake clauses.

Partnerships cut Eramet’s market risk and improve project financing access, yet they shift bargaining power to customers who control financing, offtake volumes, and pricing formulas, reducing Eramet’s margin volatility during spikes.

- Guaranteed demand via JVs/offtake, but capped pricing

- Pre-negotiated formulas tie prices to short averages (3–6 months)

- Customers often fund 40–60% of brine capex, increasing their leverage

- Reduces market risk for Eramet, shifts bargaining power to customers

Steel & battery buyers control Eramet pricing; alloys & JVs protect margins but cap upside

| Metric | 2024–25 |

|---|---|

| Top-20 steel share | 55% |

| EV sales | 10.5m |

| Alloy premium | ~20% |

| Specialty margin uplift | 15–25% |

| Buyer capex share (brine) | 40–60% |

Preview the Actual Deliverable

Eramet Porter's Five Forces Analysis

This preview shows the exact Eramet Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the full, professionally formatted document is ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Eramet faces moderate supplier power, cyclical commodity pricing, and concentrated buyers that pressure margins, while high capital requirements and complex metallurgy limit new entrants.

Competitive rivalry is intense among diversified miners and alloy producers, and substitution risks emerge from recycling and material innovation—strategic positioning and cost control are critical.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Eramet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Energy provider pricing leverage

Eramet depends on stable, low-cost electricity for manganese and nickel smelting; energy costs made up about 9–11% of COGS in 2024 and materially affect margins.

By late 2025, Gabon and Norway suppliers wield pricing leverage—few high-capacity grids and pipeline options concentrate supply; spot prices spiked 28% in 2022–24 in some regions.

Price swings force Eramet into self-generation and long-term PPA contracts; reported c.€250m capex 2023–25 for power projects and multi‑year PPAs hedge volatility.

Specialized mining equipment vendors

Eramet depends on a small global set of suppliers—Caterpillar, Komatsu— for specialized heavy gear; in 2024 capital spares and OEM services accounted for ~12% of group procurement spend, concentrating supplier leverage.

Suppliers hold power via proprietary tech and critical maintenance for deep-pit mining and ore processing; OEM contracts often include high-margin service packages, raising switching costs.

Eramet reduces risk with diverse vendor relationships and multi-year service contracts covering ~40–60% of fleet maintenance, locking costs and availability.

Strategic procurement is key as Eramet shifts to automated and electric fleets to meet 2030 carbon targets; EV/automation capex is forecasted at €120–180m through 2027, altering supplier dynamics.

Geopolitical and land access rights

Host governments in Gabon, New Caledonia and Argentina supply legal extraction rights and wield strong bargaining power by controlling permits, royalties and environmental terms; Eg: New Caledonia raised mining royalties to 3–5% in 2023 and Gabon tightened permit renewals in 2024. Eramet must prove social value and local hiring—New Caledonia and Gabon now mandate >40% local content in some contracts—so political risk directly affects project IRR and reserve access. By 2025 regulators press profit-sharing and community benefits, increasing fixed and variable costs and raising capital-return thresholds for new developments.

Logistics and infrastructure constraints

Eramet faces high supplier power from state-controlled rail and port links; Gabon’s Trans-Gabon Railway carries ~90% of manganese exports, so tariff hikes or outages quickly hit volumes and costs.

Since 2020 Eramet has spent ~€120m on rail and port upgrades and long-term logistics contracts, a move that reduces exposure to external tariff swings and delays.

- Trans‑Gabon: ~90% manganese flow

- Eramet infrastructure spend: ~€120m (2020–2025)

- Effect: lowers tariff risk, improves shipment reliability

Specialized technical labor unions

The extraction and metallurgical processing of high-performance alloys require highly skilled, often unionized labor; in France and New Caledonia unions can disrupt Eramet’s operations via strikes or wage demands—France saw 7.1% mining sector strike-days/year (2023) and New Caledonia had three major mine stoppages 2019–2023.

Eramet mitigates risk with proactive social dialogue, workforce training programs (€25m spent 2022–2024) and retention incentives; global mining engineering shortfall—ICMM estimates 140,000 skilled roles gap by 2025—keeps specialized workers’ bargaining power high.

- Union influence: high in France/New Caledonia

- Operational risk: historical stoppages 2019–2023

- Mitigation: €25m training investment (2022–2024)

- Talent shortage: ~140,000 global gap by 2025

Eramet faces strong supplier leverage; heavy capex and PPAs mitigate energy & logistics risks

Suppliers exert high bargaining power over Eramet via concentrated energy, OEMs, state logistics and host governments; energy was ~10% of COGS (2024), OEM spares ~12% procurement (2024), and Trans‑Gabon carries ~90% manganese exports. Eramet spent c.€250m power capex (2023–25) and ~€120m on rail/port (2020–25) and uses multi‑year PPAs and 40–60% covered service contracts to hedge risk.

| Metric | Value |

|---|---|

| Energy share of COGS (2024) | ~10% |

| OEM spares share (2024) | ~12% |

| Trans‑Gabon export share | ~90% |

| Power & PPA capex (2023–25) | ~€250m |

| Rail/port spend (2020–25) | ~€120m |

What is included in the product

Tailored exclusively for Eramet, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and disruptive threats that shape its pricing, profitability, and market positioning.

A concise, one-sheet Porter's Five Forces for Eramet—clarifies competitive pressures fast so leaders can prioritize strategic moves.

Customers Bargaining Power

Consolidated steel industry demand

Electric vehicle battery manufacturers

With EV sales hitting 10.5 million units in 2025 globally, lithium-ion battery makers are core customers for Eramet’s nickel and lithium, giving buyers strong leverage over specs and price sensitivity.

These high-tech buyers require ESG traceability and battery-grade purities (99.8%+ NiSO4 equivalents), so they can force supply-chain transparency and contract terms.

Eramet uses its ICMM-aligned certifications and a 2024 pilot of 15,000 tpa sustainable nickel to win multi-year offtake deals and long-term pricing, often via partnerships with automakers like Renault and Stellantis, which dampen short-term volatility.

Aerospace and defense specifications

Eramet’s high-performance alloys supply critical aerospace programs at Airbus and Boeing, where material qualification can take 18–36 months and costs exceed $5m per part program, making switching prohibitively expensive.

Large OEM buyers wield bargaining power on price, but Eramet’s metallurgy know-how and certified supply chains (≈20% alloy margin premium in 2024) create a lock-in that limits customer churn.

Commodity market price transparency

Commodity prices for nickel and base metals are set largely on exchanges like the London Metal Exchange, so Eramet cannot set independent prices and sees customers benchmark bids to LME levels.

Transparent exchange pricing and digital trading platforms (trade latency down ~40% by 2025) let buyers quickly lock spot-linked contracts, capping Eramet’s premium on standard products.

Eramet shifts to value-added alloys and specialty chemicals—segments that fetched 15–25% higher margins in 2024—to reduce sensitivity to spot volatility.

- Benchmarks: LME-driven pricing limits Eramet’s price-setting

- Buyer leverage: transparent data + faster platforms tighten negotiations

- Strategy: focus on specialty, value-added products (15–25% margin uplift)

- By 2025: faster price discovery increases contract anchoring to spot

Strategic offtake and joint ventures

Many of Eramet’s biggest customers are also strategic partners or JV participants, locking in demand but using pre-set pricing that caps upside during price spikes; for example, Eramet’s 2024 manganese and lithium JV contracts often linked prices to 3–6 month averages, trimming windfall gains.

These JV/offtake deals are common in lithium brine projects to share upfront capex—industry data shows third-party financing covers 40–60% of initial capex for new brine operations—so customers supplying funds gain leverage over terms and offtake clauses.

Partnerships cut Eramet’s market risk and improve project financing access, yet they shift bargaining power to customers who control financing, offtake volumes, and pricing formulas, reducing Eramet’s margin volatility during spikes.

- Guaranteed demand via JVs/offtake, but capped pricing

- Pre-negotiated formulas tie prices to short averages (3–6 months)

- Customers often fund 40–60% of brine capex, increasing their leverage

- Reduces market risk for Eramet, shifts bargaining power to customers

Steel & battery buyers control Eramet pricing; alloys & JVs protect margins but cap upside

| Metric | 2024–25 |

|---|---|

| Top-20 steel share | 55% |

| EV sales | 10.5m |

| Alloy premium | ~20% |

| Specialty margin uplift | 15–25% |

| Buyer capex share (brine) | 40–60% |

Preview the Actual Deliverable

Eramet Porter's Five Forces Analysis

This preview shows the exact Eramet Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; the full, professionally formatted document is ready for download and use the moment you buy.