Esker Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Esker faces moderate supplier power and growing buyer sophistication, while digital incumbents and niche SaaS entrants tighten competitive rivalry; substitutes and regulatory shifts pose manageable but notable risks to margins and growth. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Esker’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure and Hyperscaler Dependency

Esker depends on Microsoft Azure and AWS to host its AI-driven platform, creating supplier power since moving clouds is technically complex and costly; multi-cloud migration can cost 10–20% of annual cloud spend and take 6–12 months. As hyperscalers controlled ~70% of global cloud IaaS/PaaS revenue in 2024–25, Esker faces standardized pricing and SLAs with limited negotiation room. Any supplier price hike or outage risks direct margin and service impacts.

Specialized AI and LLM Developers

Suppliers of proprietary LLMs and specialized AI chips can squeeze Esker via licensing fees and access limits—OpenAI-style models saw enterprise price rises of ~20% in 2024 and Nvidia’s data-center GPU shortages pushed prices up ~15% in H2 2023, so foundational tech is a material cost/availability risk. Esker reduces this by building proprietary application layers and fine-tuned models, but key dependencies on external LLM providers and chip vendors remain.

Highly Skilled Technical Talent

The market for AI engineers and cloud architects remained extremely competitive at end-2025, with global demand outstripping supply and median US total compensation for senior AI engineers around $280k–$320k per year (H1 2025 data).

These specialists supply core intellectual property and operational continuity for Esker’s cloud-based automation platform, so their bargaining power pushes higher pay, equity, and hybrid work terms.

Shortages slow product roadmaps: a 2024–25 industry survey found 62% of SaaS firms reported hiring delays that extended feature release timelines by 3–9 months, constraining Esker’s innovation velocity.

Data Security and Compliance Auditors

As a global provider handling sensitive financial data, Esker must comply with evolving international regulations such as GDPR (EU) and SOC 2 (US), plus local standards like Brazil’s LGPD; noncompliance risks fines — GDPR fines hit 1.8 billion euros in 2023 across cases.

Security and compliance auditors who issue certifications hold strong bargaining power because their stamps are required for enterprise contracts; 78% of Fortune 500 firms demand third-party attestations in RFPs (2024 survey).

Without these independent validations, Esker would lose credibility and access to large clients, directly affecting ARR and renewal rates; enterprise deals often move 30–50% slower without certifications.

- GDPR fines: 1.8B euros (2023)

- 78% of Fortune 500 require third-party attestations (2024)

- Enterprise deal delays 30–50% without certifications

Financial Data Feed Providers

Esker depends on real-time bank and financial-institution feeds for payment processing and reconciliation; in 2025 about 62% of enterprise payments relied on API-based bank feeds, raising supplier leverage.

These financial entities set API standards and SLAs, so integration costs or a 10–25% fee hike directly raises Esker’s operating costs and reduces margins.

Any outage or data throttling—bank incidents rose 18% in 2024—would hurt Esker’s service availability and customer retention.

- 62% enterprise API reliance in 2025

- 10–25% potential fee impact on costs

- 18% rise in bank incidents in 2024

Supply-side squeeze: hyperscalers, chips, talent and APIs threaten Esker margins

Supplier power is high: hyperscalers (~70% IaaS/PaaS share in 2024–25) and LLM/chip vendors drove ~15–20% cost shocks (2023–24); AI talent median senior pay $280k–$320k (H1 2025) and 62% of firms faced hiring delays lengthening roadmaps 3–9 months; compliance auditors and bank API providers (62% API reliance in 2025) add pricing and availability risk to Esker’s margins.

| Metric | Value |

|---|---|

| Hyperscaler share | ~70% |

| LLM/GPU cost shock | 15–20% |

| Senior AI pay (US) | $280k–$320k |

| API reliance | 62% |

What is included in the product

Tailored Porter's Five Forces analysis for Esker that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its market share, with strategic commentary and editable output for reports and decks.

Clear, one-sheet Porter’s Five Forces for Esker—instantly spot where bargaining power and competitive threats hit hardest, ideal for rapid strategic decisions and slide-ready summaries.

Customers Bargaining Power

High Switching Costs and ERP Integration

Once Esker is embedded into core ERPs like SAP or Oracle, migration costs—often 2000+ integration hours and $150k–$500k per large account—make switching nearly prohibitive, lowering customers’ immediate bargaining power.

Deep technical ties give Esker leverage at renewals: median contract renewal uplift for integrated SaaS vendors is ~8%–12% in 2024, so Esker can press for price or scope changes.

By end-2025, AI-driven workflow complexity—Esker reports 35% of automation tied to ML models—further locks clients into its ecosystem, raising effective switching costs and reducing churn risk.

Concentrated Demand from Large Enterprises

Large multinationals account for roughly 40% of Esker’s 2024 revenue (€199.6m total), giving them volume-based leverage to push prices down and demand discounts. These buyers run strict RFPs and evaluate multiple global vendors, shortening vendor lock-in; in 2024 enterprise renewals rose 7% but new large-account wins slowed. Their budgets and IT teams let them insist on custom features and tighter SLAs, materially boosting their bargaining power.

Availability of Alternative SaaS Solutions

Customers face many alternatives: the financial process automation market had ~USD 6.8bn in 2024 and a 12% CAGR, with niche vendors and ERP suites like Basware (procure-to-pay) and Coupa (spend management) increasing pressure on Esker’s pricing and roadmap.

If Esker’s AI features don’t show clear ROI versus peers, large buyers—who typically lock budgets for 3–5 years—can threaten migration during renewal windows; churn risk rises if switching costs fall below ~15% of annual contract value.

Transparency in SaaS Pricing Models

By late 2025, SaaS pricing transparency has risen sharply: procurement teams use benchmarking tools showing median O2C (order-to-cash) automation prices around $45/user/month and P2P (procure-to-pay) at $3,500/month per supplier module, so Esker faces buyers armed with competitive quotes and clear TCO benchmarks. This symmetry lets customers push for discounts, shorter SLAs, and outcome-based pricing tied to invoice volumes, lowering Esker’s pricing power.

- Median O2C price: $45/user/month (2025)

- Median P2P module: $3,500/month per supplier (2025)

- Benchmark tools adoption >60% of large buyers (2025)

- Outcome-based pricing requests up 30% YoY (2024–25)

Focus on Measurable ROI and Efficiency

Customers now demand measurable ROI and efficiency before expanding Esker; 2024 vendor surveys show 72% of B2B buyers require quantified cost-savings metrics, raising buyer leverage.

If Esker cannot prove clear ROI from its AI-driven invoice and order automation—typical claims: 30–60% manual time saved—clients may cut seat counts or downgrade, pressuring pricing and retention.

This performance-first stance shifts power to buyers who control budgets and can push for performance SLAs, usage-based fees, or competitive pilots.

- 72% of B2B buyers require quantified savings (2024)

- Esker target claims: 30–60% time savings on processes

- Failure to prove ROI → downgrades, seat reductions

- Buyers push for SLAs, trials, usage-based pricing

High switching costs mute churn, but buyers’ ROI demands and benchmarks amplify pricing pressure

Customers hold moderate-to-high bargaining power: high switching costs from ERP integration (2000+ hrs, $150k–$500k) and Esker’s 2024 revenue mix (40% large multinationals of €199.6m) reduce churn, but benchmarked SaaS pricing (O2C $45/user/mo; P2P $3,500/supplier/mo), rising procurement tools (>60% adoption), and demand for ROI (72% require quantified savings) let buyers force discounts, SLAs, and outcome pricing.

| Metric | Value (2024–25) |

|---|---|

| ERP integration cost | $150k–$500k / 2000+ hrs |

| Esker revenue from large accounts | 40% of €199.6m |

| O2C price | $45/user/mo (2025) |

| P2P module | $3,500/supplier/mo (2025) |

| Procurement benchmark tools | >60% adoption (2025) |

| Buyers needing ROI | 72% (2024) |

Preview Before You Purchase

Esker Porter's Five Forces Analysis

This preview shows the exact Esker Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

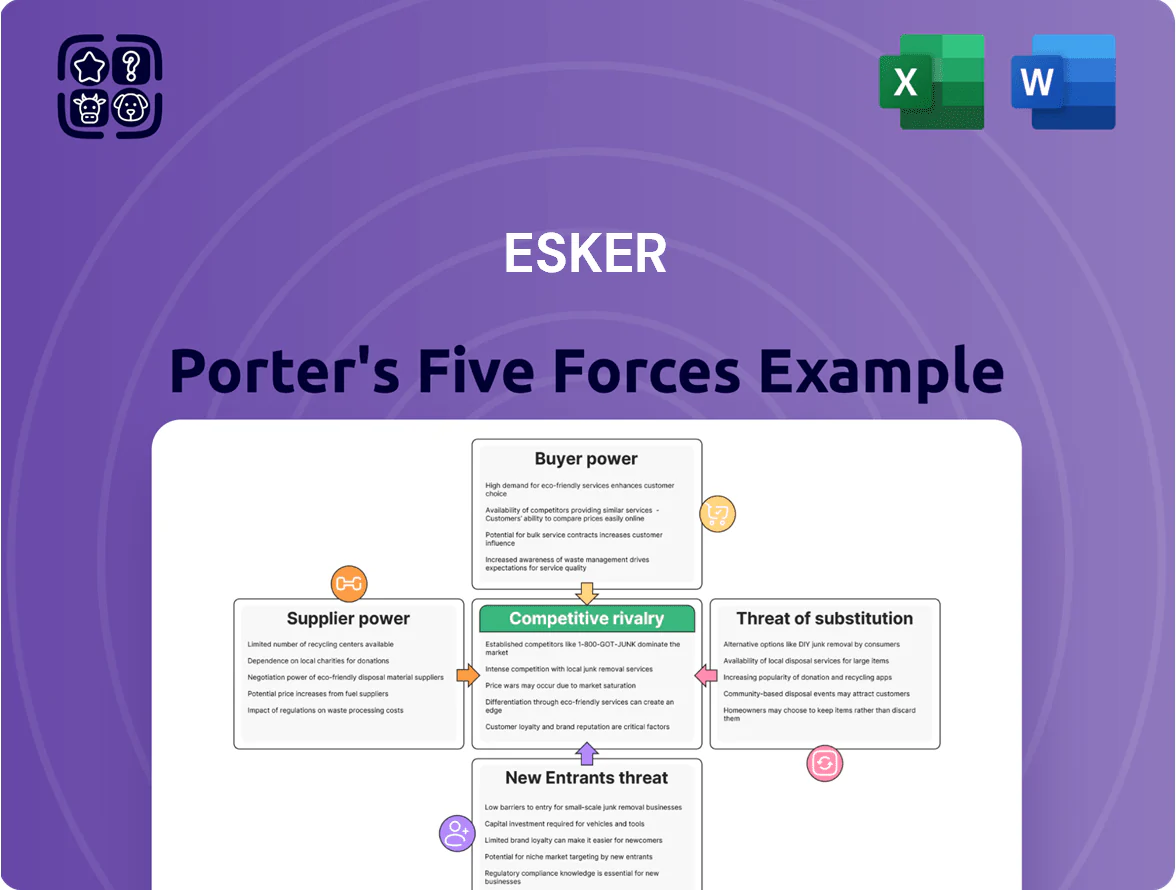

What you see is the final deliverable: a complete, ready-to-use strategic assessment covering supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Esker faces moderate supplier power and growing buyer sophistication, while digital incumbents and niche SaaS entrants tighten competitive rivalry; substitutes and regulatory shifts pose manageable but notable risks to margins and growth. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Esker’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cloud Infrastructure and Hyperscaler Dependency

Esker depends on Microsoft Azure and AWS to host its AI-driven platform, creating supplier power since moving clouds is technically complex and costly; multi-cloud migration can cost 10–20% of annual cloud spend and take 6–12 months. As hyperscalers controlled ~70% of global cloud IaaS/PaaS revenue in 2024–25, Esker faces standardized pricing and SLAs with limited negotiation room. Any supplier price hike or outage risks direct margin and service impacts.

Specialized AI and LLM Developers

Suppliers of proprietary LLMs and specialized AI chips can squeeze Esker via licensing fees and access limits—OpenAI-style models saw enterprise price rises of ~20% in 2024 and Nvidia’s data-center GPU shortages pushed prices up ~15% in H2 2023, so foundational tech is a material cost/availability risk. Esker reduces this by building proprietary application layers and fine-tuned models, but key dependencies on external LLM providers and chip vendors remain.

Highly Skilled Technical Talent

The market for AI engineers and cloud architects remained extremely competitive at end-2025, with global demand outstripping supply and median US total compensation for senior AI engineers around $280k–$320k per year (H1 2025 data).

These specialists supply core intellectual property and operational continuity for Esker’s cloud-based automation platform, so their bargaining power pushes higher pay, equity, and hybrid work terms.

Shortages slow product roadmaps: a 2024–25 industry survey found 62% of SaaS firms reported hiring delays that extended feature release timelines by 3–9 months, constraining Esker’s innovation velocity.

Data Security and Compliance Auditors

As a global provider handling sensitive financial data, Esker must comply with evolving international regulations such as GDPR (EU) and SOC 2 (US), plus local standards like Brazil’s LGPD; noncompliance risks fines — GDPR fines hit 1.8 billion euros in 2023 across cases.

Security and compliance auditors who issue certifications hold strong bargaining power because their stamps are required for enterprise contracts; 78% of Fortune 500 firms demand third-party attestations in RFPs (2024 survey).

Without these independent validations, Esker would lose credibility and access to large clients, directly affecting ARR and renewal rates; enterprise deals often move 30–50% slower without certifications.

- GDPR fines: 1.8B euros (2023)

- 78% of Fortune 500 require third-party attestations (2024)

- Enterprise deal delays 30–50% without certifications

Financial Data Feed Providers

Esker depends on real-time bank and financial-institution feeds for payment processing and reconciliation; in 2025 about 62% of enterprise payments relied on API-based bank feeds, raising supplier leverage.

These financial entities set API standards and SLAs, so integration costs or a 10–25% fee hike directly raises Esker’s operating costs and reduces margins.

Any outage or data throttling—bank incidents rose 18% in 2024—would hurt Esker’s service availability and customer retention.

- 62% enterprise API reliance in 2025

- 10–25% potential fee impact on costs

- 18% rise in bank incidents in 2024

Supply-side squeeze: hyperscalers, chips, talent and APIs threaten Esker margins

Supplier power is high: hyperscalers (~70% IaaS/PaaS share in 2024–25) and LLM/chip vendors drove ~15–20% cost shocks (2023–24); AI talent median senior pay $280k–$320k (H1 2025) and 62% of firms faced hiring delays lengthening roadmaps 3–9 months; compliance auditors and bank API providers (62% API reliance in 2025) add pricing and availability risk to Esker’s margins.

| Metric | Value |

|---|---|

| Hyperscaler share | ~70% |

| LLM/GPU cost shock | 15–20% |

| Senior AI pay (US) | $280k–$320k |

| API reliance | 62% |

What is included in the product

Tailored Porter's Five Forces analysis for Esker that uncovers competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its market share, with strategic commentary and editable output for reports and decks.

Clear, one-sheet Porter’s Five Forces for Esker—instantly spot where bargaining power and competitive threats hit hardest, ideal for rapid strategic decisions and slide-ready summaries.

Customers Bargaining Power

High Switching Costs and ERP Integration

Once Esker is embedded into core ERPs like SAP or Oracle, migration costs—often 2000+ integration hours and $150k–$500k per large account—make switching nearly prohibitive, lowering customers’ immediate bargaining power.

Deep technical ties give Esker leverage at renewals: median contract renewal uplift for integrated SaaS vendors is ~8%–12% in 2024, so Esker can press for price or scope changes.

By end-2025, AI-driven workflow complexity—Esker reports 35% of automation tied to ML models—further locks clients into its ecosystem, raising effective switching costs and reducing churn risk.

Concentrated Demand from Large Enterprises

Large multinationals account for roughly 40% of Esker’s 2024 revenue (€199.6m total), giving them volume-based leverage to push prices down and demand discounts. These buyers run strict RFPs and evaluate multiple global vendors, shortening vendor lock-in; in 2024 enterprise renewals rose 7% but new large-account wins slowed. Their budgets and IT teams let them insist on custom features and tighter SLAs, materially boosting their bargaining power.

Availability of Alternative SaaS Solutions

Customers face many alternatives: the financial process automation market had ~USD 6.8bn in 2024 and a 12% CAGR, with niche vendors and ERP suites like Basware (procure-to-pay) and Coupa (spend management) increasing pressure on Esker’s pricing and roadmap.

If Esker’s AI features don’t show clear ROI versus peers, large buyers—who typically lock budgets for 3–5 years—can threaten migration during renewal windows; churn risk rises if switching costs fall below ~15% of annual contract value.

Transparency in SaaS Pricing Models

By late 2025, SaaS pricing transparency has risen sharply: procurement teams use benchmarking tools showing median O2C (order-to-cash) automation prices around $45/user/month and P2P (procure-to-pay) at $3,500/month per supplier module, so Esker faces buyers armed with competitive quotes and clear TCO benchmarks. This symmetry lets customers push for discounts, shorter SLAs, and outcome-based pricing tied to invoice volumes, lowering Esker’s pricing power.

- Median O2C price: $45/user/month (2025)

- Median P2P module: $3,500/month per supplier (2025)

- Benchmark tools adoption >60% of large buyers (2025)

- Outcome-based pricing requests up 30% YoY (2024–25)

Focus on Measurable ROI and Efficiency

Customers now demand measurable ROI and efficiency before expanding Esker; 2024 vendor surveys show 72% of B2B buyers require quantified cost-savings metrics, raising buyer leverage.

If Esker cannot prove clear ROI from its AI-driven invoice and order automation—typical claims: 30–60% manual time saved—clients may cut seat counts or downgrade, pressuring pricing and retention.

This performance-first stance shifts power to buyers who control budgets and can push for performance SLAs, usage-based fees, or competitive pilots.

- 72% of B2B buyers require quantified savings (2024)

- Esker target claims: 30–60% time savings on processes

- Failure to prove ROI → downgrades, seat reductions

- Buyers push for SLAs, trials, usage-based pricing

High switching costs mute churn, but buyers’ ROI demands and benchmarks amplify pricing pressure

Customers hold moderate-to-high bargaining power: high switching costs from ERP integration (2000+ hrs, $150k–$500k) and Esker’s 2024 revenue mix (40% large multinationals of €199.6m) reduce churn, but benchmarked SaaS pricing (O2C $45/user/mo; P2P $3,500/supplier/mo), rising procurement tools (>60% adoption), and demand for ROI (72% require quantified savings) let buyers force discounts, SLAs, and outcome pricing.

| Metric | Value (2024–25) |

|---|---|

| ERP integration cost | $150k–$500k / 2000+ hrs |

| Esker revenue from large accounts | 40% of €199.6m |

| O2C price | $45/user/mo (2025) |

| P2P module | $3,500/supplier/mo (2025) |

| Procurement benchmark tools | >60% adoption (2025) |

| Buyers needing ROI | 72% (2024) |

Preview Before You Purchase

Esker Porter's Five Forces Analysis

This preview shows the exact Esker Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy.

What you see is the final deliverable: a complete, ready-to-use strategic assessment covering supplier power, buyer power, competitive rivalry, threat of substitution, and barriers to entry.