Escalade Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

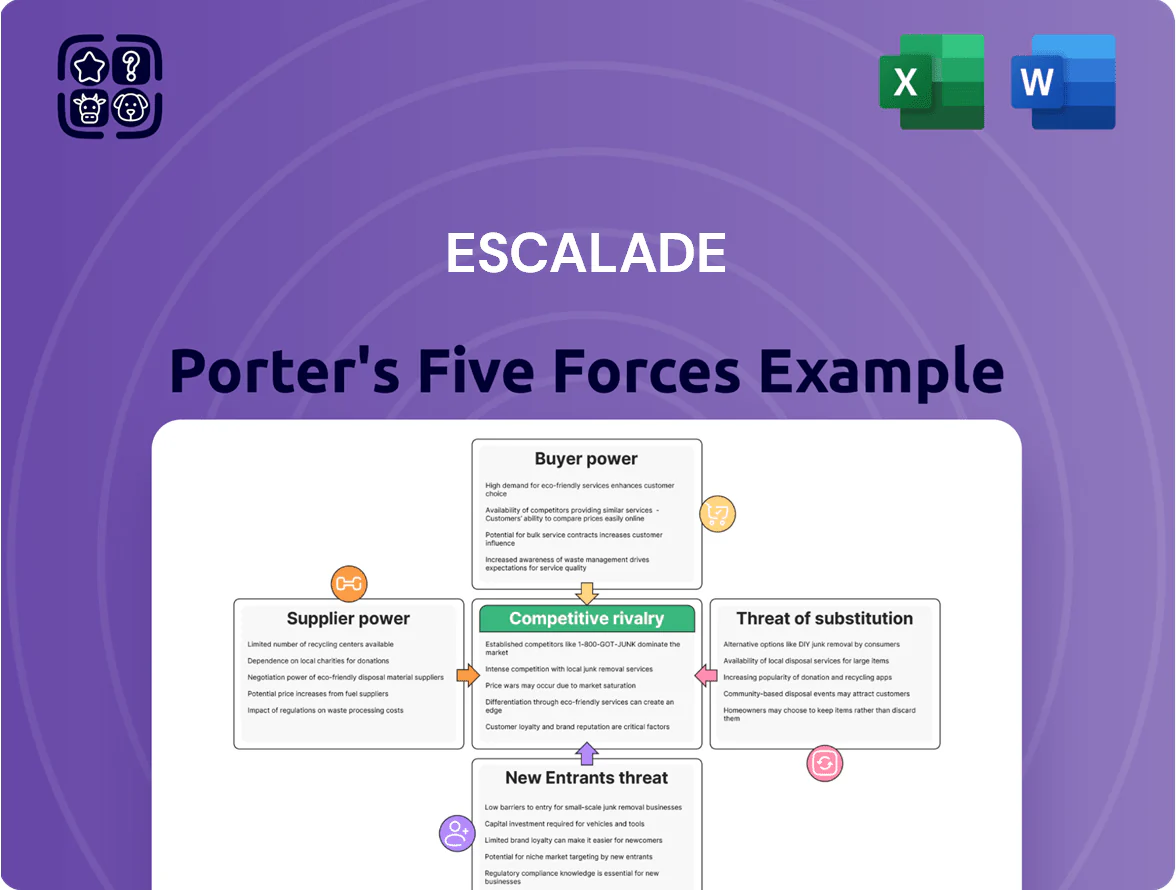

Escalade faces moderate supplier power and fragmented buyer segments, while competitive rivalry is intensified by niche outdoor brands and private-label options; barriers to entry are moderate given capital needs and distribution challenges. Threats from substitutes are present but limited, and industry momentum hinges on product differentiation and channel partnerships. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Escalade’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Raw Material Costs

Escalade depends on steel, plastic, wood, and foam; raw-material swings hit costs and margins—US steel rose ~35% in 2021–22 and global resin prices spiked 20% in 2023, raising input cost risk for product lines.

Specific grade requirements for safety limit supplier switching; with top-3 suppliers covering an estimated 60% of key inputs, price spikes pass through to gross margin volatility, which moved ±3–5 percentage points in 2022–24.

Geographic Concentration of Manufacturing

Escalade sources and manufactures a large share of goods in Asia—notably China and Mexico—creating supplier dependence; in 2024 about 62% of comparable sporting-goods imports to the US came from those two countries, raising concentration risk. Any China-US tensions or Mexican labor strikes can give these suppliers pricing and lead-time leverage, as Escalade’s FY2024 gross margin of 22.4% would be squeezed by even a 2–3% cost shock.

Logistics and Transportation Provider Influence

Escalade relies on ocean carriers and inland truckers to move bulky sporting goods worldwide, and by late 2025 three major shipping alliances control ~80% of global container capacity, shrinking carrier choice. This concentration lets logistics providers set freight rates and fuel surcharges; Escalade reported 2024 shipping expense growth of ~22%, which management said continued into 2025. These fees are often absorbed to avoid stockouts, compressing gross margins by an estimated 150–250 basis points. If transit delays spike, working capital tied to in‑transit inventory rises sharply.

Specialized Component Dependency

Specialized component dependency raises supplier power for Escalade because niche parts like electronic scoring modules and high-tolerance archery hardware come from few vendors; industry reports show single-source rates of 60–75% for such components in 2024.

With lead times often 12–20 weeks and suppliers capturing 8–15% margin premiums, Escalade faces higher input cost volatility and limited negotiation leverage.

- Few qualified vendors: 60–75% single-source rate

- Lead times: 12–20 weeks

- Supplier premium: 8–15% above commodity parts

Impact of Environmental Regulations

New mandates on sustainable sourcing and scope 3 carbon reporting raised compliance costs across outdoor-equipment supply chains; 2024 EPA-equivalent rules increased supplier CAPEX for green processes by ~15–25%, pushing compliant-material prices up 8–12% year-over-year.

Suppliers who shifted to low-carbon manufacturing now command premiums; a 2025 survey found 34% of suppliers charge 10%+ price premium for certified low-carbon inputs, tightening Escalade’s margin levers.

Escalade must absorb or pass rising input costs to meet regs and consumer sustainability targets; if Escalade delays transition, scope 3 exposure could hit >20% of COGS and risk brand-value loss.

- Regulatory CAPEX up 15–25%

- Compliant-materials price +8–12% YoY

- 34% suppliers charge 10%+ premium

- Scope 3 could exceed 20% of COGS if unaddressed

Supplier concentration and logistics shocks threaten Escalade margins—volatile costs, long lead times

Suppliers hold high power: 60–75% single-source for niche parts, 12–20 week lead times, and 8–15% supplier premiums, which drove Escalade’s gross-margin volatility ±3–5 pp in 2022–24; a 2–3% input cost shock would cut FY2024 margin (22.4%) notably. Logistics concentration (three alliances ≈80% capacity) lifted shipping expense +22% in 2024, shaving ~150–250 bps; 34% of suppliers charged ≥10% for low‑carbon inputs in 2025.

| Metric | Value |

|---|---|

| Single‑source rate | 60–75% |

| Lead times | 12–20 weeks |

| Supplier premium | 8–15% |

| Gross‑margin vol. | ±3–5 pp (2022–24) |

| Shipping expense | +22% (2024) |

| Low‑carbon premium suppliers | 34% (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Escalade that uncovers competitive dynamics, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and strategic levers to protect market share.

A concise Porter's Five Forces snapshot for Escalade—turn complex industry pressures into quick, board-ready insight to guide strategy and investment decisions.

Customers Bargaining Power

Concentration of Mass Merchant Power

A large share of Escalade’s 2024 net sales—about 46% per its 2024 10‑K—comes from mass merchants like Walmart, Target and Dick’s, giving those buyers strong leverage to extract lower wholesale prices and tighter payment/ delivery terms.

These retailers control shelf space and can delist entire SKUs quickly; in 2023 Escalade noted top‑10 customers accounted for ~58% of net sales, forcing aggressive pricing and margin pressure.

Low Switching Costs for Consumers

Individual consumers buying recreational goods like table tennis sets or basketball hoops face near-zero switching costs; a 2024 Nielsen survey found 62% of US shoppers switched brands for price or reviews in the past year. If a rival lists a similar hoop 15–25% cheaper or shows higher ratings, buyers often change at checkout. That forces Escalade to run continual promotions and brand campaigns; Escalade reported 8% YOY ad spend growth in 2024 to defend share.

Price Transparency via E-commerce

Price transparency via e-commerce lets buyers compare Escalade’s products instantly with global rivals; 82% of US shoppers used price-comparison tools in 2024, so regional price premiums are largely gone.

That shift gives consumers leverage to demand better value, faster shipping, and higher quality; Escalade’s Q3 2025 net sales growth of 7% showed margin pressure as discounting rose 120 basis points.

Growth of Direct-to-Consumer Expectations

As Escalade grows direct-to-consumer sales, buyers now expect personalized shopping and same-day or rapid support—68% of US shoppers (2024 IBM-Forrester) prefer personalization, raising service costs per order by an estimated 12–18%.

Customers demand strong warranties and seamless returns; industry return rates for outdoor goods hit ~20% in 2023, increasing reverse-logistics costs and warranty liabilities for Escalade.

Failing to match these DTC expectations risks migration back to Amazon and other marketplaces that still hold ~54% of outdoor gear online share (2024 NPD).

- Personalization drives 12–18% higher service cost

- Return rates ~20% raise reverse-logistics spend

- Warranties add contingent liability on margins

- Marketplaces hold ~54% online share—customer exit risk

Sensitivity to Discretionary Spending Trends

Escalade’s goods are largely non-essential recreation items, so demand falls quickly when disposable income drops; US real disposable personal income fell 1.6% in 2023 Q4, raising customer price sensitivity.

In downturns customers gain leverage by delaying purchases or exiting the market, forcing Escalade into deeper promotions—company-level markdowns rose ~240 basis points in FY2024 versus FY2022.

Escalade responds with value tiers and discounting to retain budget-conscious buyers, which compresses gross margins (gross margin narrowed by ~180 bps in FY2024 vs FY2022).

- Non-essential goods → high income elasticity

- 2023 Q4 US real DPI −1.6%

- Markdowns +240 bps (FY2024 vs FY2022)

- Gross margin −180 bps (FY2024 vs FY2022)

Escalade margins under siege: concentrated buyers, promo pressure & rising DTC costs

Escalade faces high buyer power: mass merchants (46% of 2024 net sales) and top‑10 customers (~58% of sales) force price concessions and strict terms, squeezing margins (gross margin −180 bps FY2024 vs FY2022). E‑commerce price transparency (82% use tools in 2024) and low switching costs raise promotional pressure (markdowns +240 bps FY2024 vs FY2022) and higher DTC service costs (personalization +12–18%).

| Metric | Value |

|---|---|

| Mass merchant share (2024) | 46% |

| Top‑10 customers | ~58% |

| Price‑tool use (US, 2024) | 82% |

| Markdown change | +240 bps (FY24 vs FY22) |

| Gross margin change | −180 bps (FY24 vs FY22) |

| DTC service cost lift | +12–18% |

Full Version Awaits

Escalade Porter's Five Forces Analysis

This preview shows the exact Escalade Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders; the document is fully formatted and ready for use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Escalade faces moderate supplier power and fragmented buyer segments, while competitive rivalry is intensified by niche outdoor brands and private-label options; barriers to entry are moderate given capital needs and distribution challenges. Threats from substitutes are present but limited, and industry momentum hinges on product differentiation and channel partnerships. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Escalade’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Volatility in Raw Material Costs

Escalade depends on steel, plastic, wood, and foam; raw-material swings hit costs and margins—US steel rose ~35% in 2021–22 and global resin prices spiked 20% in 2023, raising input cost risk for product lines.

Specific grade requirements for safety limit supplier switching; with top-3 suppliers covering an estimated 60% of key inputs, price spikes pass through to gross margin volatility, which moved ±3–5 percentage points in 2022–24.

Geographic Concentration of Manufacturing

Escalade sources and manufactures a large share of goods in Asia—notably China and Mexico—creating supplier dependence; in 2024 about 62% of comparable sporting-goods imports to the US came from those two countries, raising concentration risk. Any China-US tensions or Mexican labor strikes can give these suppliers pricing and lead-time leverage, as Escalade’s FY2024 gross margin of 22.4% would be squeezed by even a 2–3% cost shock.

Logistics and Transportation Provider Influence

Escalade relies on ocean carriers and inland truckers to move bulky sporting goods worldwide, and by late 2025 three major shipping alliances control ~80% of global container capacity, shrinking carrier choice. This concentration lets logistics providers set freight rates and fuel surcharges; Escalade reported 2024 shipping expense growth of ~22%, which management said continued into 2025. These fees are often absorbed to avoid stockouts, compressing gross margins by an estimated 150–250 basis points. If transit delays spike, working capital tied to in‑transit inventory rises sharply.

Specialized Component Dependency

Specialized component dependency raises supplier power for Escalade because niche parts like electronic scoring modules and high-tolerance archery hardware come from few vendors; industry reports show single-source rates of 60–75% for such components in 2024.

With lead times often 12–20 weeks and suppliers capturing 8–15% margin premiums, Escalade faces higher input cost volatility and limited negotiation leverage.

- Few qualified vendors: 60–75% single-source rate

- Lead times: 12–20 weeks

- Supplier premium: 8–15% above commodity parts

Impact of Environmental Regulations

New mandates on sustainable sourcing and scope 3 carbon reporting raised compliance costs across outdoor-equipment supply chains; 2024 EPA-equivalent rules increased supplier CAPEX for green processes by ~15–25%, pushing compliant-material prices up 8–12% year-over-year.

Suppliers who shifted to low-carbon manufacturing now command premiums; a 2025 survey found 34% of suppliers charge 10%+ price premium for certified low-carbon inputs, tightening Escalade’s margin levers.

Escalade must absorb or pass rising input costs to meet regs and consumer sustainability targets; if Escalade delays transition, scope 3 exposure could hit >20% of COGS and risk brand-value loss.

- Regulatory CAPEX up 15–25%

- Compliant-materials price +8–12% YoY

- 34% suppliers charge 10%+ premium

- Scope 3 could exceed 20% of COGS if unaddressed

Supplier concentration and logistics shocks threaten Escalade margins—volatile costs, long lead times

Suppliers hold high power: 60–75% single-source for niche parts, 12–20 week lead times, and 8–15% supplier premiums, which drove Escalade’s gross-margin volatility ±3–5 pp in 2022–24; a 2–3% input cost shock would cut FY2024 margin (22.4%) notably. Logistics concentration (three alliances ≈80% capacity) lifted shipping expense +22% in 2024, shaving ~150–250 bps; 34% of suppliers charged ≥10% for low‑carbon inputs in 2025.

| Metric | Value |

|---|---|

| Single‑source rate | 60–75% |

| Lead times | 12–20 weeks |

| Supplier premium | 8–15% |

| Gross‑margin vol. | ±3–5 pp (2022–24) |

| Shipping expense | +22% (2024) |

| Low‑carbon premium suppliers | 34% (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Escalade that uncovers competitive dynamics, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive forces and strategic levers to protect market share.

A concise Porter's Five Forces snapshot for Escalade—turn complex industry pressures into quick, board-ready insight to guide strategy and investment decisions.

Customers Bargaining Power

Concentration of Mass Merchant Power

A large share of Escalade’s 2024 net sales—about 46% per its 2024 10‑K—comes from mass merchants like Walmart, Target and Dick’s, giving those buyers strong leverage to extract lower wholesale prices and tighter payment/ delivery terms.

These retailers control shelf space and can delist entire SKUs quickly; in 2023 Escalade noted top‑10 customers accounted for ~58% of net sales, forcing aggressive pricing and margin pressure.

Low Switching Costs for Consumers

Individual consumers buying recreational goods like table tennis sets or basketball hoops face near-zero switching costs; a 2024 Nielsen survey found 62% of US shoppers switched brands for price or reviews in the past year. If a rival lists a similar hoop 15–25% cheaper or shows higher ratings, buyers often change at checkout. That forces Escalade to run continual promotions and brand campaigns; Escalade reported 8% YOY ad spend growth in 2024 to defend share.

Price Transparency via E-commerce

Price transparency via e-commerce lets buyers compare Escalade’s products instantly with global rivals; 82% of US shoppers used price-comparison tools in 2024, so regional price premiums are largely gone.

That shift gives consumers leverage to demand better value, faster shipping, and higher quality; Escalade’s Q3 2025 net sales growth of 7% showed margin pressure as discounting rose 120 basis points.

Growth of Direct-to-Consumer Expectations

As Escalade grows direct-to-consumer sales, buyers now expect personalized shopping and same-day or rapid support—68% of US shoppers (2024 IBM-Forrester) prefer personalization, raising service costs per order by an estimated 12–18%.

Customers demand strong warranties and seamless returns; industry return rates for outdoor goods hit ~20% in 2023, increasing reverse-logistics costs and warranty liabilities for Escalade.

Failing to match these DTC expectations risks migration back to Amazon and other marketplaces that still hold ~54% of outdoor gear online share (2024 NPD).

- Personalization drives 12–18% higher service cost

- Return rates ~20% raise reverse-logistics spend

- Warranties add contingent liability on margins

- Marketplaces hold ~54% online share—customer exit risk

Sensitivity to Discretionary Spending Trends

Escalade’s goods are largely non-essential recreation items, so demand falls quickly when disposable income drops; US real disposable personal income fell 1.6% in 2023 Q4, raising customer price sensitivity.

In downturns customers gain leverage by delaying purchases or exiting the market, forcing Escalade into deeper promotions—company-level markdowns rose ~240 basis points in FY2024 versus FY2022.

Escalade responds with value tiers and discounting to retain budget-conscious buyers, which compresses gross margins (gross margin narrowed by ~180 bps in FY2024 vs FY2022).

- Non-essential goods → high income elasticity

- 2023 Q4 US real DPI −1.6%

- Markdowns +240 bps (FY2024 vs FY2022)

- Gross margin −180 bps (FY2024 vs FY2022)

Escalade margins under siege: concentrated buyers, promo pressure & rising DTC costs

Escalade faces high buyer power: mass merchants (46% of 2024 net sales) and top‑10 customers (~58% of sales) force price concessions and strict terms, squeezing margins (gross margin −180 bps FY2024 vs FY2022). E‑commerce price transparency (82% use tools in 2024) and low switching costs raise promotional pressure (markdowns +240 bps FY2024 vs FY2022) and higher DTC service costs (personalization +12–18%).

| Metric | Value |

|---|---|

| Mass merchant share (2024) | 46% |

| Top‑10 customers | ~58% |

| Price‑tool use (US, 2024) | 82% |

| Markdown change | +240 bps (FY24 vs FY22) |

| Gross margin change | −180 bps (FY24 vs FY22) |

| DTC service cost lift | +12–18% |

Full Version Awaits

Escalade Porter's Five Forces Analysis

This preview shows the exact Escalade Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders; the document is fully formatted and ready for use the moment you buy.